Does the 15-Month Wait-Out Period for Private Property Right-Sizers Still Make Sense?

- Stanley Lim

- 7 min read

- Blog

- 5 Jun 2025

As of late May this year, fresh news has emerged that the Singapore Government might consider reviewing or even removing the 15-month wait-out period imposed on private property right-sizers who want to purchase a resale HDB flat.

During a recent visit to the Toa Payoh Ridge Build-to-Order (BTO) project, newly-appointed Minister for National Development Chee Hong Tat told reporters that the authorities would be open to the idea of a rule change “when the situation improves and resale flat prices begin to moderate.”

The 15-month wait-out period was first introduced as a temporary cooling measure in September 2022, aiming to curb demand from private property right-sizers amid rising resale HDB prices. Since then, the HDB Resale Price Index (RPI) has recorded a slower 1.6% quarterly growth in the first quarter of 2025, which Minister Chee pointed out as a possible sign of moderation.

Looking further ahead, the possibility of removing the 15-month wait-out period raises several questions: What could happen to the HDB resale market next? Is the rule still relevant in today’s market? Below, we share some thoughts on these matters.

But first, how did the resale HDB market adjust after the 15-month wait-out period was implemented?

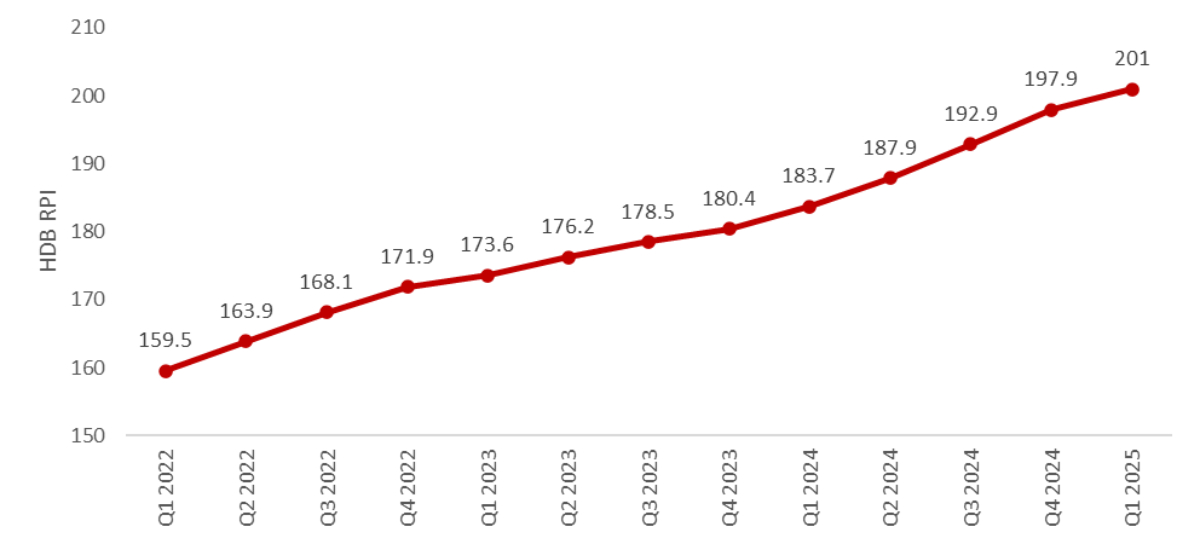

Chart 1: HDB Resale Price Index from 1Q 2023 to 1Q 2025

When examining movements in the HDB RPI after the 15-month wait-out period was implemented in 3Q 2022, it is clear that the rule had a noticeable effect on the secondary market. Although the HDB RPI continued to rise from 168.1 in 3Q 2022 to 173.6 in 1Q 2023, its rate of growth slowed markedly, with quarterly gains shrinking sharply from 2.6% to just 1.0% over the course of six months.

The accompanying decline in resale HDB transaction volumes – from 7,546 to 6,979 units – further supports the notion that the wait-out period had a moderating effect on flat demand from private property right-sizers during this period.

Table 1: HDB Resale Price Index and transaction volume by quarter

However, after the initial 15-month period following the introduction of the wait-out period in September 2022, eligible private property right-sizers were once again permitted to re-enter the secondary HDB market.

This influx of buyers resulted in a noticeable resurgence in both transaction volume and price growth of resale HDB flats. In 1Q 2024, resale transactions increased to 7,068 units, while the HDB RPI recorded a 1.8% q-o-q increase – the steepest quarterly price growth noted since 1Q 2023.

Subsequently, in 2Q 2024, the HDB RPI experienced a further quarterly increase of 2.3%. This is close to the 2.6% q-o-q jump recorded in 3Q 2022, just before the implementation of the wait-out rule.

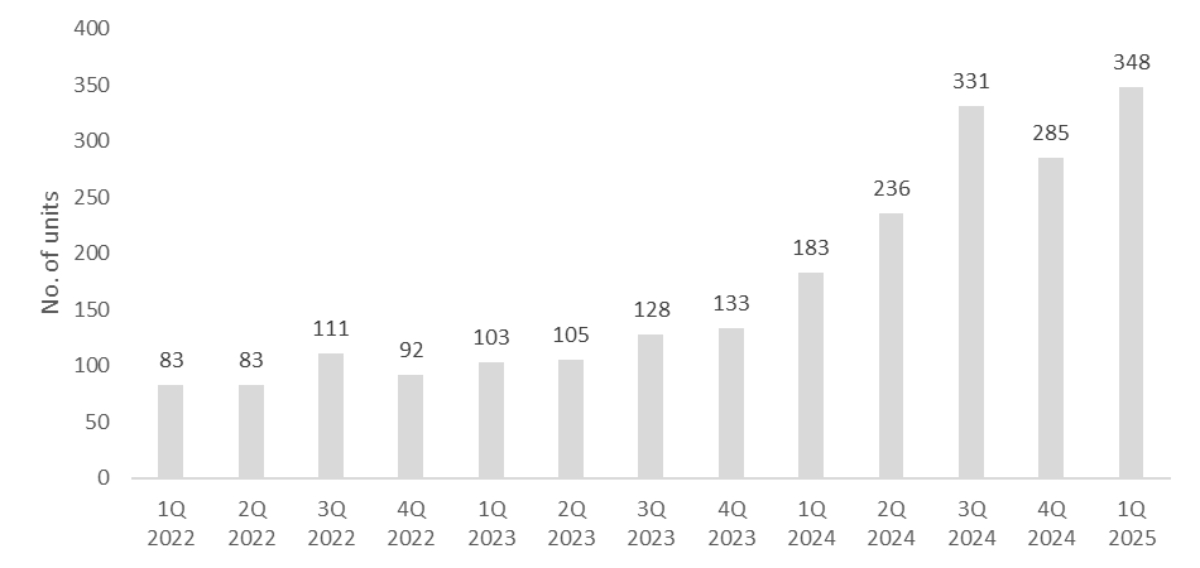

Chart 2: Volume of million-dollar HDB flats by quarter

This rebound pattern was also mirrored in the number of million-dollar HDB flat transactions – another useful yardstick for assessing the wait-out period’s effectiveness in tempering the resale market.

Following the rule’s introduction, million-dollar flat transactions fell from 111 units in 3Q 2022 to 92 units in 4Q 2022 before staying stable for most of the subsequent quarters.

However, this trend reversed direction over a year later. 1Q 2024 saw the biggest surge in the number of million-dollar flats sold in a quarter, with 183 such transactions—or double the 92 units recorded in 4Q 2022.

This surge in million-dollar HDB resale transactions shows little signs of slowing. As of May 2025, the year-to-date number of million-dollar resale transactions stands at 254 units for 4-room flats and 368 for 5-room flats. This is a notable increase compared to a year ago, with 4-room and 5-room units accounting for 93 and 229 transactions, respectively, from January to May 2024.

Overall, these ongoing increases in both million-dollar HDB flats and general resale prices present a sobering picture: the wait-out period likely experienced peak effectiveness only during its initial 15-month window.

What could happen to the HDB resale market if the 15-month wait-out period is removed?

With the resale HDB market already witnessing a growing number of million-dollar flats, there is little justification for removing the 15-month wait-out period. Doing so would spark a renewed surge in resale HDB prices, thus undermining the rule’s original purpose of keeping the secondary market in check.

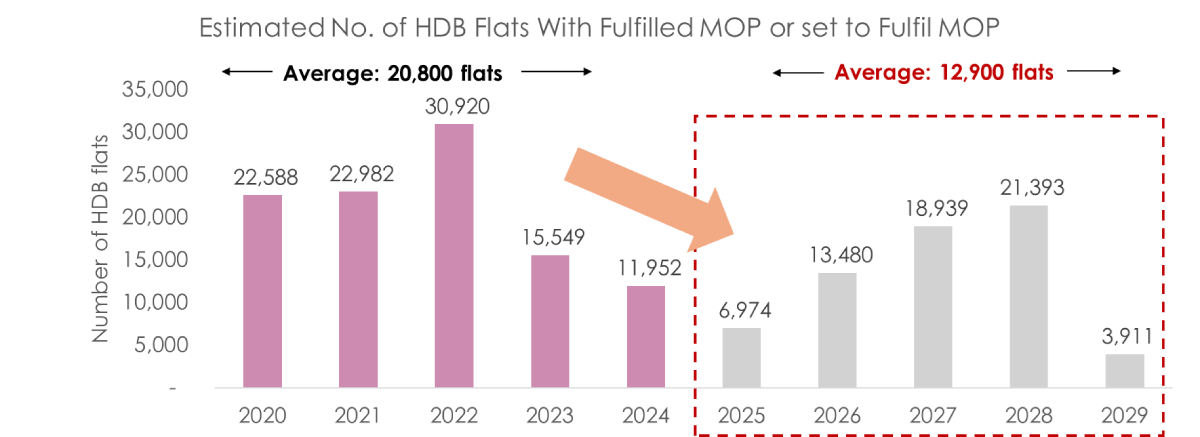

Chart 3: Estimated volume of HDB flats that have met or will meet their MOP

Market demand has also outpaced the available supply of HDB flats fresh out of their 5-year Minimum Occupation Period (MOP), leading to more intense competition in the secondary HDB market. This trend coincides with a shrinking number of HDB flats exiting their MOP, which has been steadily declining since 2022.

In 2022, 30,920 flats were estimated to have reached the end of their MOP, but this is expected to fall to a significant low of 6,974 units in 2025. Such a steep step-down in fresh resale inventory will likely exacerbate scarcity and existing price pressures, especially as demand from upgraders and right-sizers remains firm within the secondary HDB market.

At the same time, a growing bifurcation is emerging in the resale market where recently MOP-ed flats in desirable locations are seeing faster price appreciation than their older counterparts. For instance, in popular towns near the city fringe (e.g. Toa Payoh, Central Area), it is possible to see newer 4-room resale flats commanding double the price of older flats of equal size.

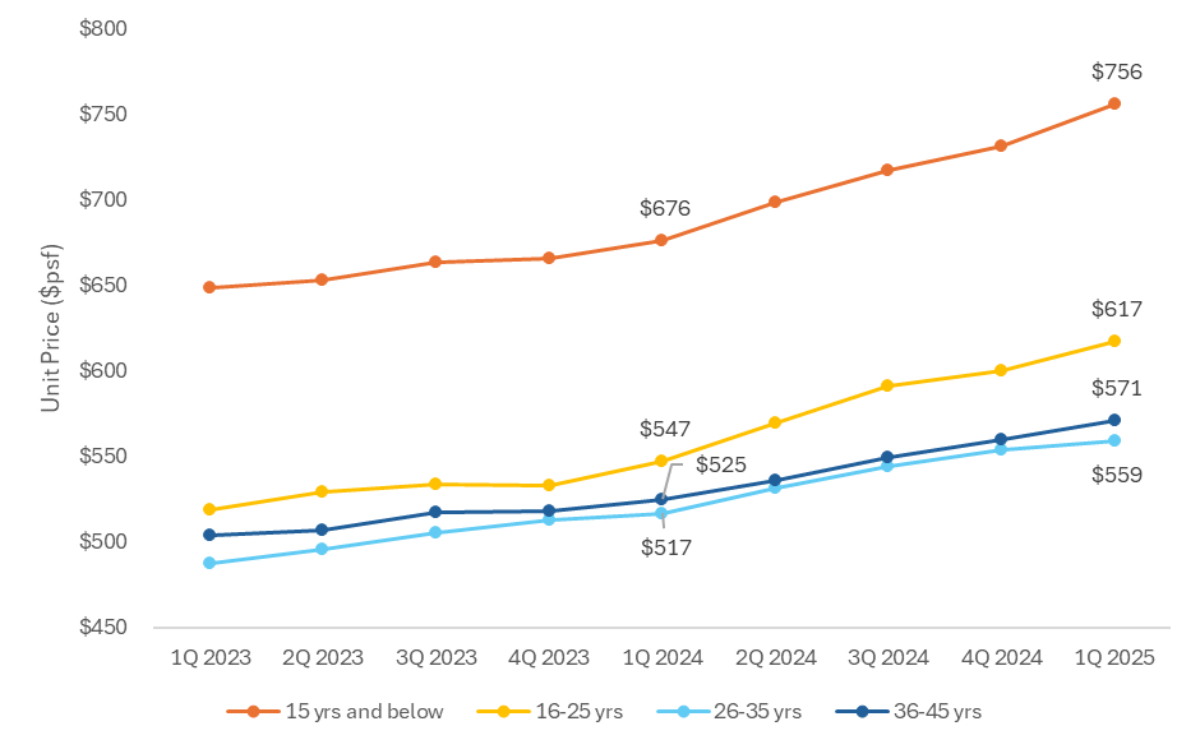

Table 2: Unit price appreciation of ‘younger’ and ‘older’ HDB flats up to 1Q 2025

This gap is further accentuated when looking at the annual price growth of HDB resale flats across different age brackets. Based on a year-on-year comparison of average unit prices as of 1Q 2025, younger resale flats aged “15 years and below” and “16 to 25 years” recorded sharper gains, with growth rates of 11.8% ($676 psf to $756 psf) and 12.8% ($547 psf to $617 psf) respectively.

In contrast, older flats in the “26 to 35 years” and “36 to 45 years” categories saw gentler growth, with unit prices rising by 8.2% ($525 psf to $571 psf) and 8.8% ($517 psf to $559 psf) on the year.

In turn, these divergences in pricing and appreciation rates between newer and older HDB flats is likely due to growing homebuyer awareness about lease decay concerns, leading them to opt for newer units even at a premium. This preference is also anticipated to sustain steady price appreciation in the secondary market, even with the slower gains of older flats moderating the appreciation of newly MOP-ed ones.

So, does the 15-month wait-out period still make sense in today’s context?

While its effectiveness has likely waned, the 15-month wait-out period remains relevant for moderating buying activity and keeping resale HDB prices in check. This perspective is warranted as private homeowners will represent a continuous pool for right-sizing and subsequent demand, even with the wait-out period in effect.

In light of current economic uncertainty, there might be a case for increased flexibility. For instance, the Government could consider implementing buying stipulations for private property right-sizers based on lease tenure. In turn, this would involve restricting HDB purchases by said right-sizers to units with shorter remaining leases.

Such a measure could be a potential solution as it would give private homeowners below the age of 55 the opportunity to secure a replacement home without having to complete the wait-out period. But at the same time, this would prevent HDB resale flat prices from rising too sharply as right-sizer demand would be channelled towards older homes with more moderated price growth, rather than recently MOP-ed flats that typically experience faster appreciation.

Addressing resale market pressures will also require meaningful supply-side intervention. For instance, efforts to deliver Build-To-Order (BTO) flats with shorter waiting periods could effectively divert first-timer demand towards the BTO market and away from the resale segment.

When combined with a refined wait-out policy, such housing supply measures should hopefully provide the necessary breathing room for the resale HDB market to maintain stable and sustainable growth in the long term.

I confirm that I have read theprivacy policy and allow my information to be shared with this agent who may contact me later.