1H 2025 Landed Shophouse Report: Shophouse Market Slows Amid Higher Prices and Heightened Economic Uncertainty

- Egan Mah Jixiang

- 5 min read

- Research

- 1 Sep 2025

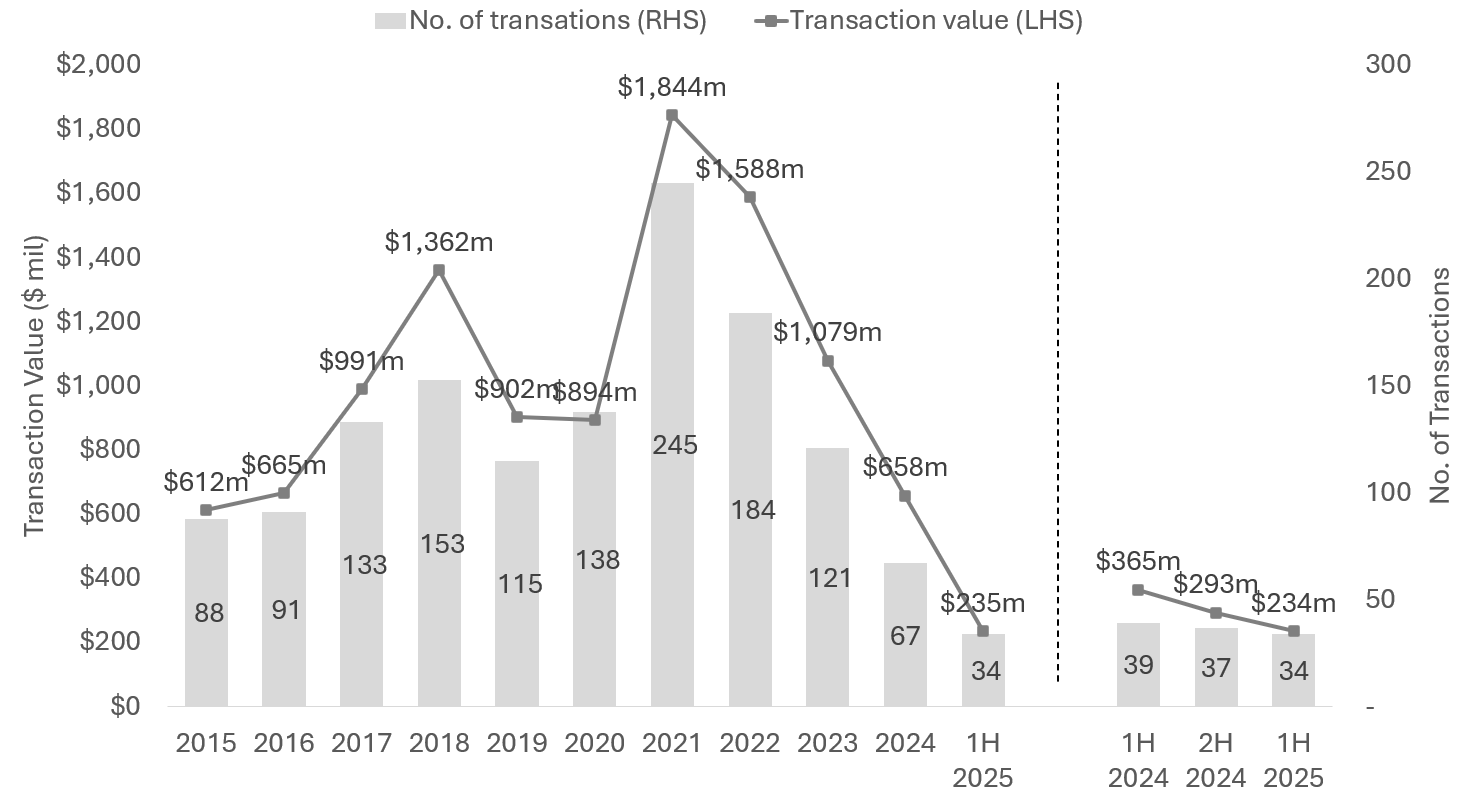

The landed shophouse market further weakened in 1H 2025, with only 34 transactions amounting to $234.7 million. This is a decline from 37 transactions worth $292.6 million in 2H 2024, and it represents the lowest number of transactions in a half-yearly period since 2H 1998, when just 31 units were transacted. Against the peak in 2021, when 245 landed shophouses worth a total of $1.8 billion were sold, the market appears to be slowing down.

A combination of factors, from rising price levels to increased global economic uncertainty, may have reduced investors’ appetite in shophouses. However, although transaction volume seems low, it is important to note that some deals might have been done through Special Purpose Vehicles (SPVs) or via share sales. Transactions without lodged caveats were also not included.

This inactivity comes as there is an impasse between sellers and buyers regarding prices as demand remains healthy.

Landed Shophouses Transaction Volume

Chart 1: Transaction volume and transaction value of landed shophouses

Source: URA as of 18 July 2025, ERA Research and Market Intelligence

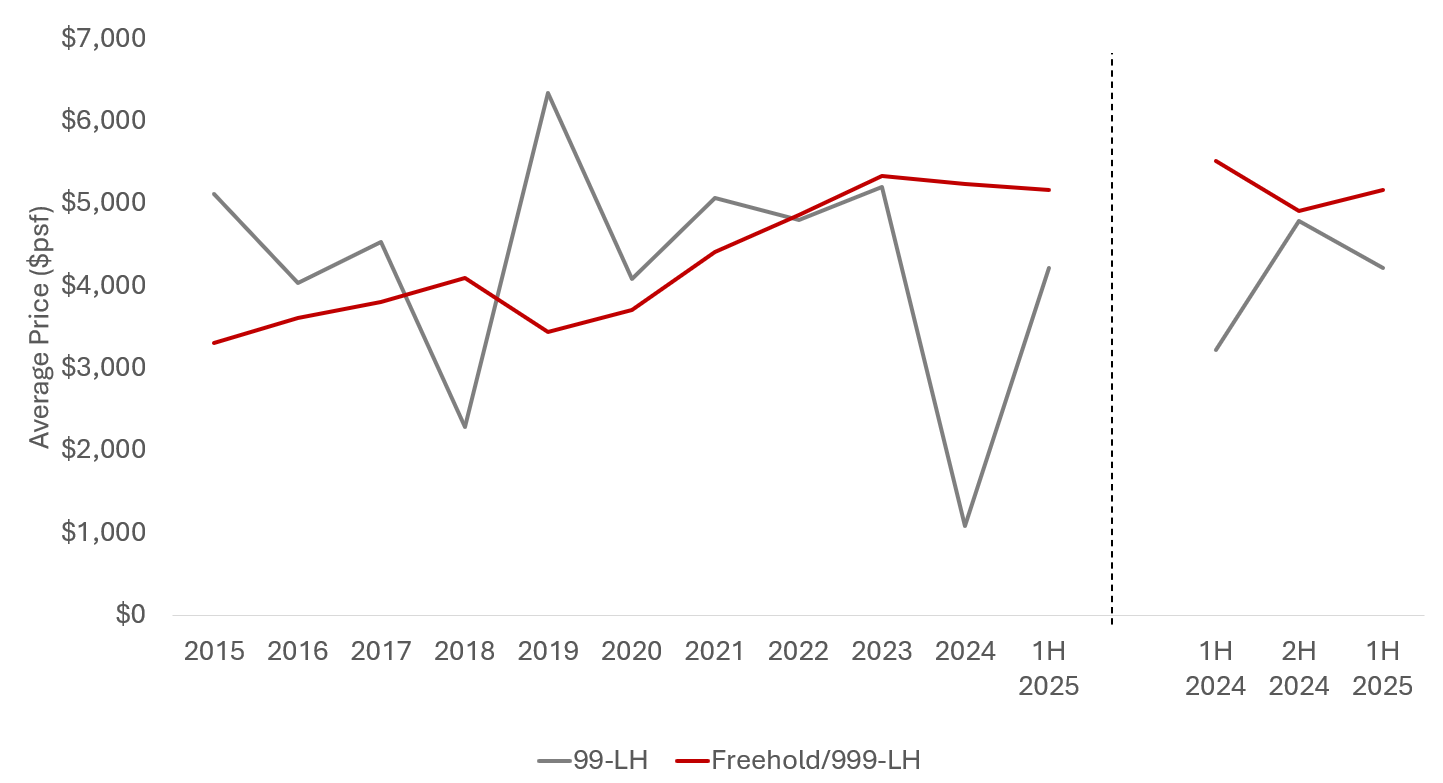

The market demonstrates a divergence based on tenure. Of the 34 landed shophouses transacted in 1H 2025, 91% (31 units) were of Freehold (FH) tenure, including shophouses with 999-year leasehold (999-LH) tenure. Comparing 2H 2024 and 1H 2025, the average psf price of freehold landed shophouses increased by 5.3% to $5,168. This is because these owners are not compelled to lower prices. Being immune to lease decay, freehold shophouses can withstand market volatility, maintaining their value over the long term. Institutional investors view this as an asset worth holding in their portfolio. In contrast, their 99-year leasehold counterparts experienced a 12% decrease in prices, as buyers may have concerns about the remaining lease term.

Chart 2: Average psf prices for landed shophouses

Source: URA as of 18 July 2025, ERA Research and Market Intelligence

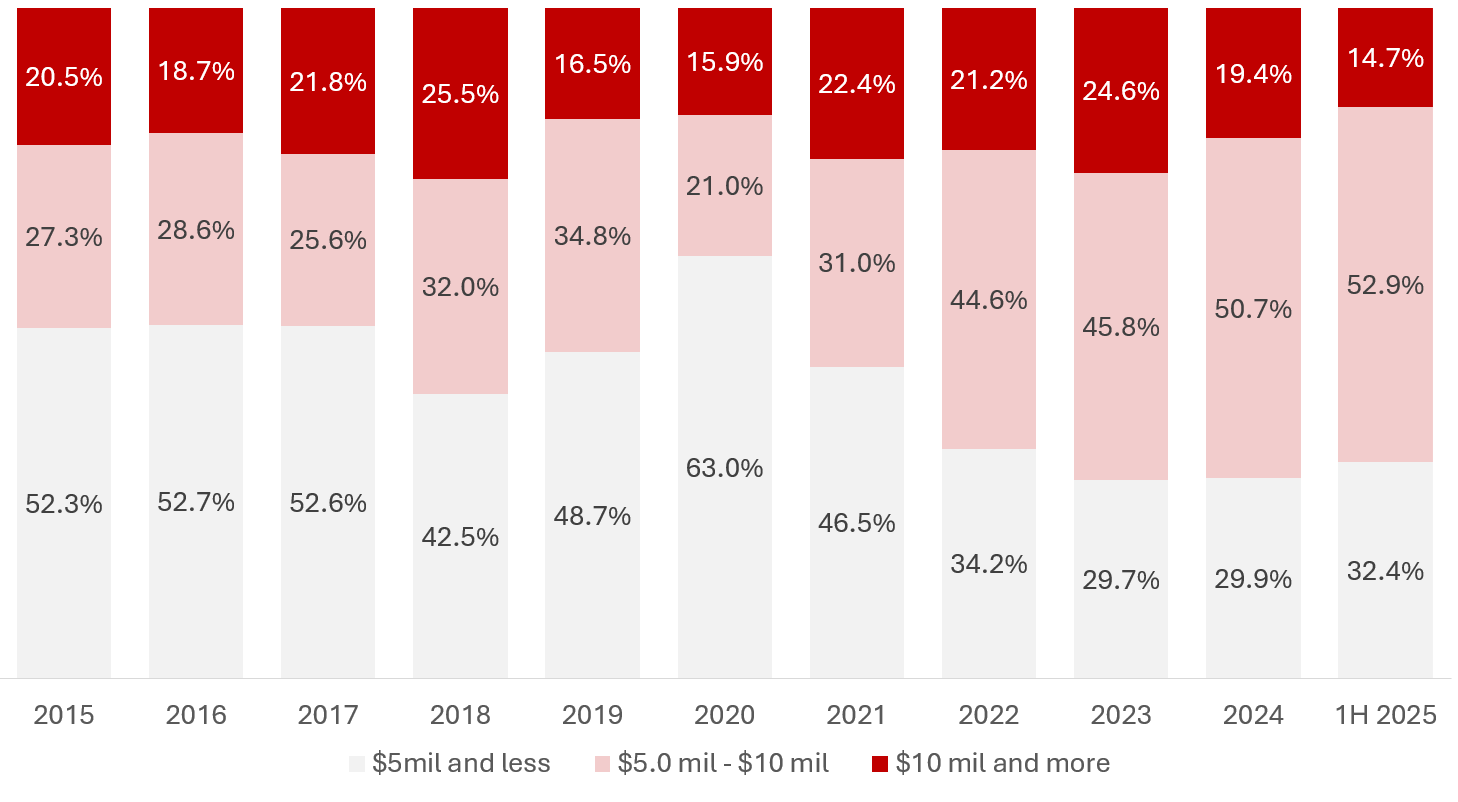

Over the past decade, the price quantum of landed shophouses has generally risen, as reflected by the proportion of higher-valued transactions. In 1H 2025, 52.9% of the shophouse transactions were between $5 million and $10 million. This could be the sweet spot for a landed shophouse. While there are shophouses transacted under $5 million, they are either not centrally located or have a 99-LH tenure.

Chart 3: Price quantum of landed shophouse in the last ten years

Source: URA as of 18 July 2025, ERA Research and Market Intelligence

Source: URA as of 18 July 2025, ERA Research and Market Intelligence

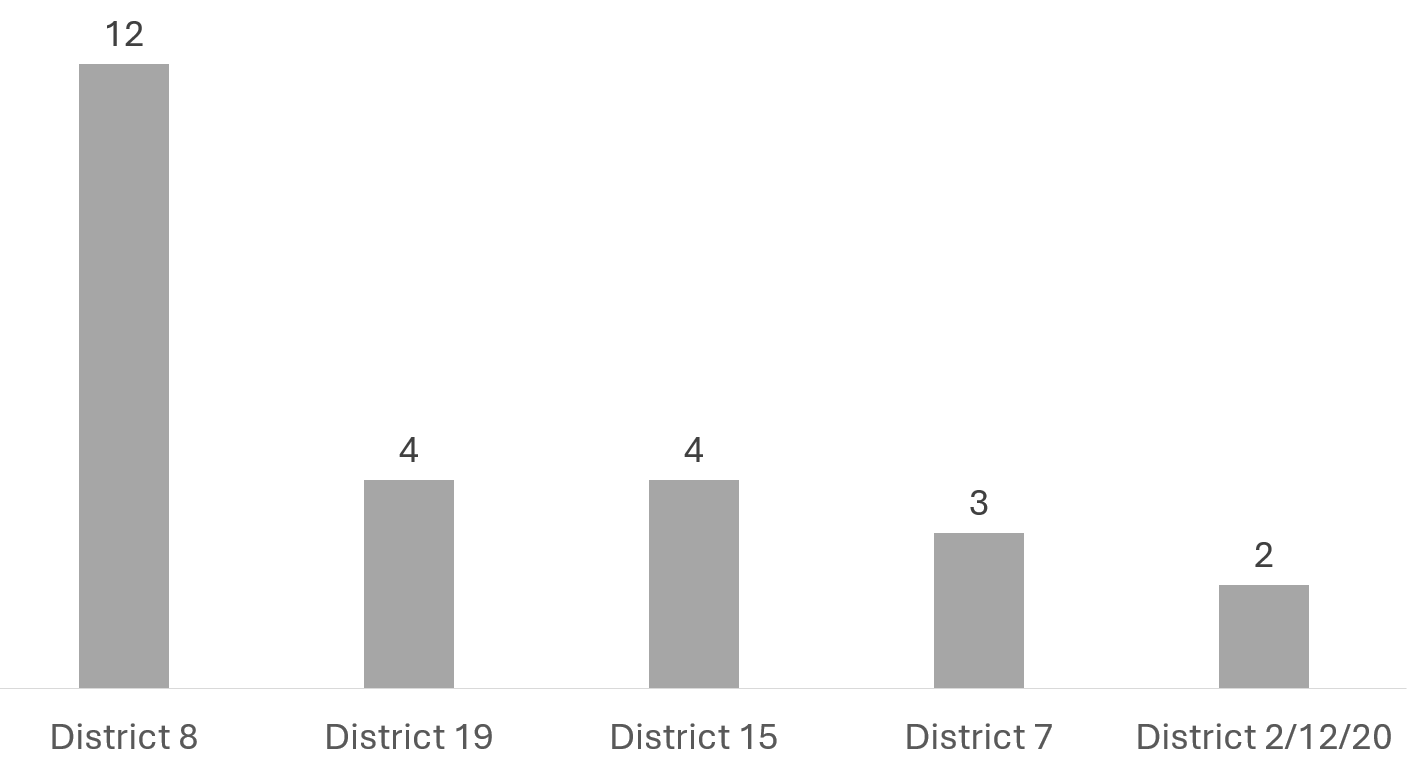

Popularity of Central Region Shophouses

Among the 34 landed shophouses sold in 1H 2025, were in the Central Region - an area popular for eateries, fitness studios and co-living spaces. As such, owners of Central Region landed shophouses will likely be able to command higher rents on their properties.

District 8 (Little India) saw the most transactions in 1H 2025. With 12 transactions, accounting for 36.4% of transactions, it proved its popularity to buyers. Some buyers saw this as an opportunity to pick up value buys present in District 8, as half of these transactions were transacted under $6m. Given is close proximity to the city, buyers are therefore able to find value buys in this district. Moreover, it draws high footfall from both local and foreigners, supporting strong hospitality and retail demand, allowing landlords to seek a higher rental yield.

District 19 (Serangoon Garden, Hougang, Punggol) and District 15 (Katong, Joo Chiat, Amber Road) each saw four transactions, while District 7 (Middle Road, Golden Mile) saw three transactions and District 2 (Chinatown, Tanjong Pagar), District 12 (Balestier, Toa Payoh) and District 20 (Ang Mo Kio, Bishan, Thomson) saw two transactions each.

Chart 4: Top five districts by transaction volume in 1H 2025

Source: URA as of 18 July 2025, ERA Research and Market Intelligence

Source: URA as of 18 July 2025, ERA Research and Market Intelligence

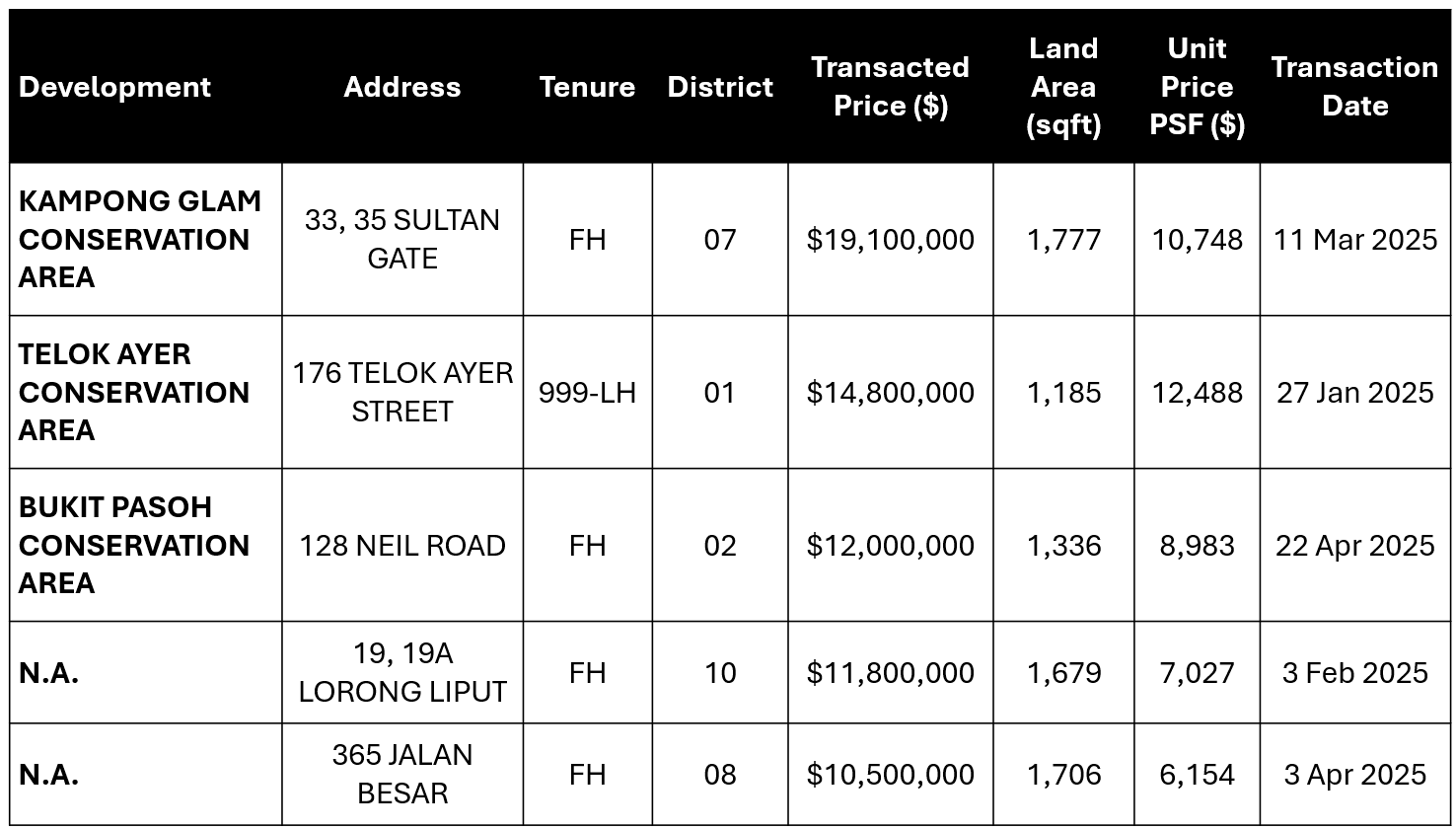

Table 1: Top five shophouse transactions in 1H 2025

Source: URA as of 7 July 2025, ERA Research and Market Intelligence

Source: URA as of 7 July 2025, ERA Research and Market Intelligence

Shophouses Transactions to Stay Subdued as Prices Expected to Remain Firm

Shophouses will continue to be sought after by local and international buyers owing to their rarity and heterogeneity. Without the additional stamp duties imposed, investors will continue to keep shophouses as a viable option. Family offices and investors are the most probable buyers for shophouses, especially when the properties are located in the Central Region or have a 999-Leasehold or Freehold tenure. Landed shophouses that can be converted for residential use may appeal to co-living operators looking to expand their portfolio.

In recent months, some businesses have shut down, succumbing to rising costs, including rents. Food and Beverage (F&B) operators in prime district shophouses have not been spared. With more retailers and F&B operators ceasing operations, pressure may mount on certain shophouse owners. A weaker rental outlook could prompt some to lower price expectations. In particular, sellers with less holding power, as well as those under Private Equity structures seeking to recycle capital, may be more willing to accept lower prices in order to close deals.

Moderating prices, where buyers and sellers can break through the impasse and bridge the bid-ask gap, will spur buying activities. Moreover, the shophouse market will further be buoyed too if the Fed proceeds to cut interest rates in September 2025.

Owing to the abovementioned factors, ERA forecasts a recovery in landed shophouse transaction volume to be between 30 to 40 units, with the transaction value to be between $260m to $360m in 2H 2025. This takes the total to be between 60 to 70 transactions with a total transaction value of $500m to $600m in the whole of 2025.

I confirm that I have read theprivacy policy and allow my information to be shared with this agent who may contact me later.