2Q 2025 URA Real Estate Statistics: Private Home Sales Dip Due to Fewer Launches, Amid School Holidays and General Elections

- ERA Singapore

- 9 min read

- PressRelease

- 25 Jul 2025

SINGAPORE, 25 July 2025 – According to the Urban Redevelopment Authority (URA), private home prices increased by 1.0% q-o-q in 2Q 2025, maintaining a steady pace of growth comparable to the previous quarter of 0.8%. By contrast, the total volume of private home transactions in 2Q 2025 plummeted 29.4% to 5,128 units over the same period, owing to a quieter new home market with fewer launches and external contributing factors, including the election season in April and May, as well as the June school holidays.

“New home sales in 2Q were weighed down by the seasonal lull, with only 1,212 units sold. The slowdown was in line with the limited number of launches during the quarter, which were primarily located in emerging residential precincts – areas that typically appeal more to investors than owner-occupiers. Nonetheless, the market remained resilient. Collectively, the 1H 2025 have seen 4,587 new homes sold – the highest first-half performance since 1H 2021.

Resale volume also rose by 2.3% to 3,647 units in 2Q 2025. Overall, the resale segment has remained stable, with transactions broadly in line with the five-quarter average of 3,715 units from 2Q 2024 to 2Q 2025.

In total, 1H 2025 saw 2,329 private home completions. An additional 2,620 units are scheduled for completion within the next six months. Excluding ECs, completions are expected to reach 4,949 units in 2025, which is a marked decrease from the 8,460 units completed in 2024.

In 3Q, new home sales are expected to rebound, supported by a strong pipeline of ten upcoming launches that will yield around 4,500 units. Price growth momentum is also likely to continue, led by launches in the CCR. Additionally, RCR may see home prices breach new benchmark pricing, particularly for projects located near the CCR-RCR boundary where buyer interest remains strong. July has already seen encouraging take-up rates at developments such as LyndenWoods (94%), UPPERHOUSE at Orchard Boulevard (54%), and The Robertson Opus (41%).

Separately, based on caveat figures, landed home sales moderated in 2Q to 426 units, with transactions declining by 2.3% quarter-over-quarter and 9.4% year-over-year. While the increase in private home prices has supported upgrading demand, the recent uptick in asking prices has resulted in some buyer resistance.

Despite the downbeat economic sentiment, the residential market has yet to feel its full impact. Buyer interest remains supported by lower interest rates, while the dip in transaction volume is more reflective of a muted new launch pipeline and fewer project completions rather than a sharp decline in demand,” said Marcus Chu, Chief Executive Officer (CEO), ERA Singapore.

Prices

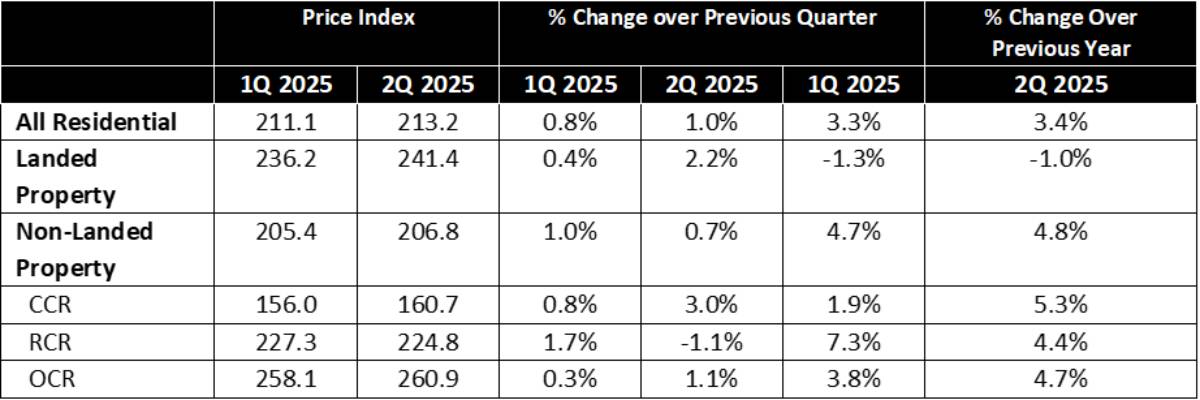

“The All Residential Private Price Index rose 1.0% quarter-on-quarter (q-o-q) in 2Q 2025, extending from the more moderate growth of 0.8% seen in 1Q 2025. On a year-on-year (y-o-y) basis, the All Residential Private Price Index rose 3.4%.

The Landed Price Index registered a faster pace of growth, at 2.2% quarter-over-quarter (q-o-q), compared to 0.4% growth in 1Q 2025. This marks the second consecutive quarter of price growth for landed homes. However, compared to the same period last year, landed property prices have moderated by 1.0%.

The Non-landed Property Price Index registered a slower pace of growth of 0.7% q-o-q in 2Q 2025, slower than the 1.0% growth seen in 1Q 2025. On a year-on-year basis, non-landed property prices rose 4.8%.

Among the market segments, non-landed homes in the Core Central Region (CCR) recorded the fastest pace of growth at 3.0% q-o-q in Q2 2025, followed by the Outside Central Region (OCR) with a 1.1% increase. Conversely, the Rest of Central Region (RCR) saw a reversal, registering a 1.1% q-o-q decline. Non-landed home prices held firm, underpinned by new home sales in the CCR and OCR that set fresh pricing benchmarks.

Meanwhile, the launch of Bloomsbury Residences and One Marina Gardens at more accessible price points—reflective of their up-and-coming locations—contributed to a moderation in overall RCR prices.”

Table 1: Change in URA Private Property Price Indexes for 1Q 2025 and 2Q 2025

Source: URA, ERA Research and Market Intelligence

Transaction Volume

New Sale

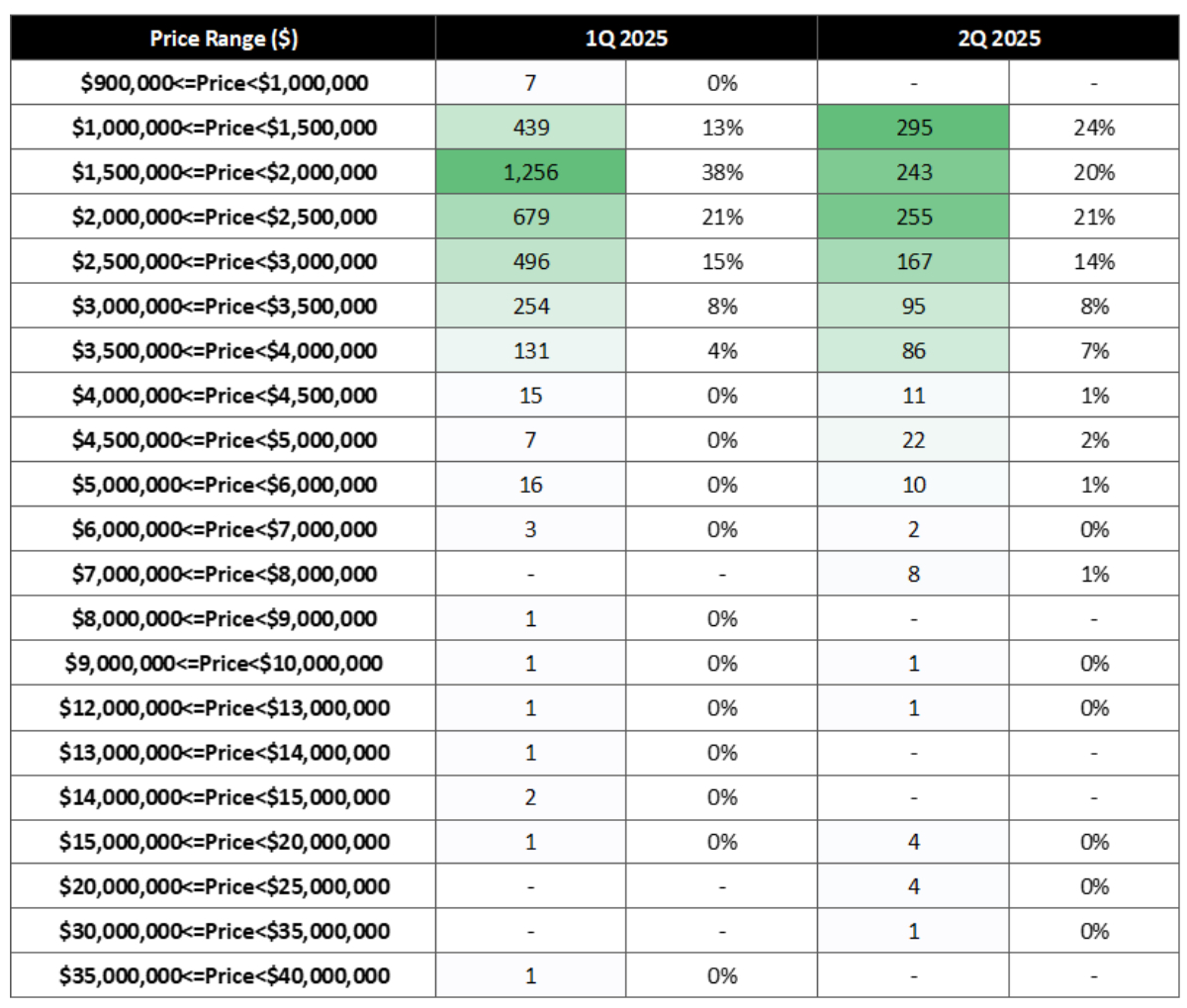

“Developers sold a total of 1,212 new homes in 2Q 2025, lower than the 3,375 new homes sold in 1Q 2025. In total, developers launched 1,520 new homes in 2Q 2025 compared to 3,139 new homes in 1Q 2025. The decline came amid a quieter launch pipeline, largely attributed to the election period and the June school holidays, which led to dampened market activity.

New home sales at RCR accounted for 74.5% of the new homes sold in 2Q. Of which, Bloomsbury Residences and One Marina Gardens made up 71% of new home sales in RCR.

In terms of price quantum, 2Q saw a more even distribution of transactions across the $1 million to $2.5 million range (Table 2), compared to 1Q, where a heavier, larger proportion of sales weight in the $1.5 million to $2 million bracket.”

Table 2: New Non-landed Home Transactions by Price Quantum

Source: URA, ERA Research and Market Intelligence

“Total unsold stock marginally increased to 18,498 units in 2Q 2025, from 18,270 units in 1Q 2025. Notably, the OCR and RCR registered their first increase in unsold stock after steady depletion since 2Q 2024. Separately, CCR saw unsold stock fall to nearly 7,200. Sales momentum has picked up for many of the earlier launches, many of which offered more attractive price points relative to newer projects.

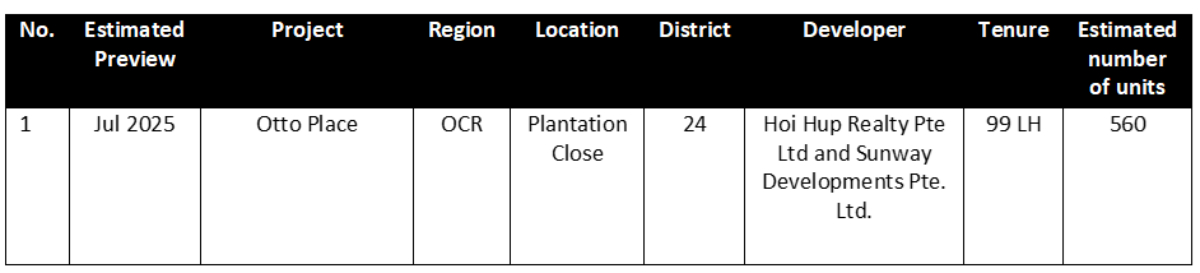

Demand in the EC market remains robust, with buyers quickly snapping up the shrinking supply. Otto Place launched in July and saw brisk sales – it sold 58.5% of its units at an average of $1,700 psf. The project will open for second-timer purchase in a month’s time. With no new EC projects expected until 2026, when Jalan Loyang Besar is slated for launch, the supply crunch is set to persist.”

Resale & Sub Sale

“In 2Q 2025, a total of 3,647 resale private homes were transacted, which marked a 2.3% q-o-q increase from the 3,565 units sold in 1Q. This performance aligns with the five-quarter average of 3,715 units from 2Q 2024 to 2Q 2025. Separately, sub-sale transactions reached 269 units in 2Q 2025, down from 321 units in 1Q. This is the lowest volume since 1Q 2023, when 243 sub-sale transactions were clocked. This trend is mainly due to a smaller pipeline of private home completions.

Completions

“A total of 341 private homes were completed in 2Q 2025, and collectively, 1H 2025 saw a total of 2,329 private home completions (excluding ECs). An additional 2,620 units are scheduled for completion within the next six months. Excluding ECs, completions are expected to reach 4,949 units in 2025, which is a marked decrease from the 8,460 units completed in 2024.”

Landed

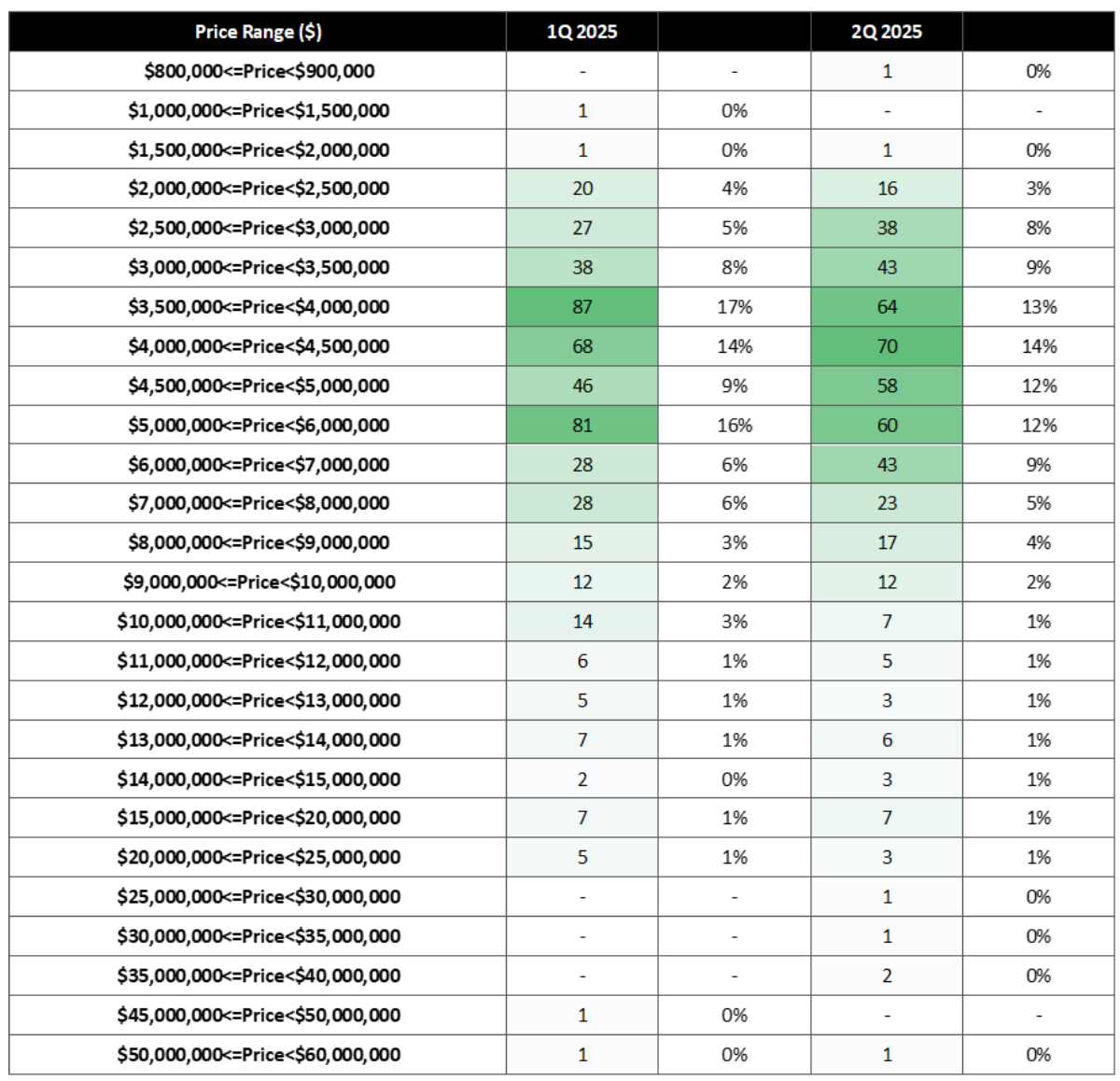

“The number of landed homes sold moderated in 2Q 2025, falling by 2.3% q-o-q and 9.4% y-o-y. Although higher private home prices have bolstered demand from landed home upgraders, the increase in asking prices (Table 3) may have tempered buying momentum, with some signs of buyer resistance.”

Table 3: Landed Home Transactions by Price Quantum

Source: URA, ERA Research and Market Intelligence

Rental

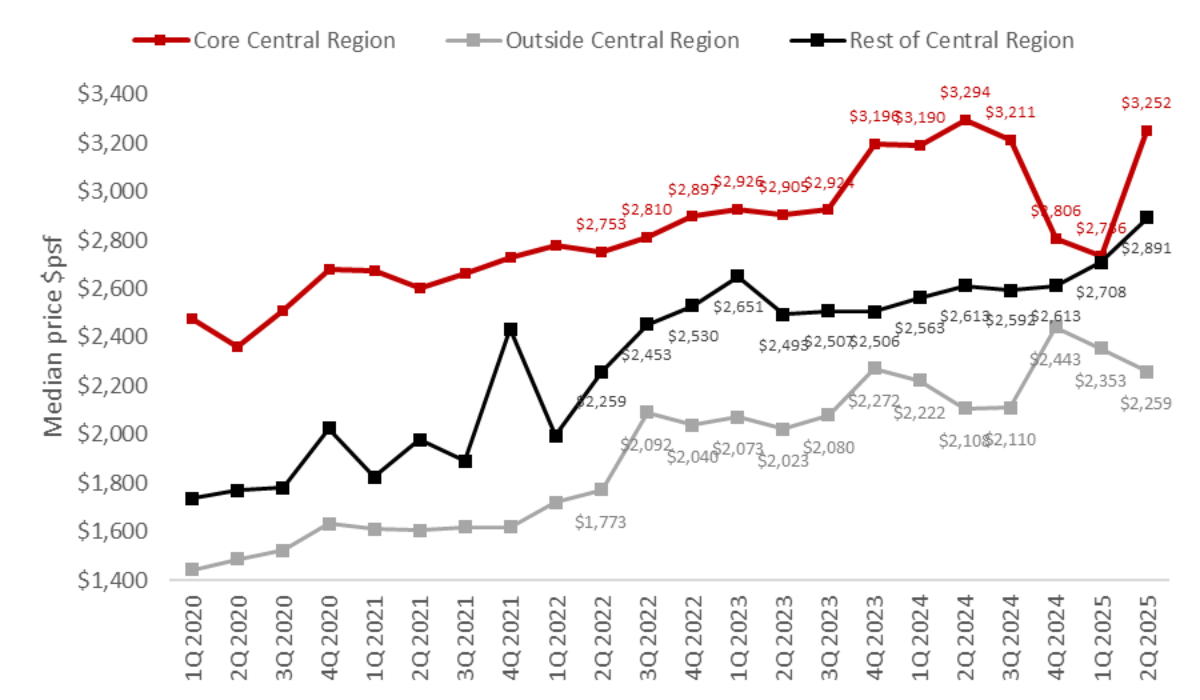

CCR rental growth was driven in part by the recent completion of homes in the region. As CCR properties are typically held for investment, landlords tend to put these newly completed units up for rent and often set higher asking rents to align with market expectations. In contrast, homes in the RCR and OCR are more commonly owner-occupied. Even when rented out, these units are less likely to command aggressive rental premiums.

Upcoming launches

“In 3Q, a strong pipeline of ten new launches—yielding around 4,500 units—new home sale is poised to pick up. We are also likely to see price growth momentum driven by launches at the CCR region. RCR may also see home prices breach new benchmark pricing earmarked by RCR launches bordering the CCR-RCR boundary, where buyer interest remains strong. July has already seen respectable take-up rates at LyndenWoods (94%), UPPERHOUSE at Orchard Boulevard (54%), and The Robertson Opus (41%).”

Chart 1: Median New Home Prices by Market Segment

Source: URA, ERA Research and Market Intelligence

Table 4: List of Upcoming Launches in 2H 2025

Source: ERA Project Marketing

Table 5: Executive Condominium

Source: ERA Project Marketing

Outlook

“Buyer interest remains supported by lower interest rates, while the dip in transaction volume is more reflective of a muted new launch pipeline and fewer project completions rather than a sharp decline in demand.”

Buyer interest remains supported by lower interest rates, while the dip in transaction volume is more reflective of a muted new launch pipeline and fewer project completions rather than a sharp decline in demand.

Turning towards a broader outlook, we also expect to see more widespread economic impact arising from global uncertainty and weaker trade demand. These outcomes may further dampen consumer sentiment, leading homebuyers to adopt a more prudent stance before committing to a purchase.

However, possible silver linings may be found in a potential interest rate cut by the Fed in July, as well as the recent 2025 Draft Master Plan announcements. The latter saw the introduction of new housing neighbourhoods in areas such as Dover, Defu, Newton, and Paterson, in addition to integrated community hubs in Sengkang, Woodlands North, and Yio Chu Kang, along with other initiatives. Together, these developments could help promote buyer confidence by reinforcing the Government’s long-term plans for urban renewal and liveability.

In 3Q, a strong pipeline of ten new launches, yielding around 4,500 units, is poised to drive new home sales. We are also likely to see price growth momentum driven by launches at the CCR region. RCR may also see home prices breach new benchmark pricing earmarked by RCR launches bordering the CCR-RCR boundary, where buyer interest remains strong. July has already seen respectable take-up rates at LyndenWoods, UPPERHOUSE at Orchard Boulevard, and The Robertson Opus.

In light of current conditions and barring any unforeseen circumstances, ERA projects that 8,500 to 9,000 new homes will be sold for the entire year of 2025. In conjunction, sub-sale and resale transactions are also expected to reach between 1,100 and 1,300 units and 14,000 and 15,000 units, respectively, by the close of 2025.”

For media enquiries, please contact:

Lisha Rodney

Public Relations Manager, ERA Singapore

Email: [email protected]

I confirm that I have read theprivacy policy and allow my information to be shared with this agent who may contact me later.