Are Prime Location Public Housing (PLH) Flats Right for You?

- Stanley Lim

- 7 min read

- Blog

- 13 Feb 2023

Let’s rewind the clock back to 2021, specifically to November, when the biggest headline in the media was the easing of COVID-19 measures on dining out in Singapore.

And while this piece of news was certainly cause for celebration, the very same month also saw the very first Built-to-Order (BTO) projects – namely River Peaks I & II in Rochor – launched under the Prime Location Public Housing (PLH) model.

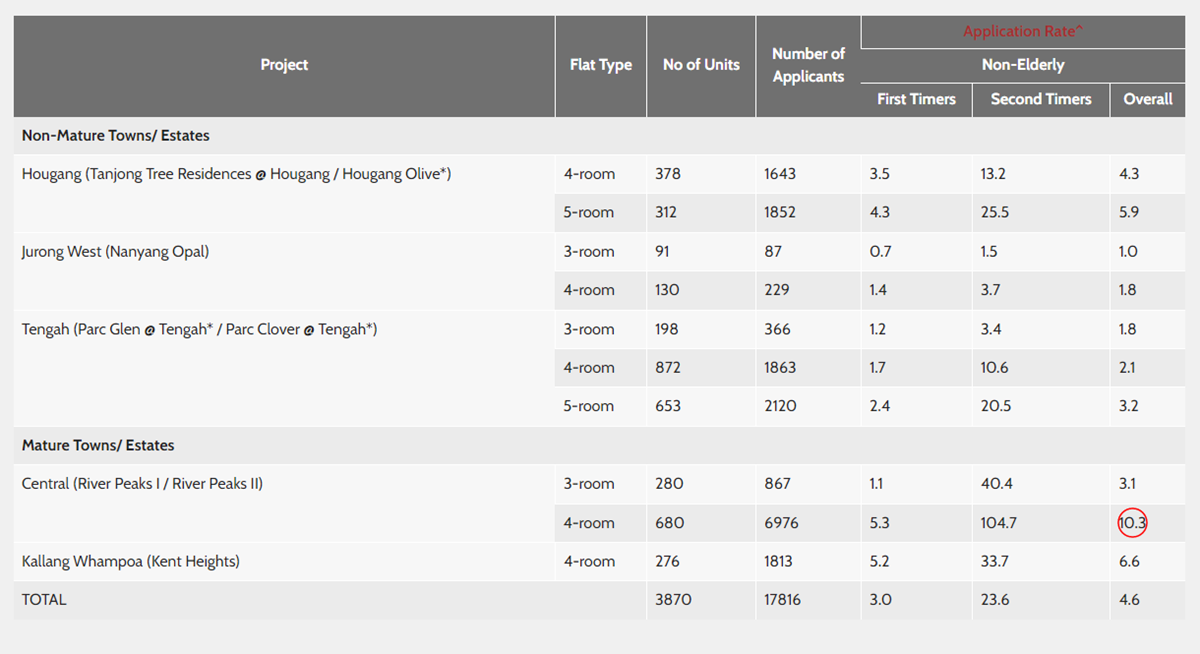

How then did the public respond? To put it lightly, demand for these PLH flats in Rochor was “moderate to healthy” with upwards of 6,000 applications received for 680 four-room units (i.e. 10.3 times oversubscribed).

Source: HDB

In contrast, subsequent PLH developments in other neighbourhoods have seen favourable, but comparatively muted results.

Examples include Ghim Moh Ascent in Queenstown (2,919 applications for 671 four-room units, i.e. 4.4 times oversubscribed) as well as Alexandra Vale/Havelock Hillside in Bukit Merah (7,916 applications for 1,298 four-room units, i.e. 6.1 times oversubscribed).

So, what gives? What could explain the difference in popularity between these PLH developments? Here’s a closer look at some reasons why BTO flats built under the PLH initiative aren’t guaranteed to pique the interest of Singaporean home buyers.

What is the Prime Location Public Housing (PLH) Initiative?

If you’re familiar with Singapore’s real estate market, surely you’ve heard of the so-called “lottery effect”.

But just to reiterate, this term refers to the favourable outcome of successfully balloting for an BTO/HDB flat in a prime area and then making a substantial profit from its sale, not unlike winning big in a TOTO draw or the Singapore Sweep.

Those who are unfamiliar with the “lottery effect” may think that it’s too good to be true, but the fact of the matter is that it’s very much real. For instance, as last reported in Singapore media, there were 277 million-dollar HDB resale flats sold in 2022 as of October.

Source: HDB

Hence, in the interest of keeping HDB homes in central areas affordable and accessible for local homebuyers, the Singapore Government reacted by implementing the PLH initiative in 2021. This saw new batches of BTO flats being introduced to prime estates, albeit accompanied by special conditions to keep their prices within reach of regular incomes.

Alternatively, the rationale behind the PLH initiative can be summarised by this quote from National Development Minister Desmond Lee: “If left to the forces of the private market, it’s likely that these attractive locations would become very expensive and exclusive locations, with housing that only the well-to-do can afford.”

Reasons why Prime Location Public Housing (PLH) flats aren’t for everyone

PLH flats are situated in some of the best neighbourhoods in Singapore, which have many positives going for them, including but not limited to, an abundance of nearby retail and entertainment choices, ample transport options, and not least, high property values.

So, with these many upsides, why aren’t PLH residential projects seeing explosive popularity? The answer mostly lies in the aforementioned special requirements that differentiate the PLH initiative from the traditional BTO public housing model.

Reason #1: There is a 10-year Minimum Occupation Period for PLH flats

To discourage speculation and encourage long-term price stability, a minimum occupation period (MOP) was introduced at the same time the local resale market for HDB flats was established in 1971.

This meant that HDB flat owners had to live in their homes for a fixed period of time – specifically, 3 years when the MOP first came to be and 5 years from 1973 onwards – before they were allowed to sell their flats on the open market.

Source: HDB

For the same reasons, PLH flats have a (much) longer MOP of 10 years to ensure their prices stay well within the means of the masses. However, this could also possibly make PLH flats less attractive in the eyes of home buyers who aspire to upgrade to a private property.

In addition to facing a longer runway to asset progression, owner-occupiers of PLH flats may find it financially tougher to make the metaphorical leap. This can be attributed to age limitations on bank loans, whereby older private homebuyers are likely to be subjected to shorter tenures, and thus higher monthly repayments on their mortgage.

Reason #2: There are tighter rental regulations in place

One of the biggest draws of owning a property of your own is the potential for earning steady income through rent, but that can be challenging with a PLH flat.

Not only are PLH flat owners restricted from renting out their homes before the MOP of 10 years is up, they’re only permitted to lease out spare bedrooms and not the entire unit. Or in other words, PLH flats are likely to be unsuitable for buyers who intend to monetise their homes.

Reason #3: Subsidies will be clawed back when a PLH flat is sold

Convenience aside, yet another big plus of purchasing a PLH flat is the additional subsidies given by HDB (on top of existing ones), which has resulted in more affordable public housing in prime areas.

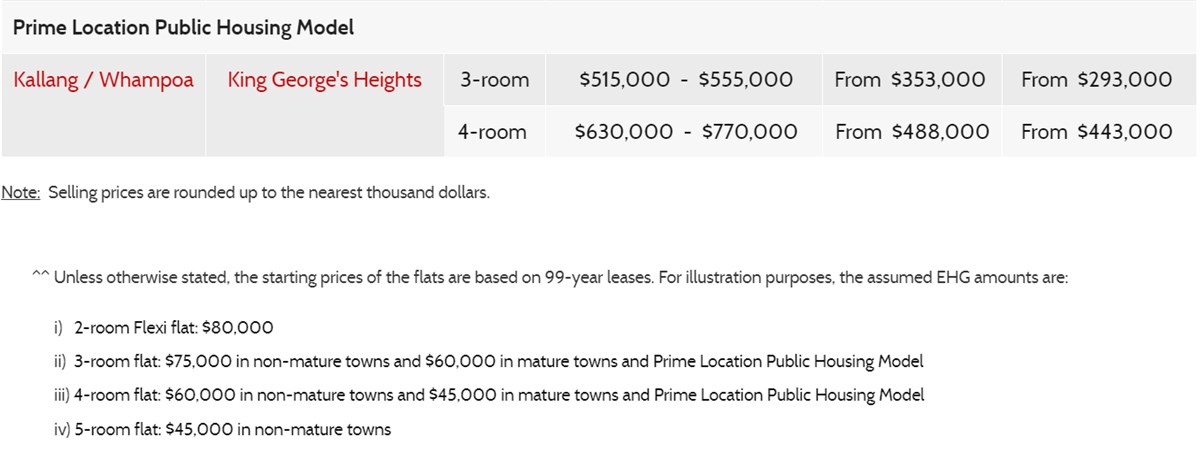

Take for instance, homes at King George’s Heights, a PLH estate that was launched during February 2022's BTO exercise. Compared to the range of transacted prices for nearby resale HDB flats at that point, the cost of new 3- and 4-room flats at King George’s Heights was considerably lower.

Source: HDB

After factoring in the relevant grants, buyers could expect to fork out upwards of $293,000 and $443,000 respectively for 3-and 4-room flats at King George’s Heights. On the other hand, if they were to purchase a 3- or 4-room HDB flat on the open market back then, they would likely have to fork out between $515,000 – $555,000 (for a 3-room flat) or $630,000 – $770,000 (for a 4-room flat).

That said, it’s not all sunshine and roses as there’s a subsidy clawback, which requires PLH flat owners to return to HDB a percentage on the sale price after their home is sold. It’s also worth noting that this clawback percentage may differ between PLH projects as the amount of additional grants given out can vary by development.

Reason #4: More stringent eligibility requirements are in place for PLH flats

Just like how the rental of PLH flats is more tightly regulated, HDB’s eligibility requirements pertaining to PLH homes are considerably stricter than those of regular HDB flats.

Firstly, the household nucleus of a PLH flat has to be comprised of at least one Singapore Citizen and one Permanent Resident (PR). In contrast, a regular HDB flat’s household can be made up entirely of PRs.

Secondly, unlike most HDB flats, PLH flats cannot be purchased by singles.

And finally, there’s an income ceiling present, whereby only families with a total monthly income of $14,000 or less ($21,000 or less, in the case of extended/multi-generational households) are eligible to purchase a PLH flat.

Should you purchase a PLH flat? Are there any other options?

If there’s one thing that’s unmistakably clear about PLH flats, it’s that they’re meant to be “affordable, accessible, and inclusive” public housing in prime areas for genuine Singaporean homebuyers. So, if you intend to build a forever home within a central location, these HDB flats are definitely a worthwhile purchase.

On the flip side, homebuyers who aim to generate wealth from their properties will do better to invest in private homes, such as new launches or resale condos, which not only offer greater flexibility in asset monetisation but also capital appreciation.

Disclaimer for consumers

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salespersons accept no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.