The Government has announced two changes to the Seller’s Stamp Duty (SSD) for residential properties:

(a) An increase in the holding period from three to four years, and

(b) increase of the SSD rates by four percentage points for each tier of the holding period.

These changes will take effect for all residential properties purchased on and after 4 July 2025, 12.00am. The revised SSD will not affect HDB owners due to the Minimum Occupation Period for HDB flats.

The Government has announced two changes to the Seller’s Stamp Duty (SSD) for residential properties:

- An increase in the holding period from three to four years, and

- An increase of four percentage points in SSD rates for each tier of the holding period.

These changes will take effect for all residential properties purchased on or after 4 July 2025, 12:00 a.m. The revised SSD will not affect HDB owners, as it is subject to the Minimum Occupation Period for HDB flats.

This reversion to the pre-2017 SSD holding period of four years aims to reduce speculative demand by lowering the number of sellers who flip their homes after just three years.

According to IRAS, the SSD for residential properties is payable for properties acquired after 20 February 2010. In most instances, the date of purchase/ acquisition of a property refers to:

-

- Date of Acceptance of the Option to Purchase* or

- Date of Sale and Purchase Agreement or

- Date of Agreement for Lease (for new HDB flat) or

- Date of transfer to a beneficiary where the property was originally held on trust for non-identifiable beneficial owner(s) or

- Date of Transfer where the above (a), (b), (c) and (d) are not applicable

*Excludes an Option to Purchase that is subject to the execution/ signing of the Sale and Purchase Agreement

ERA’s Take on the Changes:

“These adjustments to the SSD framework will help reduce speculative activity, although they will affect only a small minority of buyers. We welcome the changes and believe they will complement broader measures, such as increasing land supply, to foster a sustainable market.

Since most homebuyers are genuine owner-occupiers or longer-term investors, this measure is a gentle touch rather than a heavy-handed approach on the overall market. It aims to stabilise any spikes caused by short-term investors. It is not designed to crack down on the market but to reduce the froth from investors who sell shortly after the third year.

Notably, the elevated interest rates since September 2022 have eroded meaningful profits for property investors, which may have led them to extend their holding periods, especially now that interest rates have eased in recent months.

The property tax revisions introduced in 2023 have also resulted in higher taxes on non-owner-occupied residential properties, which may have contributed to this trend as well.

Investors have shifted towards a medium- to long-term holding strategy to increase rental income while waiting for prices to reach their preferred levels before selling. This requires greater endurance, but most now have that capacity and plan their exit strategies accordingly,” said Marcus Chu, Chief Executive Officer, ERA Singapore.

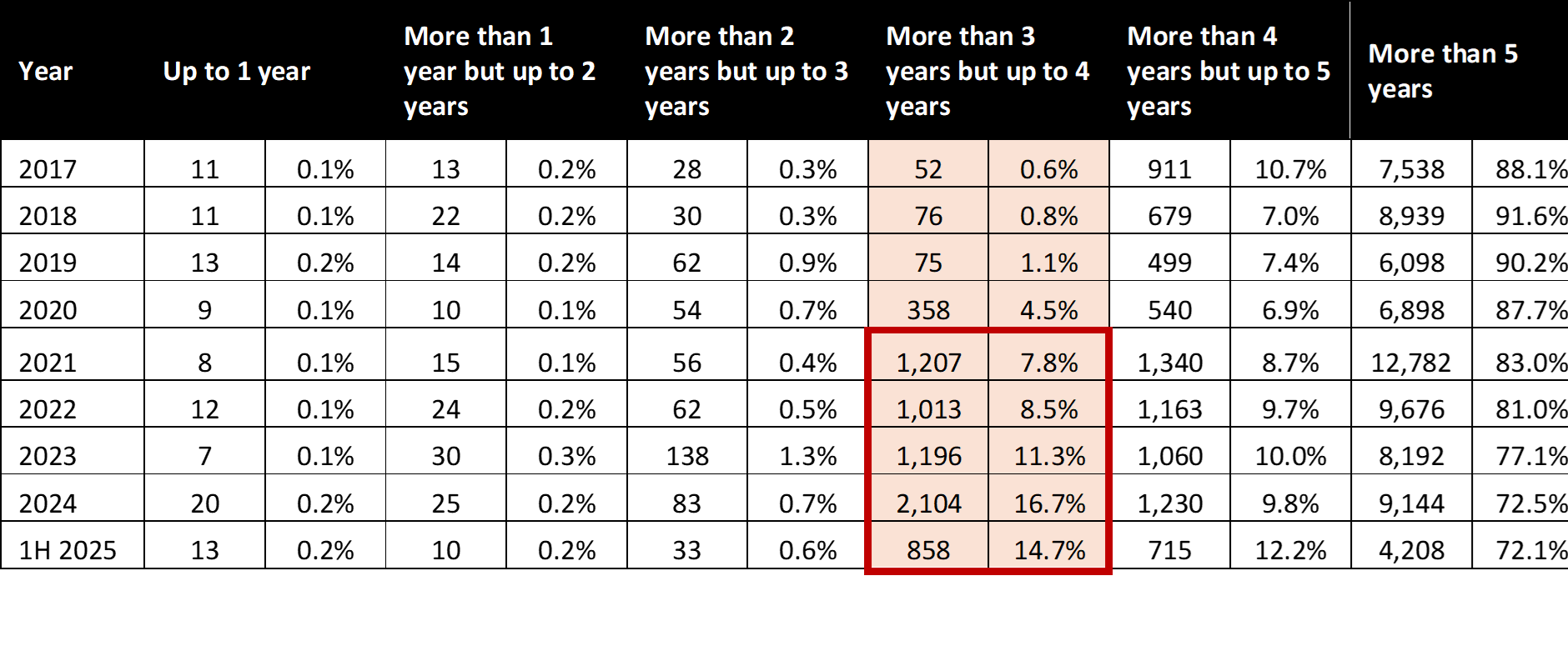

Table 1: Seller Stamp Duty Schedule

Source: MND, MOF, MAS, ERA Research and Market Intelligence

While more owners are selling after holding their homes for three to four years in recent years, they remain a minority.

There has been a significant jump in sellers who sold their homes after holding for more than 3 years but up to 4 years since 2021.

According to URA caveats, in 2020, only 358 sellers sold their non-landed homes after holding them for three to four years; however, by 2024, this number had surged to a peak of 2,104 sellers. In 1H 2025, sellers who had held their non-landed homes for more than 3 years but up to 4 years accounted for 858 transactions, or 14.7% of the total transactions.

Despite this increase, the majority of homeowners continue to sell only after holding their properties for five years or more.

In 1H 2025, about 72.1% of homeowners sold their homes after five years. This trend is further supported by SingStat data, which shows that the proportion of owner-occupied residential households remained high at 90.8% in 2024.

Table 2: Breakdown of Non-landed private homes sold by holding period

Source: URA, ERA Research and Market Intelligence

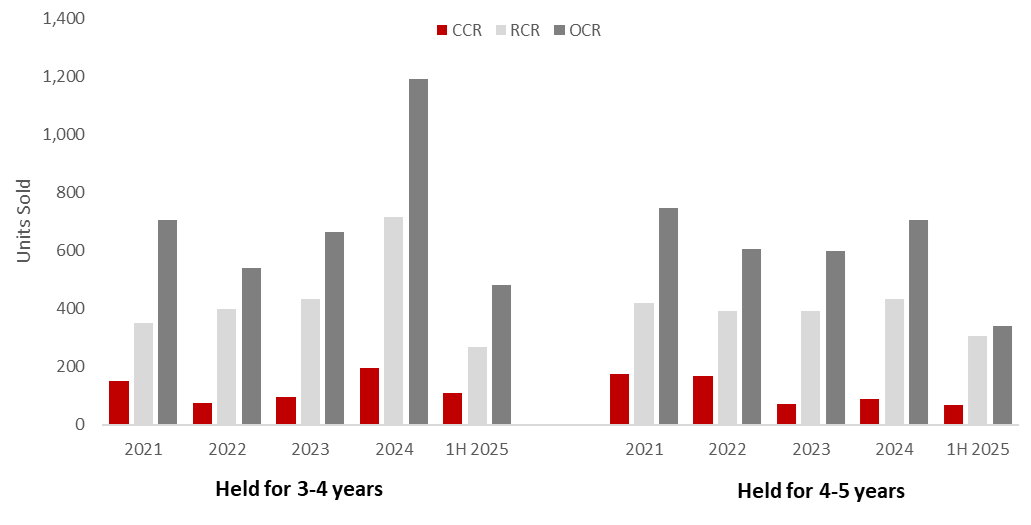

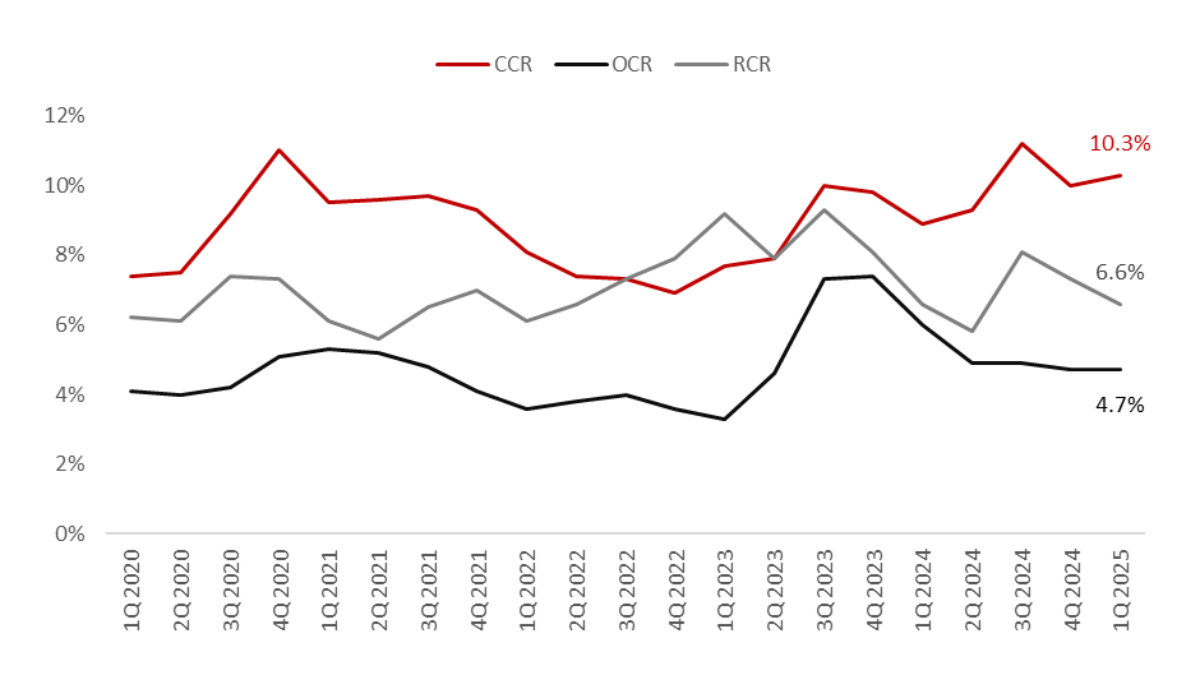

Outside Central Region saw the highest volume of homeowners selling within 3-4 years

Among the regions, the Outside Central Region (OCR) saw the highest volume of homeowners selling within 3-4 years, followed by the Rest of Central Region and the Core Central Region. This could be largely due to the more palatable price quantum of OCR homes compared to the other regions.

Chart 1: Breakdown of Non-landed private homes sold by Market Segment

Source: URA, ERA Research and Market Intelligence

Higher interest rates and property tax saw more investors extending their holding periods despite significant profits

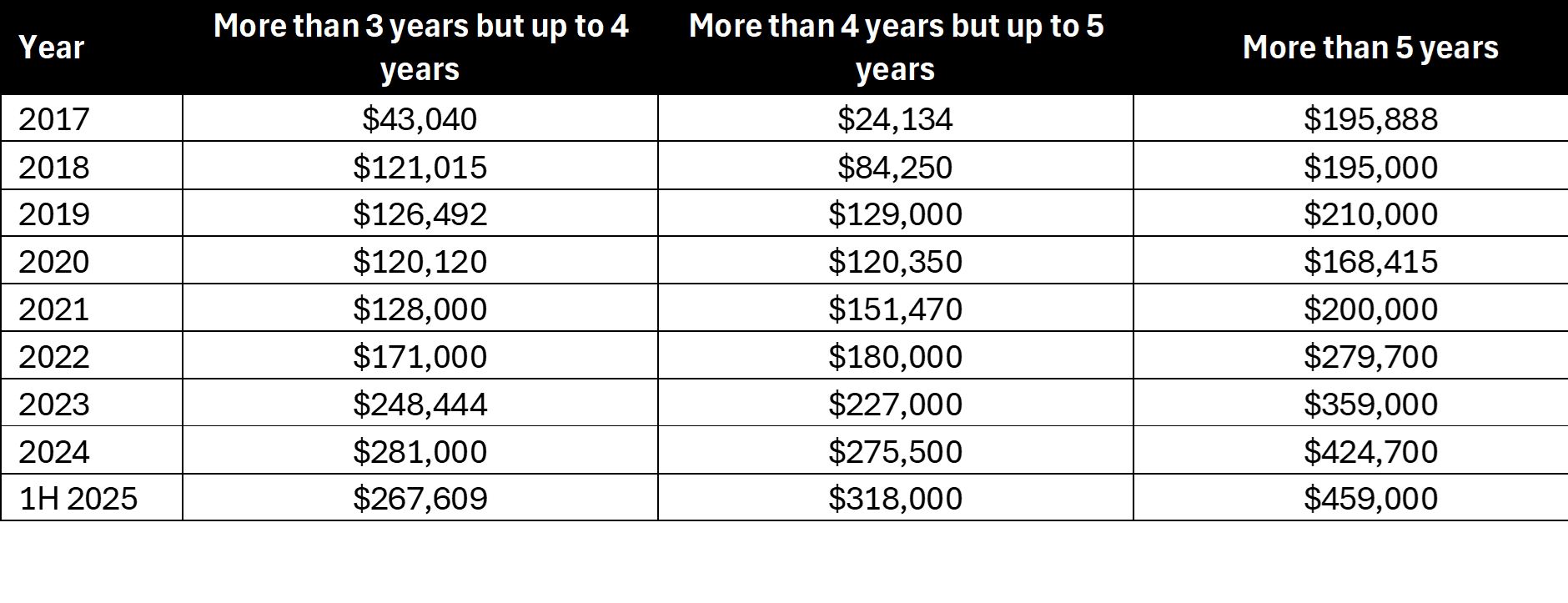

Looking at the median gross profitability of non-landed homes by holding period shows that while there are significant profits to be made after holding for three to five years, sellers who held their properties for more than five years saw the highest profitability.

Table 3: Median Gross Profitability of Non-landed private homes sold by holding period

Source: URA, ERA Research and Market Intelligence

Notably, the elevated interest rates since September 2022 have eroded meaningful profits for property investors, which may have led them to extend their holding periods, especially now that interest rates have eased in recent months. The property tax revisions introduced in 2023 have also resulted in higher taxes on non-owner-occupied residential properties, which may have contributed to this trend as well.

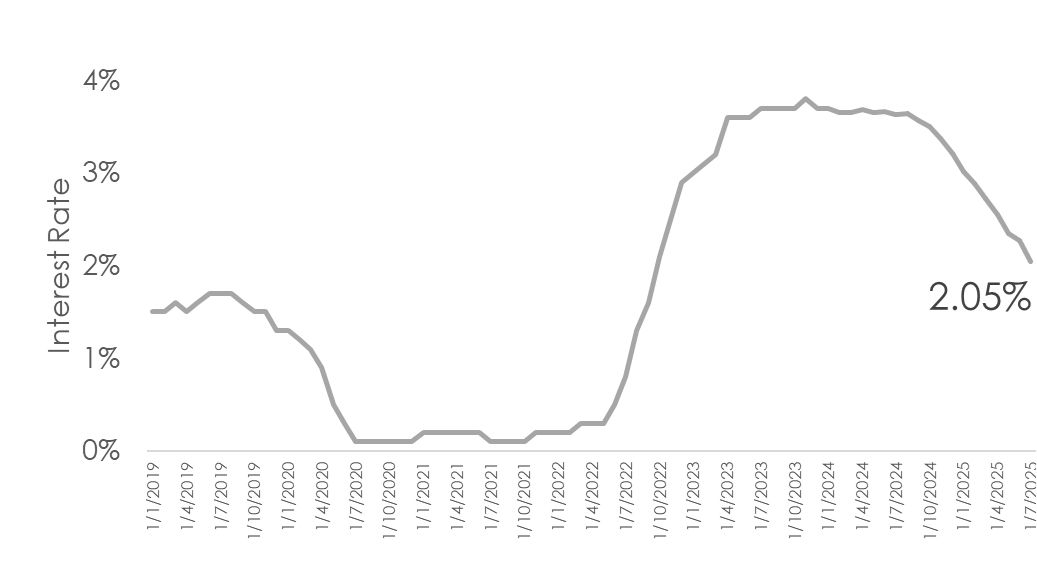

Chart : 3-month Compound SORA

Source: MAS, ERA Research and Market Intelligence

In conclusion

With the introduction of additional Buyer’s Stamp Duty tiers in April 2023, the residential market has shifted primarily towards local and owner-occupier demand.

Alongside increasing economic uncertainty in recent months, buyers have become more cautious, and more now view property as a long-term investment. We are likely to see property investors, who often buy and sell their units within three years, most affected by this change. However, the majority of homebuyers, who are owner-occupiers and long-term investors, are unlikely to be impacted.

ERA welcomes the adjustments to the SSD and expects the impact to be marginal on the overall market, as demand is primarily from owner-occupiers. The SSD revision will work alongside other policies, such as increased land supply, to support a more sustainable and stable housing landscape.

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.

The Financially Independent, Retire Early (FIRE) movement is not new to Singaporeans. In fact, many older Singaporeans might even assert that they were raised to be frugal and financially independent.

Today, however, the FIRE movement has taken on a new name and gained worldwide momentum, particularly among younger Singaporeans who are embracing it with fresh enthusiasm.

The motivation behind the FIRE movement

It is no surprise to see the revival of the FIRE movement among younger Singaporeans. As work demands become increasingly heavy, more and more Singaporeans are experiencing job burnout. Meanwhile, rising living costs add to financial pressures, making it harder for many to stick to their retirement plans. For many, the FIRE movement offers a possible way out of the rat race and a chance to take control of their finances.

For over two decades, the continuous growth in the property market has enabled some Singaporeans to achieve their FIRE goals successfully through property investment. However, in recent months, increasing global economic uncertainty and a shifting world order threaten to undermine future property gains. Yet, when we look beyond the short-term volatility, strong fundamentals still indicate that real estate is a valuable vehicle to help you achieve your FIRE goals.

Let us explore these fundamentals while discussing the trade-offs that investors may need to consider in this evolving landscape when selecting an investment property aligned with the FIRE movement.

Singapore’s agile policymaking and the adaptability of its Masterplan enable us to navigate an increasingly uncertain economic environment.

Singapore’s recent leadership transition coincides with its master plan review, providing a timely opportunity to refresh its positioning as it navigates an increasingly uncertain economic environment.

Previous versions of the Masterplan were primarily designed to address immediate demands relevant at that time. However, many of these trends have since shifted significantly. Looking ahead, we are now facing different challenges, including sustainability concerns, rising costs, an ageing population, and evolving economic needs. All of these will shape Singapore’s future real estate landscape differently.

By remaining nimble and adaptable, Singapore can uphold its relevance on the global stage and continue attracting investors, thereby supporting long-term real estate growth. This also creates opportunities for investors to venture into real estate beyond the residential segment and into the commercial and industrial sectors.

Long-Term Population Growth along with a proactive strategy to Sustain Housing Demand

It may be unpopular to believe that Singapore’s declining birth rate will negatively impact its economic competitiveness in the long term. Therefore, from a policy perspective, it makes sense to embrace more foreign talent to support and grow our economy, an approach that will undoubtedly drive housing demand.

Some may argue that the influx of foreign workers will increase housing demand, potentially leading to higher property prices. However, let us take a step back and examine this possibility. In April 2023, the Additional Buyer’s Stamp Duty (ABSD) for foreign buyers was doubled from 30% to 60%, a move that almost immediately reduced housing demand among this group of buyers. Consequently, foreign workers in Singapore are often more inclined to rent rather than purchase property, as they typically view their stay as temporary.

That said, some eventually become permanent residents or naturalised citizens, opting to settle, establish their careers, and raise their families in Singapore. Regardless of whether they are renting or buying, they will still require housing.

1. Prioritise properties that have access to a steady and sustainable tenant pool.

With nearly 90% of housing owner-occupied, the availability of homes for rent remains limited, as evidenced by the persistently low vacancy rates across various market segments. Understanding how rental demand varies across these segments can provide you with an advantage when planning your next property purchase.

Chart 1: Vacancy Rate Across Market Segments

Source: URA, ERA Research and Market Intelligence

For instance, the Core Central Region (CCR) has long been regarded as a popular housing choice for foreign expatriates, thanks to its prime location in the heart of Singapore. It offers a short commute to key business districts and convenient access to popular shopping and lifestyle amenities. Given its higher concentration of investment properties, vacancy rates in the CCR tend to trend higher compared to the Rest of Central Region (RCR) and Outside Central Region (OCR).

Although traditionally driven by Singaporean owner-occupiers, we also observe rental demand in the RCR and OCR, albeit to a much lesser extent than in the CCR. This is because more expatriate families are adapting to and embracing the local Singaporean culture, particularly as Singapore continues to enhance its decentralisation efforts.

2. Stay invested for the long haul to achieve meaningful capital appreciation

When it comes to property investing, time in the market consistently outpaces short-term timing strategies. Based on median unlevered returns from property investments in Singapore, investors who retained their properties for 15 years or longer experienced their returns increase by over 50% compared to those who held on for less than 15 years. This underscores the importance of adopting a long-term investment horizon, where capital appreciation compounds steadily over time, navigating market cycles and short-term price fluctuations.

For investors aiming to achieve financial independence, this long-term approach to holding property helps build lasting wealth while managing market fluctuations.

Chart 2: Median Unlevered Returns Base on Holding Period

Source: URA (Jan-May 2025), ERA Research and Market Intelligence

3. Narrowing price gap between CCR and RCR could open up new price growth opportunities in CCR

The successive new home launches in the RCR and OCR since 2023 have supported price growth in these regions. In contrast, the CCR has experienced fewer new home launches during this time, leading to a slower rate of price growth.

In 1Q 2021 the CCR and RCR price gap was around 39%, but it has since narrowed significantly and is now almost on par.

While some may argue that the absence of new launches in the CCR is not a significant factor in the slower price growth, they might be overlooking an important point: home prices have largely been driven by new launches. With at least five new CCR projects scheduled for launch in 2H 2025, the CCR could experience renewed momentum in price growth.

Chart 3: Narrowing Price Gap between CCR and RCR

Source: URA, ERA Research and Market Intelligence

4. Masterplan 2025 may offer a glimpse into potential medium- to long-term growth locations

This month, more concrete plans under Master Plan 2025 will be unveiled, which could provide insights into potential growth locations. For instance, URA has already announced high-level plans for areas such as the Southern Waterfront and Kallang Alive, which are expected to spearhead housing demand in these locations.

Keeping a close watch on Masterplan changes can be rewarding, as early entry into emerging locations offers opportunities to ride on future market growth. For those looking to capitalise on tenant demand, identifying key business parks such as One-North and developments in regional centres may also prove advantageous as these locations gradually become more established and populated, with a workforce driving housing demand.

FIRE Is Still Achievable Through Real Estate, But You Will Need the Right Strategies and Skilful Planning

The road ahead is more challenging, but achieving FIRE is possible through calculated trade-offs. One key consideration is that the time required to achieve FIRE may be extended, as future project growth is likely to moderate. Buyers should remain open and selective, as not all developments will perform equally or provide the same growth potential. This is where working closely with a trusted salesperson can help curate a long-term, tailored plan to remain on track towards your FIRE goals.

Ultimately, although the journey toward FIRE may encounter new challenges, with adequate planning, flexibility, and professional guidance, real estate can still serve as a powerful means to build long-term financial independence.

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.

下文由ERA公关经理岳开新翻译

此前我们曾探讨过,延长中央商务区奖励计划(CBD Incentive Scheme,简称CBDI)与战略发展奖励计划(Strategic Development Incentive Scheme,简称SDI)对振兴中央商务区所起的重要作用。这些计划为市中心老旧建筑的重建注入了活力,成为城市更新的重要催化剂。如今,作为中央商务区的延伸区域,滨海南将肩负起重塑新加坡城市景观的关键使命,揭开发展新篇章。

中央商务区的演变

19世纪

新加坡最早的商业区可追溯至19世纪初,当时商业活动沿新加坡河两岸逐步展开。凭借海上丝绸之路的战略地位,新加坡迅速崛起为重要自由港,成为中国、印度与东南亚之间贸易的枢纽。

当时,驳船码头(Boat Quay)、克拉码头(Clarke Quay)及莱佛士坊(Raffles Place)一带陆续建起大量店屋,支撑快速发展的贸易活动与日益壮大的商圈。银行及其他相关企业也随之进驻,逐步形成新加坡首个真正意义上的商业核心区。

来源:郭尚慰收藏,PictureSG,新加坡国家图书馆

进入20世纪初,随着新加坡港口地位不断上升,商业区开始面临严重拥堵问题。由于缺乏系统的城市规划,商铺、住宅与工厂混杂分布,造成道路阻塞、污染加剧,引发公众对健康与环境的担忧。

为应对这些挑战,新加坡政府在1960至1970年代启动大规模城市提升计划,旨在以更有序的方式重塑城市面貌。

1966年出台的《土地征用法令》(Land Acquisition Act)和1967年政府售地计划(Government Land Sales, 简称GLS)的推出,有效解决了土地所有权零散的问题,并为私人开发设立了更透明、规范的土地获取机制。这些政策为现代中央商务区的发展奠定了坚实基础。

迈向现代化的摩天商务区

在城市规划框架下,下一阶段的发展聚焦于建设高层办公大楼,推动中央商务区的现代化。Hong Leong Building(1976年)、华侨银行中心(OCBC Centre,1976年)、大华银行广场(UOB Plaza,1972年)和新加坡置地大厦(Singapore Land Tower,1980年)是首批拔地而起的摩天大楼,至今仍屹立在新加坡的天际线中。

这些高楼不仅重塑了城市轮廓,也满足了不断增长的办公空间需求,为新加坡金融中心的发展提供了基础设施支撑。

进入2000年代,新加坡作为区域金融枢纽的地位愈发稳固,带动了对高品质办公空间的持续需求。与此同时,商业价值稳步上扬,空置率维持在低位,吸引大量机构与私人投资者将目光投向这一市场,以期实现长期资本增值与稳定回报。

此外,中央商务区拥有覆盖全岛的交通网络,连通性强,大幅提升商务便利性。作为新加坡商业生态的核心枢纽,中央商业区不仅承载着贸易与商务活动,也促进了企业间的交流与合作。

在2024年全球金融中心指数(Global Financial Centres Index)中,新加坡在全球133个金融中心中排名第四,进一步巩固了其作为全球领先金融枢纽的地位。这一成就或将进一步推升对优质办公空间的需求。随着现有中央商业区发展逐渐饱和,且社会对绿色可持续发展的呼声日益高涨,滨海南的开发无疑为新加坡商务区的扩展提供了恰逢其时的契机。

滨海南:新加坡全新可持续综合社区的诞生

资料来源:市区重建局

资料来源:市区重建局

滨海南将被打造为一个集住宅、零售、酒店、办公与生活配套设施于一体的综合用途社区,各类设施皆可在10分钟步行范围内轻松抵达。根据总体规划,该区域正通过政府售地计划,由市区重建局主导转型升级。

2023年,由鑫丰集团(Kingsford Group)牵头的财团以每平方英尺每容积率(psf ppr)1402元的最高报价成功竞得滨海花园巷(Marina Gardens Lane)地块,计划建设937个住宅单位,将在2025年正式推出,成为滨海南首批亮相的地标性项目。

资料来源:鑫丰集团

紧接着在2024年1月,滨海花园弯(Marina Gardens Crescent)的一块白地地段仅收到国浩房地产(GuocoLand)牵头财团的一项报价,报价为每平方英尺每容积率984元。然而,市区重建局认为该报价未能体现土地应有价值,决定不予接受,并选择暂时保留地块。

这一决定充分彰显了市区重建局在维护国家土地资产价值方面的坚定立场与长远眼光。

结语

随着新加坡持续吸引全球企业与高端人才,滨海南将在未来城市发展的蓝图中扮演至关重要的角色。它不仅是一个现代化、绿色可持续、以人为本的社区,支撑着国家的经济增长,更是一个全新、充满活力的宜居住宅区——一个让新加坡人率先安家的地方。

如您有兴趣了解滨海南将为未来业主与租户带来哪些生活与投资机遇,欢迎随时联系 ERA 值得信赖的房产顾问,获取更多资讯!

本文中的信息仅供参考,不构成对信息的准确性、完整性或可靠性的保证。使用者应自行核实相关信息,并根据具体情况向独立的专业人士(如估价师、财务顾问、银行从业人员及律师)寻求专业意见。ERA及其销售人员对于因使用本信息而导致的任何直接或间接损失概不负责。此外,本文件受著作权法保护,ERA拥有其著作权。未经事先书面许可,任何个人或机构不得以任何形式或手段对本文件进行复制、传播或用于商业用途。

Many of us are familiar with the food and beverage industry, but have you ever wondered where your meal was made? You might be surprised to learn that it probably came from a food factory.

Food factories have been around for quite some time, primarily engaged in large-scale food production, producing wholesale products like noodles, biscuits, and other staples. Traditionally, these operations were housed in standalone factories. However, in recent years, food factories have evolved in form and function, and now come in a variety of sizes and formats.

During Covid, Singapore faced the challenge of securing essential food supplies from our neighbouring countries during to a myriad of factors, including export restrictions and panic buying. Taking a leaf from that experience, Singapore plans to fulfil 30% of its nutritional needs locally by 2030. This initiative underscores the significance and changing role of food factories as crucial infrastructure to enhance food resilience and security in the future.

Growing Demand for Food Service driving need for Food Factories

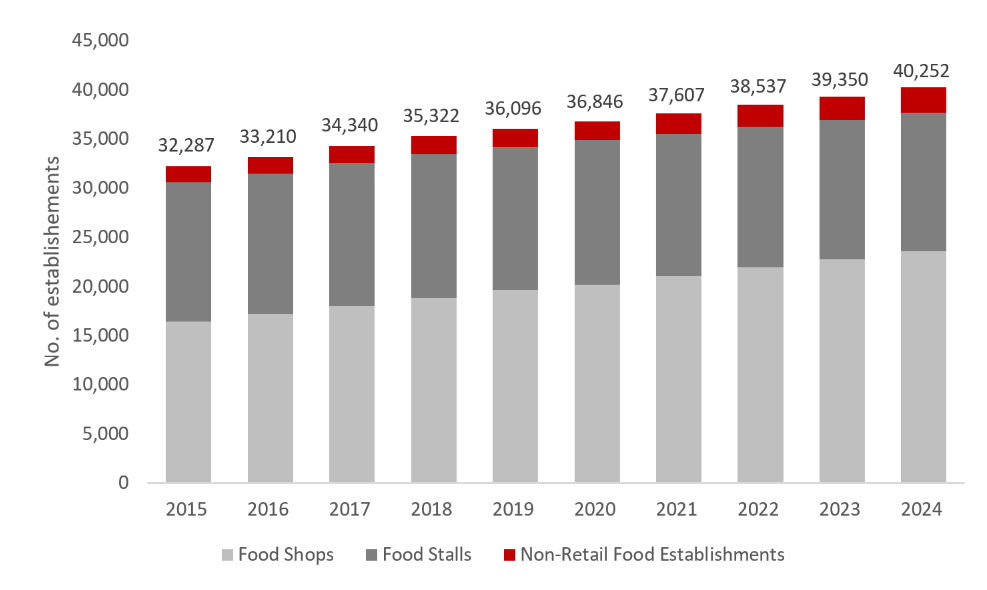

The increasing population and shifting dietary preferences have driven the growth of food and beverage (F&B) establishments throughout Singapore. Including non-retail food establishments, food shops and food stalls, Singapore reported over 40,200 such entities in 2024.

This marks a significant jump from approximately 32,300 entities seen a decade ago. Despite worries about rising closures in F&B establishment, demand for food factories is anticipated to stay strong as F&B companies consolidate their operations to centralise kitchens instead.

Chart 1: Food establishments in Singapore

Source: Singstat, ERA Research and Market Intelligence

According to the Accounting and Corporate Regulatory Authority, some 3,047 F&B business shuttered in 2024, marking the highest number of closure seen since 2005. At first glance, this may raise some concerns. However, in the long term, Singapore’s projected population growth is expected to drive demand for more F&B services, creating new opportunities for expansion and innovation in the sector.

The Changing Role of Food Factories Today

Moving from its past, food factories have discovered new functions in response to the increasing and diverse diversity demands of modern food production. This stems from changing dietary needs and a shift in eating habits that has led to higher degree of customisation, and a greater focus on small batch of food production for ready-to-eat meals.

Moreover, in light of increasing retail rents and manpower costs, many businesses are turning to central kitchens as a cost-efficient alternative. This trend has resulted in new applications for food factories such as operating as cloud kitchens. By handling the bulk of the food preparation process in a centralised location, business can execute better control over the quality and cost before distributing the product to the restaurants or café, or delivery to consumers. That said, there might be cheaper options like industrial canteens with comparable setups.

So what is driving the growing demand for centralised kitchens? This leads us to the next aspect: the necessity for stringent food safety standards.

Food Factories Designed to meet Food Safety Standards

In Singapore’s tightly regulated setting, food safety standards have come under greater scrutiny and have become more stringent. New food factories are designed to adhere to strict safety protocols set by the Singapore Food Agency. This includes the need for separate lifts for raw and cooked food, dedicated driveways for end-to-end logistics and higher electrical capacity to accommodate coldroom or automation systems.

Food factories typically operate under stricter specifications compared to traditional factories. This allows for more sophisticated installations and advanced mechanisms to meet rigorous safety and operational standards. In that way, companies can minimise food exposure and effectively lower the risk of contamination to the greatest extent possible.

Smaller Food Factories Open New Possibilities to New Ideas

In the past, some F&B operators face challenges in securing specialised spaces, that are typically much larger. Today, the emergence of smaller food factories offers increased opportunities and flexibility in the food and beverage sector.

Individuals encounter evolving dietary needs and food allergies, necessitating the production of food in small quantities, often within controlled setting.

Similarly, smaller food factories pave the way for the growth of artisanal food production, which promotes creativity and support research and development. Over time, this fuels innovation within the food industry.

A growing but limited supply of Food Factories

Although there are no official figures, the number of food factories is increasing to match the growing needs. Nonetheless, despite the emergence of new food factory developments, the overall supply remains constrained and may still fall short of meeting the market demand.

The rise of new strata food factories offers businesses the chance to secure their own food production spaces, mitigating the risks associated with rising rents and granting greater control over both capital and operational costs. This move towards ownership foster long-term stability and offers the flexibility to tailor facilities according to specific manufacturing needs.

Food Factories – The Secret Sauce to Feeding Singapore’s Future

In closing, food factories are no longer a novelty. They have transformed into a critical pillar of Singapore’s industrial landscape.

As Singapore’s population expands and consumer preferences shift towards convenience, the demand for scalable food production solutions is becoming increasingly urgent. This need is effectively addressed by consolidating operations in food factories, enabling centralised food preparation, packaging, and distribution all in one location.

Additionally, as more F&B firms seek to consolidate their operations, there is a clear preference for a centralise location to improve efficiency, manage costs and optimise labour demand. Central kitchens and food factories can help streamline operation processes, help uphold quality control, and reduced logistical challenges, making them the preferred choice for scalable food production.

Looking ahead, ERA expects the demand for food factories to remain strong, becoming essential in supporting Singapore’s food security. As food factories continue to modernise and expand, they are poised to play an even more significant role in ensuring a stable and sustainable food supply for Singapore’s future.

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.

下文由ERA公关经理岳开新翻译

尽管全球局势动荡,但新加坡经济稳定确保本地住宅市场有足够韧性来应对挑战。

2025年4月2日,美国总统特朗普在美国解放日(Liberation Day)发布了一项超出预期的关税政策,震惊全球市场。根据这一政策,除了对所有进口商品征收10%的统一基准关税外,部分国家将面临更高的关税。

美国此举的动机明确:通过调整价格竞争力,推动国内外商品之间的公平竞争,从而吸引制造业回流美国,并提振国内消费。自2001年以来,美国制造业在全球产出的占比已从28.4%下降至2023年的17.4%,而2024年,美国商品贸易逆差已达到1.2万亿美元。

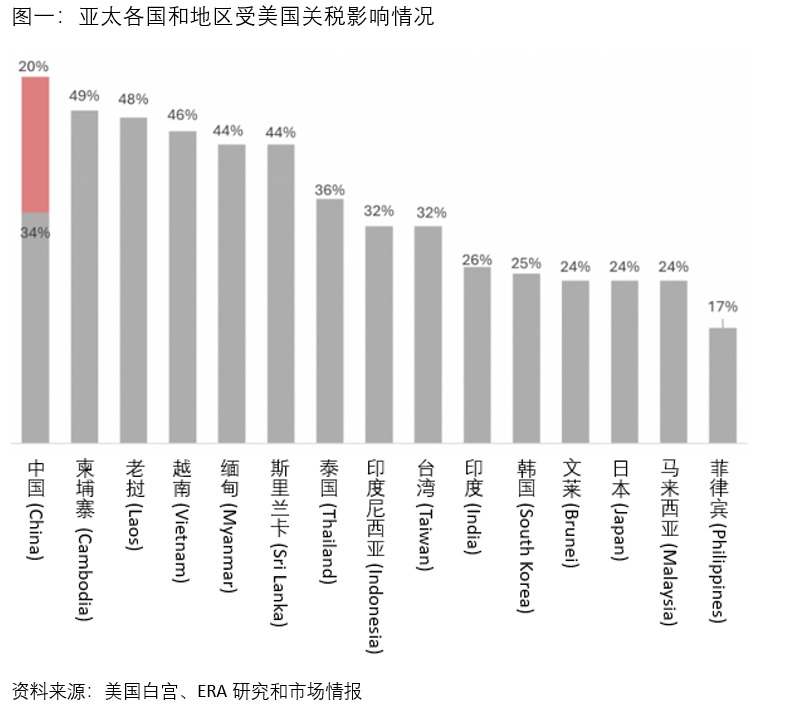

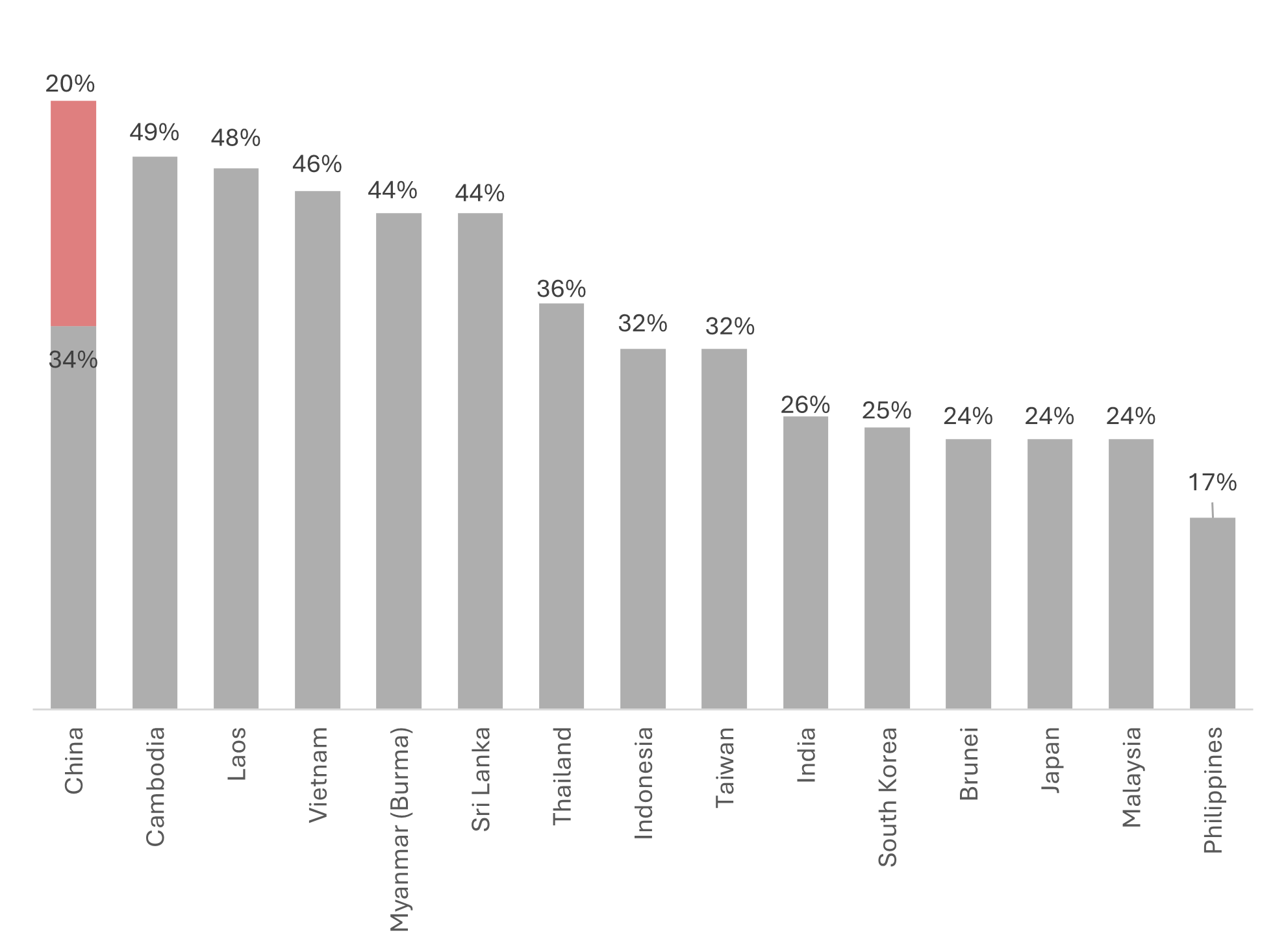

在受影响的国家中,中国是这场贸易战加剧的主要目标,除了此前已施加的20%关税外,还需再承受34%的额外关税。同时,一些东南亚国家也受到重创。例如,柬埔寨(49%)、老挝(48%)和越南(46%)是受新关税影响最为严重的市场之一。尽管新加坡不在高关税国家名单中,但我们的对美出口同样会受到10%基准关税的影响。

全球股市暴跌,美国经济可能因通货膨胀和他国报复性关税而受创

新关税政策实施后的第一个交易日,投资者的恐慌情绪引发了全球股市的暴跌,并激发了市场对经济衰退的担忧。

美国这一强硬举措迅速引发了贸易伙伴的报复性关税对策。例如,中国几乎在第一时间对所有美国进口商品加征了34%的关税。

与此同时,美国国内进口成本的上升可能加剧通货膨胀,进一步加重消费者和企业的负担。全球范围内,这可能导致贸易需求放缓,从而拖累整体经济增长。

市场的担忧会影响新加坡住宅市场吗?

在这一轮新关税中,美国对新加坡进口商品设定了10%的关税,低于其他亚太国家。此外,新加坡决定不采取报复性关税,以避免贸易战升级。尽管新关税政策带来的不确定性会对全球经济增长产生压力,而新加坡作为一个高度依赖贸易的国家,难免会受到一定影响。

但从另一个角度看,本地的房产投机可能会减少,购房者将更多地倾向于刚需和长期计划。

短期内,尽管全球经济不确定依旧存在,且贸易战升级的风险可能会抑制住宅市场的需求,但从中长期的展望来看,ERA仍保持谨慎乐观的态度。ERA认为,新加坡住宅市场本身并不具投机性,坚实的经济基本面将为中长期投资者提供稳定的增长机会。

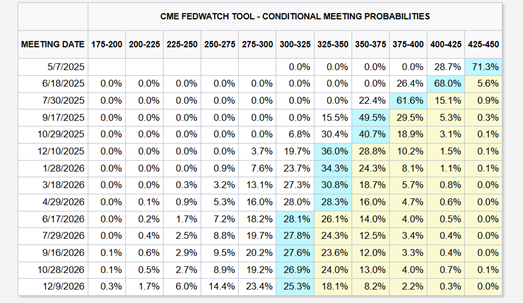

高通胀和经济增长放缓,或使美联储最多实施四次降息

根据芝加哥商品交易所集团(CME)的调查,分析师认为美联储可能在今年实施最多四次降息,主要由于贸易关税引发的更高通货膨胀和经济增长放缓。如果这一预期成真,联邦基金利率可能会降至3.25%至3.50%之间。这将有助于进一步缓解房贷利率,减轻购房者的房贷负担。

需求放缓及进口成本下降有望使建筑成本上涨趋于缓和

如果中国决定将其过剩产能转向其他国家,并以更低的价格进行出口,可能会导致亚太地区面临通缩压力。具体到建筑行业,由于中国房地产市场的放缓,国内需求减弱,钢筋价格已有所下滑。此外,美国对钢材进口加征25%关税,进一步打击了钢材需求,尤其是削弱了中国钢铁的出口。

在这样的背景下,亚太地区可能面临廉价钢材大量涌入的风险,这将有助于降低建筑材料成本。然而,建筑材料成本的下降是否能够有效缓解房价压力仍需观察。即使未来建筑成本下降,对房价的影响可能有限,因为新加坡的房价受多种因素影响,包括土地成本、劳动力成本等。

新加坡作为避风港,预计将持续吸引外国投资,这有助于保障就业并支撑住房需求。

新贸易关税的实施预计将有效遏制企业的“中国加一”(China Plus One)策略,该策略旨在降低对中国制造的依赖,并减轻贸易战带来的影响。受新政策影响,区域内许多低成本制造业可能因更高的贸易关税面临挑战。

然而,新加坡与美国始终保持着平衡互利的合作关系。2024年,美国对新加坡的货物贸易顺差达到了28亿美元,这进一步巩固了新加坡作为美国可信赖贸易伙伴的地位,可能使新加坡免于面临更苛刻的关税政策。

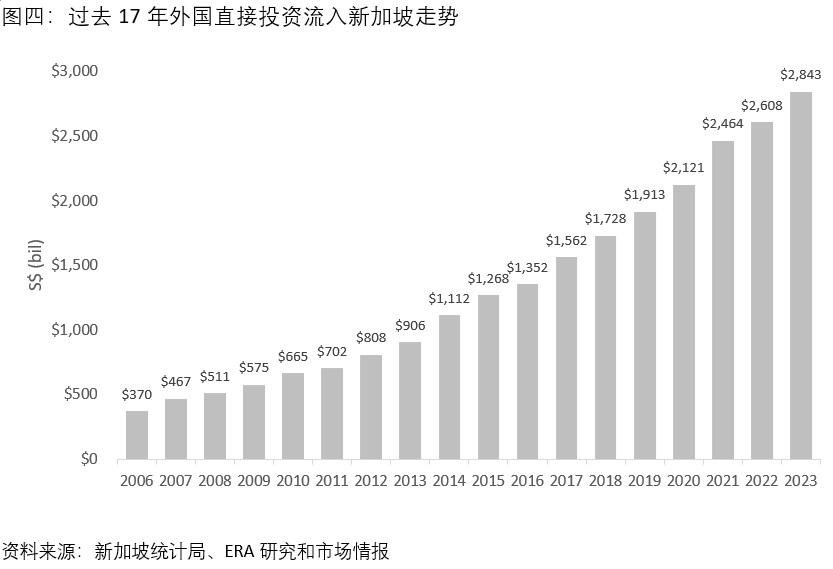

在当前形势下,寻求避风港与增长机会的区域投资者预计将继续被新加坡稳定的社会环境以及透明、开放的经济政策所吸引。这将推动外国直接投资(FDI)的持续流入,促进整体经济发展,并创造更多就业机会,进一步支撑住宅与商业地产的需求。同时,新加坡作为国际金融中心的地位以及健全的法律体系,在全球经济不确定性加剧的背景下,更加巩固了其作为投资首选地的吸引力。

新加坡多元化的经济结构和广泛的多边贸易伙伴关系有助于缓解经济冲击

新加坡多元化的经济结构和广泛的贸易伙伴网络将有效减轻个别国家贸易关税的影响。截至目前,新加坡已签署27项自由贸易协定,并将继续推动并维护与志同道合国家之间的开放、公平和自由贸易关系。

住宅市场的降温措施为应对外部冲击提供了灵活应对空间

自2010年至2024年,新加坡政府共推出了13轮降温措施,以稳定住宅市场并确保价格的可持续增长。

这些措施包括在2023年4月实施的60%的额外买家印花税(ABSD),旨在打击外国买家的投机性投资。此外,政府对购买二套房的买家征收较高的ABSD,以抑制房产的过度积累,帮助平抑房价增长,维护市场稳定。

总结

综上所述,尽管面临全球经济挑战,ERA依然对新加坡住宅市场在中长期保持积极展望。

新加坡政府已经为此奠定了坚实的基础,包括签署广泛的自由贸易协定、发展先进的基础设施以及培养高素质劳动力。这些努力为新加坡吸引持续的外国投资创造了有利条件,而外国投资是推动新加坡长期经济增长的关键驱动力,并为本地创造了大量就业机会。

住房方面,政府采取务实的措施,既能有效跟上需求增长,又能避免过度投机性资产积累。政府始终将保障住房可负担性作为核心目标,并通过可持续的价格增长实现这一目标。此外,政府实施的多轮降温措施为应对外部经济冲击提供了充足的空间,能够迅速作出反应。

总之,新加坡房地产市场建立在韧性、远见和审慎治理的基础上。ERA相信,在持续的政策支持和强劲的需求推动下,新加坡的住宅市场将继续展现增长潜力和长期价值,为购房者提供机会,也为投资者创造回报。

本文件中的信息仅供参考,不构成对信息的准确性、完整性或可靠性的保证。使用者应自行核实相关信息,并根据具体情况向独立的专业人士(如估价师、财务顾问、银行从业人员及律师)寻求专业意见。ERA及其销售人员对于因使用本信息而导致的任何直接或间接损失概不负责。此外,本文件受著作权法保护,ERA拥有其著作权。未经事先书面许可,任何个人或机构不得以任何形式或手段对本文件进行复制、传播或用于商业用途。

The world may be “shook”, but the firm economic fundamentals ensure that the Singapore’s residential market is well-positioned to weather the storm.

On Liberation Day, 2 April 2025, President Donald Trump shook the world by unveiling a higher-than-expected Reciprocal Tariff Policy. In addition to a sweeping 10% baseline trade tariff on all imports, selected countries will face steeper trade tariffs under the policy.

The implementation of this tariff policy holds clear motivations. US manufacturing has declined from 28.4% of global output in 2001 to 17.4% in 2023, while United States goods trade deficit has reached US$1.2 trillion in 2024. Through this move, President Donald Trump aims to level the playing field on pricing, which in turn, could bring manufacturing jobs back to United States and boost domestic consumption.

While China, the primary target in the deepening trade war faces a 34% tariff on top of the earlier imposed 20%, several smaller Southeast Asia Markets are also deeply impacted. Cambodia (49%), Laos (48%) and Vietnam (46%) are among the markets that are worst hit by the new tariffs. Despite not on the list of countries affected by higher tariffs, Singapore will still be subjected to the 10% baseline tariffs on our exports to the United States.

Chart 1: Asia Pacific Markets impacted by higher trade Tariffs imposed by United States

\

\

Source: The White House, ERA Research and Market Intelligence

Global stock markets plunge, while the United States could potentially face whiplash from rising inflation and retaliatory tariffs

As the trade war intensifies, uncertainty and fear among investors sent global stock markets plunging on the Monday following the implementation of the Reciprocal Tariff Policy on 5 April 2025. More importantly, these developments have sparked fears of a broader economic downturn.

This aggressive move by the United States could provoke retaliatory tariffs from trade partners, such as China, which almost instantaneously retaliated with a 34% levy on all US imports.

Meanwhile, domestically, rising import costs may fuel inflation and put further pressure on consumers and businesses in United States. Globally, this could spell slower trade demand, which could translate to slower growth.

For now, the market may be gripped by heightened volatility, but what can we expect for the Singapore residential market?

Singapore will face a moderate impact due to the lower baseline 10% trade tariff and has decided against retaliatory tariffs. However, other countries may choose to retaliate and further intensify the ongoing trade war. This heightened volatility will weigh on global economic growth, and on Singapore’s growth, given our heavy reliance on trade.

On a more positive note, residential homebuyers tend to be less speculative, often taking a medium- to long-term view of the market and are more likely to be driven by genuine housing needs.

Although uncertainty persists and the risk of an escalating trade war may dampen near-term demand in the residential market, ERA maintains a cautiously optimistic medium- to long-term outlook. ERA believes that Singapore’s residential sector is non-speculative and will continue to offer growth opportunities for investors with a medium- to long-term perspective, supported by several key fundamentals.

-

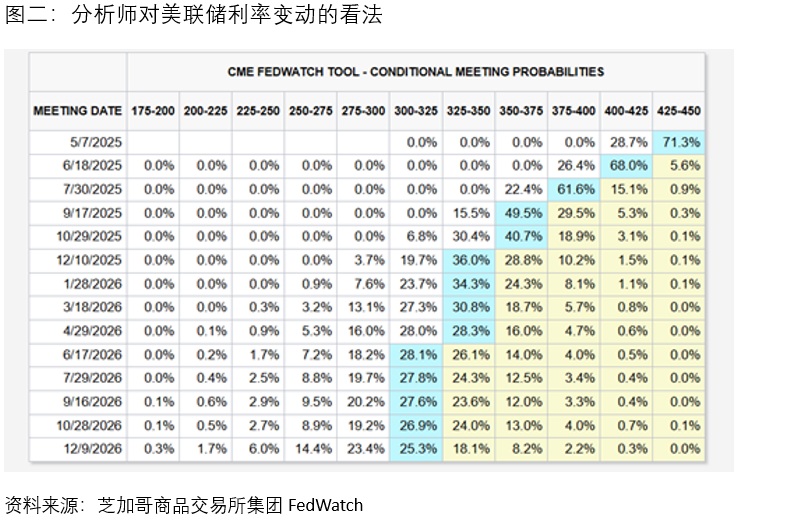

Fed could implement up to four rate cuts due to potentially “higher inflation and slower growth”

Analysts surveyed by CME Group suggest the Federal Reserve could implement up to four rate cuts in 2025, potentially driven by higher inflation and slower growth resulting from trade tariffs. Should this materialise, the federal funds rate could fall to between 3.25% and 3.50%. This could lead to a further moderation in mortgage interest rates which will help ease housing costs.

Chart 2: Analysts view on probabilities of changes to the Fed rates

Source: CME FedWatch

-

Construction cost may ease with cheaper imports ahead as demand slows

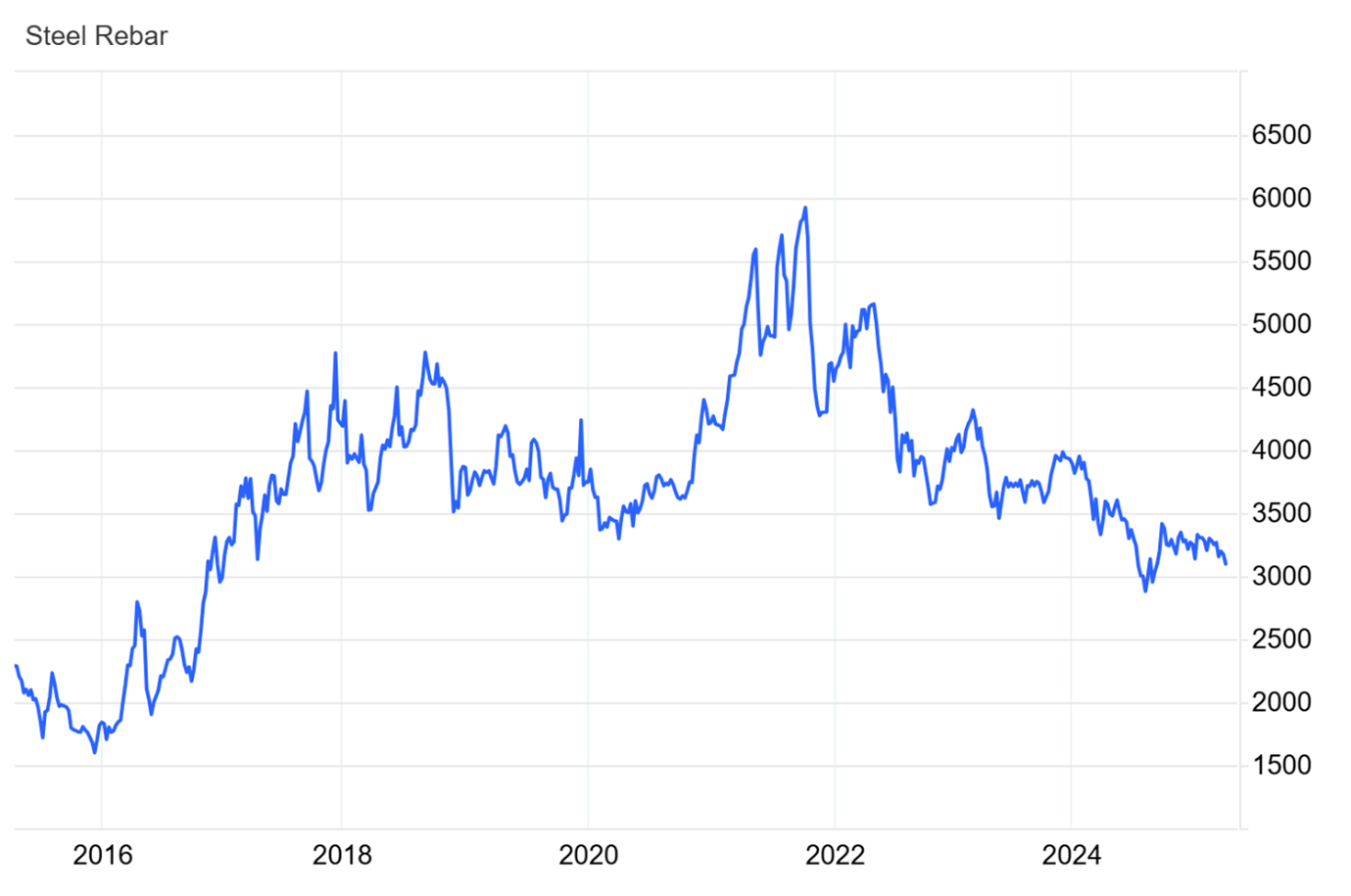

The region may face significant deflationary pressures if China decides to divert its export surpluses and flood the market with cheaper exports. Specific to the construction sector, the slowdown in China’s real estate market has led to weaker domestic demand and softer prices for steel rebar. The 25% US import tariffs are a double whammy on steel demand and could further dampen export demand for Chinese producers.

There could be a risk of a flood of cheaper steel exports in the region, driving down construction material costs. Could this mark the beginning of moderating construction material costs, thereby helping to ease housing prices? Although this might seem plausible, moderating construction costs ahead could have muted impact on housing prices, since Singapore home prices are influenced by a variety of factors including land and labour cost.

Chart 3: Steel Rebar Prices on a steady decline since late 2021 on the back of sluggish demand

Source: tradingeconomics.com

-

Singapore’s safe haven status could continue to attract foreign investments seeking growth in the region, ensuring job opportunities which can support driving housing demand

The imposition of trade tariffs is set to effectively curb the ‘China Plus One’ strategy, which is widely adopted by companies to reduce reliance on China and mitigate the impact of the trade war. Consequentially, many of the regional low-cost manufacturing hubs could face challenges due to higher trade tariffs.

Singapore, however, maintained a balanced and mutually beneficial partnership with the United States, as reinforced by the U.S. goods trade surplus with Singapore, which stood at US$2.8 billion in 2024. This underscores our position as a trusted trade ally and has likely shielded us from harsher tariff measures.

Investors in the region seeking safe havens and growth could look to Singapore, drawn by it’s relative stability, transparent and open economy. This could drive a steady influx of Foreign Direct Investment (FDI) which is instrumental in supporting job opportunities and contribute to the overall economic development of Singapore. This in turn could support demand for residential and commercial properties in Singapore. Singapore’s status as a financial hub and its robust legal framework further enhances its attractiveness in times of economic uncertainty.

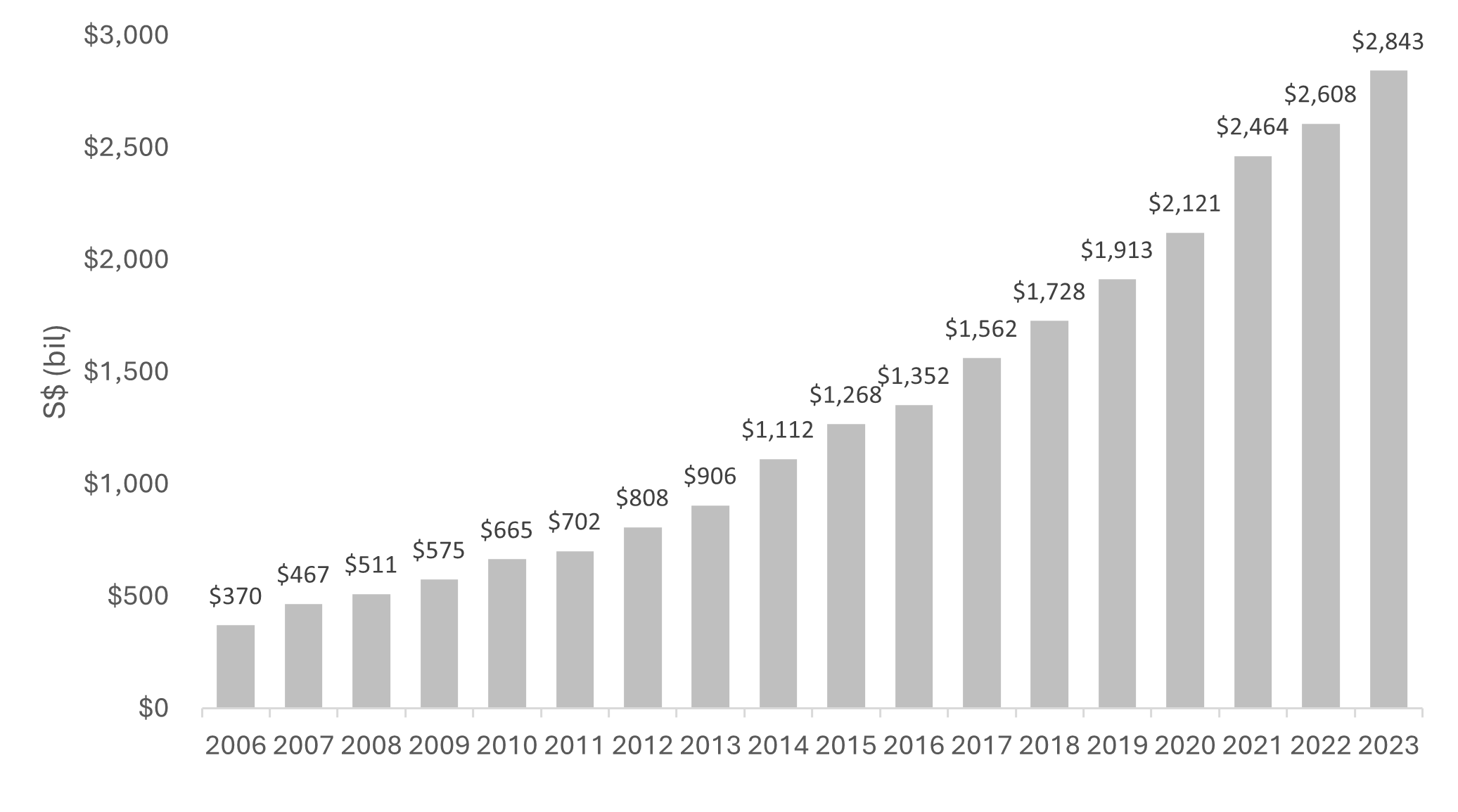

Chart 4: Steady increase in Foreign Direct Investment

Source: Singstat, ERA Research and Market Intelligence

-

Singapore’s diversified economy and extensive multilateral trade partners can help mitigate economic shocks

Singapore’s diversified economy and broad network of trade partners will mitigate the impact of individual countries’ trade tariffs. Till date, Singapore has 27 free trade agreements and will continue to pursue and uphold open, fair, and free trade among like-minded countries.

-

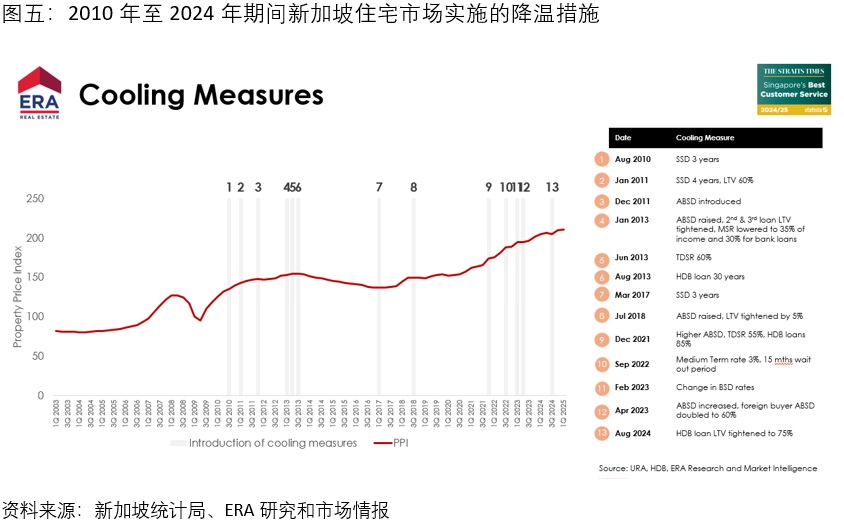

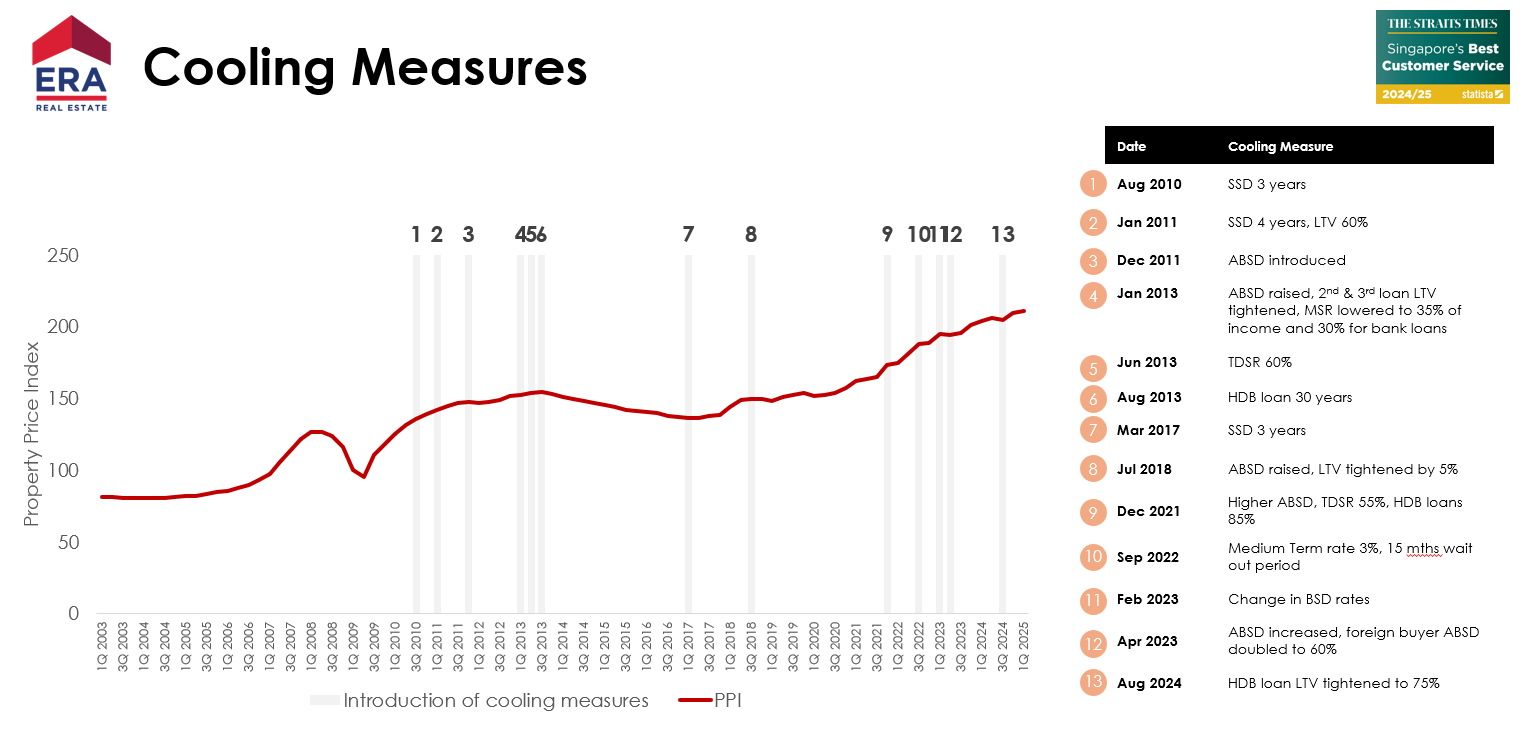

Proactive cooling measures in the residential market provide flexibility to navigate against external shocks

Between 2010 and 2024, the Singapore government introduced 13 rounds of cooling measures aimed at maintaining a stable residential market and ensuring sustainable price growth.

These measures included the significant 60% Additional Buyer’s Stamp Duty (ABSD) implemented in April 2023, targeting speculative investment from foreign buyers. Additionally, the higher Additional Buyer’s Stamp Duty (ABSD) on second homes is intended to discourage accumulation of multiple properties, helping to moderate home price growth and maintain market stability. All of this contributes to sustaining the intrinsic value of residential properties in Singapore.

Chart 5: Cooling Measures for Singapore Residential Market

Source: URA, HDB, MND, ERA Research and Market Intelligence

In conclusion

There you have it – and this is why ERA maintains a positive medium- to long-term outlook for Singapore’s residential market, even in the face of global headwinds.

Much of the groundwork has been laid by our government prior. This includes establishing extensive free trade agreements, developing sophisticated infrastructure, and nurturing a highly educated workforce. These efforts form a firm foundation that continues to attract sustained foreign investment, a key driver of Singapore’s long-term economic growth, as well as creating job opportunities.

When it comes to housing, the government takes a pragmatic approach to keep pace with demand, while being careful to discourage excessive accumulation of property assets for speculative purposes. Instead, the focus remains deeply rooted in ensuring that homes stay accessible for Singaporeans through sustainable price growth. Furthermore, the multiple rounds of cooling measures offer plenty of room for the government to respond swiftly should the property market face external shock.

In summary, Singapore’s property market is built on a foundation of resilience, foresight, and prudent governance. ERA believes that with sustained policy support and strong demand drivers, Singapore’s residential market will continue to present resilient growth potential and long-term value for both homeowners and investors.

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.

Previously, we touched on how the extension of the Central Business District Incentive (CBDI) and Strategic Development Incentive (SDI) schemes matter in the CBD’s revival, serving as catalysts for the redevelopment of older buildings in the city. In much the same way, we believe that Marina South – the extension to Singapore’s CBD – will play a pivotal role in transforming our country’s landscape.

The evolution of the CBD

1800s

Singapore’s first commercial district traces its humble beginnings to the early 19th century, where it took shape along the banks of the Singapore River. Strategically located along the Maritime Silk Road, the Singapore River quickly established its presence as one of the important free ports facilitating trades between China, India and Southeast Asia.

During this period, shophouses were built along Boat Quay, Clarke Quay, and Raffles Place to support the thriving trade and growing business community. Banks and related businesses gravitated towards the area, shaping it into Singapore’s first commercial district.

Source: Kouo Shang-Wei Collection, PictureSG, National Library, Singapore

By the early 1900’s, Singapore’s growing importance as a major port led to overcrowding in its commercial district. A lack of urban planning saw shops, houses, and factories all cramped into the same area. This led to issues like road congestion and pollution that gave rise to health and environmental concerns.

This slew of problems prompted the Singapore Government to undertake a major urban renewal program in the 1960’s and 70’s, aimed at creating a more systematic approach towards transforming Singapore’s built environment.

Through the Land Acquisition Act and the Government Land Sales (GLS) or Sale of Sites programme introduced in 1966 and 1967 respectively, the Singapore government was able to address the issues of fragmented land ownership and the need for a more regulated process for land acquisition by the private sector. Together, these changes set the stage for the development of our modern CBD.

Rethinking CBD with modern skyscrapers

With the government’s urban planning efforts laying the foundation, the next phase of development focused on modernising the CBD with high-rise office buildings. Hong Leong Building (1976), OCBC Centre (1976), UOB Plaza (1972) and Singapore Land Tower (1980) were some of the first skyscrapers in Singapore’s CBD that are still standing to this very day.

Far beyond shaping Singapore’s skyline, these office buildings played a pivotal role in meeting the real estate demands essential for supporting the growth of Singapore’s financial centre.

In the early 2000’s, Singapore continued to solidify its status a regional financial hub, leading to a significant increase in demand for office space since. As demand for offices grew, commercial properties have reported a strong growth trajectory amid tight vacancies. These assets have also proven to be valuable investment opportunities for institutional investors and private entities seeking stable returns and long-term capital appreciation.

Beyond offering excellent office infrastructure, the CBD is also supported by an extensive transport network that reaches all parts of Singapore. More importantly, it plays the role of a hub that serves Singapore’s business ecosystem by facilitating networking and trade.

In the 2024 Global Financial Centre Index, Singapore placed fourth out of 133 global financial centres, cementing its status as one of the world’s leading financial hubs. This could drive the demand for more office space within the CBD. With office space in the existing CBD becoming increasingly constrained and demand for sustainable developments rising, Marina South presents a timely expansion for Singapore’s business district.

Marina South: Birth of Singapore’s new sustainable mixed-use neighbourhood

Source: URA

Source: URA

Marina South is set to evolve into a mixed-use residential neighbourhood, featuring retail, hotels, offices, and amenities, all within a 10-minute walk. Through the GLS programme, Marina South is currently undergoing a Master Plan transformation in the hands of URA.

In 2023, a consortium led by developer Kingsford Group put in a top bid of $1,402 per square foot per plot ratio (psf ppr) for a site at Marina Gardens Lane, which will be developed into a new residential project. Set to yield 937 units, the development is expected to launch in 2025, thus setting the stage for one of Marina South’s pioneering projects.

Source: Kingsford

Subsequently, in January 2024, a white site at Marina Gardens Crescent received a single bid from a GuocoLand-led consortium at $984 psf ppr. URA rejected the bid, opting instead to hold onto the site for a fair price instead of accepting an undervalued offer.

This decision reaffirms URA’s commitment towards upholding and preserving the value of Singapore’s land.

In Conclusion

As Singapore continues to draw international businesses and talent, Marina South will play a pivotal role in shaping the future of Singapore’s urban landscape. Offering more than just a modern, sustainable, and people-centric environment that supports our city-state’s economic growth, Marina South also sets the stage for a vibrant new residential district – one that Singaporeans can be the first to call home.

Interested to know more about what the estate offer to prospective homeowners and tenants? Speak to any ERA Trusted Advisor today to find out more!

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.

This article was written in collaboration with Tay Liam Hiap, Managing Director of Capital Markets and Investment Sales.

市区重建局(URA)日前宣布将中央商业区奖励计划(CBD Incentive Scheme,简称CBDI)和策略发展项目奖励计划(Strategic Development Incentive Scheme,简称SDI)延长至2030年。这项计划于2019年推出,旨在推动楼龄至少20年的旧建筑重新开发,以提升中央商业区活力。

新加坡的城市发展日新月异,但其中仍不乏一些老旧商业建筑。在鳞次栉比的摩天大厦中,显得有些不那么协调,也已无法满足现代需求。随着建筑老化,维护成本也逐渐增加。落后的通风系统导致空气质量不佳,还可能影响员工健康。这一系列的问题,让地区焕新迫在眉睫。同时,租户也越来越青睐工作环境更舒适的优质办公空间。

两项奖励计划目标相同,但方式不一

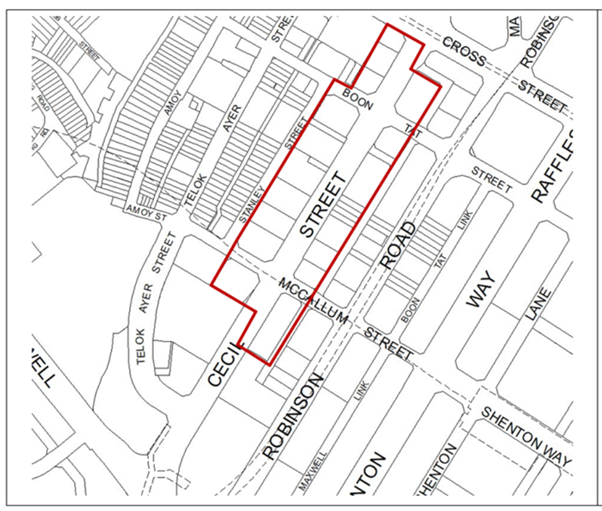

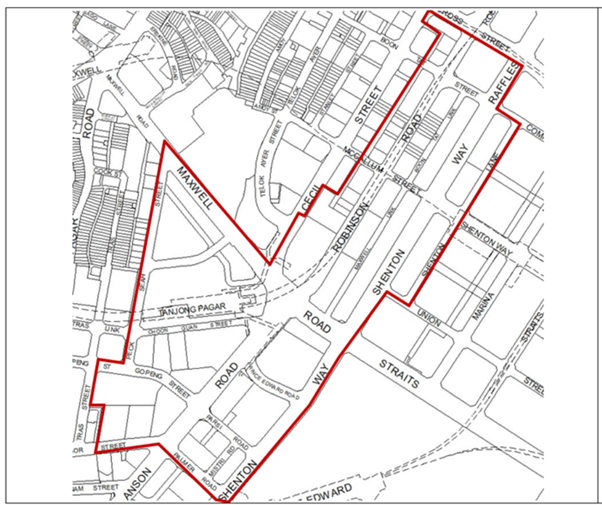

中央商业区奖励计划适用于竣工至少20年以上的办公楼,且仅限位于安顺路(Anson Road)、丝丝街(Cecil Street)、罗敏申路(Robinson Road)、珊顿大道(Shenton Way)和丹戎巴葛的指定区域(Tanjong Pagar precincts)。为了保障这些重新开发的质量,项目需满足最低地段面积(site area)要求,即1000至2000平方米,也不允许分层出售。申请成功的项目可获得额外25%至30%的总楼面面积(gross floor area,简称GFA)。

图表1: 安顺

图表2:丝丝街

图表3:罗敏申路、珊顿大道和丹戎巴葛的指定区域

此外,政府近期公布的中央商业区奖励计划2.0也进行了更新,允许安顺路和丝丝街的办公楼可将长住型服务公寓作为混合用途开发的一部分。

自2019年计划推出以来,17份申请中的14份已获得原则性批准。其中,铂海综合大厦(Newport Plaza)即前富士施乐大厦(Fuji Xerox Towers)原址、The Skywaters即安盛保险大厦(AXA Tower)原址、海德大厦(Realty Centre)、珊顿大厦(Shenton House)、安顺路51号(51 Anson Road)以及和昌路15号( 15 Hoe Chiang Road)都已获得批准。随着该计划的延长,源美大厦(GB Building)、同荣大厦(Tong Eng Building)、Cecil Court和春叶大厦(Springleaf Tower)等建筑也有望在未来加入重新开发的行列。

相比之下,策略发展项目奖励计划则是为鼓励在指定区域的旧建筑重建,地区涵盖乌节路、中央商业区奖励计划区域之外的中央商业区以及滨海中心(Marina Centre)地区。要符合此项计划的要求,无论是商业项目还是混合用途发展项目,申请建筑同样须已建成至少20年。更重要的是,重建项目必须涉及至少两个相邻的土地。

目前,12份申请中已有7份获得了原则性批准,包括誉岭峰(Union Square Residences)即中央商场(Central Mall)和市中广场(Central Square)原址、乌节路的新酒店开发项目即华峰大厦(Faber House)原址和奥迪安大厦(Odeon Towers)资产增值项目,以及voco酒店、福临购物中心(Forum The Shopping Mall)和旅店置业大厦(HPL House)的重建。

图表4:福临购物中心

奖励计划推行的局限和挑战

然而,要获得此项奖励计划也非一帆风顺,挑战之一是要在邻近地块寻找愿意共同参与重新开发的合作方,这导致一些项目夭折。其中,远东购物中心(Far East Shopping Centre)就因此而未通过。看到这些挑战和限制后,可能会让部分业主望而却步。

另一方面,尽管这些计划提供了丰厚的奖励措施,但并非所有业主都愿意参与。具体原因除高昂的开发成本外,施工带来的不便以及与其他利益相关者意见不一致等因素也消弱参与意愿。同时,许多分层地契的旧商业建筑,需经过漫长的集体出售流程,包括争得不少于八成业主同意的要求。

目前,这些旧建筑因租金较低,吸引了那些渴望留在中央商业区的中小型企业。同样,老旧的分层地契零售商场也以较低租金吸引着传统的小店铺,实惠的租金帮助它们留住为长期客户,这些客户更倾向光顾熟悉的购物环境。

然而,随着城市区域化战略的推进,中小企业可能最终会搬迁至中央商业区附近的区域,这有利于它们控制运营成本。同时,电子商务的发展和人口结构的变化,使越来越多的年轻消费者习惯通过网络和社交媒体平台购物,这可能导致传统小店铺逐渐失去市场竞争力。

图表5:远东购物中心

实施建筑项目重建与时俱进

去年9月,新加坡推行的强制能耗改善(Mandatory Energy Improvement)制度,要求总楼面面积超过5000平方米的商业建筑须进行能效审计和改进措施。这可能会促使一些旧建筑的业主考虑重新开发,尤其是那些租约即将到期的建筑。

同时,因可持续性发展报告要求的提升,公司租赁旧建筑不利于其满足可持续性指标,这也可能使它们逐步撤离。旧建筑租赁需求的下降,将影响业主整体收益率。因此,现在或许是时候考虑重新开发,以适应未来的需求。

随着更多建筑参与中央商业区奖励计划,预计中央商业区将出现更多的住宅项目。截至2024年底,第一邮区(莱佛士坊、丝丝街、滨海湾)和第二邮区(安顺、丹戎巴葛)已有超过9000个住宅单位。随着铂海综合大厦、The Skywaters、和昌路15号和51号安顺路项目的竣工,安顺-丹戎巴葛地区预计将新增超过1000个住宅、酒店和零售单位。与此同时,更新的中央商业区奖励计划2.0允许部分重建项目把商业用途与长住型服务公寓结合,这为中央商业区内的居民提供了更多住宅选择,以满足不断增长的需求。

总体来说,两项奖励计划的延长,反映了市区重建局推动本地关键战略区域的决心。中央商业区转型将进一步提升其作为居住区的吸引力,并为投资者提供资本增值机会。然而,这些计划的实施仍依赖于业主们的合作与积极参与,来克服短期挑战。重新开发这些建筑,将有助于他们的资产适应未来需求,同时推动新加坡城市的可持续发展。

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.

This article was written in collaboration with Tay Liam Hiap, Managing Director of Capital Markets and Investment Sales.

The Central Business District Incentive (CBDI) and the Strategic Development Incentive (SDI) schemes were first launched in 2019 by URA to encourage the redevelopment of older buildings in the CBD and strategic areas. One may ask: why is there the need for such schemes?

Singapore’s landscape is always changing. The CBD’s skyline, despite its modernity is still dotted with clusters of older commercial buildings that have since outlived their glory days. These developments may be less relevant to modern-day needs and may be in stark contrast to the sleeker, more modern commercial buildings. As these commercial buildings age, maintenance costs can get increasingly expensive, and poor ventilation or air quality could contribute to the sick building syndrome, impacting the well-being of occupants. All of these factors are driving the ongoing flight-to-quality trend as tenants seeks prime spaces which offer a better, more comfortable working environment.

Why the need for these schemes?

To address this, the CBDI scheme and the SDI scheme were introduced in 2019 to encourage owners to redevelop older buildings into mixed-use developments aimed at transforming the CBD into a vibrant 24/7 mixed-use district.

Same motivation but different approaches

CBDI scheme

The CBDI scheme is confined to office developments, that are at least 20 years from completion, and are within the selected parts of the Anson, Cecil Street and, Robinson Road Shenton Way, Tanjong Pagar precincts. To safeguard the quality of these redevelopments, the sites are required to meet a minimum site area (1,000 to 2,000 sqm) and are not allowed to be strata subdivided. Successful proposals could be granted an additional 25% to 30% Gross Floor Area (GFA).

In 2025, the CBD incentive scheme 2.0 was updated to allow office buildings in the Anson and Cecil Street precincts the new option to include long-stay service apartments as part of their mixed-use developments.

Picture 1: Anson

Picture 2: Cecil Street

Picture 3: Robinson Road, Shenton Way & Tanjong Pagar

Since its launch, 14 out of the 17 CBDI applications were granted in-principle approval. This includes projects such as Newport Plaza (former Fuji Xerox Towers), The Skywaters (former AXA Tower), Realty Centre, Shenton House, 51 Anson Road and 15 Hoe Chiang Road.

Following this extension, could we see developments such as GB Building, Tong Eng Building, Cecil Court, and Springleaf Tower take advantage of the scheme and undergo redevelopment in the new future?

SDI scheme

Separately, the SDI scheme is designed to encourage redevelopment of older buildings in strategic areas including Orchard Road, wider CBD areas that fall outside the designated zones for the CBDI scheme, and Marina Centre. To qualify for the SDI scheme, a development must be at least 20 years after completion, be either a commercial or mixed-use development, and more importantly, the redevelopment must involve at least two adjacent sites.

So far, the SDI Scheme has granted seven in-principle approval for 12 applications. These include Union Square (former Central Mall & Central Square), new hotel development (former Faber House and asset enhancement of Odeon Tower), and the redevelopment of voco Hotel, The Forum Mall and HPL House.

Picture 4: Forum The Shopping Mall

The requirements for the SDI scheme are stringent, and finding an adjacent site that is willing to undergo joint redevelopment can be challenging. For that reason, the Far East Shopping Centre was unable to obtain approval to redevelop under the SDI scheme. This underscores the challenges and limitations of the SDI scheme, which can discourage some older developments from pursuing redevelopment.

Picture 5: Far East Shopping Centre

Why are there not more owners taking up the schemes?

Despite the attractive incentives, not all building owners are ready to take the plunge and participate in these schemes. There is a myriad of reasons, but the more commonly cited ones includes the high cost and inconvenience of redevelopment, the complexity of the scheme (particularly in the case of the SDI scheme), and conflicting views among stakeholders regarding redevelopments. For others, it boils down to complacency, as their older assets continue to generate attractive yields since many of them were acquired years ago.

Moreover, many of the older commercial buildings in the CBD are strata-titled and the redevelopment option will entail a lengthy collective sale process whereby 80% of owners’ consensus is required.

But with a shift in demographic trends and evolving real estate needs, it may make more sense for older developments to embark on redevelopment to avoid becoming obsolete or displaced in the medium term.

The Mandatory Energy Improvement (MEI) regime implemented in September 2024, which requires energy audits and energy efficiency improvement measures to be carried out for commercial buildings with more than 5,000 sqm of gross floor area, may also prompt owners of older commercial buildings to consider the redevelopment option, especially for buildings with short remaining lease tenures.

For now, these older buildings carve their niche by offering attractive office rental rates for smaller companies who want to stay within the CBD precinct. Likewise, older strata-titled retail malls served as a haven for mom-and-pop shops where affordable rents allow them to service their long-time customers who value familiarity.

But eventually, as the broader decentralisation strategy gains stronger traction, smaller companies may see more value in relocating to regional centres which are within a short commute to the CBD. E-commerce and shift in demographic could also see the irrelevance of mom-and-pop shops, as young shoppers are increasing purchasing items through websites and social media platforms.

Furthermore, as sustainability reporting becomes more stringent, companies may avoid leasing older buildings completely due to the negative impact on their sustainability metrics.

Over time, rental demand for older buildings may decline, impacting the overall yield. Perhaps it is time to consider redevelopment and future-proofing their assets.

Could CBD become the up-and-coming residential enclave as more are projected to participate in the CBDI scheme?

As more developments participate in the CBDI scheme, we can expect to see more residential homes within the CBD. As at end-2024, District 1 (Raffles Place, Cecil, Marina, People’s Park) and District 2 (Anson, Tanjong Pagar), has over 9,000 homes.

With the completion of Newport Plaza, The Skywaters, 15 Hoe Chiang Road and 51 Anson Road, the Anson-Tanjong Pagar area could see more than 1,000 new homes, hotels and retails offerings. At the same time, with the enhanced CBDI scheme 2.0, selected redevelopment sites can opt to redevelop as commercial spaces with long-term service apartments. These initiatives will expand the residential offerings in CBD to accommodate the growing workforce. Opportunistic investors may view this as a chance to acquire a home in CBD to capitalise on potential future growth.

Picture 5: Newport Plaza

In conclusion

The extension of the CBDI and SDI schemes reflects URA’s commitment to drive rejuvenation in key strategic areas. The transformation of CBD into a vibrant mixed-use district will further enhance its appeal as a residential enclave and present astute investors the opportunity to capitalise on potential future growth. But the success of these schemes hinges on the willingness and collaboration from these owners to drive the redevelopment. Looking beyond the inconvenience, redeveloping these buildings could help owners future-proof their assets, ensuring long-term growth while supporting sustainability efforts in the Singapore urban landscape.

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.

This article was first featured on EdgeProp Singapore and was contributed by Wong Shanting, head of ERA Research and Market Intelligence.

According to Chinese astrology, the Year of the Wood Snake in 2025 could bring about transformative energy, driving reforms ahead with a mix of tension and global shake-ups. With US President Trump taking office for a second term, we are already seeing glimpses of protectionist policies that could trigger worldwide uncertainty and sweeping changes.

But as the Chinese saying goes, “危机” or crisis is where one can find opportunities within challenging circumstances. A Trump 2.0 administration suggests that the rest of the world may be gearing up for what’s ahead, with governments and markets likely to implement measures or collaborate more closely to mitigate any potential policy changes.

Slower pace of rate cuts

Following Trump’s return to the presidency, the US Federal Reserve (Fed) reiterated its cautionary stance, signalling fewer rate cuts ahead in anticipation of rising inflation in 2025. This announcement came as no surprise, given Trump’s intention to raise trade tariffs for major economies — a move that is expected to trigger inflationary pressures in the near term.

New launches spicing up with returning buyers

For the whole of 2024, developers launched some 7,500 new homes across 24 project launches, largely concentrated in the Rest of Central Region (RCR) and Outside Central Region (OCR). In 2025, we anticipate an increase in Core Central Region (CCR) launches, balancing fresh homebuying opportunities across the island and drawing more buyers into the new home market.

This boils down to the dynamics between the new home and resale markets. Since 2023, an influx of newly completed resale homes has drawn buyers away from the new home market. These homes are in pristine condition and ready to move in, making them popular with buyers who have immediate housing needs.

Abundance of BTO flats to ease HDB resale market

HDB resale prices soared 9.7% throughout 2024, driving prices higher overall. Notably, a record 1,035 million-dollar flats were sold in 2024, more than double the 469 units sold in 2023.

Despite HDB’s commitment to offering 100,000 Build-to-Order (BTO) flats between 2021 and 2025, the market continues to grapple with a housing crunch. This has pushed some buyers towards the secondary market, where tighter resale flat supply has sent prices soaring further, particularly for those in mature locations.

In response, HDB announced plans to continue developing a stable pipeline of BTO flats between 2025 and 2027, committing to launch over 50,000 flats over this period. In the long term, the higher supply of BTO flats entering the resale market will offer more resale options. This is likely to temper the price growth of resale HDB flats, steering it towards a more sustainable and manageable pace in the long term.

Key Master Plan developments stir interest in GLS sites

Continuing its push towards decentralisation, the Government is poised to introduce significant updates to the draft Master Plan 2025 on land use. This update comes at a critical juncture, addressing the evolving needs arising from technological disruptions and the ageing population, key themes that will reshape how Singaporeans live, work and play.

For starters, we are seeing the strengthening of three economic gateways in the North, East and West regions of Singapore. The Master Plan also includes introducing additional regional centres designed to drive the development of emerging industries and support job creation.

The success of these regional centres hinges on having a workforce living close to these emerging hubs, with nearby housing developments playing a pivotal role. In recent years, we have already seen a significant ramp-up in housing supply in these locations. These include new estates in Jurong and Tengah, which are strategically planned to support the growth of the Jurong Regional Centre. Similarly, housing developments near One-North and Science Park address the imbalance between industrial spaces and residential options, creating more integrated and vibrant communities in the future.

Expect heightened policy risks with pockets of opportunities

A series of better-than-expected sales at select new home launches have sparked concerns about the possibility of the Government introducing additional cooling measures to temper market activity.

While genuine upgrader demand is evident in today’s market, with many buyers welcoming the Fed’s recent cuts as a reprieve from persistently high interest rates since 2022, affordability remains constrained by the growing price quantum of new private homes.

Buyers’ fears of another round of cooling measures may prompt them to rush into the housing market prematurely due to fear of missing out (FOMO). This FOMO mentality could also trigger unnecessary urgency, as buyers become increasingly concerned about higher cash outlays in the future due to the possibility of tighter loan conditions or higher additional buyer stamp duty rates.

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.