30 Condos Completed in 2025, But Where Were the Profitable Ones?

- Egan Mah

- 8 min read

- Blog

- 26 Mar 2026

2025 saw a total of 30 private condominiums attaining their Temporary Occupation Permit (TOP). These developments were launched in 2021 or 2022, during a period marked by economic and geopolitical uncertainty, as the economy was still reeling from the impact of the COVID-19 pandemic.

Since then, private property prices have increased substantially. From 1Q 2021 to 4Q 2025, URA All-residential non-landed property price index increased by 32.5%, benefiting owners amid a strong price upcycle, primarily driven by higher land costs in the primary market.

Newly completed developments are typically highly sought after due to their longer remaining lease, new condition, while featuring modern facilities. Sellers have ridden the wave of the strong price run-up since the Covid-19 pandemic, cashing out before completion. Such properties are also attractive to buyers as they are typically more affordable than new launches. Thus, many sub-sale transactions, recorded when a buyer resells a property bought directly from the developer before completion, turned out to be highly profitable.

So, how much did sellers profit? This blog examines the transactions made in 2025 for these 30 developments.

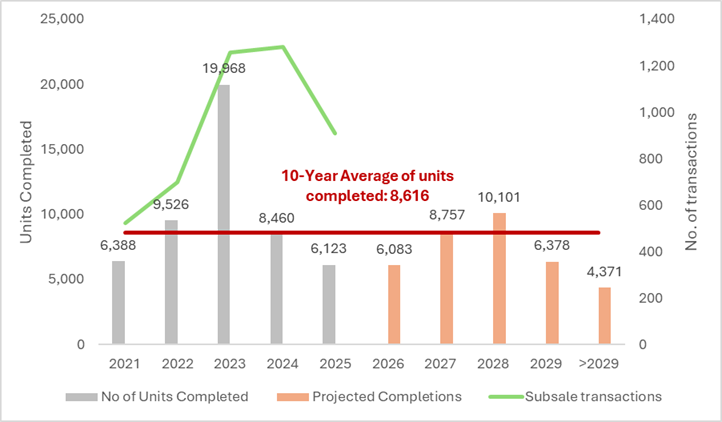

Fewer New Home Completions in 2025

2025 recorded just 6,123 new home completions across the 30 condos, marking the lowest annual supply since 2020. With the tighter pipeline of homes coming into the market, subsale transactions have been on a decline.

Among the notable developments completed are Pasir Ris 8 (OCR, 487 units) and Midtown Modern (CCR, 558 units) in 1Q 2025, Piccadilly Grand (RCR, 407 units) and Lentor Modern (OCR, 605 units) in 3Q 2025, and The Landmark (CCR, 396 units) and Tembusu Grand (RCR, 372 units) in 4Q 2025.

Chart 1: Number of subsale and units completed

Source: URA as of 1Q 2026, ERA Research and Market Intelligence

As a result of fewer completions, the smaller supply of newly completed project has driven up subsale prices. Those seeking a new home with longer lease but have urgent housing needs will have to fork out more for such homes, compared to older resale homes.

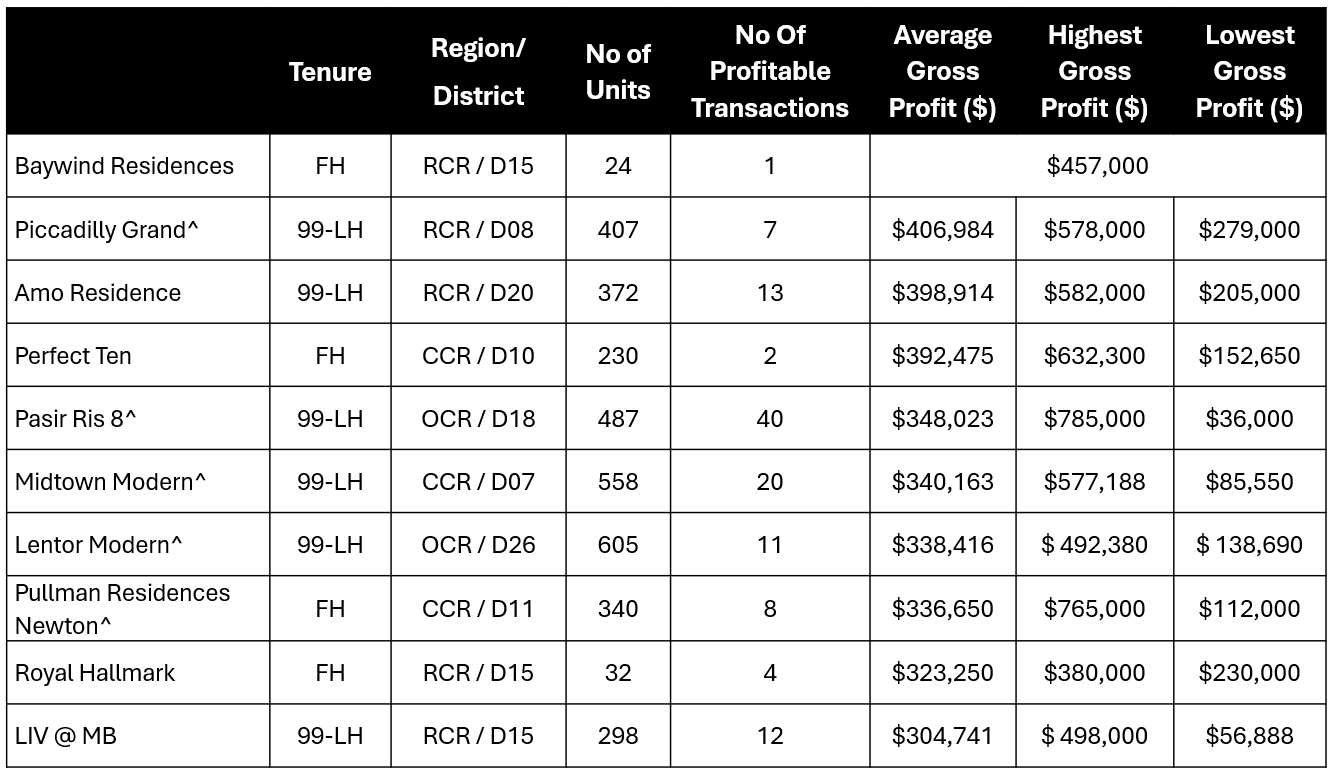

Profitable subsale developments

Table 1: Top 10 projects with the highest average gross profits in 2025

Source: URA as of 23 Jan 2026, ERA Research and Market Intelligence

^Indicates developments located in close proximity to MRT station

Popularity of homes near MRT

Of the ten projects with the highest average gross profits, five were either mixed-use developments with direct MRT access (i.e. integrated development) or are within a 5-minute walk to one. Today, convenience and connectivity are key factors that buyers look for when buying a home. As Singapore turns car-lite, car ownership is no longer a priority. Hence, buyers seek homes that are near amenities and transport nodes. The unmatched convenience and connectivity that residents enjoy typically support price growth as there is evergreen demand for such homes.

Smaller, freehold developments can be profitable too

Resale transactions is an important factor that can drive price growth. Large developments with more units typically see more transactions, allowing prices to move faster. Thus, people seldom link profitable developments to boutique developments (less than 100 units). In addition, freehold developments also typically see fewer transactions as buyers pay the premium for long-term holdings, mostly for their own occupation.

However, the numbers tell a different story. Smaller and/or freehold developments can be profitable too.

Baywind Residences and Royal Hallmark, two boutique freehold developments located in the landed enclaves Telok Kurau and Haig Road respectively, saw sellers make sizable profits. A 1,270 sqft unit at Baywind Residences was sold for $3.03 million in January 2026, after its completion in 1Q 2025. The owner profited $457,000 after holding the property for 43 months. Similarly, there were four subsale transactions at Royal Hallmark, for units between 1,130 and 1,711 sqft. The profits ranged between $230,000 and $380,000 after a holding period of 37 to 40 months.

In the CCR, Pullman Residences Newton and Perfect Ten, both with freehold tenure, saw eight and two profitable transactions respectively.

Pent up demand for homes in estates with no recent new launches

Some housing estates have not seen launches in several years. Buyers seeking to live in these estates, such as those who have family living there, or are familiar with them as it is where they grew up in would be willing to pay more due to the short supply.

For example, prior to Pasir Ris 8’s launch in 2021, the last private development launch is Coco Palms in 2014. Similarly, AMO Residences was also the first launch in Ang Mo Kio since 2014. Lentor Modern, the maiden development in the up-and-coming Lentor Hills estate was also popular among homebuyers.

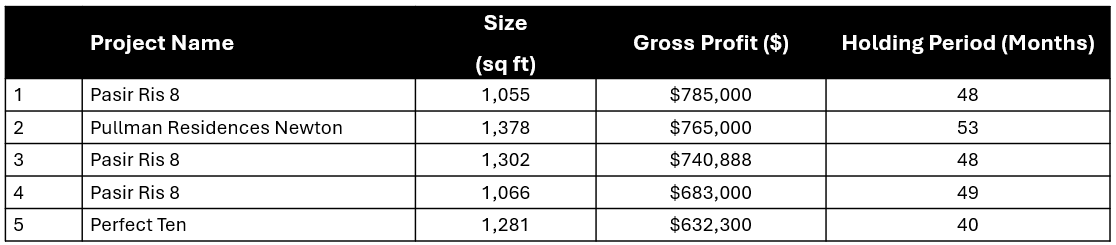

Pasir Ris 8 – The standout subsale development

Pasir Ris 8 is an integrated development comprising 487 residential units. It has direct connectivity to the mall and Pasir Ris MRT Station, part of the integrated transport hub. Buyers would likely have bought into the growth story of Pasir Ris, which station will become an interchange once the Cross-Island Line is completed in 2030. Despite being in the outskirts of Singapore, its proximity to nature (Pasir Ris Park) and employment nodes such as Changi Airport and Changi Business Park are also draws to some buyers.

The development saw 40 subsale transactions, with all of them being profitable. These 40 sellers made gross profits of between $36,000 and $785,000.

The most profitable deal was a 1,055 sqft 3-bedroom unit. The seller made $785,000 after selling the unit for $2.32 million in July 2025, 4 years after the purchased it.

Table 2: Top 5 most profitable transactions from projects that completed in 2025

Source: URA as of 23 Jan 2026, ERA Research and Market Intelligence

The ‘flipping’ strategy does not always guarantee profits

While sub-sale transactions are mostly profitable, as shown by the transactions above, it does guarantee a profit upon attaining TOP. Some property speculators, such as those buying a new launch and selling for profit upon completion may see themselves badly burnt.

While few, there are still five unprofitable transactions. Due to their small unit sizes, these sellers could be speculators, buying a smaller second property to make a quick profit.

Table 3: Loss-making subsale transactions

Source: URA as of 23 Jan 2026, ERA Research and Market Intelligence

Property is meant to be a long-term investment and requires strong holding power to ride the waves of any market unpredictability. Having a longer holding period gives a longer runway for price growth. Moreover, buyers who do not have adequate savings may find themselves also hit with Seller Stamp Duty (SSD) if sold before the minimum holding period.

Moreover, there are other factors that affects the profitability of units. For example, not all unit types, sizes and configurations can be profitable. More crucially, the entry price that you pay for your property will also determine how much profits can be made, if any.

Longer SSD Holding Period Now

In July 2025, the government announced a higher SSD rate and an extended Holding period for property owners, aiming to curb speculative demand further. This reversion to the pre-2017 SSD holding period of 4 years seeks to reduce speculative demand by decreasing the number of sellers who ‘flip’ their homes after just 3 years.

Hence, buyers seeking to profit from new home sales will be looking at a longer horizon, a different condition from the profitable projects mentioned.

Subsale transactions set to decline further in 2026 with tighter completion supply

2026 is set to see slightly fewer private home completions compared to 2025. Furthermore, Singapore’s property market is driven by genuine demand for buyers looking to buy for their own stay rather than for short-term investment gains. Hence, despite units being completed, they may not be put onto the subsale market. Additionally, with another 18 new private developments set to launch in 2026, we could also see buyers attention turning towards the new home market. Thus, subsale transactions will likely decrease further.

Nonetheless, the subsale market will continue to be supported by buyers seeking recently completed homes with modern features, longer remaining leases, urgent housing needs, and more accessible price points than new developments.

Large developments expected to attain their TOP are Grand Dunman (RCR, 1,008 units), Pinetree Hill (RCR, 520 units), and The Lakegarden Residences (OCR, 306 units). With this fresh supply of units, we could see more profitable subsale deals in 2026.

Will Subsale Properties Continue to be Profitable?

Singapore’s property market is well-established and resilient, with a proven track record. Active regulation by the government continues to drive stable and sustainable price growth. The market is also largely driven by genuine homebuyers demand, rather than for speculation. With fresh supply of sites available biennially to cater to the rising demand for homes, prices will be able to continue to grow at a stable and sustainable pace.

Hence, with stable long-term genuine demand for homes in Singapore, we could likely see prices growing in tandem with the economy. Profitable homes, particularly those newly completed, could continue to be a norm.

If you are interested to seek opportunities in the new home market, and potentially make gains too, check out this article of the 2026 new launches. Or, speak to any ERA trusted advisor today.

I confirm that I have read theprivacy policy and allow my information to be shared with this agent who may contact me later.