A Foreigner’s Guide to Buying Property in Singapore

- kwong seong ping

- 6 min read

- Blog

- 7 May 2026

A Foreigner’s Guide to Buying Property in Singapore

Singapore’s strong governance framework, political stability, and long-term economic growth make the city-state very appealing to foreign investors. However, purchasing property in Singapore as a foreigner involves a distinct set of rules, costs, and processes that differ from those faced by local buyers. It is critical for foreign buyers to understand these factors before signing on the dotted line.

Who is Considered a Foreigner

A foreigner refers specifically to individuals who are neither Singapore citizens nor Singapore permanent residents (PRs). The residency status of the buyer is important because different regulations apply to Singaporeans, PRs and foreign buyers. The two key differences are property purchase eligibility and stamp duties payable, especially Additional Buyer’s Stamp Duty (ABSD).

This regulatory framework gives Singaporean buyers priority to housing access while still controlling foreign participation in the market.

What Foreigners Can and Cannot Buy

Foreigners do not have unrestricted access to all property types in Singapore. The government imposes clear boundaries to maintain housing affordability for locals and control land ownership.

Allowed

Foreigners are allowed to purchase private non-landed residential properties i.e. private condominiums and apartments.

Restricted

Landed properties namely terrace houses, semi-detached, detached houses and GCBs require approval from the Singapore Land Authority (SLA). Approval is typically granted only under exceptional circumstances. Sentosa is the only place in Singapore where foreigners can buy a landed home without getting prior approval from the government.

Not Allowed

In general, HDB flats cannot be purchased by foreigners. The only exception is when the foreigner has a Singaporean spouse. This restriction is to ensure that public housing remains affordability for Singaporeans.

Additional Buyer’s Stamp Duty (ABSD)

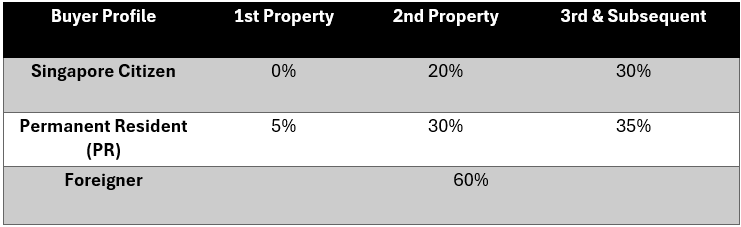

The biggest cost driver affecting foreign buyers in Singapore’s property market is the ABSD. The table below outlines the applicable stamp duty rates for each buyer profile.

Table 1: Stamp Duty Rates for Singaporeans, Permanent Residents (PRs), and Foreigners (on or after 27 April 2023)

The current ABSD rate for foreigners is 60% of the purchase price regardless of the number of residential property that the buyer owns in Singapore. This is applied on top of Buyer’s Stamp Duty (BSD), which is a tiered stamp duty that is applicable to all buyers, regardless of their nationality and the number of properties they own.

Notably, nationals or permanent residents of Iceland, Liechtenstein, Norway or Switzerland as well as nationals of the United States of America will be accorded the same stamp duty treatment as Singaporeans due to free trade agreements between Singapore and their respective countries.

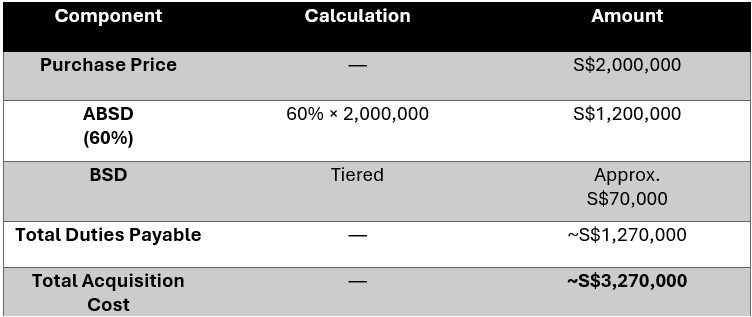

The table below illustrates the BSD and ABSD payable for a typical 3-bedroom condominium purchase by a foreigner who does not enjoy the stamp duty exemption. As the average cost for such condo units is around $2 million, we have used this price in our calculations below.

Table 2: Stamp Duty Calculation for a Foreigner Purchasing a S$2million

These two stamp duties increase the total acquisition cost significantly and requires foreign buyers to commit a substantial amount of capital upfront.

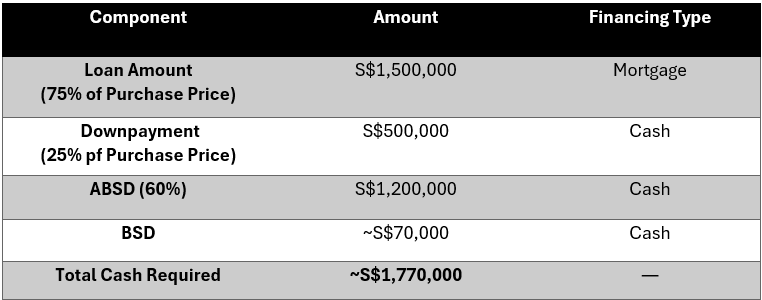

Financing and Purchasing Process for Foreign Buyer in Singapore

The typical loan structure for homebuyers of residential properties in Singapore is up to 75% Loan-to-Value (LTV), meaning the buyer must pay the remaining 25% in cash as a downpayment. In addition, buyers are required to fund the ABSD and BSD fully in cash, resulting in a significant upfront capital commitment. Buyers who are unable to do so will have to sought out a person loan which typically comes with a higher interest rate than a mortgage loan, thus adding to their financial burden.

While foreigners can obtain bank mortgages in Singapore, the loan amount and interest rates offered to them might be less generous.

Table below illustrates a typical 3-bedroom condominium finance by a foreigner in Singapore with an average price of S$2 million.

Table 3: Financing Breakdown of a S$2million Property for Foreigner

Given the large upfront cash commitments, especially for ABSD, buyers need to ensure that they have sufficient funds before committing to a property.

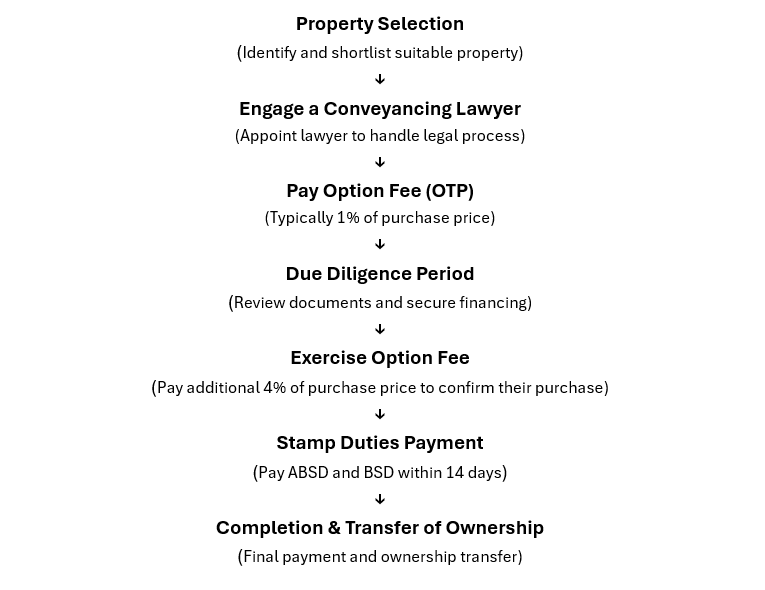

The property purchase process in Singapore is well-structured and transparent, with each step closely aligned to the financing process and timeline. As illustrated in the flowchart below, the initial option fee (Step 3) and exercise option fee (Step 5) form part of the 25% downpayment, while stamp duties payments (Step 6) must be completed shortly after the option is exercised. As such, it is critical for buyers to have their finances in place to ensure a smooth transaction.

Chart 1: Step-by-Step Process for a Foreigner Purchasing Property in Singapore

Legal representation is essential, especially for foreign buyers who may be less familiar with Singapore’s conveyancing process. The conveyancing lawyer will ensure compliance with all regulatory and contractual requirements.

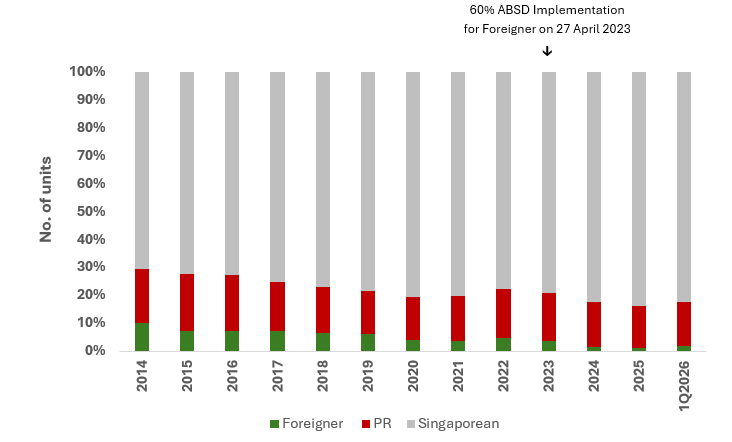

Foreign Buyer Activity Before and After ABSD Implementation

Foreign buying activity in Singapore’s property market has been greatly influenced by government policy changes, particularly the introduction of ABSD and subsequent increases in its rate. These measures have had a clear impact on foreign buyers over time. Prior to the tightening of ABSD, foreign buyers were a more visible segment of the market, especially in the private residential sector.

Chart 2: Property Transaction Trend for Singaporeans, PRs and Foreigners Buyers

However, this changed when ABSD rates were progressively increased, culminating to the 60% rate for foreigners that took effect on 27 April 2023. The sharp increase in acquisition cost has led to a noticeable decline in foreign buying activity. This is reflected in the transaction share, which drastically fell from 3.5% in 2023 to 1.4% in 2024, before falling further to 1.2% in 2025. Although it edged up slightly to 1.8% in 1Q2026, it remains well below the levels recorded in the years prior to the ABSD hike, suggesting that foreign demand has remained subdued since the higher rates took effect.

In the current market, foreign buyers tend to be high-net-worth individuals (HNWIs) who are less affected by financing constraints and more focused on long-term investment. Rather than targeting broad segments of the market, they are more likely to concentrate on prime districts and well-located assets that offer stronger potential for capital preservation and appreciation.

In conclusion, buying property in Singapore as a foreigner is relatively straightforward and transparent in terms of process, but is more complex when it comes to costs and regulations. While the market offers strong fundamentals such as stability and long-term growth, measures like ABSD significantly increase the overall acquisition cost. As a result, foreign buyers who enter the Singapore property market are likely to take a more measured approach, focusing on long-term capital preservation and appreciation rather than short-term gains.

These restrictions are intentional and serve clear policy objectives. The higher stamp duties for foreigners help curb speculative demand, reducing the risk of excessive price volatility and supporting market stability.

Overall, Singapore takes a balanced approach by allowing foreign investment while keeping it carefully regulated. This ensures the market remains attractive to global investors, while still safeguarding housing affordability for locals. Given the large capital outlay, it is important for buyers to be well-informed and take a long-term perspective.

I confirm that I have read theprivacy policy and allow my information to be shared with this agent who may contact me later.