ERA’s Wishlist for Budget 2026

- ERA Singapore

- 10 min read

- Blog

- 15 Jan 2026

Today, Singapore’s property market is reflective of genuine buyers’ demand. The continued residential property price growth is indicative of deeper concerns around the real estate market. The 2025 ERA’s “My Dream Home Survey” revealed that while 75% of respondents are positively satisfied with their current housing arrangements, many still aspire to upgrade but remain concerned about affordability. As we approach Budget 2026, ERA wishes to share our wish-list of changes to make housing for Singaporeans more sustainable and accessible. As announced by the Ministry of Finance, the 2026 Budget Statement will be delivered on 12 February 2026.

HDB policies in recent years, such as the reclassification of HDB flats into Standard, Plus, and Prime flats, as well as opening applications for 2-room flats to singles islandwide, has made public housing more accessible than ever. However, more Build-To-Order (BTO) and Sale of Balance Flats (SBF) released in 2025 resulted in a slower price growth with more options for homebuyers.

Nonetheless, many Singaporeans still have strong aspirations to upgrade to private homes. Private homes suit the lifestyle of most Singaporeans while hedging against economic uncertainty, making them aspirational assets for Singaporeans to pursue. However, rising private home prices (pushed up by increasing land and development costs) are fueling concerns around future upgrading possibilities.

On another front, it has been a challenging year for residential en-bloc and the new home segment. The bumper supply of GLS sites since 2023 offered developers an ample supply of residential sites across existing and new housing estates and precincts. As a result, en-bloc sites have become comparatively less attractive due to the complexities, risks involved, administrative challenges, and time taken. This affects progress towards the rejuvenation of our urban skyline and effort to modernise dated buildings.

With the higher cost of replacement homes, further aggravated for foreign owners who are subject to the 60% ABSD on their home purchase, en-bloc sellers demand for increasingly higher prices during the en-bloc attempts. However, this hampers the success of en-bloc sales and over time, hampers the rejuvenation of the housing landscape as residential projects continue to age.

Nevertheless, these challenges and difficulties faced in the previous year were navigated amidst a backdrop of solid market fundamentals, prudent local buyers and a well-regulated housing environment. Like any dynamic and forward-thinking society, challenges exist to catalyse progress and innovation. As we look ahead into 2026, here is a considered Wishlist of policies and initiatives that could be put forth in Budget 2026 to ensure that Singapore’s property market continues to thrive and stay resilient in a sustainable manner.

Good time to relook measures now that price growth has stabilised

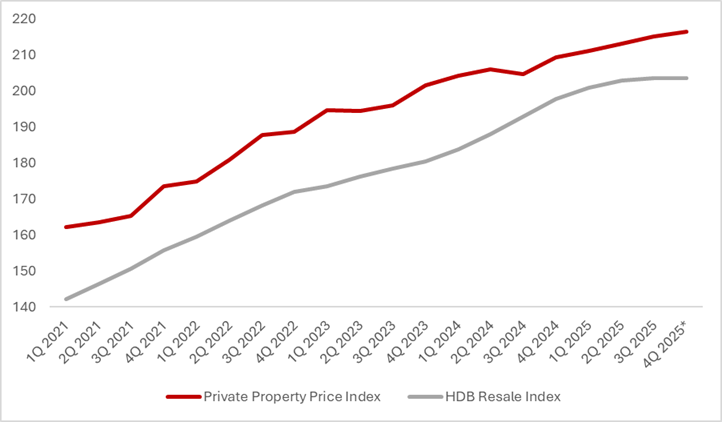

With property price growth stabilising in 2025, it could perhaps represent an opportune time to relook into the ABSD regime. The full year growth in 2025 was a more moderate 3.4%, compared to 3.9% in 2024. This marked the lowest rate of increase since 2020.

For HDB resale prices, full year growth has slowed significantly, from 9.7% in 2024 to 2.9% in 2025, based on flash estimates. It also represents the slowest price growth since 2019.

Chart 1: Price growth of private properties and HDB resale flats

Source: HDB, URA, ERA Research and Market Intelligence *Based on flash estimates

Lifting of the 15-month wait-out period for downgrading private property owners

With HDB resale price growing at a more sustainable pace in 2025, it may be timely for HDB to consider reducing the wait-out period or lifting it altogether, especially if the moderation continues.

The measure, introduced in October 2022, was intended to promote more sustainable market conditions. Since then, price growth has stabilised, suggesting that its objectives may have been largely met. With Minister for National Development Chee Hong Tat having hinted that this condition could be removed before 2027, a recalibration of the policy may be on the horizon.

ABSD Regime:

Differentiating between genuine homebuyers and investors

Singapore’s government has ensured a well-regulated market through active intervention. Cooling measures, such as the Additional Buyers’ Stamp Duty (ABSD), Total Debt Servicing Ratio (TDSR) and Mortgage Servicing Ratio (MSR) for HDB buyers, are periodically tightened and loosened to curb speculative demand. This ensures stable and sustainable growth in prices in the long-term, preventing unmitigated spikes and dips.

One possible suggestion is to differentiate between genuine homebuyers and investors. This will allow genuine homebuyers to upgrade or right-size more easily, making housing more accessible.

The existing ABSD remission applies only to married couples and seniors; and one needs to pay ABSD upfront then apply for refund later.

Removal of ABSD to facilitate homeowners upgrading from HDB to private homes

For a Singaporean family that genuinely want to upgrade from their HDB flat to a $2 million private residential property (and eventually just own that one private residential property), the current ABSD regime requires them to sell their HDB flat before buying the private residential property or pay $400,000 ABSD first should they decide to buy first then sell. This stronger the aspirations of Singaporean household who wishes to live in a private property.

Thus, ERA proposes that Singaporean households upgrading from an HDB flat to a private residential property (whether new or resale) could be allowed to defer ABSD, provided they sell their HDB within a stipulated timeframe of 6 to 9 months after taking possession of the private property. This grace period would account for renovation works and relocation logistics.

If the HDB is not sold within this window, ABSD would then be imposed on the private property, along with a penalty determined by the authorities. This ensures the scheme supports genuine owner-occupiers, while discouraging property hoarding or speculative behaviour.

This suggestion is similar to HDB flat owners who move to another HDB flat, or are upgrading to a new EC. This allows them to continue living in their current homes, without the need to rent in the meantime.

Property investors who seek to own multiple properties will still be liable for the full ABSD.

Removal of ABSD for Private Property Owners Right-sizing to a HDB Resale Flat

Similarly, Singaporean households that own one private property and are right-sizing to an HDB resale flat could be allowed to purchase the HDB first, with a 6 to 9-month window to dispose of their private property. This would allow time for renovations and a smoother transition.

Such an arrangement would reduce friction for genuine owner-occupiers, particularly older households or families looking to downgrade, while still preserving the integrity of the ABSD framework.

ABSD for Foreigners:

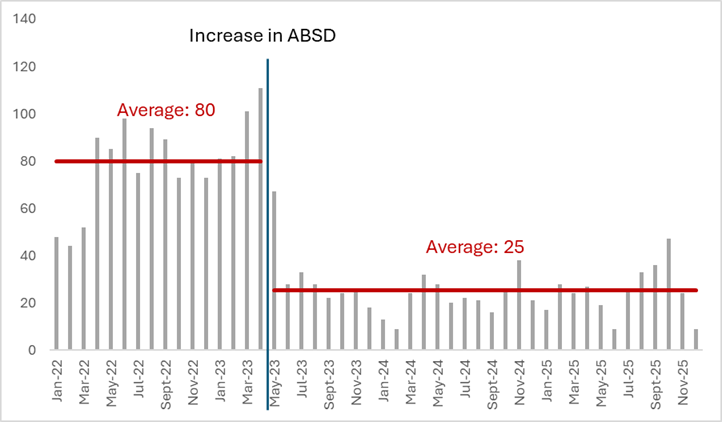

Reduction of the ABSD for foreign buyers to between 30% and 60%.

Prior to the increase in ABSD in April 2023, there was an average of 80 foreign buyer transactions per month. Since then, the average transactions fell to just 25 monthly. This is evident that the current market 60% rate might be a bit too harsh for most buyers.

Chat 2: Number of Foreign Buyers

Source: URA as of 13 Jan 2026, ERA Research and Market Intelligence

A prudent approach may be to gradually and carefully recalibrate ABSD rates for foreigners as price growth moderates towards more sustainable levels. The key is to strike a middle ground between the current 60% rate and the previous 30% rate, an approach that ERA had already proposed in last year’s Budget Wishlist.

This could help meet genuine home-buying demand from foreigners who are unable to obtain PR status and are ineligible to purchase public housing. In exchange for a lower ABSD, additional safeguards could be considered, such as a longer seller’s stamp duty holding period or restrictions on renting out the property, similar to the framework for Sentosa Cove landed homes, to discourage speculative activity. For those looking to stay in Singapore in the long-term, this move could help alleviate some cost pressures.

Reduction of the ABSD for Sentosa Cove

A more differentiated ABSD approach could also be considered for niche segments such as Sentosa Cove, where demand is largely driven by foreign buyers and expatriate tenants who prioritise exclusivity. Singaporean buyers, on the other hand, prioritises practicality and would prefer homes nearer everyday conveniences such as schools, MRT connectivity and neighbourhood amenities. Hence, homes in Sentosa operate in a very different demand segment and do not have a meaningful spillover effect on the broader housing market.

As such, a targeted reduction, or even removal of ABSD for Sentosa properties could be considered without materially affecting the wider residential market. Foreign purchases in this enclave are unlikely to push up mass-market or even core central region prices, given the highly specialised nature of demand. Instead, such a move could help revive activity in a structurally subdued niche segment, without undermining broader affordability objectives.

Adjustments to Executive Condominiums (EC) criteria to ensure better affordability

Despite the 30% MSR and the $16,000 household income ceiling, demand for ECs has remained resilient, as they continue to be more affordable than new private homes. This is reflected in healthy take-up rates at recent launches, even as prices have risen — with the median price of new ECs increasing by 47.4%, from $1,175 psf in 2021 to $1,732 psf in 2025.

Based on the maximum household income ceiling of $16,000, EC buyers can only borrow a maximum of around $1 million from the banks. With new EC prices ranging $1.3m to $1.8m, most new EC buyers must come up with significant cash to fund their purchase. This may lead to unnecessary actions like getting the parents to chip in or taking additional unsecured loans.

Adjusting both the MSR and income ceiling could broaden the pool of eligible buyers and increase demand for ECs, which has already been high despite higher prices. Moreover, this may also intensify competition for EC sites, encouraging developers to bid more aggressively. Over time, higher land costs could translate into further upward pressure on prices. Hence, it is unwise to increase both the MSR and income ceiling at the same time.

Instead, to preserve affordability, ERA suggests a modest rise in the income ceiling but leaves the MSR rate of 30% unchanged to encourage prudence. This is to ensure ECs continue to be affordable pathway for middle-income households to improve their living standards.

Change in en-bloc rules for rejuvenation efforts and greater housing supply

Lower en-bloc threshold for older developments

This will encourage rejuvenation of older strata developments which may be increasingly becoming an eyesore or even have safety risks as the physical condition of the development deteriorate over time.

Lowering the 80% consent threshold for private developments could provide some support to the en-bloc market, which has been subdued in recent years. It may better facilitate urban renewal and more efficient land use, while reducing the likelihood that a small minority will hold up collective sales to secure higher proceeds. For many owners in ageing developments, this could also offer a pathway to unlock the value of their homes, especially as maintenance costs continue to rise with wear and tear. That said, any adjustment would need to be carefully calibrated to ensure that minority owners’ interests are still adequately protected.

Longer ABSD remission deadline for larger en-bloc sites

Instead of extending ABSD remission deadlines across the board for larger sites, a more targeted approach could be considered. For instance, longer remission timelines could be applied specifically to sites acquired through collective sales. This would provide developers with greater certainty and flexibility, potentially encouraging more bids for large en-bloc sites capable of yielding over 1,000 units.

Such mega-developments typically involve extensive demolition, reconstruction and infrastructure coordination. In some cases, agencies such as BCA or LTA may also require supporting works, for example, new access roads or transport linkages, which add to project complexity and lengthen development timelines. These additional layers of planning and consultancy naturally take time.

A longer ABSD remission window for en-bloc sites could help revive the currently subdued collective sale market and support URA’s broader push for urban renewal, particularly for ageing developments that may no longer meet modern living standards.

Beyond GLS Confirmed List sites, a healthier en-bloc market would also expand the pool of available land, especially in estates with no vacant new sites. This could ease aggressive bidding behaviour, support a more sustainable pace of price growth, and inject fresh supply into the market, while delivering newer, better-designed homes that meet evolving lifestyle needs.

I confirm that I have read theprivacy policy and allow my information to be shared with this agent who may contact me later.