From Portfolio to Property: How Investing Bridges the Gap to Your Dream Home

- Egan Mah

- 5 min read

- Blog

- 22 Jan 2026

This article is written in collaboration with StashAway, a leading digital wealth management platform

Buying a home is among life’s biggest milestones. Eventually, nearly everyone will want to buy a place of their own. A new home represents a fresh start to newlyweds, a place to create memories with your children, or just a place for yourself.

Whether it is to buy your first home, or upgrading to your dream home, financial planning is crucial. Beyond putting down your initial down payment, having adequate savings and investments can also help to ensure financial freedom to upgrade and a comfortable lifestyle.

Why Singaporeans Believes in Buying Property

Historically, Singapore’s property market has been supported by consistent economic growth and the country’s capacity to attract long-term foreign investment. Properties are traditionally viewed as safe-haven assets due to their relative stability, making them the default choice for wealth preservation for many Singaporeans. A homeownership rate of 91% (as of 2024) is testament to the Singaporean’s love of property.

Affordability is often the largest stumbling block when it comes to property. Prices have gained significantly since 2021, driven by the surge in demand and shortage of new homes built as a result of the COVID-19 pandemic. Between 3Q 2021 to 3Q 2025, non-landed private homes and HDB resale prices have risen 30% and 35% respectively.

Table 1: HDB Prices in 4Q 2025

Price Range ($) - BTO (October 2025) | |||

3-room | 4-room | 5-room | |

Standard | $295,000 - $448,000 | $344,000 - $624,000 | $466,000 - $857,000 |

Plus | $340,000 - $434,000 | $514,000 - $650,000 | N.a |

Prime | $408,000 - $552,000 | $541,000 - $778,000 | N.A |

Average Price ($) - Resale | |||

3-room | 4-room | 5-room | |

Mature Estate | $474,000 | $772,000 | $937,000 |

Non-mature Estate | $457,000 | $604,000 | $714,000 |

Source: HDB as of 8 Jan 2026, ERA Research and Market Intelligence *Rounded to the nearest ‘000

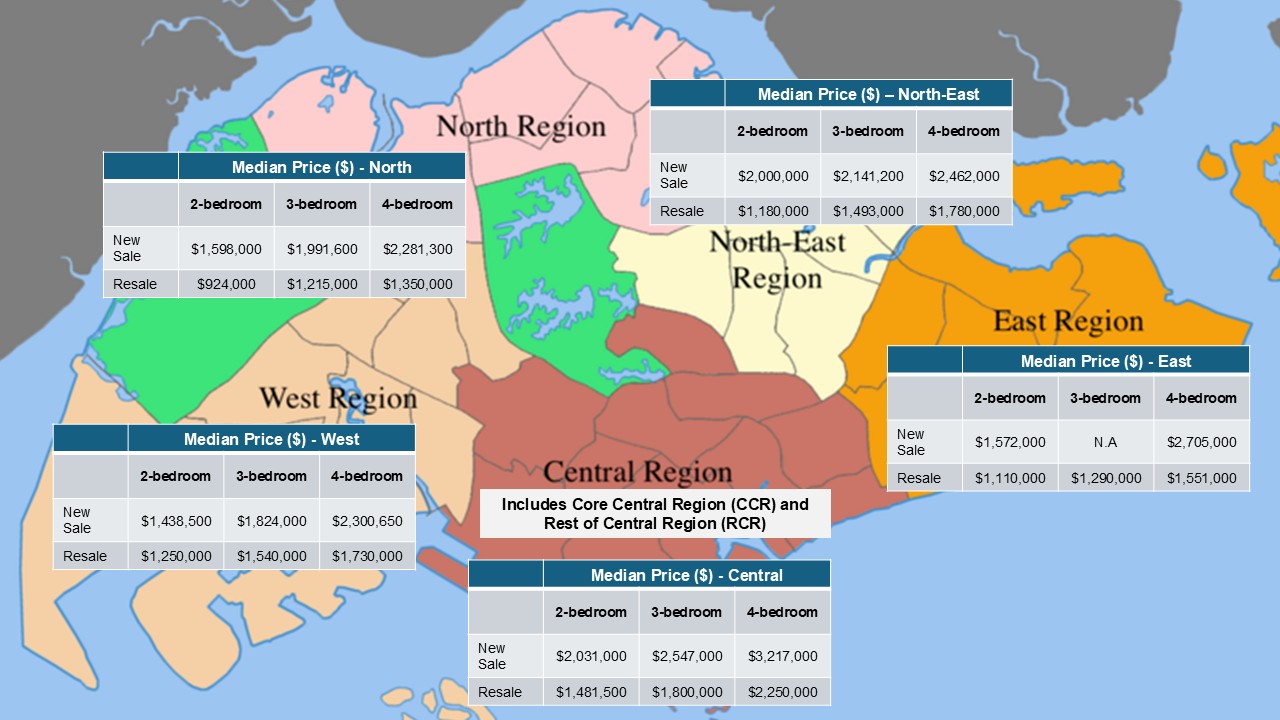

Image 1: Median Private Property Prices in 4Q 2025

*Assumptions: 2 Bedroom: 600 - 800 sqft; 3-bedroom: 800 – 1,000 sqft; 4-bedroom: 1,000 – 1,200 sqft

In Singapore, a property purchase will require a minimum of 25% down payment in addition to legal fees and Buyer Stamp Duties (BSD). For a $2 million property, the BSD payable is $69,600. This takes the minimum total down payment required to be $572,600 for $2 million property. Singapore Permanent Residents (SPRs) and foreign buyers are required to pay Additional Buyer’s Stamp Duty (ABSD) of 5% and 60% respectively. For a $2 million property, this translates to $100,000 for PRs and $1.2 million for foreign buyers.

Table 2: Costs of purchasing a home in Singapore

Property Value | Buyer Stamp Duty | 25% Downpayment* | Legal Fees^ | Total Capital Outlay |

$500,000 | $9,600 | $125,000 | $3,000 | $137,600 |

$750,000 | $17,100 | $187,500 | $3,000 | $207,600 |

$1,000,000 | $24,600 | $250,000 | $3,000 | $277,600 |

$1,500,000 | $44,600 | $375,000 | $3,000 | $422,600 |

$2,000,000 | $69,600 | $500,000 | $3,000 | $572,600 |

$2,500,000 | $94,600 | $625,000 | $3,000 | $722,600 |

$3,000,000 | $119,600 | $750,000 | $3,000 | $872,600 |

$3,500,000 | $149,600 | $875,000 | $3,000 | $1,027,600 |

$4,000,000 | $179,600 | $1,000,000 | $3,000 | $1,182,600 |

$4,500,000 | $209,600 | $1,125,000 | $3,000 | $1,337,600 |

$5,000,000 | $239,600 | $1,250,000 | $3,000 | $1,492,600 |

Source: ERA Research and Market Intelligence

*Based on minimum down payment ^Estimated amount.

The Importance of Early Financial Planning

To achieve your dream home, saving alone won’t be enough. Even disciplined savers may find it difficult to keep pace with rising home prices if their wealth isn’t keeping up with inflation. At 3% annual inflation, $100 today will have the purchasing power of roughly $86 in five years and $74 in ten years. Cash sitting in a savings account earning 0.5% loses purchasing power every year.

Investing bridges that gap. By allowing your capital to work harder over time, investing directly supports your bigger goals, like building a down payment. Starting early also means a longer runway to grow wealth, leveraging on the power of compounding.

Start with $10,000 at age 25 and add $500 monthly. At 11% annual returns (the average return for the S&P 500 over the past 20 years) you will have roughly $1.7 million by 55! Simply put, letting your cash sit idle while you save for a property down payment represents a real opportunity cost.

Access to investing has never been easier. Modern investment platforms let anyone start with minimal capital. You can easily customise your portfolio based on your risk tolerance and preferences for different asset types and markets, and the whole process can also be automated in a few clicks, with recurring payments and scheduled deposits.

Choosing the Right Portfolio and Investing Strategy

A well-constructed investment strategy aims to balance growth and stability. Long-term market data shows that staying invested through different market cycles has historically helped investors grow their wealth.

The tradeoff is volatility. After all, markets do not move in straight lines. Diversification is key to managing that risk. By spreading investments across different asset classes (such as equities or bonds) and geographies, you reduce reliance on any single market.

This is where a structured, long-term investing approach can support your homeownership goals. General Investing by StashAway is designed as a core wealth-building solution. It combines global diversification informed by our systematic investment framework, ERAA®.

Rather than a one-size-fits-all approach, General Investing portfolios are tailored to different risk profiles and adapt across varying market environments. This lets you stay invested with confidence, knowing that your portfolio is built for long-term wealth accumulation rather than short-term speculation.

If you’re starting out, consider setting up a recurring dollar-cost averaging (DCA) plan, such as investing $500 to $1,000 a month. Investing regularly over time smooths out market and exchange-rate fluctuations, reduces the risk of investing at market peaks, and makes it easier to stay disciplined on your investment (and home ownership) journey.

Build Your Foundation

Ultimately, whether your goal is a first home, an upgrade, or a “forever home”, starting early and investing consistently can make a meaningful difference. By combining saving with long-term investing, you can build greater financial resilience and put yourself in a better position to turn your homeownership aspirations into reality.

Agents: Receive a S$100 cash rebate when you place a qualifying deposit into any eligible StashAway portfolio. Find out more here: https://www.stashaway.sg/ref/era-agent

Clients: Enjoy up to S$50,000 of free investing for 3 months when you invest with StashAway. Find out more here: https://www.stashaway.sg/ref/era-client

I confirm that I have read theprivacy policy and allow my information to be shared with this agent who may contact me later.