Good Selection of Homes to be Launched in 2026. There is Something for Everyone and Every Budget.

- Egan Mah

- 5 min read

- Blog

- 12 Mar 2026

Strong new home sales performance in 2025

2025 was a stellar year for the private home market, largely driven by strong performance in new home sales. With a rosy economic outlook and a low-interest-rate environment, buyers were quick to enter the fray when developers launched new developments. Moreover, rising HDB prices also enabled HDB owners to upgrade to private property.

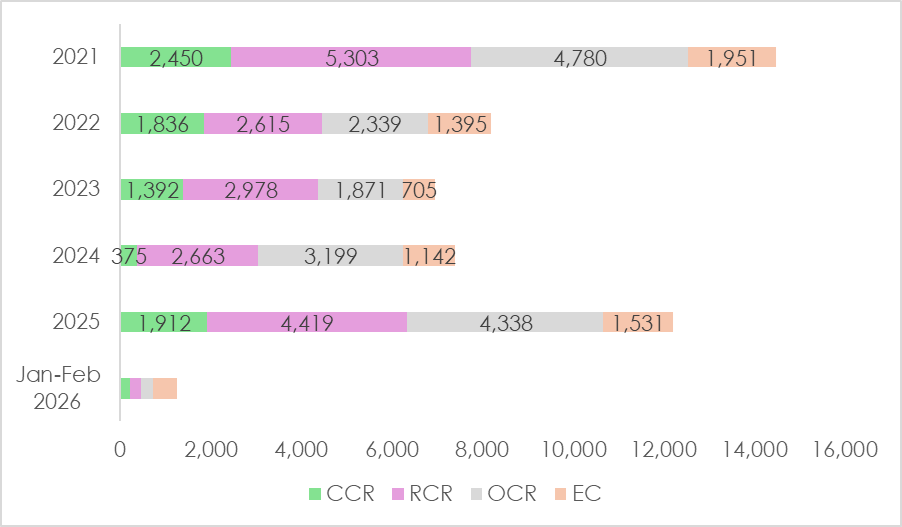

This comes as more units launched in 2025 attracted homebuyers’ interest. In particular, launches at locations that either experienced a pause in new supply or welcomed their inaugural project saw strong pent-up demand. The Core Central Region (CCR) also experienced a recovery, with over 4,600 units launched, about 75% more than in 2024. As a result, new home transactions exceeded 10,000 units for the first time since 2021.

Out of the 26 launches in 2025, 17 had more than half their units sold during launch weekend, with 11 projects surpassing an 80% take-up rate.

Chart 1: New home units sold, including Executive Condominiums (ECs)

This momentum has continued into 2026, as previously forecasted by ERA Singapore. Strong demand for new homes has carried over into this year’s launches. Projects launched in the first quarter of 2026 have performed well, including River Modern, which sold 90% of its units at launch, as well as Coastal Cabana EC (66%) and Newport Residence (57%).

This raises a key question among homebuyers who have yet to secure a unit: Will there still be enough homes available if they miss the next launch?

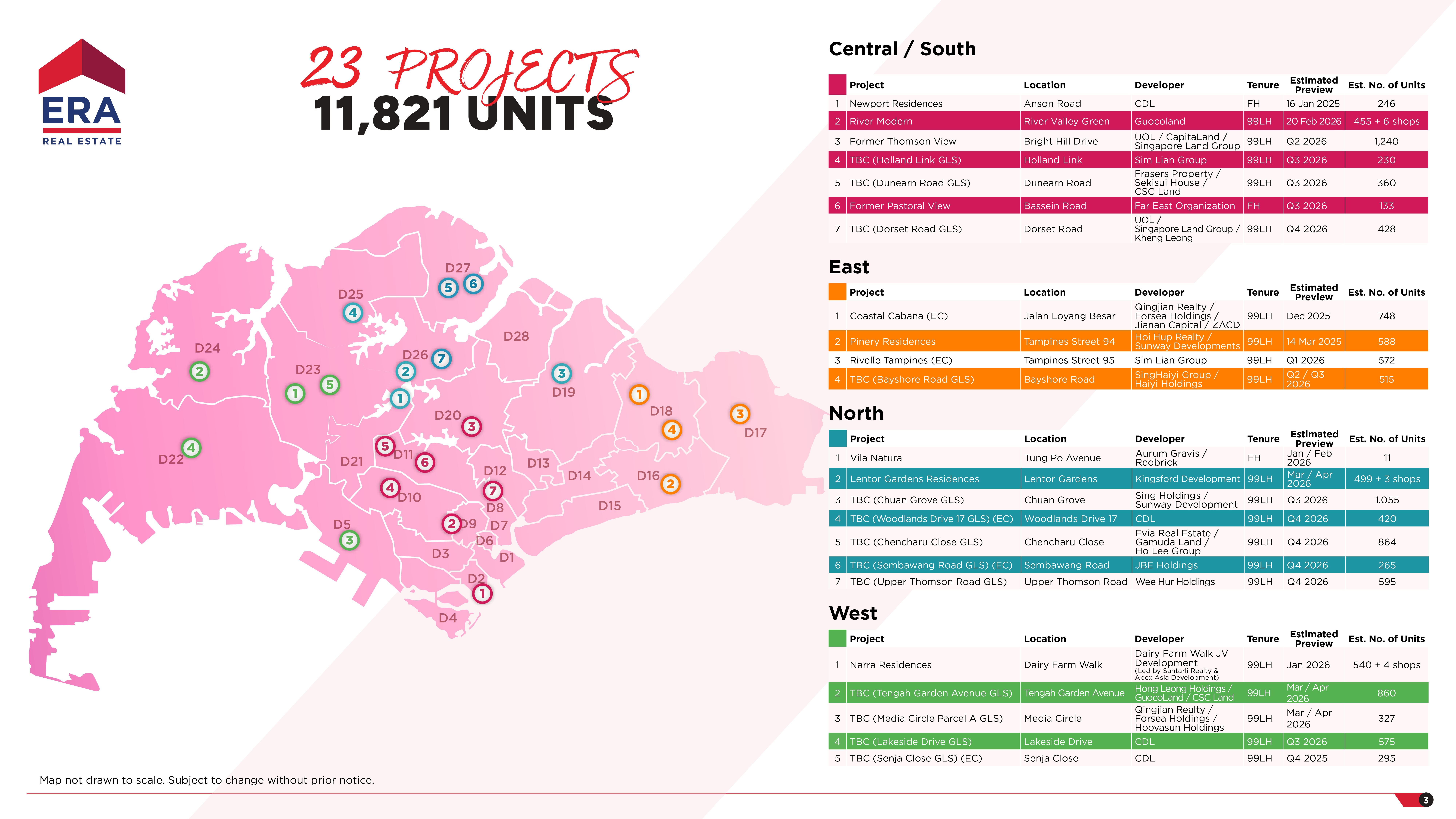

2026 is set to see 22 new non-landed private launches (Including 5 ECs)

In 2026, buyers can look forward to a pipeline of 22 new non-landed projects, adding fresh supply.

Located throughout Singapore, these 22 new projects will cater to buyers' diverse preferences and needs. There will be a good mix of developments and units across all regions to suit different locational preferences. The unit mix, with various sizes and layouts, will meet the requirements of households of various sizes. These factors, including five ECs, will accommodate buyers with different budgets and affordability levels.

Over 11,800 units are expected to enter the market, including 2,300 EC units. Around 71% of these units are located in the Outside Central Region (OCR), which attracts most HDB upgraders because of the lower price range. With ample supply, worries about not securing a unit can be eased.

In-depth analysis on each of the upcoming projects can be found here.

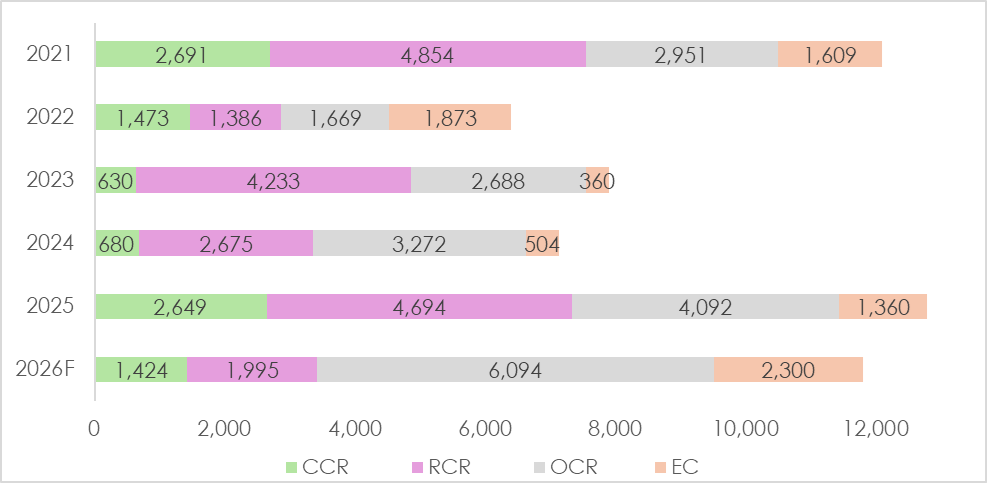

Chart 2: New home launches, including ECs

*2021-2025 data based on URA monthly developer sales data

Image 1: New launches in 2026

*Includes 1 landed project - Villa Natura

Government Land Sales (GLS) Programme supply is scalable, should the need arise

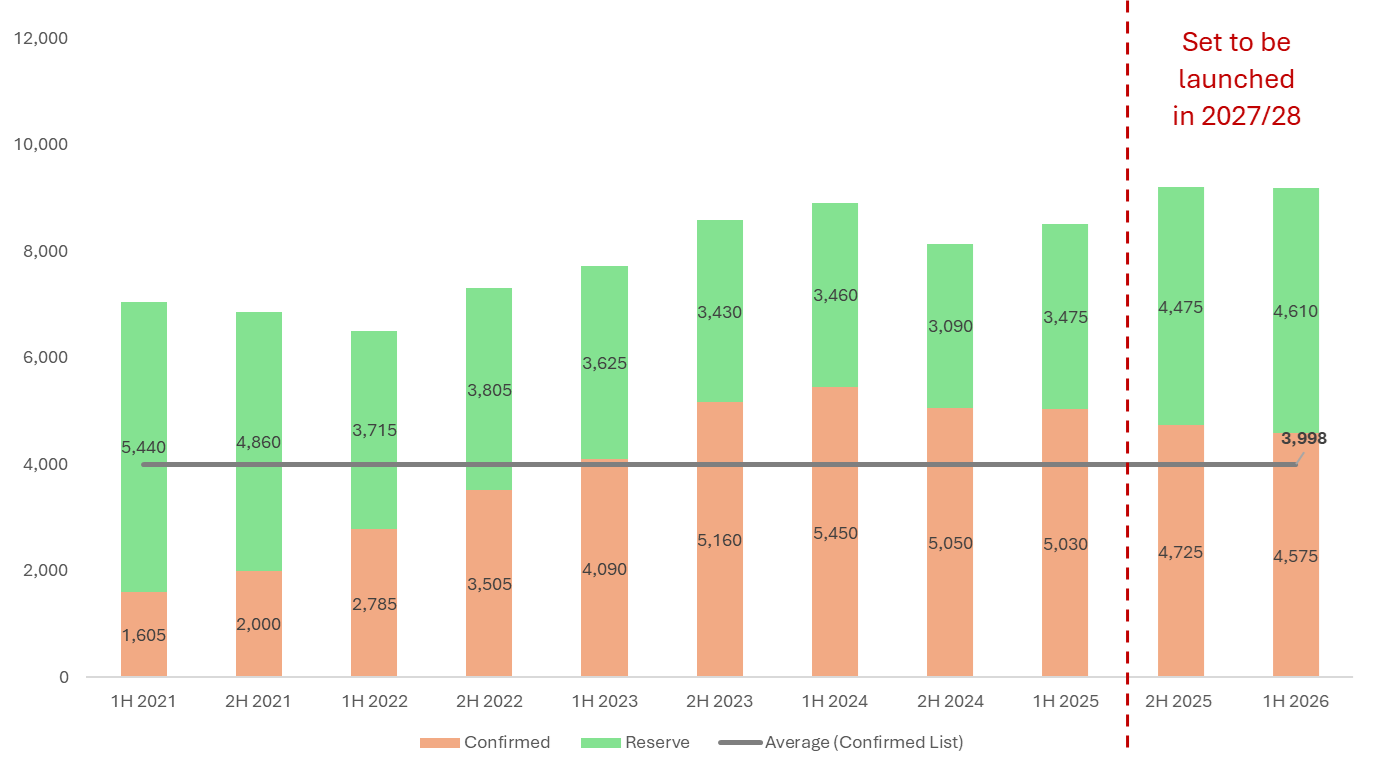

In the short to mid-term, more units have also been added to the GLS Confirmed List. URA continues to monitor economic and property market conditions and makes necessary adjustments to the supply of units under the GLS Programme, if needed. This helps to ensure that Singapore's property market remains stable and sustainable.

With the increase in demand for homes following the post-Covid-19 pandemic, URA has adjusted the private housing supply accordingly. The additional supply ensured there were enough homes to meet the rising demand.

Since the first half of 2021, the number of units on the Confirmed List has generally increased. From the first half of 2023 onwards, this number has also surpassed the half-yearly average of 3,998 units recorded since the first half of 2021. Therefore, beyond 2026, there is a strong pipeline of new homes expected to be completed in 2027 and 2028.

Chart 3: GLS units in the Confirmed List and Reserve List

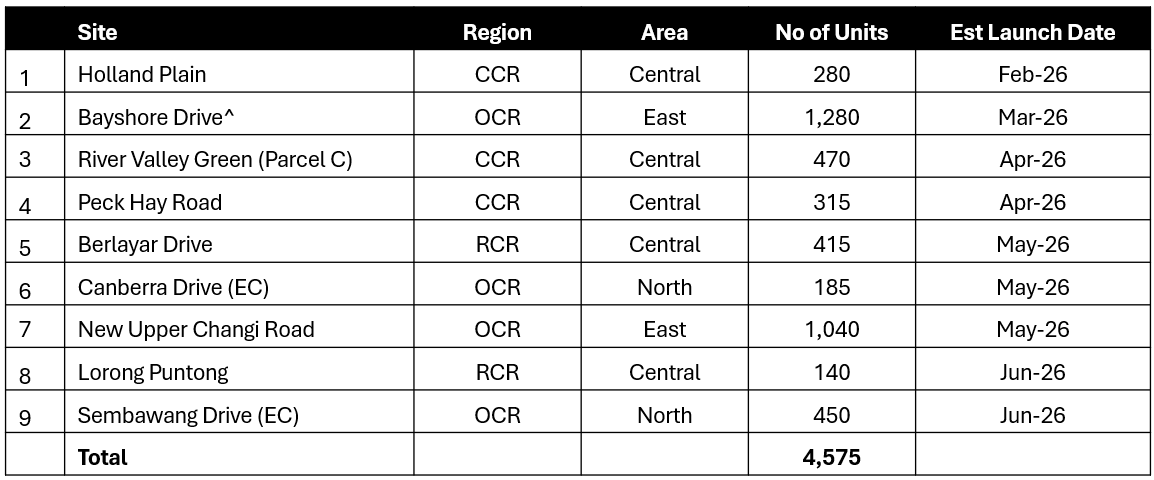

Most recently, the 1H 2026 Government Land Sales (GLS) programme will introduce 4,575 units. The nine Confirmed List sites include two EC land parcels and one major mixed-use development. More information on each site can be found here.

Table 1: GLS sites to be launched in 1H 2026

^includes 22,500 sqm of commercial space

Moving forward, the number of units will continue to be tweaked and re-calibrated as needed. For instance, to address possible new home shortages in the coming years, more sites can be moved from the Reserve List to the Confirmed List. Similarly, if there is a potential supply glut or signs of weakening demand, sites and units can be reduced. This active intervention helps prevent sudden and arbitrary spikes and dips in property prices.

Supply Pipeline is Strong – There is something for everyone!

Amplified by media reports on multiple, consecutive near-sellout projects, it is common for some buyers to develop FOMO - a fear of missing out on their preferred projects.

However, the supply pipeline remains robust, and with many upcoming projects of various sizes across Singapore, there is certainly something for everyone.

We expect around 11,800 units (including ECs) to be launched in 2026. Based on GLS sites that have been awarded, are pending award, or are scheduled for tender, at least 9,000 additional units are in the pipeline. In June this year, URA will announce the 2H 2026 Confirmed List sites, which are likely to offer greater variety and options for buyers going forward.

Alongside new launches, the resale market will also offer more housing options. More units are expected to be completed in the coming years, increasing supply to meet the higher demand. By 2026, approximately 7,000 units are expected to be completed, with another 10,000 units in both 2027 and 2028.

With a steady flow of new and resale homes entering the market, buyers have time to carefully assess their options without rushing into a purchase.

Have you missed out on your preferred development? Are you eyeing one of the upcoming projects? Or are you unsure about what launches are in the pipeline? Speak to any ERA Trusted Advisor today to find out more!

I confirm that I have read theprivacy policy and allow my information to be shared with this agent who may contact me later.