Can Singapore’s Private Property Market Stay Resilient Amid 2026’s Geopolitical Tensions?

- Stanley Lim

- 7 min read

- Blog

- 10 Mar 2026

The information contained within this piece is accurate as of 9 March 2026.

While it is still early in the year, 2026 has already been marked by a series of global uncertainties. Between the recent escalation of hostilities in the Middle East – which has caused oil prices to skyrocket – and the shifting tariff policies of the West, global events have sent global financial markets into a tailspin.

For risk-averse investors, this has sparked a search for safer investment destinations, with many turning their gaze turning towards Singapore.

Despite its inherent vulnerability as a small, open economy, Singapore has consistently punched above its weight, which has allowed it to be viewed as a safe haven and world-class financial hub in Asia. In turn, this reputation is anchored by a potent combination of long-term political stability and prudent economic management.

More relevantly, Singapore’s strengths have allowed its economy to weather the disruptive effects of past Middle Eastern conflicts – from the Gulf War in the 1990s, and the Iraq War in 2003, to more recent crises such as the Russo-Ukrainian War in 2022.

But does this resilience also extend to Singapore’s private property market? History suggests that “yes” is a possible answer over the longer term, but it is worth taking a look at the finer details.

How has Singapore’s property market performed during past conflicts?

By and large, oil-related geopolitical crises have drawn significant attention, as they are often intertwined with spikes in global inflationary pressures. These shocks often filter into the real estate sector through higher construction costs, as material manufacturing and transportation become more expensive.

At the same time, elevated inflation and tighter financing conditions from heightened interest rates may dampen buying sentiment, especially as prospective homebuyers and investors adopt a more cautious stance in the face of affordability concerns.

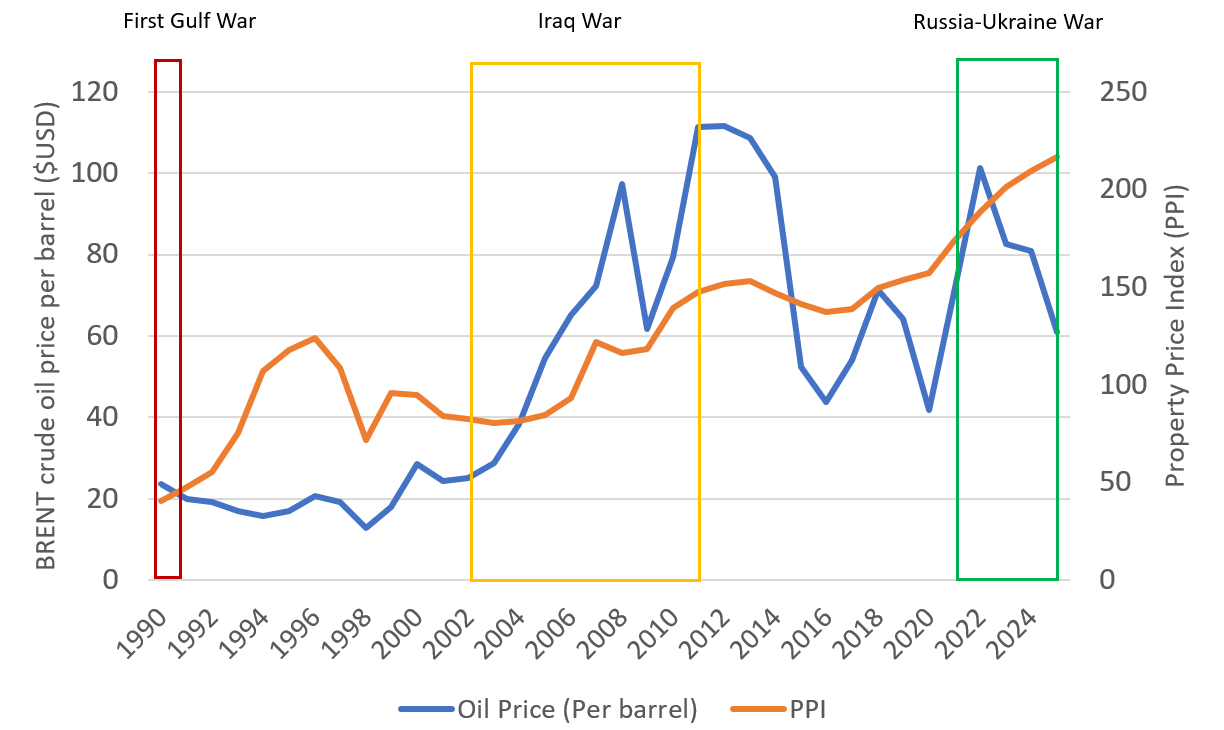

Chart 1: BRENT crude oil price (per barrel, $USD) vs Singapore Private Property Price Index (PPI)

Despite the uncertainty in the immediate aftermath of international conflicts, the long-term trajectory of Singapore’s residential market has generally stayed stable. This is clear in the steady growth of home prices, both during and after such episodes of geopolitical tension.

Specifically, in the case of local private properties, movements in URA’s Private Residential Property Price Index (PPI) have largely reflected the market’s ability to maintain a broader upward trajectory over time.

For instance, during the first Gulf War (1990-1991), the PPI maintained its growth throughout the conflict and rose by roughly 160% over the following five years, before peaking in 1996. Subsequently, during the Iraq War (2003–2011), the PPI rose by around 82.9% throughout the conflict. Similarly, an upward trend in private property prices has been observed since the outbreak of the Russia–Ukraine conflict in 2022.

Taken together, these historical trends suggest that Singapore’s private residential market possesses a degree of resilience in the face of geopolitical disruptions. But to fully appreciate this strength, it is equally important to look at the events that have led to market corrections in the past.

What are the key factors influencing Singapore’s private property market?

Aside from geopolitical crises, Singapore’s property market has also experienced several notable episodes that resulted in measurable declines in the PPI. These include the Asian Financial Crisis of 1998, the Global Financial Crisis of 2008, and the implementation of market cooling measures in 2013.

Although these events originated differently, they share several common themes that ultimately exerted downward pressure on private residential property prices. Simultaneously, they underscore the structural strengths that have supported Singapore’s property market through previous cycles.

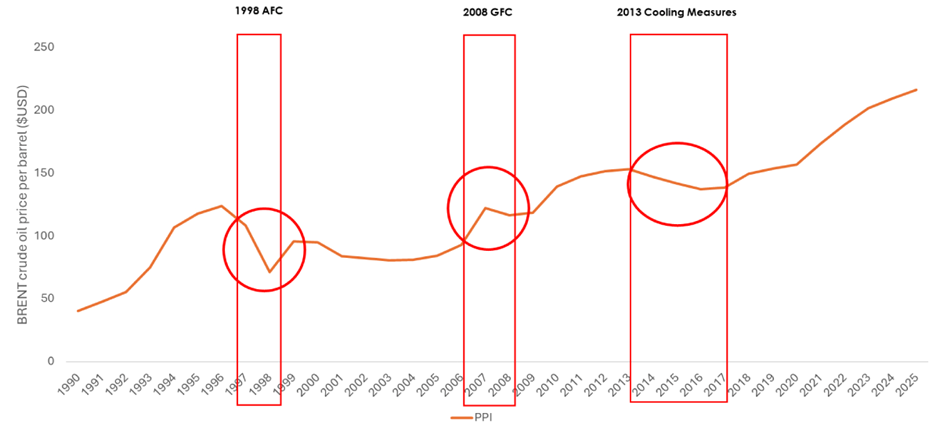

Chart 2: Singapore Private Property Price Index (PPI) amid financial shocks

In 1998, amidst the Asian Financial Crisis, Singapore’s labour market deteriorated markedly as the regional economic fallout impacted sectors such as manufacturing, commerce, construction, transport, and communications. This led to a record 28,300 workers being made redundant within a year.

As a result, declining consumer confidence caused by these job losses dampened demand across the property market, affecting not only residential property prices but also commercial and industrial assets. During this period, the PPI fell by 34.0% year-on-year from 1997 to 1998.

Between 2007 to 2008, a similar story unfolded once more. Following the collapse of the U.S. subprime mortgage market in early-2007, and the subsequent failure of major financial institutions in September 2008, global financial markets experienced severe disruption. These developments also coincided with a liquidity crunch that constrained banks’ ability to extend credit to consumers and businesses, tightening financing conditions across many foreign economies.

Domestically, the sharp deterioration in global economic conditions also weighed on Singapore’s trade-dependent economy, with layoffs, slower hiring and wage cuts locally raising concerns over income stability. As uncertainty grew, prospective buyers and investors adopted a more cautious stance, while developers also delayed project launches amid weak sentiment. This slowdown in demand contributed to the continued decline in private residential property prices, which lasted until the market turned around in 3Q 2009.

In contrast, 2013's downtick in private property prices was mainly caused by policy measures rather than an external shock. In January that year, a new set of cooling measures was introduced, including higher Additional Buyer’s Stamp Duty rates and stricter loan-to-value limits. Most notably, the Total Debt Servicing Ratio (TDSR) was implemented, limiting monthly debt repayments to 60% of income at that time.

Together, these cooling measures aimed to limit speculative demand and ensure property price growth remained aligned with economic fundamentals. As credit conditions tightened, local investment activity and transaction volumes slowed, contributing to a period of price moderation that lasted until 2018.

So, what do these episodes reveal about the underlying factors supporting Singapore’s private property market?

A closer look suggests that significant corrections in Singapore’s private property prices tend to occur under specific conditions. These include severe economic downturns that weaken incomes and employment. They may also arise from deliberate policy interventions aimed at cooling the market through tighter financing conditions that limit borrowing.

By the same token, underlying economic fundamentals, such as stable employment, household earning power, and Singapore’s strong governance have generally supported private property demand, while keeping prices growing in times when destabilising factors are absent.

The road ahead: Can Singapore’s private property market maintain its strength in 2026?

Looking back at the start of 2026, national data released in January indicated that Singapore’s economic fundamentals had strengthened over the past year. According to the Ministry of Manpower1, total employment growth for the full year of 2025 stood at 57,300, up from 44,500 in 2024.

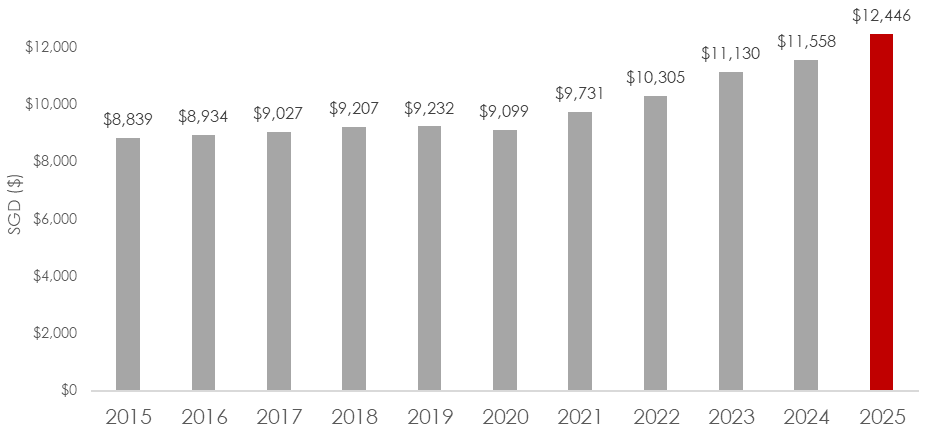

At the same time, Singaporean households saw their earning power reach a new peak. Median monthly household market income rose from S$11,558 in 2024 to S$12,446 last year2, marking the first time the figure has crossed the S$12,000 mark.

Chart 3: Median monthly household market income among resident households (2015 to 2025)

Moreover, at this juncture, Singapore’s macroeconomic outlook remains relatively stable. GDP growth for 2026 is projected at between 2.0% and 4.0% (at the time of writing), following stronger-than-expected economic performance for 20253.

Viewed as a whole, these signs point to the same structural factors that have consistently anchored demand and price growth in Singapore’s private property. Or in other words, as long as employment remains stable and household balance sheets continue to strengthen, the private housing market could remain on relatively firm footing over the long run.

But at the same time, it is undeniable that this stability is being tested anew by global tensions. Recent fighting involving Israel, Iran and the United States has driven oil prices higher and rattled financial markets. The conflict has also disrupted activity around the Strait of Hormuz, a crucial route for roughly 20% of global oil supply.

For Singapore, this could translate into higher energy, construction and living costs if supply disruptions persist. That said, past episodes suggest that while global markets can become unsettled, Singapore’s property market has tended to remain resilient and recover over time. Whether this pattern persists in 2026 will mainly depend on the duration of these global tensions and the resilience of Singapore’s economy.

Sources

1 Ministry of Manpower (MOM), Labour Market Advance Release 4Q 2025.

https://www.mom.gov.sg/newsroom/press-releases/2026/0129-labour-market-advance-release-fourth-quarter-2025

2 Singapore Department of Statistics, Key Household Income Trends 2025. https://www.singstat.gov.sg/find-data/search-by-theme/households/household-income/latest-data

3Ministry of Trade and Industry, MTI upgrades 2026 GDP growth forecast to 2.0%–4.0%. https://www.mti.gov.sg/newsroom/mti-upgrades-2026-gdp-growth-forecast-to--2-0-to-4-0-per-cent-/

I confirm that I have read theprivacy policy and allow my information to be shared with this agent who may contact me later.