Singapore’s Government Role in Attracting Industrial Investment: Three Key Trends Shaping Singapore’s Industrial Property Market

- Kwong Seong Ping

- 7 min read

- Blog

- 9 Apr 2026

The rising geopolitical tensions and conflicts in the Middle East have heightened global uncertainty, raising concerns about inflation, interest rates, and disruptions to energy and supply chains.

In this environment, Singapore is regarded as a stable place for investment, consistently attracting capital inflows and foreign investment, thereby strengthening its status as a safe haven and a global wealth centre.

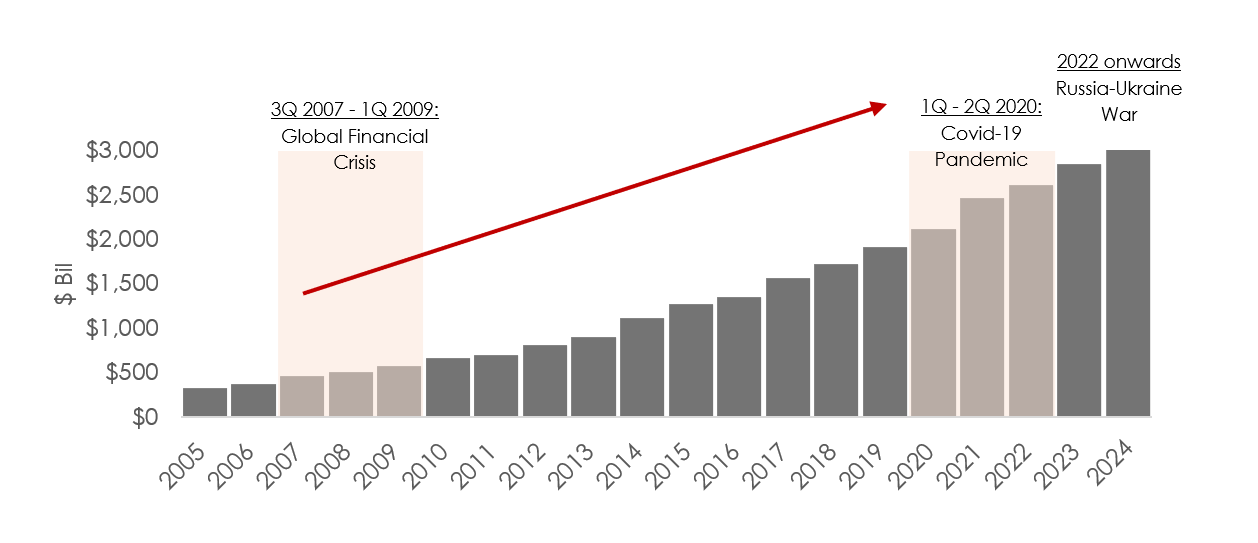

Chart 1: Foreign Direct Investment in Singapore

This wider change in capital flows is transforming Singapore’s industrial property market. Previously considered mainly a yield-focused asset class, it is now regarded as a more balanced investment that supports both capital preservation and long-term growth. This shift is intentional, driven by strategic government planning, solid economic fundamentals, and Singapore’s persistent attractiveness as a global safe haven.

This shift has also influenced investor behaviour, which now prioritises asset quality, tenant stability, and long-term positioning over merely high rental yields.

Trend 1 – Singapore as a Safe Haven

Singapore combines political stability, transparency, and pro-business policies, which significantly reduce investment risks and enhance confidence among both local and international investors. Although its small size presents certain vulnerabilities, the open economy has consistently exceeded expectations, establishing itself as a secure destination and a global wealth centre.

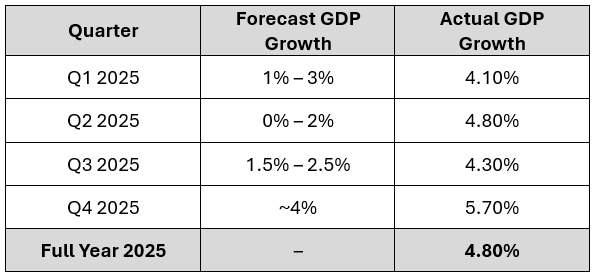

Table 1: 2025 Quarterly GDP Forecast vs Actual Growth in Singapore

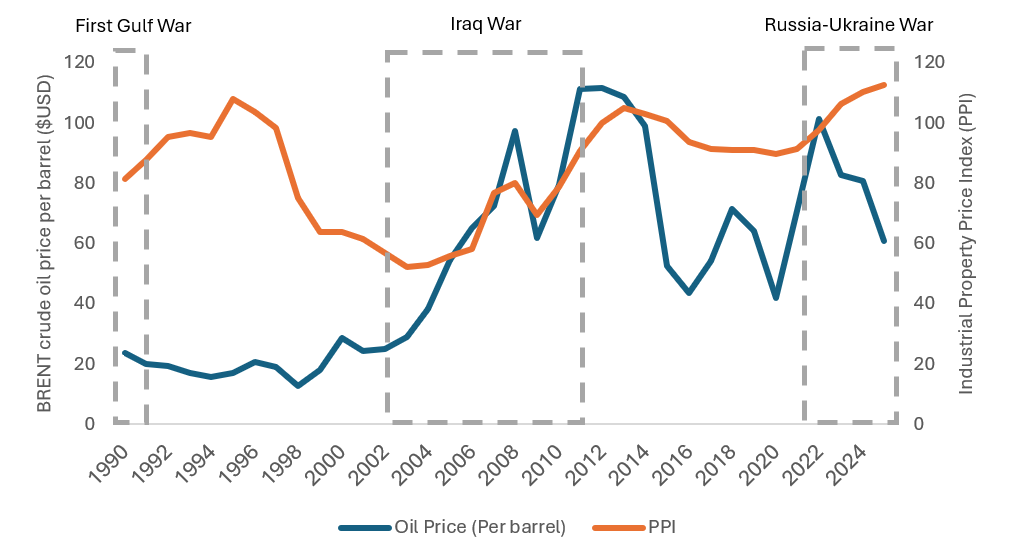

Amid escalating geopolitical conflicts, the long-term trend of Singapore’s Industrial market has generally remained stable. These historical trends suggest that Singapore’s Industrial residential market demonstrates a degree of resilience against geopolitical disruptions.

During the first Gulf War (1990-1991), the Industrial PPI grew throughout the conflict, increasing by around 17.2% over the subsequent five years, reaching a peak in 1995. Later, during the Iraq War (2003–2011), the PPI rose by approximately 73.9% over the course of the conflict. Similarly, an upward trend in Industrial property prices has been observed since the Russia-Ukraine conflict began in 2022.

Chart 2: BRENT crude oil price (per barrel, $USD) vs Singapore Industrial Property Price Index (PPI)

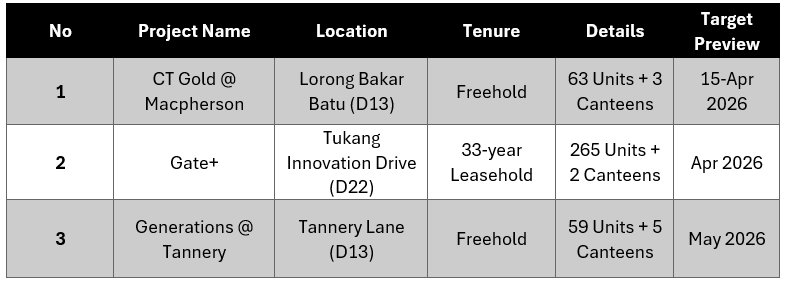

The demand for industrial space is also shaped by structural factors rather than short-term fluctuations. Much of the demand originates from downstream activities such as final-stage manufacturing, assembly, and distribution, primarily driven by small and medium-sized enterprises (SMEs). These companies typically seek affordable and flexible spaces, with strong connectivity to transport networks and access to labour being crucial considerations. Below are the upcoming projects that are well-placed to meet these needs.

Table 2: 3 Upcoming Industrial Project Launches

Overall, the demand in Singapore’s industrial market is driven by strong governance and ongoing operational requirements. This results in stable occupancy rates, diverse tenant profiles, and relatively low vacancy levels, reinforcing the resilience of the industrial sector.

Trend 2 – Government-Led Industrial Clustering

A key feature of Singapore’s industrial landscape is the government’s proactive role in shaping industrial clusters. Instead of letting industrial development happen naturally, Singapore adopts a planned strategy that groups similar industries into specialised ecosystems.

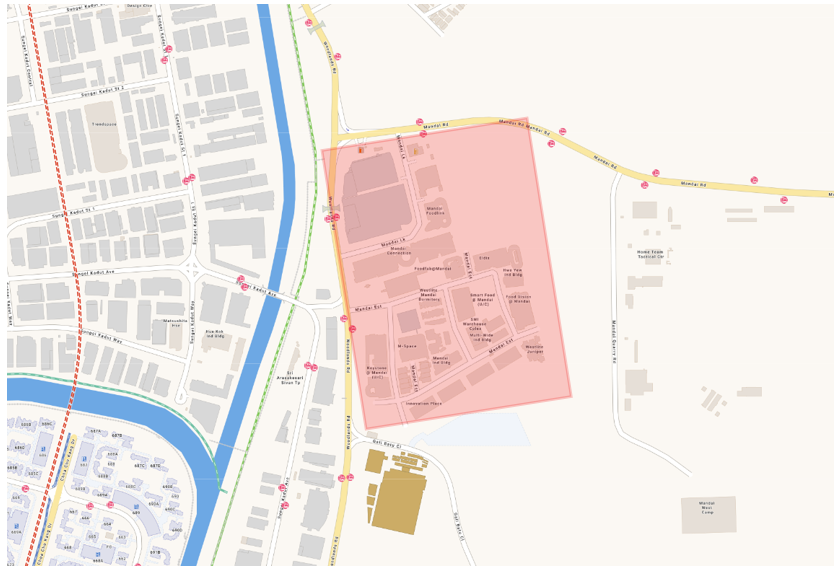

This marks a shift away from generic industrial spaces towards purpose-built industrial clustering and specialisation that enhance productivity, efficiency, and collaboration. For example, the Mandai industrial area, which has increasingly evolved into a food-focused industrial cluster, supports activities such as food manufacturing, processing, and related uses to cater to the growing needs of SMEs and food operators.

Image 1 : Map of Mandai Industrial Cluster

Several other key industrial clusters illustrate this strategy:

- Tuas Industrial Cluster: A significant industrial centre in western Singapore specialising in heavy industry, logistics, and maritime activities. Major developments include the Tuas Port expansion and the Tuas Biomedical Park, a specialised cluster for pharmaceutical manufacturing.

- MacPherson Industrial Cluster: It is recognised for its light industrial (B1) developments, supporting a diverse range of light industrial activities, including e-commerce, technology, and manufacturing. The area benefits from well-established infrastructure and planning that supports diverse light industrial uses. Upcoming projects such as CT Gold @ MacPherson and Generations @ Tannery are well-placed to capitalise on these advantages.

- Jurong West Industrial Cluster: This zone is designated for heavy industrial (B2) activities, including logistics, engineering, and advanced manufacturing. The upcoming Gate+ industrial building at Tukang Innovation Drive enhances this focus by providing B2 space with features such as contemporary development and heavy-vehicle access.

Industrial clustering offers several benefits. By grouping similar industries together, it promotes more steady rental growth, particularly for higher-quality industrial spaces where supply is limited and demand remains fairly stable. Additionally, specialisation reduces vacancy risks. Companies within these clusters gain from proximity to suppliers, skilled labour, and shared infrastructure, which enhances efficiency and makes relocation less attractive, even as costs rise.

Conversely, older or less strategically located industrial properties are at greater risk of becoming obsolete, especially as demand moves towards modern, purpose-built buildings designed for specific industry needs.

Trend 3 – Industrial Government Land Sales (IGLS) Programme

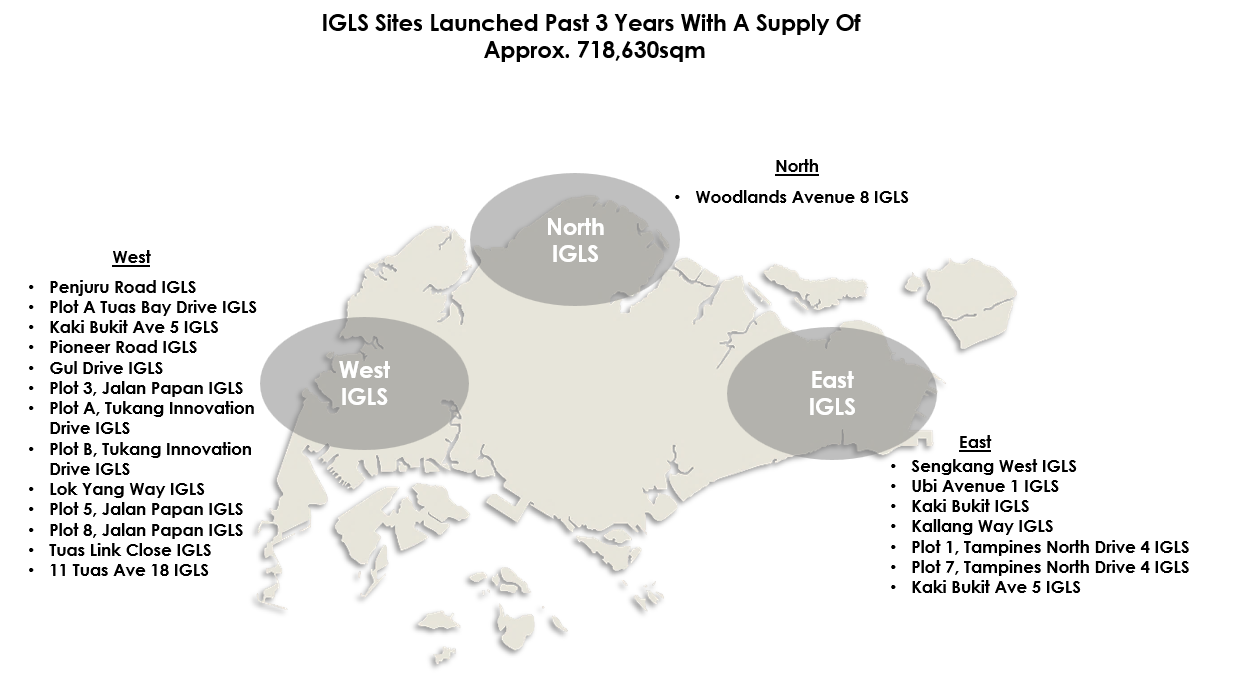

The Industrial Government Land Sales (IGLS) programme, led by JTC, plays a vital role in managing the supply of industrial land in Singapore. The programme ensures a steady, controlled supply of industrial space, preventing oversupply while meeting long-term economic demands. Over the years, industrial spaces released under the IGLS programme have typically been on shorter leasehold tenures of around 30 years. In the first half of 2026, several confirmed sites were released under the IGLS programme, totalling approximately 8.58 hectares. Most of the releases are concentrated in the western region.

Image 2 : IGLS Sites Launched Past 3 Years

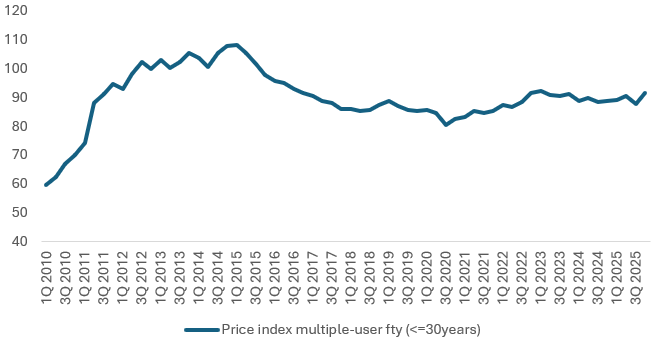

These shorter-term leasehold properties typically cater to more price-sensitive buyers, with entry prices often below $1 million per unit. This is particularly relevant for SMEs and business owners, who require more working capital for operations, making shorter leasehold tenures more attractive as they help preserve cash flow and provide greater financial flexibility.

Chart 3: Price index of Multiple-user factory (<=30 years)

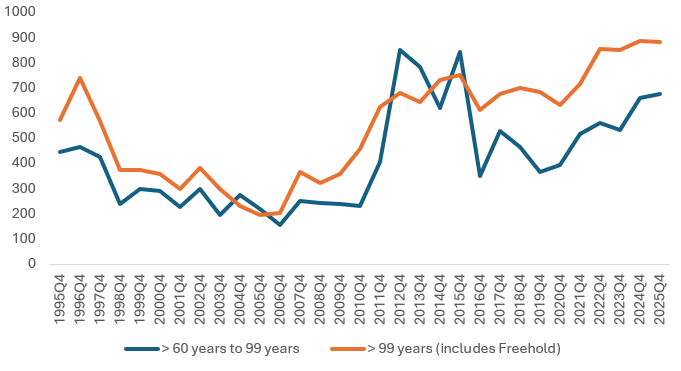

With the continuous supply of leasehold properties, freehold assets are becoming increasingly scarce, enhancing their attractiveness to investors seeking stability and long-term value preservation. As a result, the price gap between freehold and leasehold industrial properties has been widening. The price gap between these industrial properties has increased by 63.3% from $128 to $209 since 1995, showing its resilience in price and demand.

Chart 4: All Sale Median Industrial Property Price (psf)

Examples of such freehold new launch industrial properties include the upcoming CT Gold @ MacPherson and Generations @ Tannery Lane, which benefit from strong locations, established tenant demand, and long-term holding potential.

Conclusion

The ongoing US-Iran conflict has heightened global uncertainty, particularly through its impact on energy markets and key shipping routes like the Strait of Hormuz. This has led to increased global uncertainly and a shift in capital towards safer, more stable markets. Singapore continues to benefit as a trusted and well-regulated investment destination, attracting steady inflows of capital into sectors such as industrial real estate.

Singapore’s industrial property market will continue to remain resilient and stable. This resilience is supported by its strategic position as a regional hub, along with proactive government policies such as industrial clustering and controlled industrial land supply under the IGLS programme.

Looking ahead, investor behaviour is likely to be driven more by property fundamentals than short-term market conditions. Well-located, high-quality assets within established industrial clusters are expected to remain in demand, particularly those with strong specifications and longer-term holding potential.

I confirm that I have read theprivacy policy and allow my information to be shared with this agent who may contact me later.