The Fire Horse Cycle: Singapore’s Economic and Property Story, 1966–2026

- ERA Singapore

- 10 min read

- Blog

- 13 Feb 2026

This article was first published on EdgeProp (13 Feb 2026) with insights contributed by CEO Marcus Chu.

The Year of the Fire Horse is 2026 (specifically 17 Feb 2026 – 5 Feb 2027, according to the Lunar Calendar), a rare 60-year cycle. The last Year of the Fire Horse fell in 1966, just a year after Singapore gained independence and embarked on its development path.

The year of the Fire or Red Horse is characterised by passion, rapid change, and potential. It favours bold, independent action over cautious, slow or fearful approaches.

Let us examine the bold moves in the property market during each zodiac cycle of the Horse.

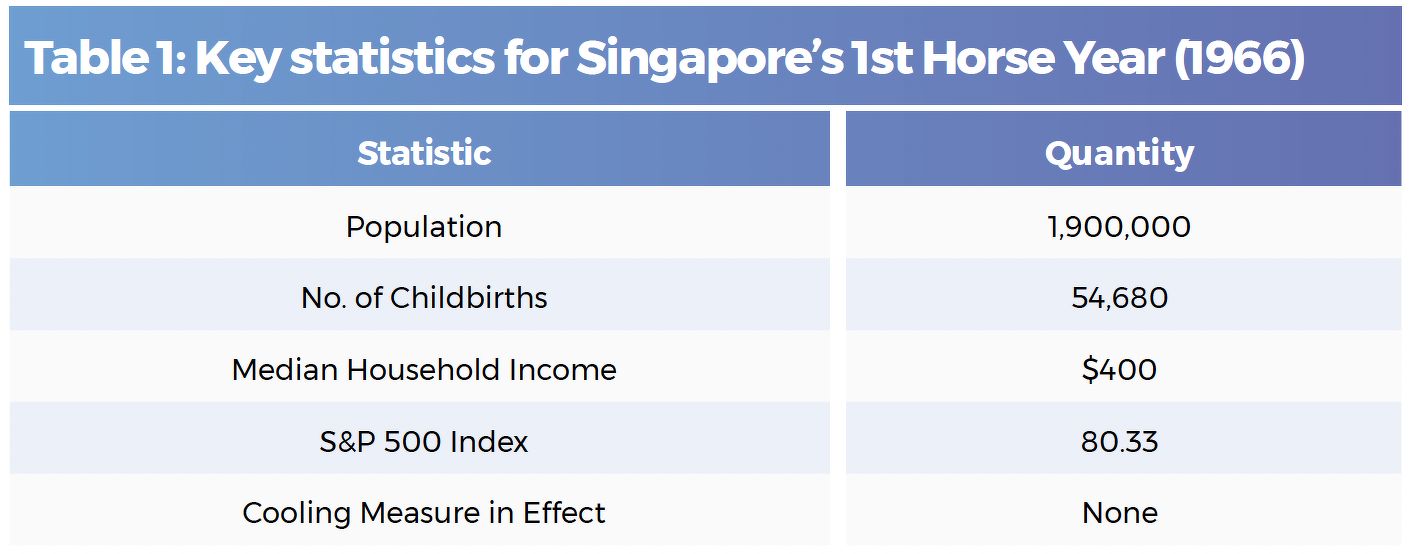

1966 – Sovereign Singapore’s inaugural Year of the Horse

Following Singapore’s separation from Malaysia and declaration of independence in August 1965, the following year, the year of the Fire Horse, required Prime Minister Lee Kuan Yew and the founding fathers of the People’s Action Party to be bold and decisive to ensure that independent Singapore got off to the best possible start.

Land Acquisition Act

In 1966, the Land Acquisition Act was introduced to provide the government with a legal framework for the compulsory acquisition of private land. The key objective of the Act was to make land readily available for public housing, infrastructure works or industrial projects by public agencies such as HDB, LTA and JTC Corp.

Toa Payoh – Singapore’s first HDB town

Due to Singapore’s population boom in the 1950s and 1960s, the government relocated residents from kampungs to newly built housing estates, ensuring they had adequate living conditions and access to essential amenities. One such estate, developed in 1966, was Toa Payoh — one of Singapore’s oldest and most recognisable HDB towns.

Vandalism Act

The Vandalism Act was also introduced in 1966, imposing severe penalties for damaging, marking, or stealing public or private property. The Act’s stringent bail restrictions served as a strong deterrent, underscoring Singapore’s first stance on maintaining public cleanliness and order.

Over the next six decades, the impact of policies introduced during Singapore’s first Fire Horse year became visible in the nation’s spotless streets and the glass-and-concrete skyscrapers that define its skyline today.

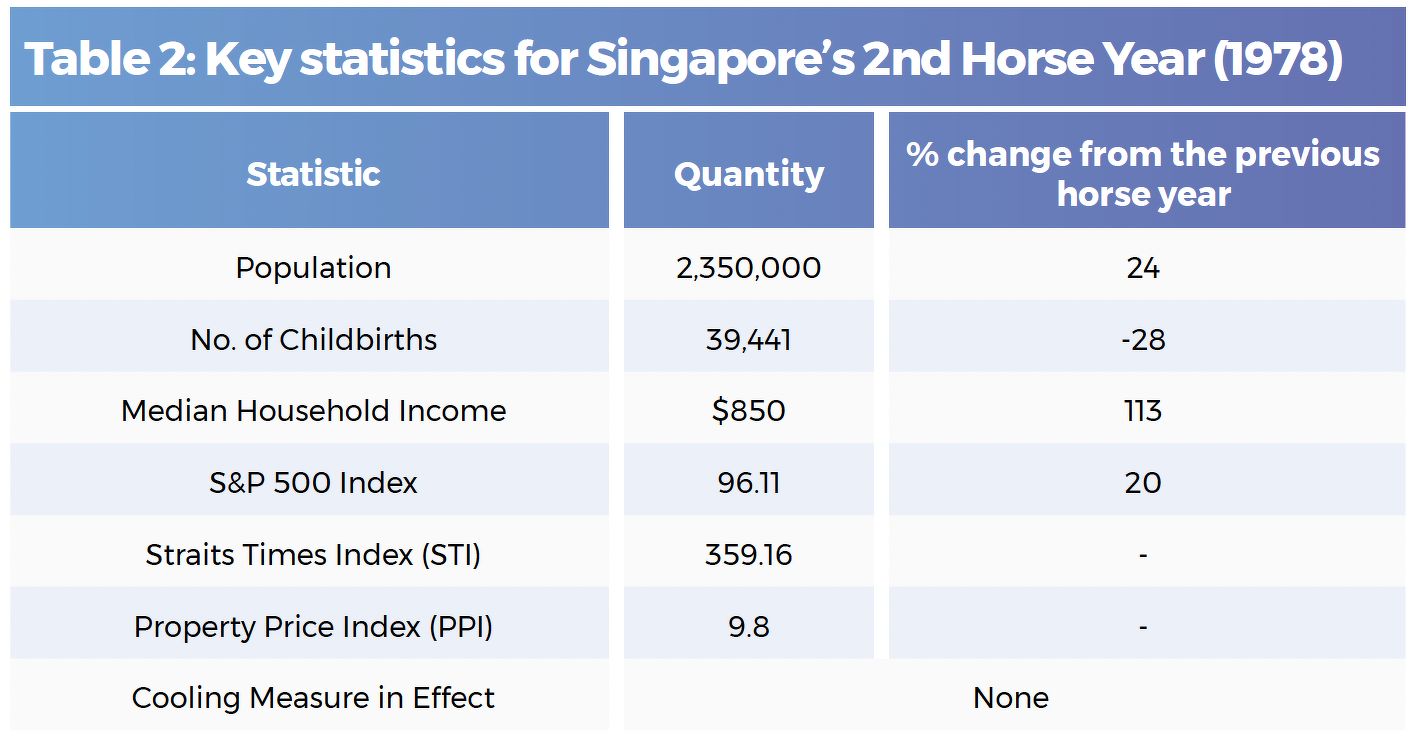

1978 – Development of HDB towns, 5-room flats and Singapore’s first condos

The second horse cycle saw Singapore’s rapid development and the expansion of HDB towns such as Ang Mo Kio and Clementi, which have since matured into well-established estates with a wide range of amenities and quality infrastructure.

Five-room flats, introduced in the 1970s for middle-income families, became popular during that period to support Singapore’s growing population and economy. Such flat also offer generous layouts in what have since become mature estates. Despite their age, they remain highly sought after and command competitive prices in the resale market.

Introducing – The condominium

Notably, 1978 saw the construction of one of Singapore’s first condominiums, Pandan Valley. In a market largely defined by HDB blocks and landed properties, Pandan Valley provided spacious, middle-income apartments on private land — carving out a middle ground between public housing and landed living.

The project comprises over 600 units across a large hillside site, complemented by extensive landscaping and a range of facilities, including tennis and squash courts, gyms, swimming pools and more.

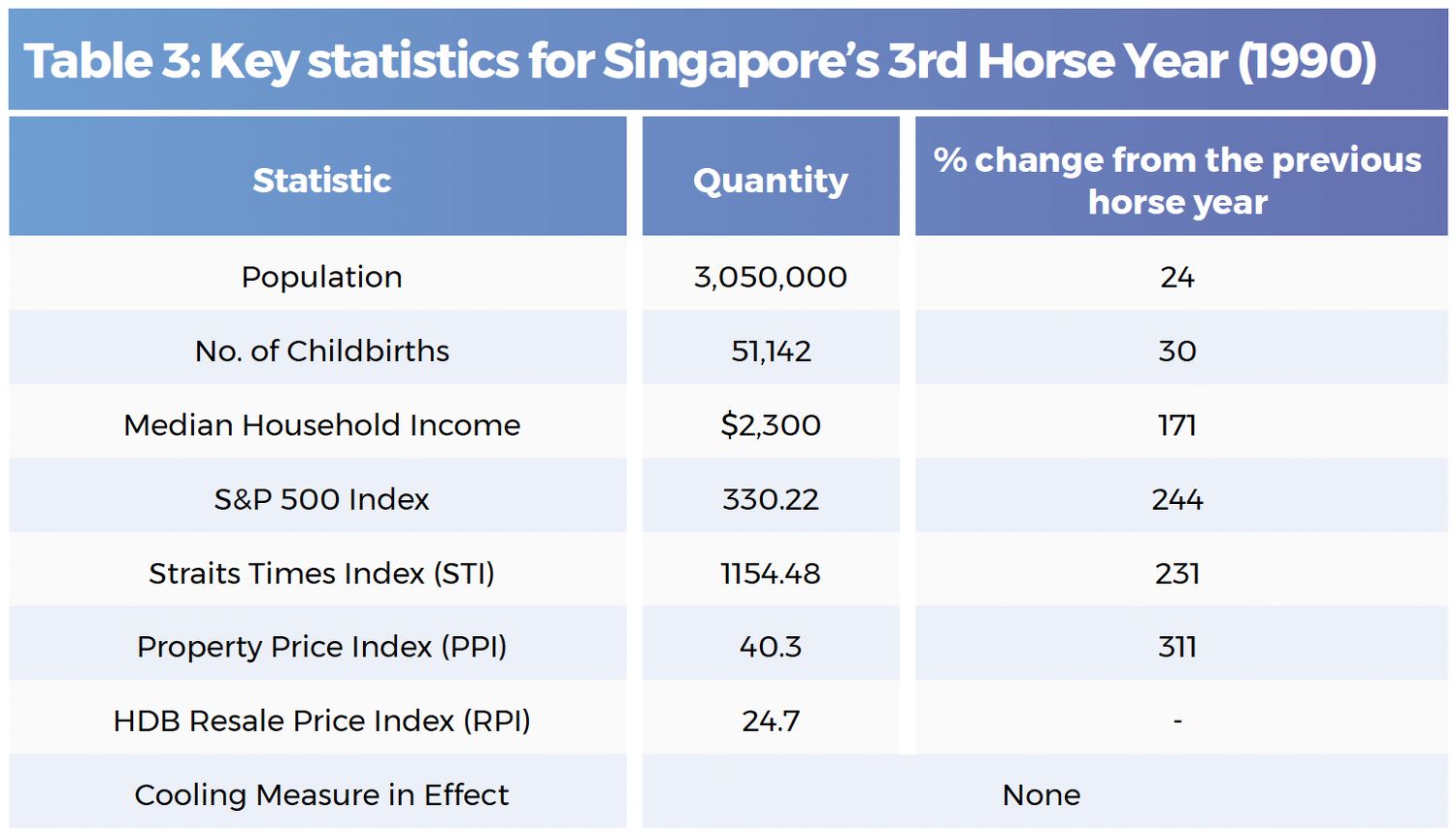

1990 – Galloping along at full speed

In 1990, the Singapore property market was characterised by strong growth, high demand and rising prices for both public and private housing, driven by a robust economy and low interest rates.

The 1990s saw robust capital appreciation, with price growth peaking at 36% in 1993 and 42% in 1994. The surge was further driven by rising foreign interest, as investors viewed Singapore as a “safe haven” due to its political stability, strategic position as a trade hub and sound economic fundamentals.

Developing new estates that we call home today

HDB continued to develop more projects to keep pace with Singapore’s expanding population, building new estates in towns including Tampines, Choa Chu Kang, Hougang, Pasir Ris and Woodlands.

With Singapore’s population exceeding three million and more than 50,000 births recorded in 1990, new estates were developed to meet growing housing demand through satellite towns across the island.

As homeownership aspirations rose, the government expanded beyond its early estates such as Queenstown, Bukit Merah and Toa Payoh. Today, many of these satellite towns have matured into well-established, self-sustaining communities — a testament to Singapore’s steady progress.

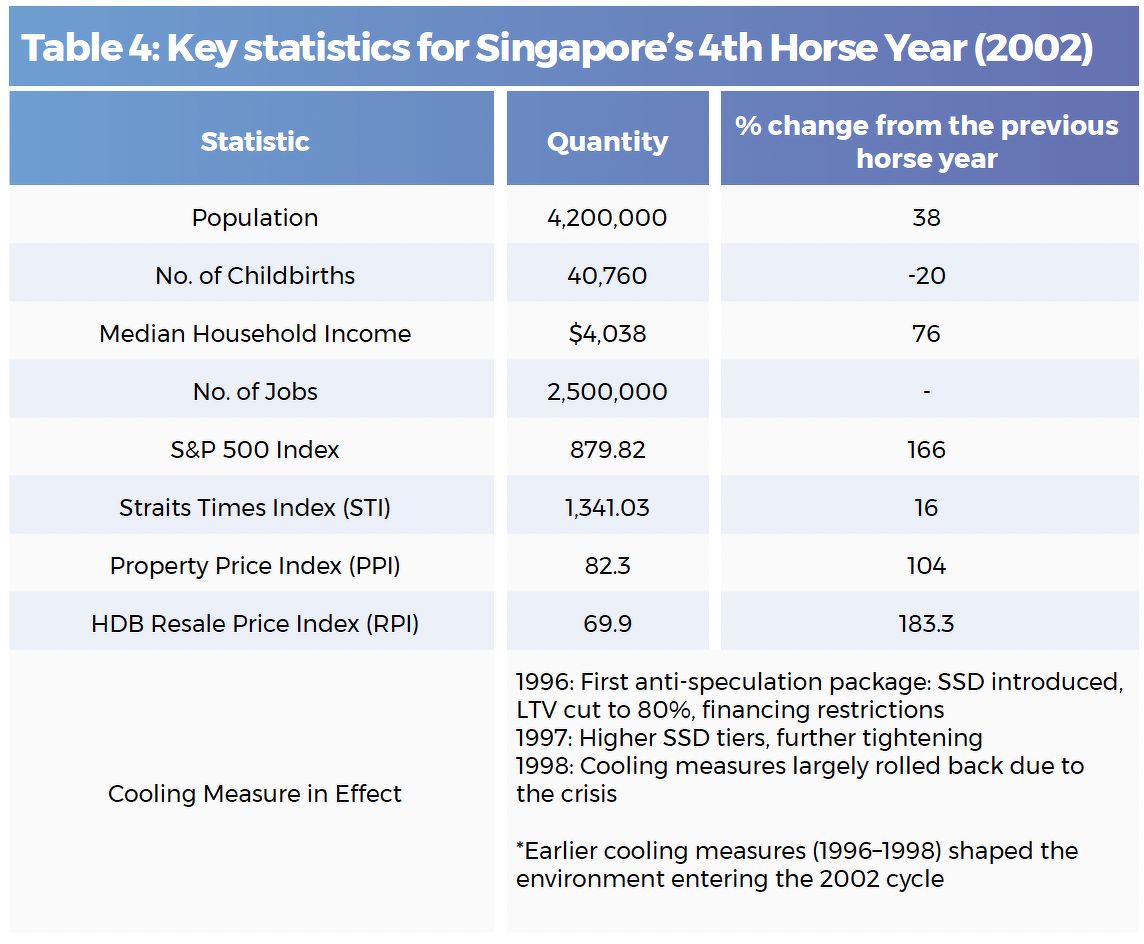

2002 – Singapore’s resilient start to a challenging new millennium

The year 2002 saw a downturn in the stock market, following the September 11 attacks late in the previous year. The downturn was partly driven by the early-2000s recession, triggered largely by the dot-com bust and the subsequent global slowdown, which resulted in a prolonged 16-quarter decline in the overall property price index.

Around the same time, the government announced plans to raise the Goods and Services Tax (GST) from the prevailing 3% in the following years. The increase was intended to offset revenue losses from reductions in corporate and top personal income taxes, while preserving Singapore’s competitiveness as an investment and business hub.

Introduction of the BTO system

In 2002, the full implementation of HDB’s Built-To-Order (BTO) system — which had begun in Sengkang and Sembawang — was completed. This new approach fundamentally changed how flats were allocated, allowing buyers to choose the location and flat type before construction began.

It was a significant departure from the previous Registration for Flats System, which allowed only the broad geographical zone of desired neighbourhoods, giving future generations of home seekers greater flexibility and control over their housing journeys.

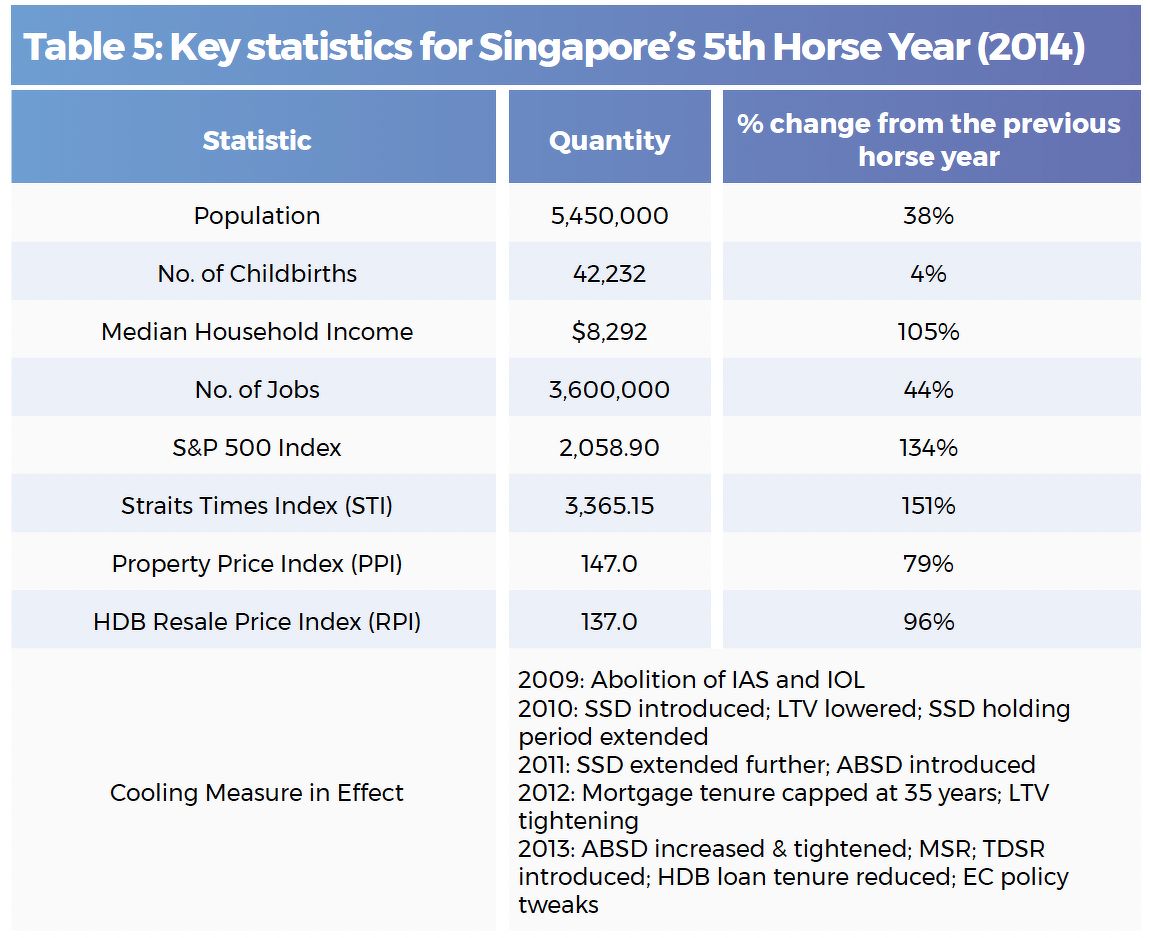

2014 – Trotting onwards despite the effects of cooling measures

In 2014, the Singapore property market cooled significantly, with private home prices declining by 4% for the year — the first annual drop since 2008. The downturn was largely attributed to government cooling measures, including the Total Debt Servicing Ratio (TDSR) loan framework, introduced at the end of June 2013 to limit buyers’ borrowing capacity and leverage.

Transaction volumes fell sharply to a six-year low, while private residential rents declined by 3%. New home sales were particularly weak, totalling just 7,378 units for the year — less than half the 15,291 units sold in 2013. To date, 2014 and 2015 remain reference points for downturns in the property market.

Yet 2014 was not entirely negative. Under the Master Plan 2014, gazetted in June that year, Bidadari was unveiled as Singapore’s newest housing estate. Envisioned as an ecology- and heritage-sensitive town, it was planned to accommodate about 10,000 HDB flats and 1,000 private homes. Since the launch of its first HDB project in 2015, Bidadari has consistently ranked among Singapore’s most sought-after new towns.

The year ahead

As the Year of the Fire Horse begins, a new set of social, economic and property markers defines the landscape.

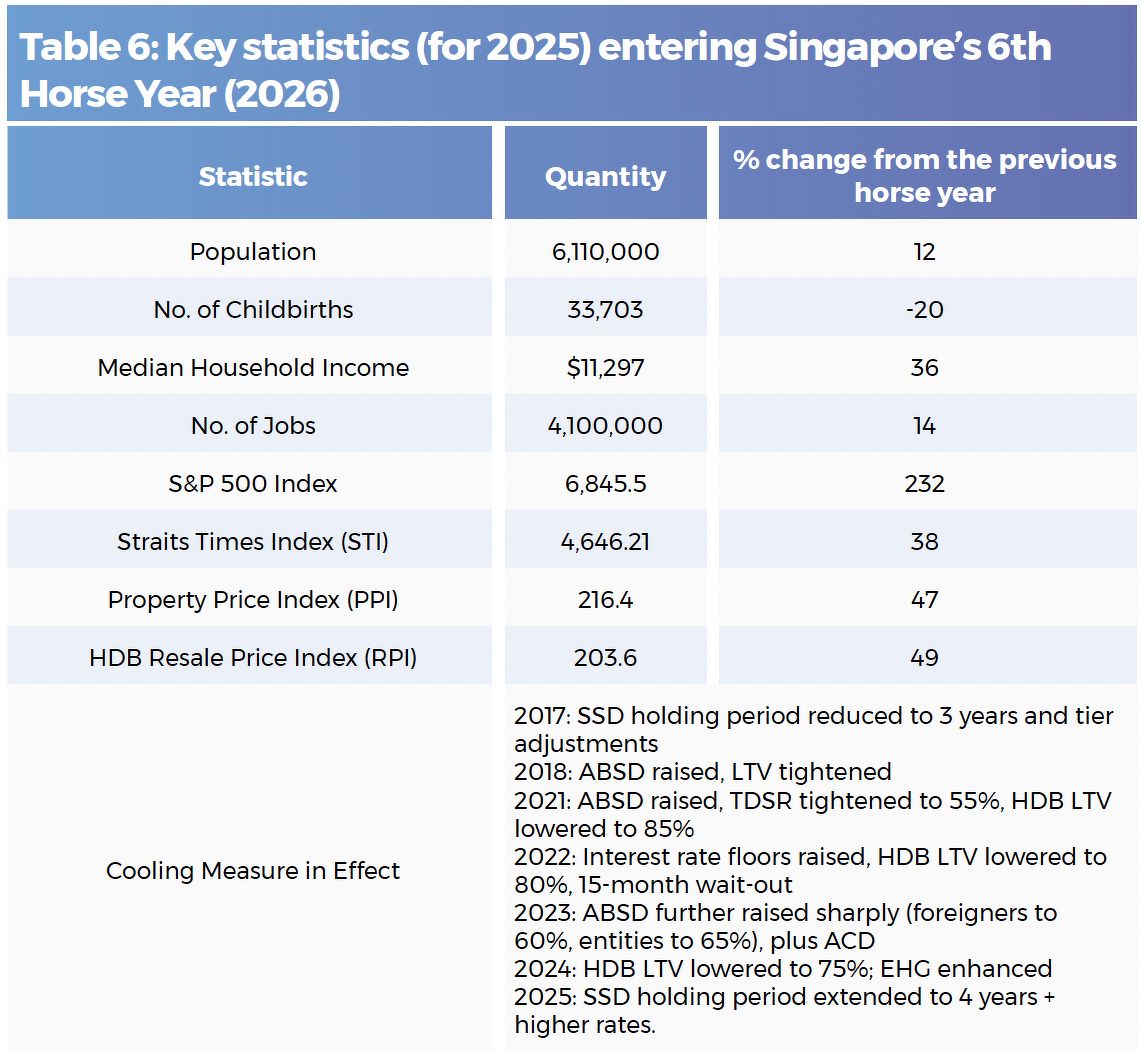

Since 2014, when 42,232 births were recorded, the 10-year average (2014–2024) has fallen to 38,148. In 2025, births are estimated to decline further to 33,703.

As household sizes shrink, these demographic shifts have reshaped housing demand. Developers have introduced smaller unit sizes to maintain price accessibility, while two- and three-bedroom units have become the dominant product type. In the HDB segment, five-room flats are now less common and are largely offered only in Standard-classification projects, reflecting the same shift towards more compact living.

Property trends and what we can expect

While Singapore’s long-term structural growth remains intact, the pace of expansion has moderated in recent cycles, particularly in income growth and equity markets — a reflection of its transition into a mature, developed economy.

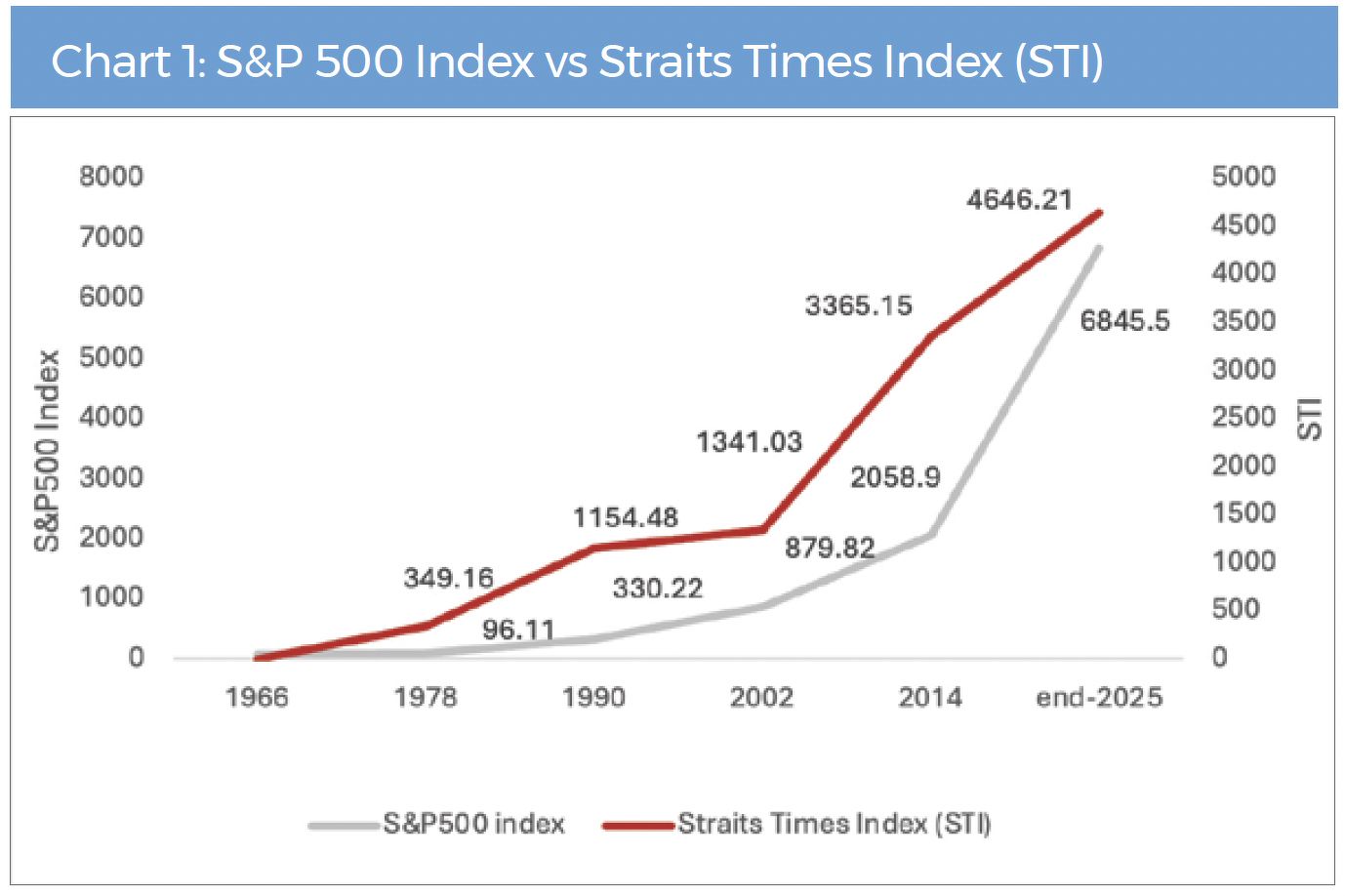

Over the past six decades, Singapore has evolved from a modest trading port into a global metropolis and a leading financial, logistics and technology hub. This transformation is mirrored in the sustained rise of the Straits Times Index (STI), alongside the long-term growth of global benchmarks such as the S&P 500.

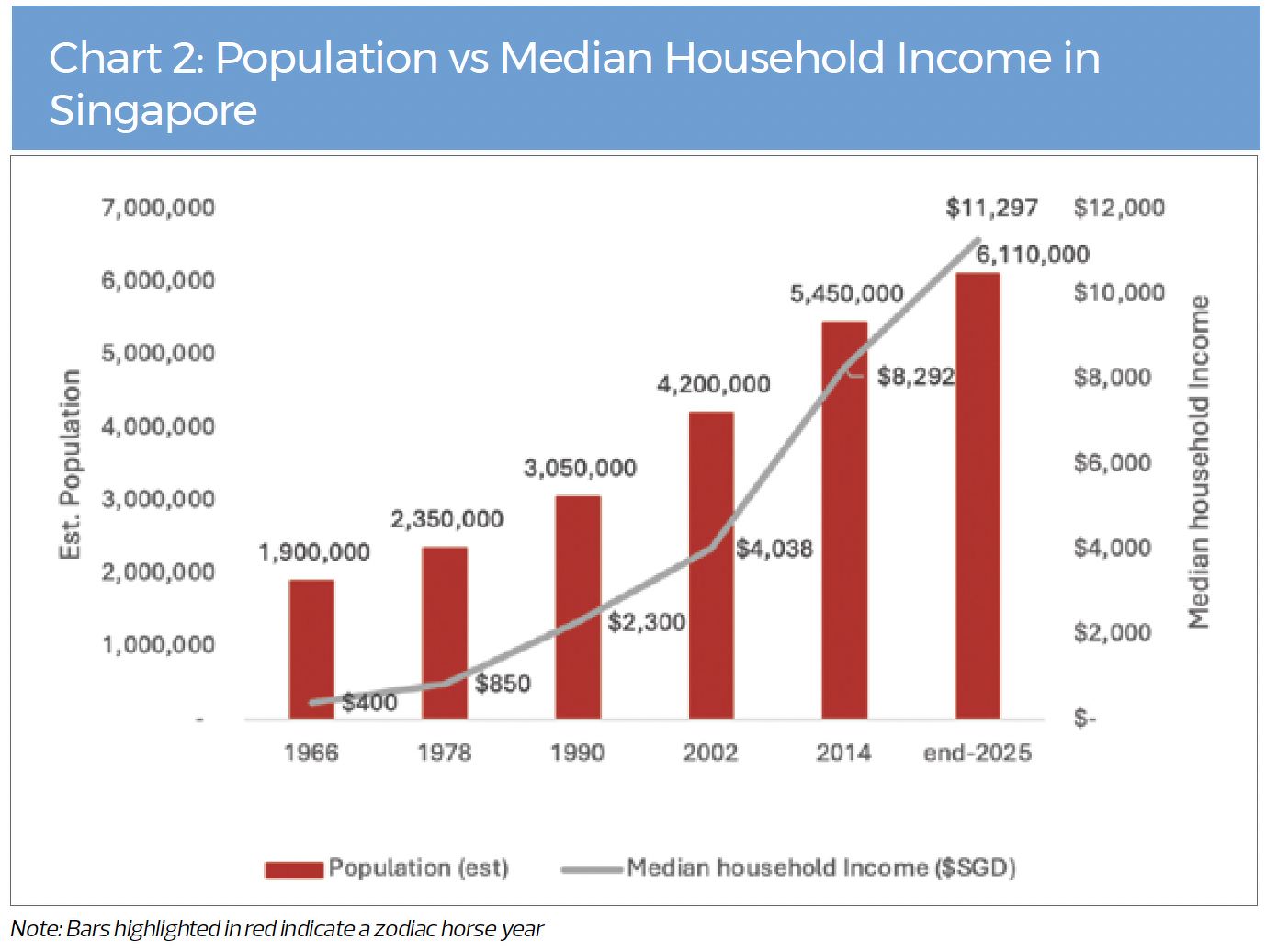

Singapore has experienced sustained growth in both population and median household income. With both now at record highs, attention has naturally turned to the property market to meet the nation’s evolving housing needs.

In previous Horse zodiac cycles, the economy and property market have demonstrated resilience and expansion despite successive rounds of cooling measures. As the Year of the Fire Horse approaches, expectations are once again building. Symbolically associated with dynamism, transformation and potential, it arrives at a time when the next chapter of Singapore’s housing story is unfolding.

New HDB flats are set to be developed in Shunfu and Lakeview — the first new public housing projects in these estates in four decades. At the same time, construction timelines have shortened significantly, with some BTO projects completed in as little as one year and 11 months. This underscores HDB’s commitment to sustaining a vibrant public housing market that responds to Singaporeans’ needs.

In the private sector, a residential site in Tanjong Rhu was sold earlier this month — the first Government Land Sales (GLS) tender in the neighbourhood in 28 years. The site is expected to introduce much-needed new supply in an area with limited recent launches, highlighting the continued appeal of well-connected waterfront locations near the city centre. By 1H2026, strong interest is anticipated for other coveted GLS sites, including Bayshore and Berlayar.

The new home market also has many exciting developments in store for this Fire Horse year. There will be 18 new private home projects and a further five Executive Condo projects are slated to launch in 2026, providing multiple options across different locations for new homebuyers — upgraders, right-sizers and investors alike.

What does the Year of the Fire Horse hold for you?

As we enter the Year of the Fire Horse, it is an opportune moment to reflect on the milestones ahead for Singapore’s economy and housing market. Will the nation continue to build on its strong foundations, fostering greater prosperity and a growing — and thriving — population?

In the year ahead, disciplined confidence and strategic clarity will matter more than speed alone.

I confirm that I have read theprivacy policy and allow my information to be shared with this agent who may contact me later.