Why En Bloc Sales Could Make a Comeback in Singapore’s Property Market

- Ethan Hariyono

- 13 min read

- Blog

- 18 Jun 2026

Singapore's collective sale market may be stirring again.

If you have spent enough time following the Singapore property market, you would probably have come across stories of homeowners receiving substantial payouts after their development was successfully sold for redevelopment.

Often described as “striking the lottery”, these transactions have generated significant wealth for some property owners. But how do such redevelopment sales work, and why are developers willing to pay such large sums for ageing properties?

An en-bloc sale, also known as a collective sale, involves the sale of an entire strata-titled development to a developer for redevelopment. Instead of individual owners selling their units separately, owners collectively agree to sell the land and existing buildings as a single asset, allowing the site to be rejuvenated and intensified for future housing needs.

In Singapore, the process is governed under the Land Titles (Strata) Act, where owners must meet the statutory majority threshold (or reach a unanimous decision) before applying to the Strata Titles Boards or the High Court for a sale order.

En-blocs normally take place for older or ageing developments, where the threshold lies at 80% by share value and strata area. While rare, collective sales can also take place for developments under 10 years old, at a threshold of at least 90%.

En-bloc vs GLS sales

For developers, acquiring land for project development is paramount. Acquiring land to develop into projects is the bread and butter of their business. The easiest way for them to do so would be through the Government Land Sales (GLS) program.

These GLS sites are planned and announced every six months, with a set number of sites sold through the Confirmed List and Reserve List systems. GLS sites offer transparency and fresh leases but have grown increasingly competitive and closely watched.

For all intents and purposes, GLS sites offer developers a relatively straightforward route to land acquisition. They are released with clear technical conditions of tender, where developers will know the parameters and restrictions up front. Furthermore, they come with no demolishment requirements, which saves them valuable time and money.

This gives developers greater visibility when assessing site potential, making valuation and bidding more transparent than many private-market alternatives.

A land acquisition alternative from GLS sites

For developers, collective sales provide an alternative source of developmental land to the Government Land Sales (GLS) program.

The en-bloc market offers sites beyond those offered in the GLS lists. Apart from location, there may be sites that have a freehold tenure compared to all GLS residential sites which come with a 99-year lease.

Over the years, successive Master Plan revisions may have raised the Gross Plot Ratio (GPR) for selected residential sites. This means some older developments may not be at the full development potential. For developers, this creates an opportunity to acquire these sites through an en-bloc sale and redevelop them into larger projects with a higher number of homes.

Notable examples throughout Singapore’s history such as the en-bloc sale of the iconic Pearl Bank Apartments in 2018 (which was the tallest residential building in Singapore when it was completed in 1976) into One Pearl Bank, as well as the en-bloc of Farrer Court in 2007 (a 618-unit HUDC, a 1970s–1980s hybrid housing type for middle-income families), serving as precursors to Executive Condominiums) into d’Leedon for a staggering $1.34 billion.

Case studies like these two redevelopment projects show how en-bloc sales can be used by developers to acquire land in strategic locations (particularly developed or mature estates), while also fulfilling Singapore’s vision of intensifying and making land use more efficient.

While GLS sites remain developers' primary source of land supply, we are observing growing interest in collective sale opportunities as competition for quality sites intensifies. Developers who are unable to secure GLS sites may increasingly explore en-bloc projects, particularly those in mature estates with redevelopment potential.

Why Collective Sales Remain Important In Land-Scarce Singapore

Singapore’s land constraints mean that urban renewal is not simply desirable—it is necessary.

As a city-state with finite land resources, Singapore cannot continually expand outwards. Instead, redevelopment and intensification of existing land parcels play a critical role in meeting future housing needs and supporting population growth.

Collective sales are one of the most effective mechanisms for achieving this objective. Many older developments were built under earlier planning guidelines and may not fully utilise their allowable plot ratio today. Redevelopment allows these sites to be rejuvenated, modernised and, in many cases, intensified to accommodate more homes.

Projects such as Farrer Court and Pearl Bank Apartments demonstrate how ageing developments can be transformed into higher-density residential communities that better align with contemporary housing demand.

Beyond creating new housing supply, redevelopment also improves the quality of Singapore’s built environment by replacing ageing infrastructure with modern homes, updated facilities and more efficient land use.

In this sense, collective sales are not merely a land acquisition strategy for developers. They are also an important urban renewal tool that supports Singapore’s long-term planning objectives and ensures that scarce land resources continue to be utilised efficiently.

En-bloc sites come with more encumbrances than GLS sites

Planning assumptions for en-bloc sites may also be less straightforward than for GLS parcels, which are typically released with prescribed technical and development conditions. En-bloc sales come with drawbacks that GLS sites do not. In addition to the land cost, there are also other costs such as a land betterment charge to top up the land lease for leasehold en-bloc sites. There are also more professional fees involved to assess the site and larger holding costs.

Processes may also be more long drawn. In addition to securing the collective agreement (80%/90% requisite), objections may arise in future, while the legal process can delay or derail a transaction. And with the five-year deadline, time becomes money.

Timelines are also generally longer for en-bloc sites, due to the more complex construction and regulatory processes and demolishment of the existing project. If the developer is unable to obtain an extension, all this will have to fit within the five-year ABSD deadline, which may have a more pronounced effect in larger developments. Developers may also be exposed to possible changes in construction costs and market demand before redevelopment can begin.

Entropy and a resurgence in the en-bloc market

Because of these drawbacks, developers have been lukewarm towards en-bloc sales in the recent years. Furthermore, with successive increase in foreigner ABSD rate in 2018, 2021, and 2023, reaching the collective sale threshold for redevelopments with foreigner households has grown substantially more difficult, due to the higher cost of replacement homes. Demand has likewise fallen, particularly in districts 9, 10, and 15 that feature a higher density of foreigner and expatriate enclaves where en-bloc sales are traditionally popular.

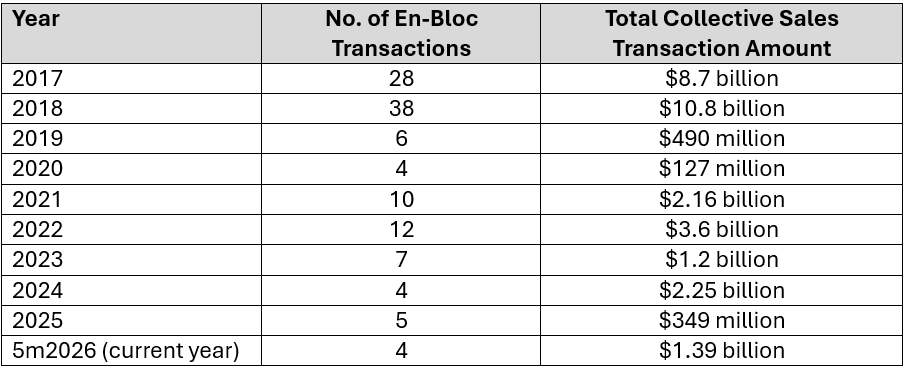

Compared to the en-bloc “boom” witnessed in 2017 and 2018, where the total collective sales transaction amounts were $8.7 billion and $10.8 billion respectively, the highest total collective sales transacted in the last five years was $3.6 billion in 2022.

Table 1: Total collective sales transacted by year, 2017-2026

Instead, developers have turned their attention towards the GLS market, which has proven to be a more streamlined route to land acquisition and project development.

However, with rising land rates and greater competition for GLS sites, alongside saturation in the primary market with several GLS sites launched in areas like Lentor, River Valley, and one-north, developers are starting to set their sights on the en-bloc market again. Where the en-bloc market was once perceived with uncertainty, developers’ perspectives are shifting towards that of opportunity, amid a highly competitive real estate development market.

At the point of writing this article in early May 2026, the total value of en-bloc sites sold stands at roughly $1.39 billion, following the most recent, high-profile sale of Loyang Valley ($880 million).

With High Point Orchard ($580 million asking price) and Balestier Regency ($225 million asking price) open for tender, the en-bloc market is on track to potentially reach $2.25 billion in collective sale value (if both developments are successfully sold). This is on par with 2024’s total amount and on track to outpace the highest total of $3.6 billion witnessed since the 2017/2018 boom.

Despite their drawbacks, why are en-bloc sales starting to pick up speed this year, and what could be the reasoning behind their resurgence?

GLS Sites are Getting More Competitive Despite a High Supply

Since 2024, we have witnessed a larger number of GLS sites released on the confirm list each year. Between the five GLS exercises that commenced between 1H 2024 to 1H 2026 GLS exercises, a total of 42 sites were tendered, compared to only 30 GLS sites awarded in the same timeframe prior.

Table 2: GLS sites awarded from 2H 2021 to 2H 2023 vs 1H 2024 to 1H 2026

Source: URA as of 11 May 2026, ERA Research and Market Intelligence

This reflects a strong underlying demand for land amongst developers, despite the government’s efforts to intensify GLS land supply.

For every fiercely competitive GLS site that is tendered, the more participants in the tender equals to more developers that have missed the opportunity to fill their land bank. This leads to greater competition in bidding prices for future sites (benchmark pricing), which might put certain GLS sites out of smaller developers’ hands.

Developers need to factor in future pricing too: if they are paying higher prices for land, they will have to adjust their future sale prices accordingly. If priced too high, the project might not be appealing to and become unaffordable for buyers. Too low, and the already thin margins could come dangerously close to disappearing.

Chart 1: GLS Land Rates (2024-2025) have been on the rise

In short, real estate development is a gameof numbers. If GLS sites start to become out of reach and unfeasible, developers will have to set their eyes on other land banking alternatives, which could be why we are seeing a crescendo in en-bloc activity this year.

Owners of Older Homes Might be More Compelled to Sell Now Than Ever

Older homeowners who were once reluctant to support an en-bloc sale may also be reassessing their position. For many, the issue is no longer just whether a collective sale offers an attractive premium (via windfalls), but whether it still makes sense to hold on to an ageing asset.

As leasehold properties grow older, lease decay becomes a more visible concern, potentially affecting resale appeal and long-term value. At the same time, the realities of living in an older estate become harder to ignore. These include dated facilities, ageing lifts, water seepage, and worn common areas. Termite infestations, which are more likely to affect older developments, have also been proven to cause incessant headaches for those unfortunate enough to live with them.

These issues can also affect the owners’ pockets. As developments age, higher maintenance fees or special levies may be required for the upkeep of the development. For some households, the trade-off becomes less attractive: they are paying more to maintain a property with a declining lease and facilities that may no longer match newer developments.

In this context, an en-bloc sale may be seen less as a speculative windfall and more as a practical exit route. They present an opportunity to unlock value before the physical condition and dwindling leases become more difficult to ignore.

Outlook: En-Bloc Projects Could Offer Developers a Variety in Development Opportunities

Lastly, en bloc sites offer developers a wider range of redevelopment options because they are not limited to land parcels under the GLS programme. They can be located wherever older private developments already exist, including mature estates where fresh GLS land may be limited. This allows developers to leverage on access to established neighbourhoods that have established schools, amenities, and transport infrastructure.

Moreover, GLS sites have a 99-year leasehold tenure. For developers looking for 999-year leasehold or freehold sites, en-bloc sites are the only option.

Lastly, GLS sites tend to come with fixed planning parameters and technical conditions. In contrast, en-bloc sites can range from small boutique redevelopment plots to large former condominium estates. En-bloc sites are also not constrained to Prefabricated Prefinished Volumetric Construction (PPVC), which could give en-bloc redeveloped projects a greater diversity in their floorplans.

Overall, these factors give developers more options when it comes to project scale, positioning and target market. But at the end of the day, not every ageing condominium is a viable en-bloc candidate. Developers are not only looking at the age of a project, but also whether the eventual redevelopment would appeal to future homebuyers.

This means factors such as proximity to public transport, nearby amenities, schools, neighbourhood appeal and the overall profile of the location will matter. Developers will also assess whether the site is under-utilising its allowable plot ratio, as this could create room for a larger redevelopment with more saleable units. Just as importantly, the reserve price must be realistic enough to leave developers with a workable margin after factoring in construction costs, financing costs, regulatory charges and profit requirements.

Pandan Valley is a useful example. It is an older development near established residential areas such as Holland and Queenstown, and its large land area could offer meaningful redevelopment potential. However, its scale is also what makes it challenging. With owners reportedly agreeing to a S$2.6 billion reserve price in 2018, the site would require a developer, or a consortium of developers, to take on a very large financial commitment. This shows why even attractive en-bloc candidates may struggle to transact if the overall quantum is too high or if the pricing leaves too little room for redevelopment risk.

Conclusion

Ultimately, en-bloc sales are unlikely to replace GLS as developers’ main source of land, but they could become an alternative in today’s market. While the process of bidding for GLS sites is more predictable, competition for such sites is also getting increasingly more stiff and hence more difficult to acquire.

Therefore, any resurgence is likely to be selective. En-bloc sites come with more moving parts: owner expectations, consent requirements, possible objections, demolition costs, lease top-ups, land betterment charges, and longer timelines can create intricacies and complications that developers do not need to face when it comes to GLS sites.

For an en-bloc deal to work, the numbers must make sense for both sides. Owners need to be appeased with a price that justifies giving up their homes, while developers need enough margin after accounting for the full suite of redevelopment costs.

More importantly, collective sales continue to play a broader role in Singapore’s urban transformation story. As the nation seeks to optimise limited land resources, redevelopment remains one of the most practical ways to rejuvenate ageing estates, increase housing supply and support sustainable long-term growth.

For this reason, the next wave of collective sales, may look different from past en-bloc booms. Developers today are more disciplined, focusing on projects where redevelopment economics remain attractive amid higher construction costs and tighter margins. As a result, we are likely to see en-bloc sites in locations with pent-up demand or holding a freehold tenure. The priority is likely to fall on well-located, realistically priced developments where the redevelopment upside is clear. In a market where GLS land remains expensive and closely contested, en-bloc opportunities may once again find their place.

I confirm that I have read theprivacy policy and allow my information to be shared with this agent who may contact me later.