A brief history of Singapore’s North Region

In the years around and after Singapore’s independence, the North region of Singapore – comprised of Sembawang, Woodlands, and Yishun remained largely undeveloped. These areas served as kampungs, rubber plantations, and in the case of Sembawang, home to a naval base – both under British and Singaporean power.

Development in the north started with Yishun New Town in the 1980’s, followed by Woodlands later in the decade. Woodlands then rapidly took shape, growing into the regional centre. It featured the town’s transformation into the North’s largest residential town, featuring residential, industrial, and commercial developments.

The 90’s saw a decade of further change for the North, with the opening of Woodlands MRT as part of the North South Line expansion, and the subsequent opening of Woodlands checkpoint in 1999. This marked Woodlands as an important commercial and transport hub for Singaporeans and Malaysians alike, who would often transit through the regional centre to move between the two countries.

Sembawang Naval Base in the time of colonial rule

Interestingly, throughout these two decades, Sembawang remained relatively untouched as a naval base, until the turn of the millennium where we began to see a shift towards a residential town and estate through the construction of HDB flats.

Sembawang Today

Today, Sembawang has grown into a fully-fledged residential town. Its naval heritage remains, with road names in the town paying homage to the British naval vessels that once used to grace the docks of the northern town. A prominent example of this would be the planning subzone Canberra, named after the old HMS Canberra.

A visit to Sembawang today would present you with the picture of an idyllic suburban estate. The town is quiet and peaceful, particularly due to its lower density. Of all the residential towns in the North region, Sembawang is by far the smallest, housing just over 30,000 dwelling units.

Sembawang today is a quaint residential town, with around 30,000 homes

In comparison, Woodlands, the regional centre of the North is home to almost 72,000 dwelling units, while Yishun, the other large residential town in the north is also home to over 69,000 of such homes.

With less than half as many homes, it is evident that Sembawang has received less love than its neighbours. But with a projected ultimate capacity of 65,000 – over double of the current inventory in the area, it is clear that Sembawang will be the next town to experience rapid development.

Bukit Canberra

Spearheading Sembawang’s development and transformation into a new-age residential town is Bukit Canberra, an integrated community and sports hub.

Partially opened since 2021, Bukit Canberra is modelled after Our Tampines Hub, aiming to integrate community focused amenities such as healthcare and dining with sports facilities to promote a greener and more active lifestyle among Singaporeans.

The facility comprises extensive sports facilities, such as indoor and outdoor lap pools, 3km of running trails, a polyclinic, a senior care centre, and a hawker centre with 800 seats and over 40 stalls.

Despite being an entirely modern and new development, Bukit Canberra also does its best to preserve Sembawang’s roots. It is built on the site of the old Chong Pang Village market and hawker centre and will house the refurbished Admiralty House into a library full of historic stories of Sembawang’s naval past during colonial times.

Other Amenities

Shopping and Retail

Despite its small size, Sembawang is home to two shopping centres, Sun Plaza (located next to Sembawang MRT) and Canberra Plaza, an integrated development next to Canberra MRT.

Across the two malls spanning both the neighbourhood’s MRT stations, residents have easy access to amenities and services such as grocery stores, dining options, clinics, enrichment centres, and retail shops. These options easily provide day-to-day necessities for its residents, while alternatives can be easily accessed within 5 minutes at either Yishun or Woodlands, which boast large shopping malls of their own.

Sun Plaza, one of the malls that serve the residents of Sembawang

Nature and Recreation

In terms of recreation, Sembawang is home to its very own Sembawang Park, which is a seaside park with beaches, barbecue pits, and views of the Johor Strait.

Sembawang is also unique as it is home to Sembawang Hot Spring Park, the only natural hot spring park in Singapore. Visitors can enjoy foot-soaking pools and heritage exhibits in a well-maintained and landscaped setting.

Sembawang Hot Spring park is home to the only natural hot spring in Singapore

Transport and Accessibility

Sembawang is connected to Singapore’s transport network through two stations on the North-South Line, Sembawang and Canberra. The line connects Sembawang directly to the city centre in around 30-minutes.

The most recent Thomson-East Coast Line runs through Woodlands MRT station, a mere two stop from Sembawang. The additional line provides access to additional locations, such as various parts of Woodlands, and even all the way through to the east coast of Singapore.

In addition to this, various feeder buses serve the town, providing easier access to nearby MRT stations for residents that might stay slightly out of walking distance from the MRT.

North-South Corridor

Sembawang will also directly benefit from the future North-South Corridor (NSC). The 21.5km multi-vehicle expressway will directly connect Woodlands to Marina Bay and promises a much faster commute to the city for residents in the North region.

The NSC will cut travel times by 10-15 minutes during peak hours, and reduce the reliance on the often-congested Central Expressway. There will also be express bus services to serve those that do not own a vehicle, allowing them a much faster commute on public transport to the city centre.

A New Neighbourhood in Sembawang North

You might ask: what’s the purpose of constructing so many amenities for a town with such a low number of residents? With many plans for development in Sembawang, the picture starts to become clear.

Announced by the Ministry of Development and Housing Development Board in October 2024, we can expect around 8,000 BTO flats and 2,000 new private housing units to be constructed in Sembawang North, a planned 53-hectare residential neighbourhood.

This starts with the BTO exercise in July 2025, where a 775-unit development, Sembawang Beacon will be the first of many housing projects that will occupy the up-and-coming neighbourhood. Additionally, the project completion timeline is slated to be under three years, as it is classified as a Shorter Waiting Time (SWT) project.

SWT projects are normally selected in up-and-coming locations with ample development potential, shoring up confidence that Sembawang North’s development is a priority.

What about the Private Market?

Sembawang is also receiving further development interests in the private and executive condominium markets as well. Currently, there are a few non-landed private homes in the town. As the town still has much room to grow, we can expect many more new condominiums and even ECs built here in the future.

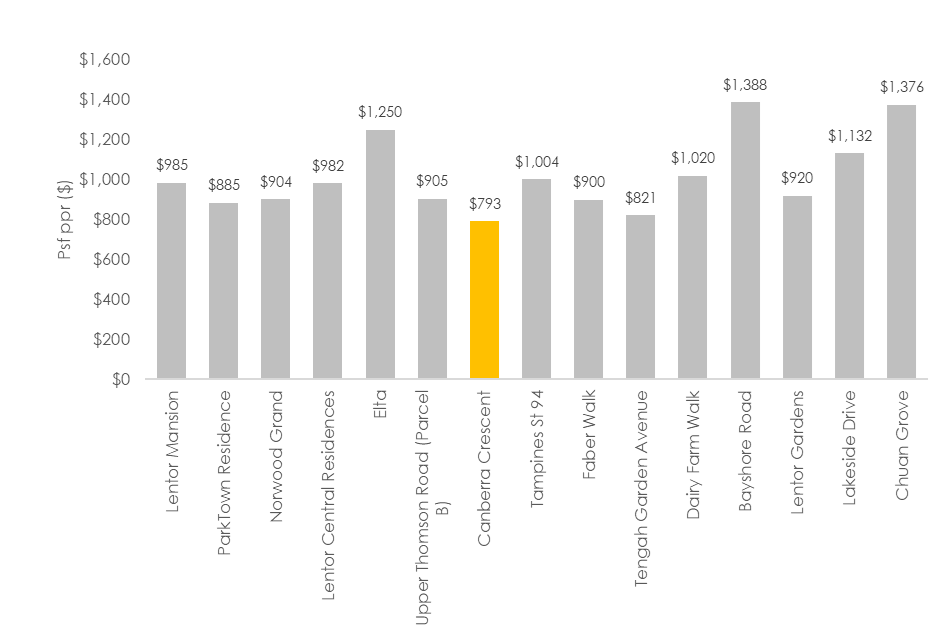

In July 2024, a private residential land parcel was sold via the Government Land Sales at Canberra Crescent.

Chart 1: Land Cost for OCR Private Non-Landed Developments

Source: URA, ERA Research and Market Intelligence as at 21 July 2025

Furthermore, the GLS plot at Canberra Crescent was also tendered at a more attractive land rate compared to other Outside Central Region (OCR) sites. With a land rate of $793 psf ppr, Canberra Crescent Residences, slated to launch in Aug 2025 should feature attractive pricing, allowing buyers to buy into the estate at an accessible price point.

The last new condominiums in the area were The Watergardens at Canberra and The Commondore, both which were launched in 2021. Since then, we have witnessed resale transactions averaging $1,755 psf at The Watergardens at Canberra. This resale price, a significant increase from the median price of $1,469 psf witnessed during its launch month highlights the area’s growth and potential.

Chart 2: Canberra Crescent GLS and EC price comparison

Source: HDB, URA, ERA Research and Market Intelligence

With a land rate that is comparable with that of the last 3 EC sites tendered, Canberra Crescent Residences should offer a compelling alternative for a private property upgrade to HDB owners in the surrounding estate that might have originally been considering an EC instead.

Executive Condominiums (EC)

Recently, in May 2025 we also saw the opening of a GLS tender for an EC site at Sembawang Road. This is the first EC introduced in Sembawang since 2021. The introduction of ECs is a great way to support the development of the town and provides a sustainable upgrading and housing option.

There is currently no stock for ECs, with North Gaia, the last EC launched in the North region having sold out the remainder of its units earlier this year. While there is certainly a supply gap in the market for North region ECs, the demand for this Sembawang site might be moderated by another EC parcel that is currently on sale at Woodlands.

Conclusion

From the full completion of Bukit Canberra, to the upcoming BTO, EC, and private home launches, there is much to be excited about for the quaint town of Sembawang.

The prospect of staying in the North is getting better as time goes by, with developmental plans for not only Sembawang, but in Yishun (the new precinct Chencharu), and Woodlands (Woodlands North Coast and Woodlands regional centre).

With much to look out for – now might very well be the right time to consider investing or staying in Sembawang. If you are curious on how you can do so, do not hesitate to speak to an ERA Trusted Adviser today.

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.

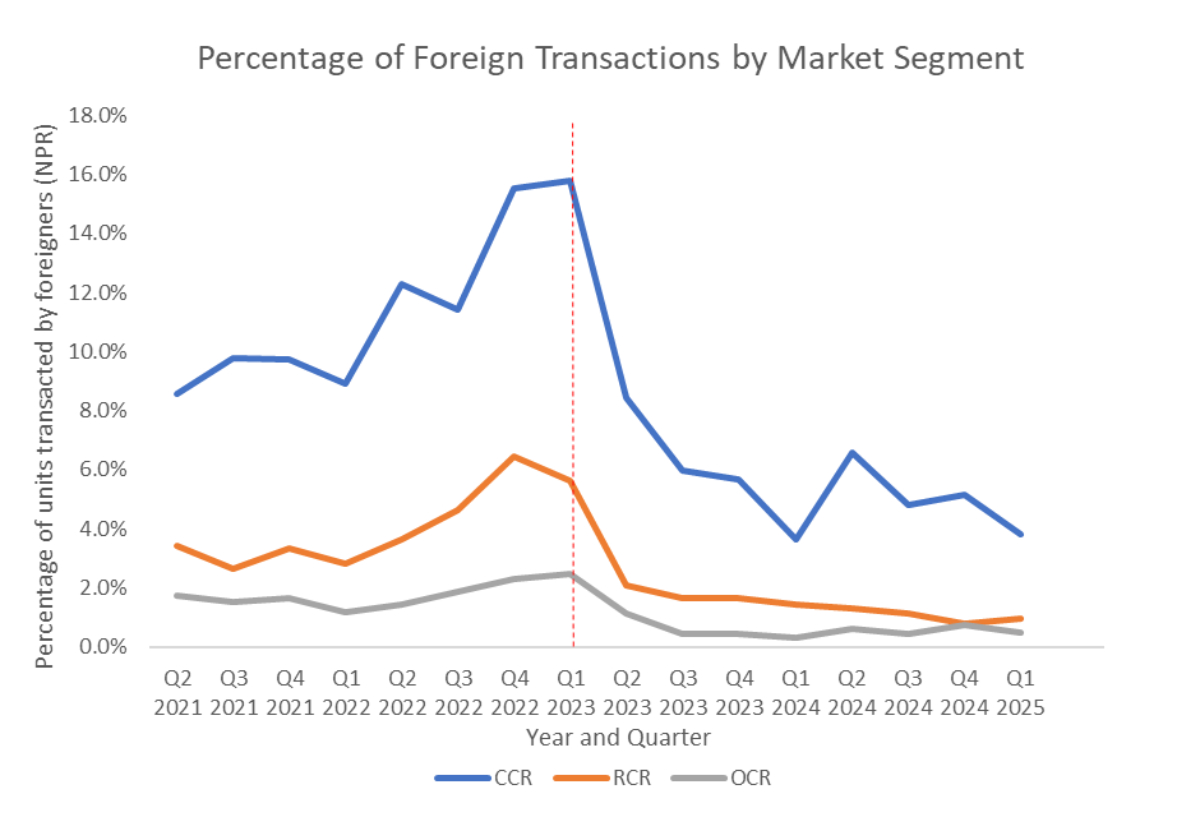

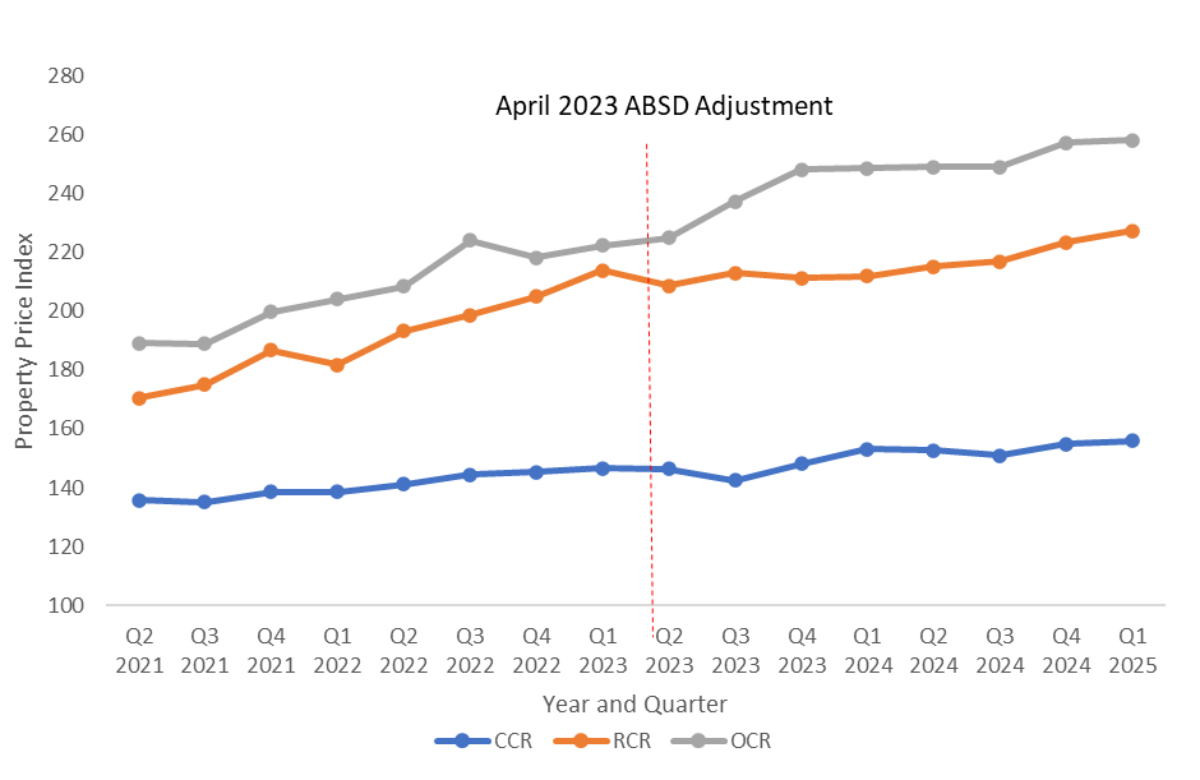

This is part two of the ABSD article series, which analyses the impact of ABSD adjustments on foreigners – the first part is here.

Disclaimer: This article will examine skilled foreigners who are not classified as High Net-Worth Individuals (HNWIs) and are not covered by the benefits of the free trade agreements (FTAs) established with Singapore.

Attracting skilled foreign professionals has long been a strategic policy adopted by the Singapore government in response to demographic challenges, including a rapidly ageing population and low birth rates. However, with the current high ABSD environment for foreigners, this raises questions about whether the increased foreigner ABSD discourages foreigners from coming to Singapore to settle and contribute to the economy.

Demographic challenges faced in Singapore

Singapore has been experiencing a decline in birth rates. As of 2024, Singapore’s resident total fertility rate remains at a historic low of 0.97 births per woman since 2023, with an average decline rate of approximately 4.28% year on year. Even the culturally significant “Dragon Year” in 2024, which is traditionally associated with birth spikes, failed to boost Singapore’s fertility, reflecting shifting priorities and goals among young couples.

Chart 1: Birth rate in Singapore (2015-2024)

Source: singstat.gov.sg

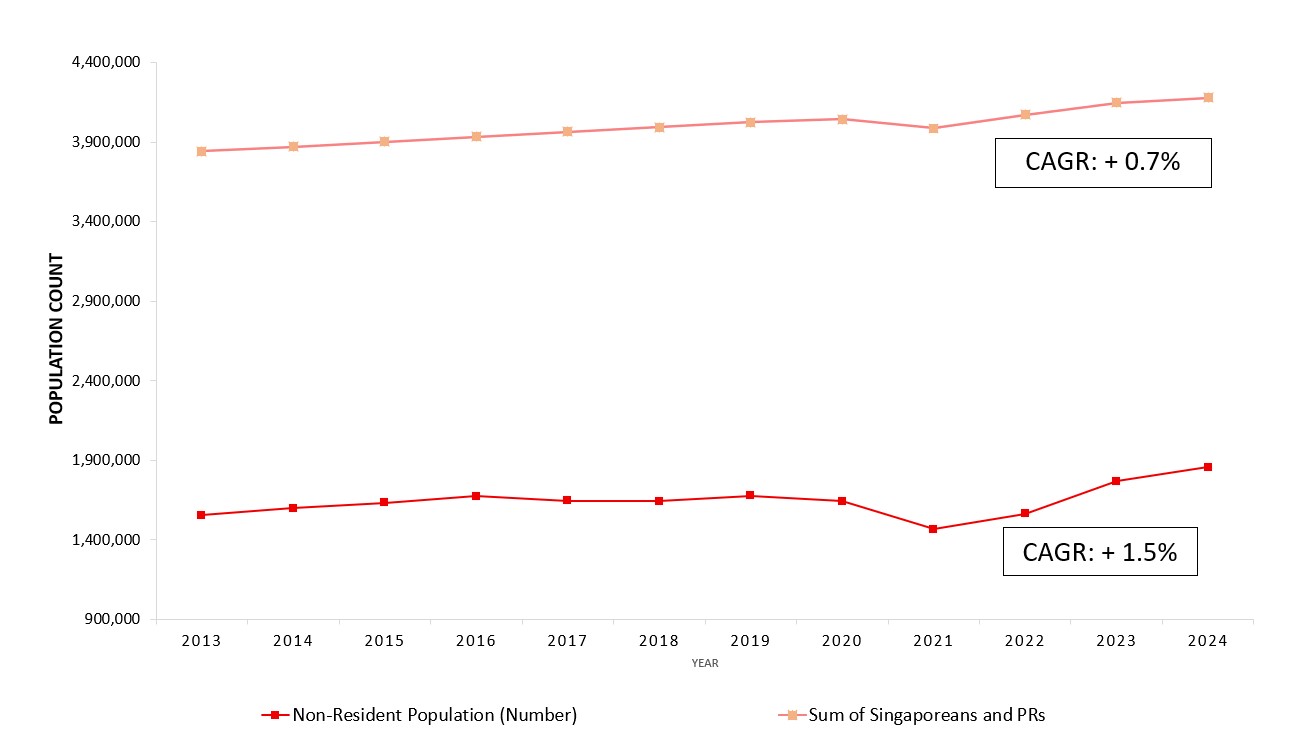

As highlighted in the Population White Paper 2013, Singapore’s total population is expected to reach between 6.5 and 6.9 million by 2030. However, growth rates for Singaporeans and Permanent Residents have been sluggish, with a compound annual growth rate (CAGR) of +0.7%. This contrasts with a higher growth rate for non-residents, at a CAGR of +1.5%.

The current population of Singapore is 6 million, with a total of 30,808 resident live births as of 2024. Assuming the birth rate remains constant, it will be very difficult to reach the target of 6.5 million by 2030 without either significantly increasing the local birth rate or attracting more foreign nationals. This shows that foreigners continue to play a vital role in supporting the overall population and helping to achieve a higher population goal.

As such, we observed the Singapore government implementing a two-pronged approach: encouraging locals to have children through incentives like the Baby Bonus Scheme, and attracting foreigners to Singapore to establish businesses, such as the Overseas Networks & Expertise Pass (ONE Pass) introduced in Jan 2023.

Chart 2: Population growth of Singapore (2013- 2024)

Source: singstat.gov.sg

Attracting foreign skilled workers to migrate to Singapore, settle, and contribute to the economy has therefore been a key message echoed by the Singapore government, compelling Singapore to remain open to global talent to sustain its economic resilience and international standing.

How does ABSD impact decision-making for foreigners who want to purchase property in Singapore

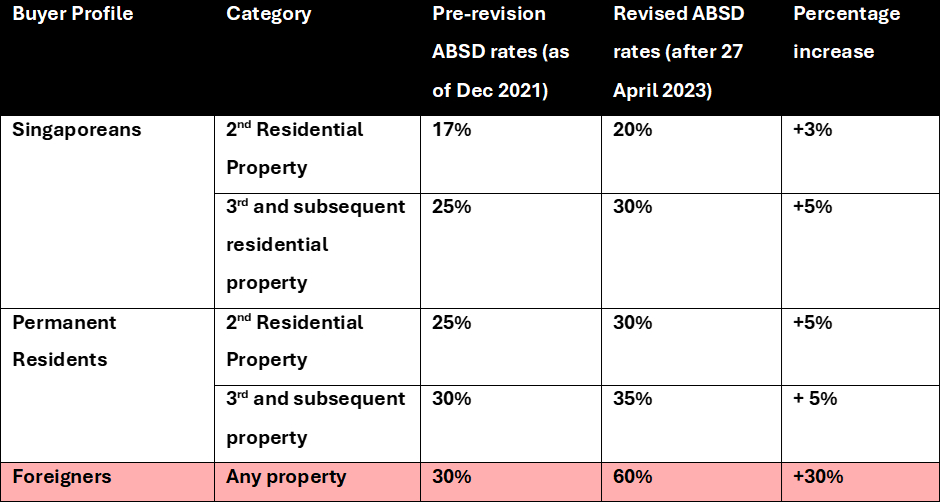

While the high ABSD rates do prevent speculative demand, they also impact foreigners who plan to purchase private property for long-term residence. The 60% ABSD rate on a first property for foreigners results in a significant cost difference compared to SPRs, who only pay 5%. Consequently, there is a financial disincentive for foreigners to establish their roots here through property ownership.

Table 1: Calculation of ABSD when purchasing first property

Source: ERA Research & Market Intelligence

Therefore, the most practical way for foreigners to buy property for personal residence is to initially rent then apply for PR status to minimise the ABSD tax burden. However, this approach may not be sustainable in the long term.

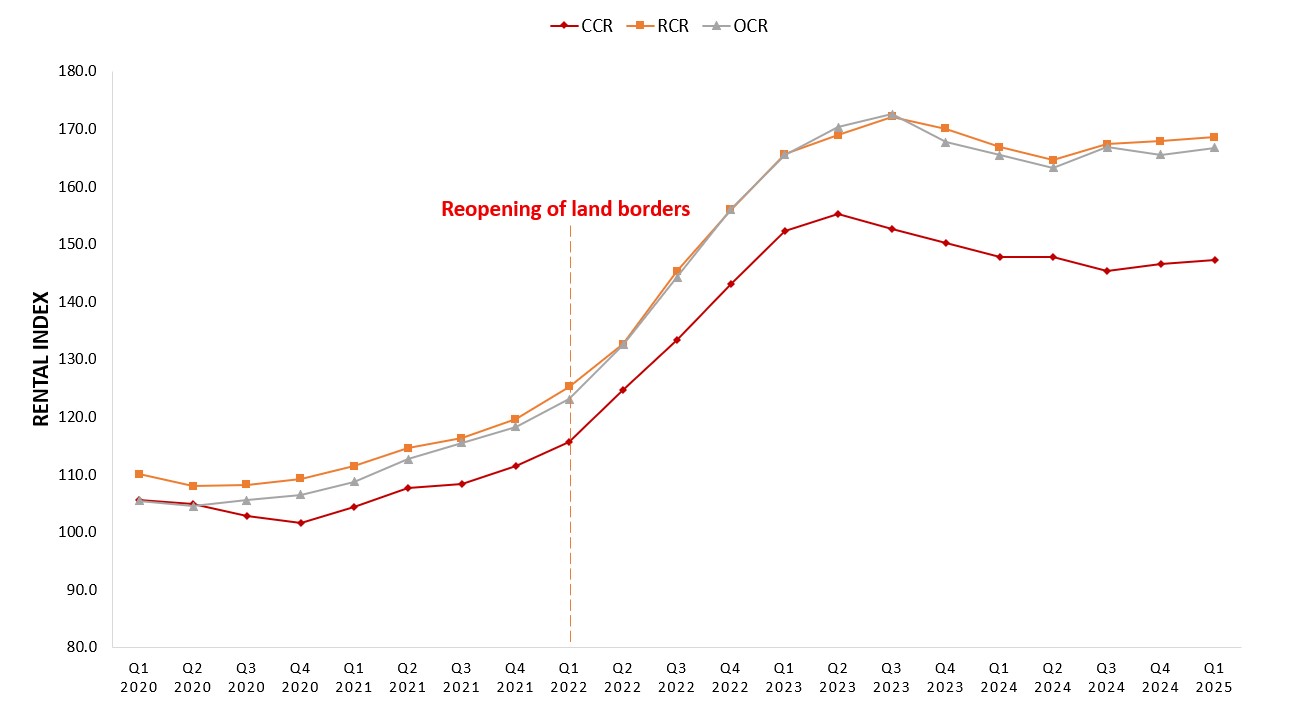

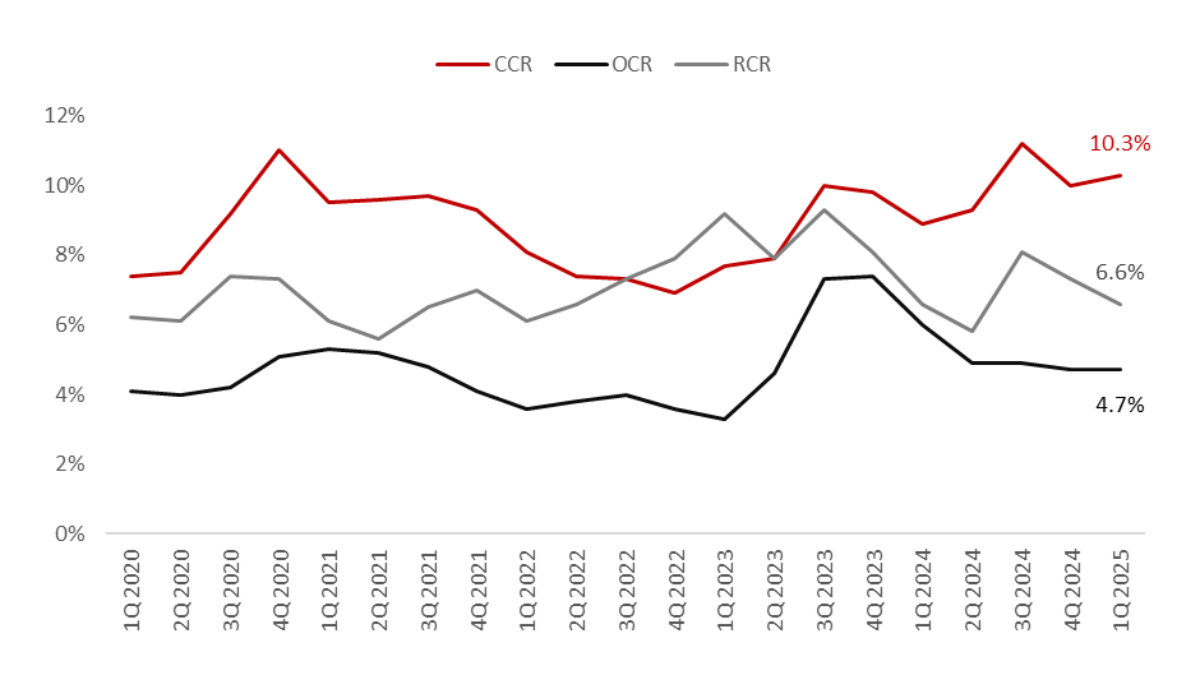

Looking at the Rental Price Index (RPI), rents have surged since the end of COVID, likely due to the reopening of borders and an influx of new foreigners. The sustained high level indicates strong rental demand, with the index remaining consistently above 160 for OCR and RCR segments since its peak in 1H 2023.

Chart 3: Rental Price Index Across Market Segments (1Q 2020 – 1Q 2025)

Source: URA REALIS, ERA Research & Market Intelligence

Moreover, rents are increasingly taking up a significant portion of monthly income, especially for foreigners holding Employment Passes and S-Passes. Based on average monthly rental data for a typical 2-bedroom private unit, foreigners on S-Passes will face rental costs that exceed their current qualifying salary of $3,150. For foreigners on an Employment Pass, the average rent for CCR units accounts for approximately 90% of their minimum monthly qualifying wage of $5,500, whereas renting units in the RCR and OCR will take up approximately 56% to 70% of their monthly income.

Such figures thus highlight the financial strain faced by middle-tier foreign professionals in securing affordable rents while waiting for their PR approvals.

Chart 4: 5-Year Average Monthly Rent For a 2-Bedroom Private Non-Landed Property (2020-2025)

Source: URA REALIS, ERA Research & Market Intelligence

HDB rental rates to remain strong

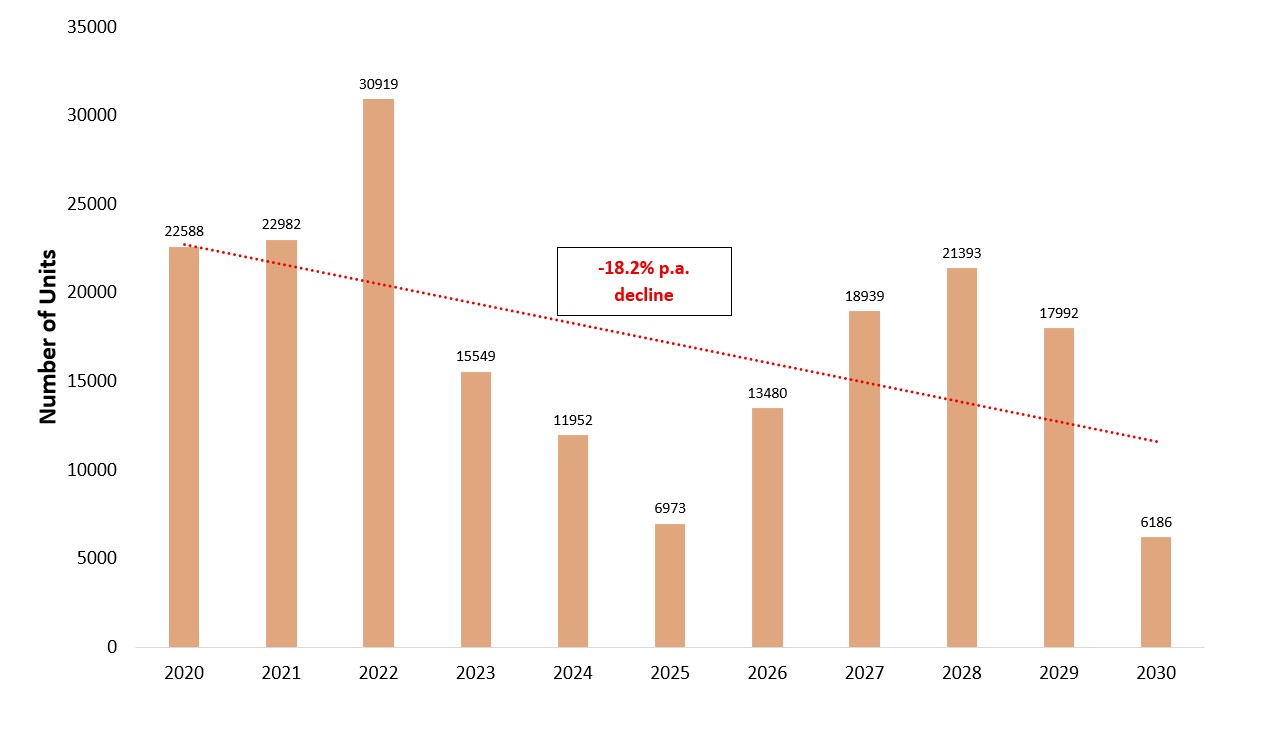

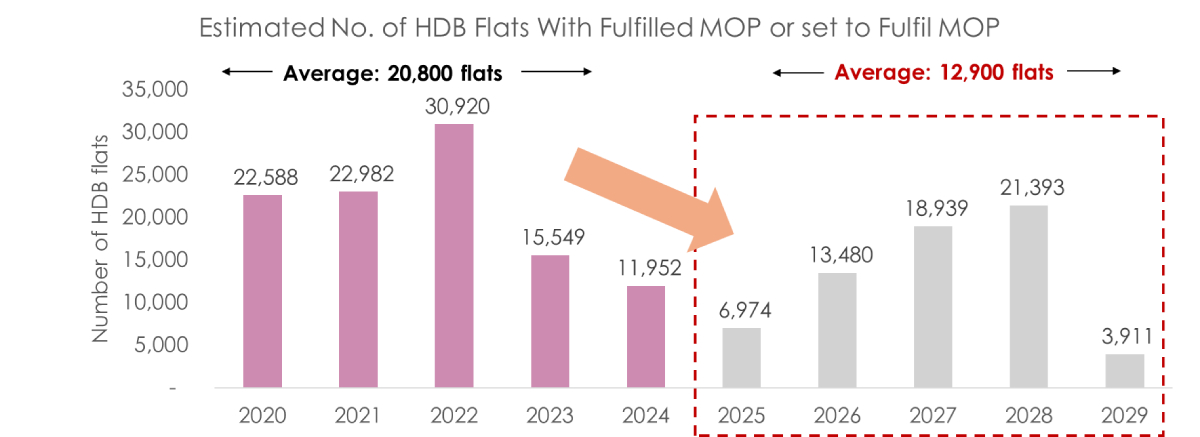

Alternatives such as renting HDB flats, while an affordable option for foreigners, are likely to see more rental price increases as the number of MOP flats continues to tighten at an average rate of 18,2% decline per year, decreasing the number of flats entering the rental market. Considering possible competition from local renters and price-sensitive tenants amidst the current economic uncertainty, demand for HDB rentals might rise and persist, applying more upward pressure on rental prices. However, not all flats reaching their Minimum Occupation Period translate into rental stock; a significant proportion remains owner-occupied, which caps the HDB rental supply.

Chart 5: Number of HDB flats reaching the 5-Year MOP period

Source: data.gov.sg, ERA Research & Market Intelligence

Amidst supply-side constraints, foreigners who opt for the rent-and-wait approach will face higher costs and might not prove to be a suitable long-term solution for owning a property in Singapore. This adds to the already lengthy and stringent process of obtaining a SPR, which involves multiple criteria and considerable uncertainty.

Is it time to rethink ABSD for Foreigners Who Intend to Stay Long Term

To better align housing policy with Singapore’s broader population and foreign talent objectives, adjustments can be considered to the current ABSD policy for foreigners while maintaining its deterrent effect on speculative demand.

One potential policy recommendation is a tiered ABSD remission scheme for foreigners who demonstrate genuine intent to reside long-term, rather than purchase for investment purposes. Conditions such as obtaining PR status and meeting minimum occupancy targets can be considered to further encourage foreigners for long-term stay.

Table 2: Example of a tiered ABSD Remission Scheme (up to 30%)

Conclusion

As Singapore navigates demographic shifts and global competition for foreign talent, its housing policy must also adapt accordingly. Looking beyond the use of ABSD as a deterrent, a targeted and effective ABSD policy for foreigners could remove key obstacles in Singapore’s population strategy.

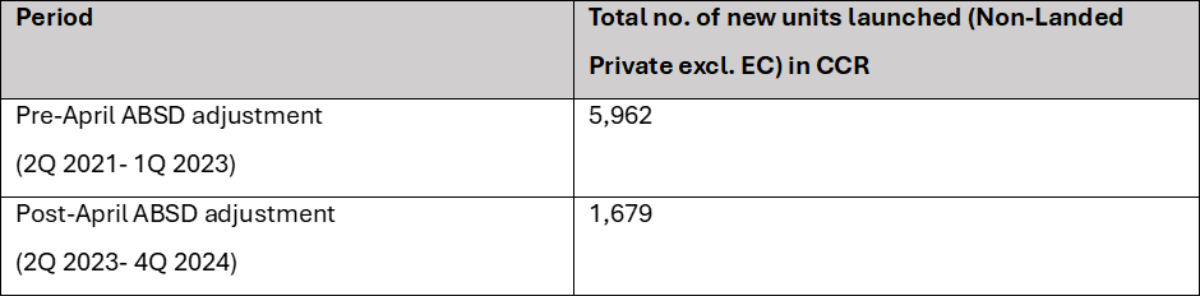

On that note, in part 3 of our article series, we will expand this discussion by examining the Core Central Region (CCR). This market is the most vulnerable to foreign buyer trends and is therefore crucial to analyse what is needed to sustain long-term market resilience despite the high ABSD environment.

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.

The Government has announced two changes to the Seller’s Stamp Duty (SSD) for residential properties:

(a) An increase in the holding period from three to four years, and

(b) increase of the SSD rates by four percentage points for each tier of the holding period.

These changes will take effect for all residential properties purchased on and after 4 July 2025, 12.00am. The revised SSD will not affect HDB owners due to the Minimum Occupation Period for HDB flats.

The Government has announced two changes to the Seller’s Stamp Duty (SSD) for residential properties:

- An increase in the holding period from three to four years, and

- An increase of four percentage points in SSD rates for each tier of the holding period.

These changes will take effect for all residential properties purchased on or after 4 July 2025, 12:00 a.m. The revised SSD will not affect HDB owners, as it is subject to the Minimum Occupation Period for HDB flats.

This reversion to the pre-2017 SSD holding period of four years aims to reduce speculative demand by lowering the number of sellers who flip their homes after just three years.

According to IRAS, the SSD for residential properties is payable for properties acquired after 20 February 2010. In most instances, the date of purchase/ acquisition of a property refers to:

-

- Date of Acceptance of the Option to Purchase* or

- Date of Sale and Purchase Agreement or

- Date of Agreement for Lease (for new HDB flat) or

- Date of transfer to a beneficiary where the property was originally held on trust for non-identifiable beneficial owner(s) or

- Date of Transfer where the above (a), (b), (c) and (d) are not applicable

*Excludes an Option to Purchase that is subject to the execution/ signing of the Sale and Purchase Agreement

ERA’s Take on the Changes:

“These adjustments to the SSD framework will help reduce speculative activity, although they will affect only a small minority of buyers. We welcome the changes and believe they will complement broader measures, such as increasing land supply, to foster a sustainable market.

Since most homebuyers are genuine owner-occupiers or longer-term investors, this measure is a gentle touch rather than a heavy-handed approach on the overall market. It aims to stabilise any spikes caused by short-term investors. It is not designed to crack down on the market but to reduce the froth from investors who sell shortly after the third year.

Notably, the elevated interest rates since September 2022 have eroded meaningful profits for property investors, which may have led them to extend their holding periods, especially now that interest rates have eased in recent months.

The property tax revisions introduced in 2023 have also resulted in higher taxes on non-owner-occupied residential properties, which may have contributed to this trend as well.

Investors have shifted towards a medium- to long-term holding strategy to increase rental income while waiting for prices to reach their preferred levels before selling. This requires greater endurance, but most now have that capacity and plan their exit strategies accordingly,” said Marcus Chu, Chief Executive Officer, ERA Singapore.

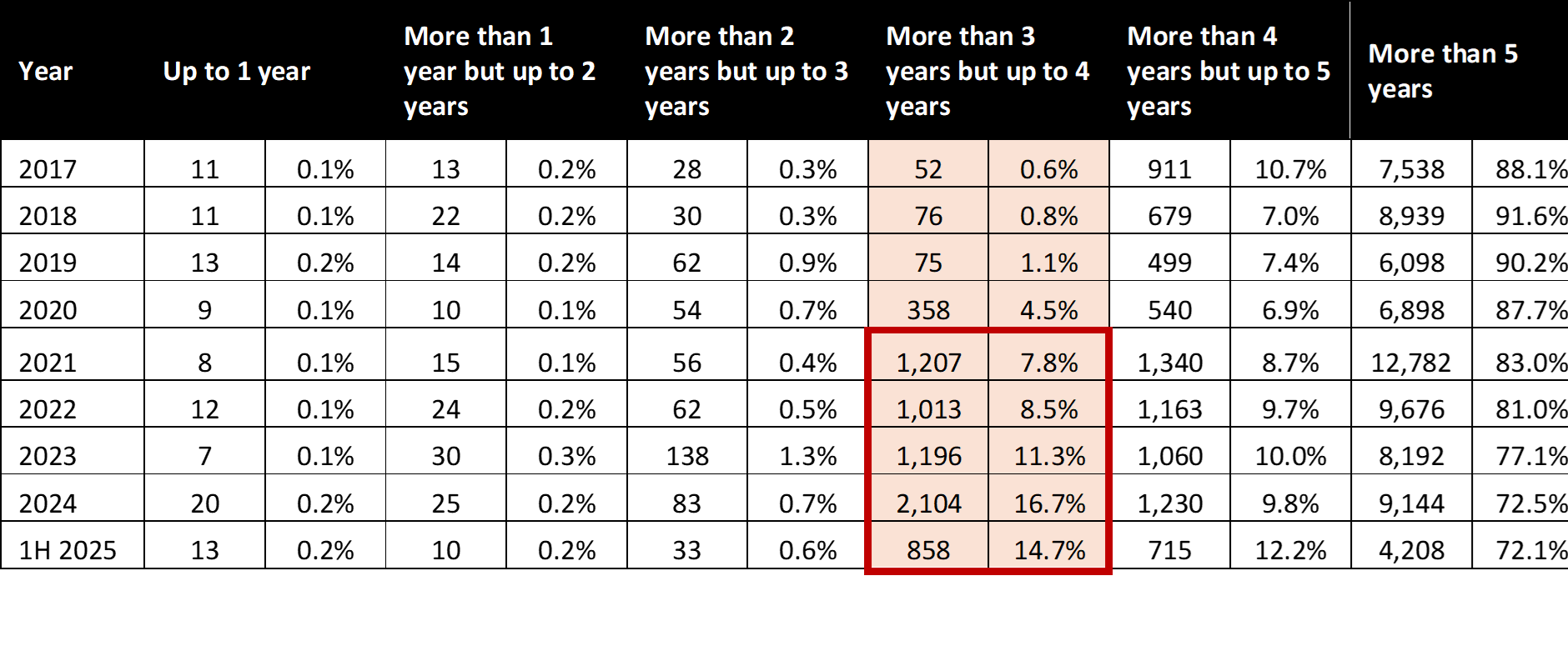

Table 1: Seller Stamp Duty Schedule

Source: MND, MOF, MAS, ERA Research and Market Intelligence

While more owners are selling after holding their homes for three to four years in recent years, they remain a minority.

There has been a significant jump in sellers who sold their homes after holding for more than 3 years but up to 4 years since 2021.

According to URA caveats, in 2020, only 358 sellers sold their non-landed homes after holding them for three to four years; however, by 2024, this number had surged to a peak of 2,104 sellers. In 1H 2025, sellers who had held their non-landed homes for more than 3 years but up to 4 years accounted for 858 transactions, or 14.7% of the total transactions.

Despite this increase, the majority of homeowners continue to sell only after holding their properties for five years or more.

In 1H 2025, about 72.1% of homeowners sold their homes after five years. This trend is further supported by SingStat data, which shows that the proportion of owner-occupied residential households remained high at 90.8% in 2024.

Table 2: Breakdown of Non-landed private homes sold by holding period

Source: URA, ERA Research and Market Intelligence

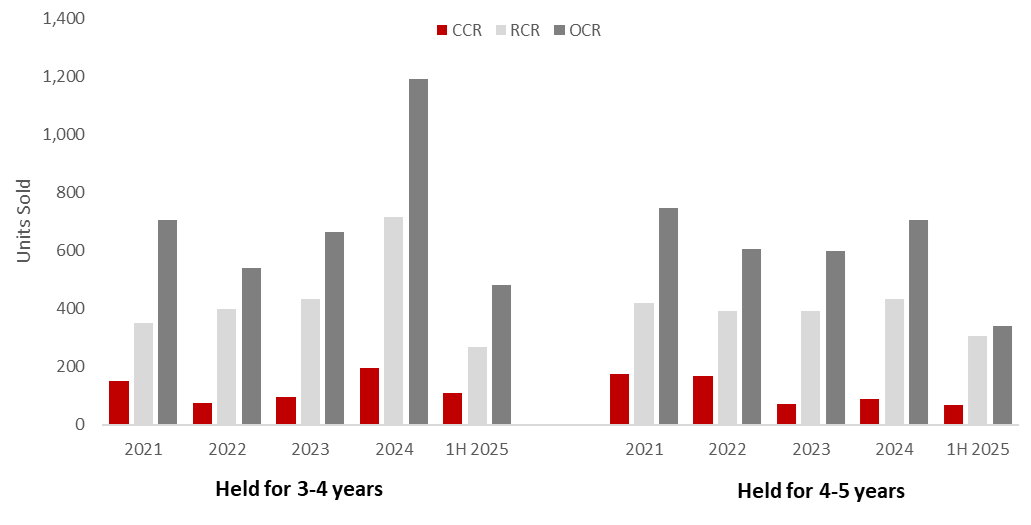

Outside Central Region saw the highest volume of homeowners selling within 3-4 years

Among the regions, the Outside Central Region (OCR) saw the highest volume of homeowners selling within 3-4 years, followed by the Rest of Central Region and the Core Central Region. This could be largely due to the more palatable price quantum of OCR homes compared to the other regions.

Chart 1: Breakdown of Non-landed private homes sold by Market Segment

Source: URA, ERA Research and Market Intelligence

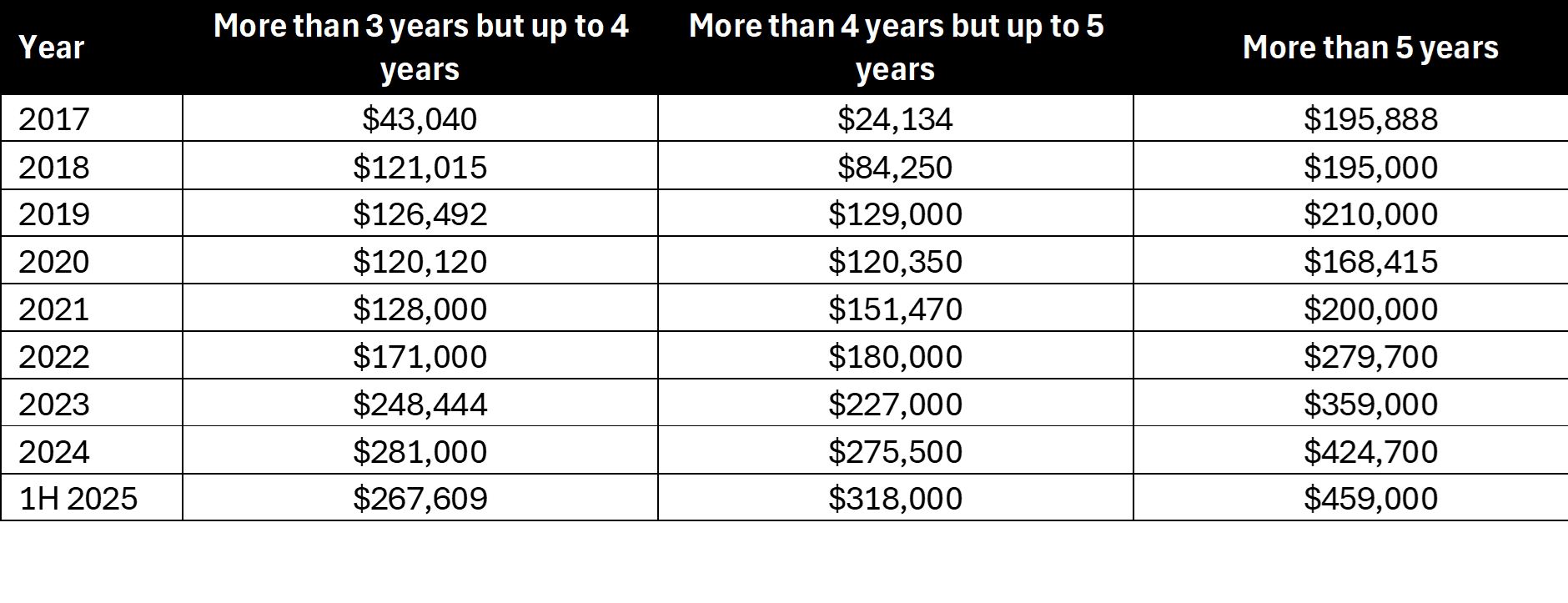

Higher interest rates and property tax saw more investors extending their holding periods despite significant profits

Looking at the median gross profitability of non-landed homes by holding period shows that while there are significant profits to be made after holding for three to five years, sellers who held their properties for more than five years saw the highest profitability.

Table 3: Median Gross Profitability of Non-landed private homes sold by holding period

Source: URA, ERA Research and Market Intelligence

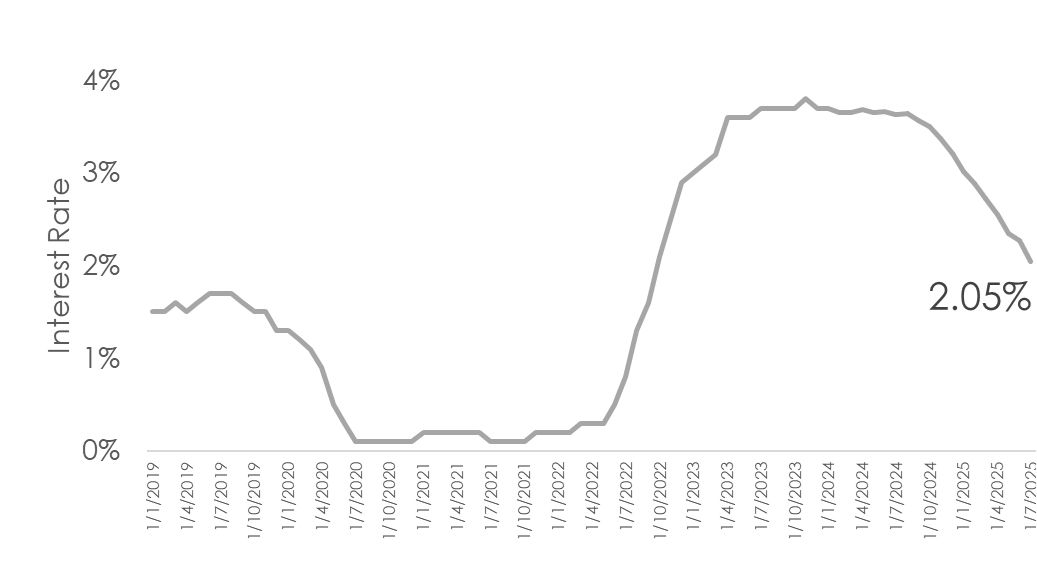

Notably, the elevated interest rates since September 2022 have eroded meaningful profits for property investors, which may have led them to extend their holding periods, especially now that interest rates have eased in recent months. The property tax revisions introduced in 2023 have also resulted in higher taxes on non-owner-occupied residential properties, which may have contributed to this trend as well.

Chart : 3-month Compound SORA

Source: MAS, ERA Research and Market Intelligence

In conclusion

With the introduction of additional Buyer’s Stamp Duty tiers in April 2023, the residential market has shifted primarily towards local and owner-occupier demand.

Alongside increasing economic uncertainty in recent months, buyers have become more cautious, and more now view property as a long-term investment. We are likely to see property investors, who often buy and sell their units within three years, most affected by this change. However, the majority of homebuyers, who are owner-occupiers and long-term investors, are unlikely to be impacted.

ERA welcomes the adjustments to the SSD and expects the impact to be marginal on the overall market, as demand is primarily from owner-occupiers. The SSD revision will work alongside other policies, such as increased land supply, to support a more sustainable and stable housing landscape.

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.

The Financially Independent, Retire Early (FIRE) movement is not new to Singaporeans. In fact, many older Singaporeans might even assert that they were raised to be frugal and financially independent.

Today, however, the FIRE movement has taken on a new name and gained worldwide momentum, particularly among younger Singaporeans who are embracing it with fresh enthusiasm.

The motivation behind the FIRE movement

It is no surprise to see the revival of the FIRE movement among younger Singaporeans. As work demands become increasingly heavy, more and more Singaporeans are experiencing job burnout. Meanwhile, rising living costs add to financial pressures, making it harder for many to stick to their retirement plans. For many, the FIRE movement offers a possible way out of the rat race and a chance to take control of their finances.

For over two decades, the continuous growth in the property market has enabled some Singaporeans to achieve their FIRE goals successfully through property investment. However, in recent months, increasing global economic uncertainty and a shifting world order threaten to undermine future property gains. Yet, when we look beyond the short-term volatility, strong fundamentals still indicate that real estate is a valuable vehicle to help you achieve your FIRE goals.

Let us explore these fundamentals while discussing the trade-offs that investors may need to consider in this evolving landscape when selecting an investment property aligned with the FIRE movement.

Singapore’s agile policymaking and the adaptability of its Masterplan enable us to navigate an increasingly uncertain economic environment.

Singapore’s recent leadership transition coincides with its master plan review, providing a timely opportunity to refresh its positioning as it navigates an increasingly uncertain economic environment.

Previous versions of the Masterplan were primarily designed to address immediate demands relevant at that time. However, many of these trends have since shifted significantly. Looking ahead, we are now facing different challenges, including sustainability concerns, rising costs, an ageing population, and evolving economic needs. All of these will shape Singapore’s future real estate landscape differently.

By remaining nimble and adaptable, Singapore can uphold its relevance on the global stage and continue attracting investors, thereby supporting long-term real estate growth. This also creates opportunities for investors to venture into real estate beyond the residential segment and into the commercial and industrial sectors.

Long-Term Population Growth along with a proactive strategy to Sustain Housing Demand

It may be unpopular to believe that Singapore’s declining birth rate will negatively impact its economic competitiveness in the long term. Therefore, from a policy perspective, it makes sense to embrace more foreign talent to support and grow our economy, an approach that will undoubtedly drive housing demand.

Some may argue that the influx of foreign workers will increase housing demand, potentially leading to higher property prices. However, let us take a step back and examine this possibility. In April 2023, the Additional Buyer’s Stamp Duty (ABSD) for foreign buyers was doubled from 30% to 60%, a move that almost immediately reduced housing demand among this group of buyers. Consequently, foreign workers in Singapore are often more inclined to rent rather than purchase property, as they typically view their stay as temporary.

That said, some eventually become permanent residents or naturalised citizens, opting to settle, establish their careers, and raise their families in Singapore. Regardless of whether they are renting or buying, they will still require housing.

1. Prioritise properties that have access to a steady and sustainable tenant pool.

With nearly 90% of housing owner-occupied, the availability of homes for rent remains limited, as evidenced by the persistently low vacancy rates across various market segments. Understanding how rental demand varies across these segments can provide you with an advantage when planning your next property purchase.

Chart 1: Vacancy Rate Across Market Segments

Source: URA, ERA Research and Market Intelligence

For instance, the Core Central Region (CCR) has long been regarded as a popular housing choice for foreign expatriates, thanks to its prime location in the heart of Singapore. It offers a short commute to key business districts and convenient access to popular shopping and lifestyle amenities. Given its higher concentration of investment properties, vacancy rates in the CCR tend to trend higher compared to the Rest of Central Region (RCR) and Outside Central Region (OCR).

Although traditionally driven by Singaporean owner-occupiers, we also observe rental demand in the RCR and OCR, albeit to a much lesser extent than in the CCR. This is because more expatriate families are adapting to and embracing the local Singaporean culture, particularly as Singapore continues to enhance its decentralisation efforts.

2. Stay invested for the long haul to achieve meaningful capital appreciation

When it comes to property investing, time in the market consistently outpaces short-term timing strategies. Based on median unlevered returns from property investments in Singapore, investors who retained their properties for 15 years or longer experienced their returns increase by over 50% compared to those who held on for less than 15 years. This underscores the importance of adopting a long-term investment horizon, where capital appreciation compounds steadily over time, navigating market cycles and short-term price fluctuations.

For investors aiming to achieve financial independence, this long-term approach to holding property helps build lasting wealth while managing market fluctuations.

Chart 2: Median Unlevered Returns Base on Holding Period

Source: URA (Jan-May 2025), ERA Research and Market Intelligence

3. Narrowing price gap between CCR and RCR could open up new price growth opportunities in CCR

The successive new home launches in the RCR and OCR since 2023 have supported price growth in these regions. In contrast, the CCR has experienced fewer new home launches during this time, leading to a slower rate of price growth.

In 1Q 2021 the CCR and RCR price gap was around 39%, but it has since narrowed significantly and is now almost on par.

While some may argue that the absence of new launches in the CCR is not a significant factor in the slower price growth, they might be overlooking an important point: home prices have largely been driven by new launches. With at least five new CCR projects scheduled for launch in 2H 2025, the CCR could experience renewed momentum in price growth.

Chart 3: Narrowing Price Gap between CCR and RCR

Source: URA, ERA Research and Market Intelligence

4. Masterplan 2025 may offer a glimpse into potential medium- to long-term growth locations

This month, more concrete plans under Master Plan 2025 will be unveiled, which could provide insights into potential growth locations. For instance, URA has already announced high-level plans for areas such as the Southern Waterfront and Kallang Alive, which are expected to spearhead housing demand in these locations.

Keeping a close watch on Masterplan changes can be rewarding, as early entry into emerging locations offers opportunities to ride on future market growth. For those looking to capitalise on tenant demand, identifying key business parks such as One-North and developments in regional centres may also prove advantageous as these locations gradually become more established and populated, with a workforce driving housing demand.

FIRE Is Still Achievable Through Real Estate, But You Will Need the Right Strategies and Skilful Planning

The road ahead is more challenging, but achieving FIRE is possible through calculated trade-offs. One key consideration is that the time required to achieve FIRE may be extended, as future project growth is likely to moderate. Buyers should remain open and selective, as not all developments will perform equally or provide the same growth potential. This is where working closely with a trusted salesperson can help curate a long-term, tailored plan to remain on track towards your FIRE goals.

Ultimately, although the journey toward FIRE may encounter new challenges, with adequate planning, flexibility, and professional guidance, real estate can still serve as a powerful means to build long-term financial independence.

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.

Punggol was developed over the two decades and is emerging as a choice location for many homeowners. In the next decade or so, we can almost visualise how Tengah will be evolving and mirroring the growth of the Punggol estate.

In 1996, the blueprint for Punggol 21 was unveiled to develop Punggol as a Waterfront Town of the 21st century. Today, it is a vibrant residential town home to an HDB resident population of 187,800, as well as the Punggol Digital District and the Singapore Institute of Technology. Tengah may undergo a similar transformation.

Both towns were developed off greenfield sites. Homes were built to support commercial and industrial hubs – Punggol Digital District and Jurong Innovation District for Punggol and Tengah respectively. Additionally, universities were located near these towns to foster stronger industrial-academia collaborations between these nodes. Furthermore, both towns have reliable public transport nodes within their towns, with the Punggol LRT and the Jurong Region Line serving residents.

One difference is that Punggol is located in the North-East Region, while Tengah is in the West Region. Following the announcement of the development of Tengah, could we potentially see Tengah mirroring the growth of Punggol?

This piece will talk about what Tengah currently offers and future plans for this new forest town.

Tengah – the 24th and latest HDB town

Tengah is located within the West Region of Singapore. It is bordered by Bukit Batok to the east, Chua Chu Kang and Bukit Panjang to the north-east, Western Water Catchment to the north and west, and Jurong East and Jurong West to the south.

Image 1: Developed New Township of Tengah

Source: ERA Research and Market Intelligence

HDB first announced the development of Tengah town in 2016. Billed as a “forest town”, the estate will span nearly 700 hectares. It is similar to the size of Bishan and will house nearly 42,000 new homes when fully developed. Homes in Tengah will be located across five districts, each with their own unique character.

What sets Tengah apart is that it will be the first sustainable housing town in Singapore. The estate is set to boost smart technologies and eco-friendly features, driving Singapore’s commitment to meet our sustainability targets.

The Tengah town centre, which will be known as The Market Place, will be within the Park District. It will be Singapore’s first “car-free” Town Centre where the roads will run beneath the Town Centre, freeing up space at the ground level for shopping and recreational uses. As such, walking and cycling are the encouraged modes of transport within the estate. Tengah MRT Station on the future Jurong Region Line (JRL) will be located there. Other features include the Central Park, Rainforest Walk and a plethora of retail and dining services.

Image 2: Map of Districts in Tengah

Source: Google Maps, ERA Research and Market Intelligence

Amenities and Connectivity

The completion of the first 10,000 HDB flats in Tengah in 2023 marked a major milestone for the new town, drawing in its first wave of residents. However, early hurdles quickly emerged with residents facing a lack of amenities and transport options.

Since then, Tengah’s first Neighbourhood Centre, Plantation Plaza, has been completed. Located within Plantation District, which will have 10,000 new homes when fully completed, it will serve the daily needs of residents. It houses a wide variety of dining, retail, healthcare and recreational services.

Image 3: Plantation Plaza Shopping Mall in Tengah

Source: HDB

As the residential population in Tengah is still relatively small, there are currently only a few schools in the area. However, it was announced by the MOE that new schools will be set up in newer estates such as Tengah and Punggol. Schools within Tengah includes Pioneer Primary School, Anglo-Chinese School (Primary), and Bukit View Primary School.

With Tengah planned as a car-lite town, more transport nodes have been planned in comparison to other towns. There will be four MRT stations on the upcoming Jurong Region Line (JRL). These stations are slated to start operations in phases between 2027 and 2028. Additionally, the Brickland District will be served by Brickland MRT Station (NS3A) on the North South line. The station is aimed to be completed by 2034.

In terms of bus connectivity, Tengah currently has a bus interchange with 5 services connecting commuters to parts of Jurong and Bukit Batok. By the end of 2025, it was announced that there would be two new bus services introduced, and six more by 2026. Most bus stops in Tengah will be within 300 metres of residential estates.

Image 4: Map of stations on Jurong Region Line serving Tengah

Source: HDB, ERA Research and Market Intelligence

With these MRT stations, residents would be three stations away from Jurong East MRT and Chua Chu Kang MRT, which serves the East West and North South Lines respectively, enhancing connectivity throughout the island.

Jurong Innovation District

The Jurong Innovation District (JID) is a 620-hectare industrial district is home to advanced manufacturing, supporting an ecosystem of manufacturers, technology providers, researchers and education institutions with Nanyang Technological University nearby. It is located around 14 minutes away from Tengah by car. When the Jurong Region Line is completed, connectivity between the places will be improved with the JID being served by Corporation Station (JS5) on the line. It will be one stop away from Hong Kah MRT station.

Image 6: Artist Impression of the future Jurong Innovation District

Source: JTC, ERA Research and Market Intelligence

When completed, the JID is expected to introduce about 95,000 new jobs in advanced manufacturing, innovation and research. Individuals working in this district or industry could look at housing in Tengah, as it is a short distance away from JID, as well as the Jurong Lake District, which contributes 100,000 more jobs. Furthermore, housing in Tengah is likely to be affordable to attract more Singaporeans to the new town.

According to the URA Master Plan, Tengah has several plots of land zoned for commercial use, including a recent GLS site which is zoned for commercial and residential use. This could further boost the number of jobs available within this district.

What’s next for Tengah

Currently, there are no new private condominium developments in Tengah planning area. As of June 2025, there have been four EC launches and 22,521 HDB units launched across 20 BTO estates in Tengah. Six BTO estates are yet to be completed with the latest slated to be completed by 2Q 2027.

Table 2: Details of Projects in and around Tengah

Source: URA as of 1 July 2025, ERA Research and Market Intelligence

The first private condominium GLS site was awarded in January 2025 along Tengah Garden Avenue. The site was tendered at $821 per square foot per plot ratio (psf ppr) and can yield around 800 units. It is located conveniently next to the future Hong Kah MRT station. It is expected to launch in 2026 and be completed by 2030.

In Closing

Tengah reflects many similarities to the early days of Punggol. They were both developed from the ground up, supported by strong intra-connectivity, and developed near innovation hubs. However, Tengah has some elements of uniqueness, having a strong focus on sustainability, smart living, as well as being home to Singapore’s first car free town centre.

One key difference between both towns – Tengah’s flats have a height restriction due to its proximity to Tengah Air Base. While Tengah may not replicate Punggol’s scale or waterfront appeal, it is positioned to achieve similar or greater success in terms of liveability, sustainability, and job opportunities. With a strong emphasis on sustainability in its planning, as well as being strategically located to the future Jurong Innovation Hub which will provide jobs, it has a strong foundation set for long term growth.

Are you interested to live in an up-and-coming estate that will see major transformations in the years to come? If so, Tengah is a place that you can call home. There is another upcoming EC launch in 2025. Interested to know more? Speak to any ERA Trusted Advisor today to find out more!

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.

The first half of 2025 (1H 2025) carried buying momentum from end-2024, when six projects were successfully launched in November 2024. In these six months, there were ten private developments, and one Executive Condominium (EC) launched across these six months.

Based on URA’s developer sale data as of 16 June 2025, developers have sold 4,384 units in the first five months of 2025.

Chart 1: Units launched and sold excluding ECs

Source: URA as of 16 June 2025 (based on monthly Developer Sales data), ERA Research and Market Intelligence

2H 2025 is set to see another 14 new private launches, adding 6,732 units into the market. In addition, one more EC could be launched with 600 units collectively. Located across various estates in Singapore, these launches will cater to a diverse range of buyer profiles, depending on their needs, lifestyles, and preferred locations.

This article serves as an overview of what launches that are expected to hit the primary market in the coming months. An overview of each project will be provided in their respective sections below.

Centrally Located Homes Making a Comeback

Since 2022, there were just three developments with at least 100 units launched in the Core Central Region (CCR). However, with more CCR sites awarded via the Government Land Sale (GLS) in 2024, we will in turn see more of such launches in 2025. This could meet the pent-up demand for properties within the various prime locations.

Luxury homes

W Residences – Marina View (683 units)

Branded residences are luxury residential properties that are developed in collaboration with well-known brands. They combine private homeownership with high-end brand services, design, and prestige. Apart from the high-quality product with high-quality finishings, they are professionally managed and comes with services such as a 24-hour concierge and housekeeping. W Residences – Marina View will be only the fifth branded residences in Singapore, and the first in the city centre. Located within the Central Business District (CBD), just 100m away from Shenton Way MRT Station, there are ample amenities and commercial services around.

UPPERHOUSE at Orchard Boulevard (301 units)

Linked to Orchard Boulevard MRT Station, UPPERHOUSE at Orchard Boulevard is both well-connected and exclusive, nestled between Good Class Bungalow (GCB) areas with some of the most prestigious addresses in Singapore. Moreover, both the Orchard Road Shopping Belt and the world-renowned Botanic Gardens are one MRT stop away.

The Robertson Opus (348 units)

If you’re seeking a waterfront home in the city centre that also offers proximity to nature, The Robertson Opus could be a compelling option. Being in the heart of Robertson Quay, there are a plethora of amenities, dining and retail options. A 10-minute walk will take you to Clarke Quay, a vibrant hub for entertainment and nightlife. The upcoming Canninghill Mall, New Bahru, and a charming row of shophouses in River Valley filled with bars, eateries, and cafés are also in its immediate vicinity.

Moreover, the 999-year leasehold tenure allows the project to double as a legacy asset.

Skye At Holland (666 units)

Skye at Holland is sited along Holland Road, one of Singapore’s most coveted addresses. Located in District 10 and surrounded by GCB Areas, homeowners will enjoy a prestigious and tranquil living environment.

Despite the exclusivity, it is just a few minutes’ walk from Holland Village MRT and the bustling Holland Village lifestyle enclave. Residents enjoy easy access to a wide array of dining, retail, and entertainment options, including the vibrant mall at One Holland Village.

It is also surrounded by prestigious schools such being within 2km to Henry Park Primary School, New Town Primary School, Nanyang Primary School, Queensway Secondary School, Fairfield Methodist School (Primary and Secondary), Anglo-Chinese School (Independent), Anglo-Chinese Junior College, Tanglin Trust School, and the Singapore Polytechnic.

New housing cluster in the Central location

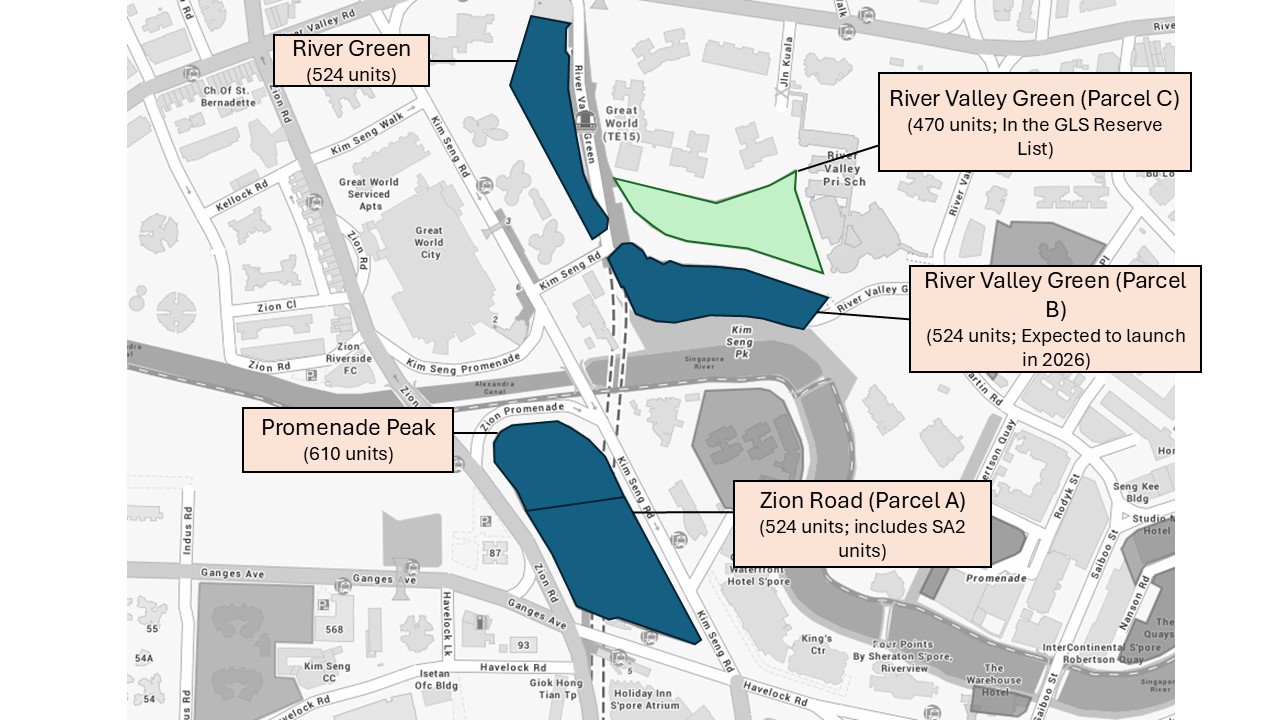

A new housing cluster is being developed in the River Valley Green/Zion Road precinct. Four of five Government Land Sales (GLS) sites have been sold. Three of these sites are expected to be launched in 2H 2025. Both Zion Road sites are located between Great World and Havelock MRT Stations, while the River Valley Green sites are beside Great World MRT Station.

The Zion Road (Parcel A) site is expected to yield a total of 1,170 housing units, although 435 units will be long-stay serviced apartments (SA2). These units are part of a new pilot, which requires a minimum 3-month stay. This development is located right next to Havelock MRT Station.

Map of the River Valley/Zion Road Cluster

Source: URA, ERA Research and Market Intelligence

Suburban Condos to cater to HDB upgraders’ demand

There are three new upcoming suburban condominiums set to be launched. They are all in locations without launches in recent years. As a result, we could see pent-up demand for homes there.

Canberra Crescent Residences (376 units)

Canberra is a new housing estate in the North, sited between Sembawang and Yishun. Despite being a young estate, it has ample amenities. Located just a 10-minute walk from Canberra MRT Station and Canberra Plaza, residents of Canberra Crescent Residences will enjoy convenience, while being close to nature (Sembawang Park and Simpang Kiri Park Connector).

This site was awarded for just $793 per square foot per plot ratio (psf ppr) in July 2024. This was the lowest land rate recorded for private development since November 2020. In comparison, an EC site at Tampines St 95 was awarded for $768 psf ppr, just 3.3% lower.

Springleaf Residence (941 units)

Springleaf Residence could be amongst the biggest launch in 2Q 2025. Located within a 5-minute walk from Springleaf MRT Station, it will be the first development in this new housing estate. Currently, there are no high-rise developments in the estate, with with only landed homes there. Just one MRT stop from the Lentor Hills Estate, which has seen strong interest among homebuyers, there could be spillover demand to this development. Being a mega-development, we can expect higher interest as buyers have more options in terms of sizes, layouts and unit mix.

The Sen (347 units)

Located along De Souza Avenue, The Sen lies within the more serene and tranquil side of Upper Bukit Timah. Surrounded by landed homes and three nature parks – the Rail Corridor, Bukit Batok Nature Park and Bukit Timah Nature Reserve, it provides residents with a getaway from the crowd.

It is also short bus rides away from Hume and Beauty World MRT Stations, where the latter is also where the integrated transport hub and several malls and eateries are located.

City fringe properties remain a popular choice

Living in the Rest of Central Region (RCR) remains a popular choice for many homebuyers. It provides the convenience of being near the city centre, while being away from the hustle-and-bustle to enjoy a quieter environment. With plenty of amenities and strong connectivity, residents enjoy the best of both worlds. In the coming months, three upcoming launches in the RCR may capture the attention of prospective buyers.

Lyndenwoods (343 units)

Lyndenwoods is the first and only development within Singapore Science Park. Beyond just a conventional business park, Science Park is a work-live-play estate with amenities already in place.

It will feature direct access to Kent Ridge MRT station via a fully sheltered passageway that will provide convenience. In the same vein, the ample retail options and natural spaces surrounding the development will also contribute to its liveability for both tenants and homeowners.

Margaret Drive GLS (460 units)

Queenstown is a mature HDB estate with established amenities. The popularity can be seen from the number of HDB flats that have crossed the million-dollar mark. In the first six months in 2025, there were 76 million-dollar flats transacted.

The Margaret Drive site is within a 10-minute walk to Queenstown MRT Station, Margaret Drive Hawker Centre and Dawson Place. There are also several primary and secondary schools around the site.

Artisan 8 (42 units)

Artisan 8 is a freehold boutique development located just 280m from Upper Thomson MRT Station. It offers exclusivity as it has just 34 residential units. Being part of a mixed-use development where retail shops, eateries and a supermarket below, residents can enjoy unmatched convenience. Otherwise, Thomson Plaza is also an 11-minute walk away. Families with school-going children will also like that it is within 1-km of Ai Tong Primary School and Catholic High School.

One of the few freehold launches in 2025, the scarce supply will make this appealing to those seeking a legacy asset.

Executive Condominiums Poised to See Stellar Performance

ECs continue to allure buyers which presents a strong value proposition despite higher prices. Aurelle of Tampines, the latest EC launch in 2025, has set a new benchmark price. It sold at a median of $1,767 psf. However, ECs still provide a lower price option compared to new private homes, while offering the same lifestyle. Hence, ECs are a property class that HDB owners typically look towards when planning to upgrade.

However, there is a lack of available new EC units available today. As of 1 July 2025, there are only 4 unsold units island wide. With the strong buyers’ interest, we are likely to see new home stocks continue to deplete. The only remaining EC launch in 2025 will be Otto Place in Tengah, which is anticipated to preview in July 2025.

Otto Place (600 units)

Tengah, being a new estate, saw strong interest among younger families, which provides a large pool of HDB upgraders. As seen in the adjacent Novo Place, which sold 57% of units at an average price of $1,510 psf in November 2024, a new EC benchmark price then, we could see similar interest especially with a short supply of units. Otto Place sits just beside Novo Place and is developed by the same developer – a joint venture between Hoi Hup and Sunway Developments.

List of upcoming new launches in 2H 2025

With a total of 15 exciting new launches coming up in the next few months, buyers still waiting on the sidelines will have something to think about. Having choice fatigue with so many options? Or can’t decide which property matches your needs? For a more in-depth analysis to help you choose the right project for your needs, speak to an ERA Trusted Advisor today.

Table 1: Upcoming new project launches for 2H 2025

Source: ERA Project Marketing

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.

Co-written By Egan Mah & Stanley Lim

It’s the classic narrative of Singapore’s housing landscape: dating, getting married, and then moving into a newly completed Build-to-Order (BTO) flat as newlyweds. However, this familiar route isn’t always accessible to everyone, whether by personal choice or due to circumstances beyond their control.

Thankfully, for those who are unable to enjoy shared ownership of a property with a spouse, there are still avenues to enter Singapore’s property market with a trusted someone – be they a live-in partner, close friend, or family member. This guide will explore the various housing options, eligibility criteria, and key considerations for co-owning a Singapore property even when legal marriage isn’t on the cards.

Why is property co-ownership outside of marriage a consideration for some Singaporeans?

There are numerous reasons why some Singaporeans might opt to co-own a residential property outside of marriage.

While some aspiring homeowners may choose to do so due to practical concerns, such as financial constraints or caregiving responsibilities towards a disabled and/or elderly family member, others may be motivated by personal circumstances. Moreover, not all aspiring homeowners fall within the conventional definitions of family or marital status; yet they too are also seeking pathways to co-ownership.

For instance, a widower who has found love again may choose not to remarry to avoid the hurdles of legal marriage. Accordingly, they might choose to co-own a property with their new partner, which would enable them to build a shared home, sans the bureaucracy and formalities.

From a purely financial perspective, there is also a compelling case for co-ownership outside of marriage, given the robustness of Singapore’s property market. Property has long been regarded as a reliable investment asset locally, owing to its history of consistent appreciation. Between 2021 and 2025 alone, HDB flats and private homes have experienced significant upward momentum, as evidenced by the sharp 41.3% (142.2 to 200.9) and 30.1% (162.2 to 211.1) increases in their respective price indices.

Chart 1: HDB resale price index (RPI) and private residential property price index (PPI) from 1Q 2021 to 1Q 2025

Source: URA, HDB, ERA Research and Market Intelligence

In this light, property co-ownership transcends merely fulfilling housing needs; it also represents a strategic decision for long-term financial security. This is especially relevant for those who may not have children of their own and/or lack familial support in later stages of life.

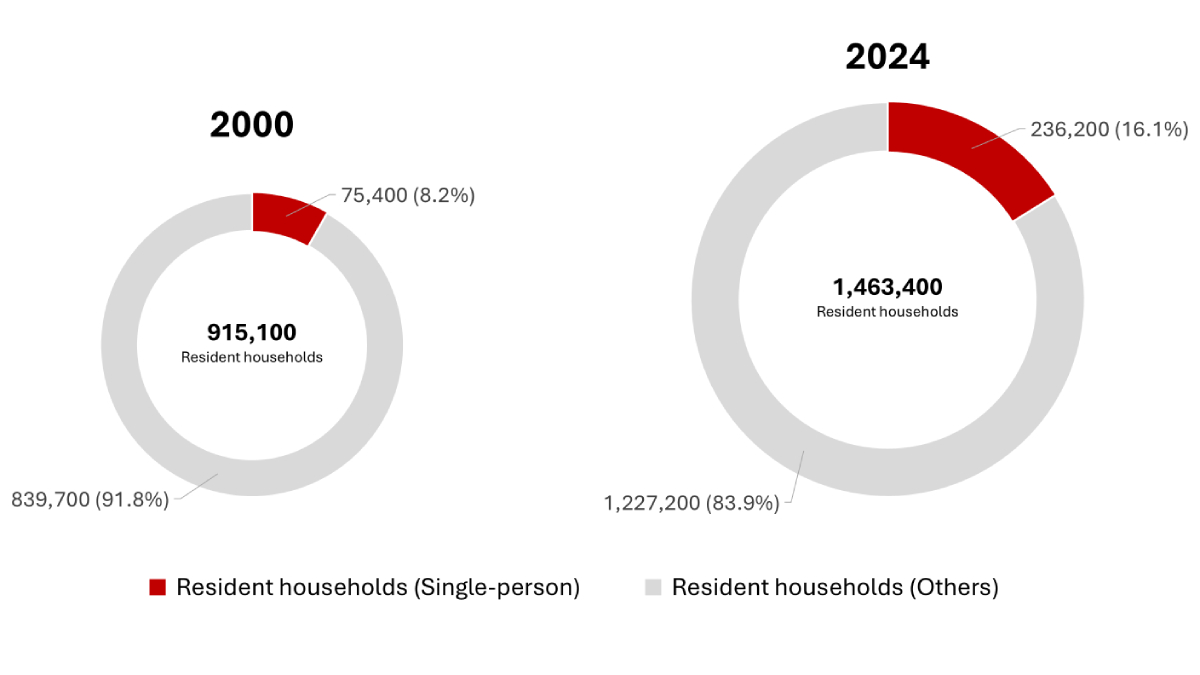

However, given the increasing proportion of singles in Singapore’s resident population, personal choice and/or a desire for freedom are likely the main factors influencing interest in alternative paths to homeownership, including co-ownership arrangements.

Chart 2: Growth in single-person households as a proportion of total resident households (2000 – 2024)

Source: SingStat, ERA Research and Market Intelligence

These beliefs tie in with a greater preference for single living as well, especially among Singaporeans seeking flexibility and privacy. Based on official SingStat figures, the number of single-person resident households has risen by over 200% from 75,400 in 2020 to 236,200 in 2024. Likewise, the share of single-person resident households has also seen a notable increase, doubling from 8.2% in 2000 (75,400 of 915,100 households) to 16.1% in 2024 (236,200 of 1,463,400 households).

Therefore, given the increasing prevalence of singlehood among Singaporeans, it is reasonable to suggest that there may indeed be a growing need to reimagine local homeownership beyond the traditional couple-centric model.

The Singapore Government has taken steps in this direction, with the most recent change being the expansion of public housing options for singles. A key policy revision in the second half of 2024 now allows singles – or, for co-ownership purposes, groups of up to four singles – to purchase 2-room Flexi HDB flats in any housing estate, including prime locations.

However, different homeownership requirements and considerations will apply depending on whether one is considering co-owning an HDB flat, an executive condominium (EC), or private housing.

What are the laws, rules and considerations for co-owning different residential properties for joint-singles?

Buying an HDB flat will require all parties to be at least 35 years old.

While HDB offers numerous eligibility schemes to support various demographic groups in their housing journey, single buyers interested in co-owning a flat need only focus on one: the Joint Singles Scheme.

Introduced in 1990, the Joint Singles Scheme allows eligible Singaporean men and women at least 35 years old to jointly purchase an HDB flat or Executive Condominium (EC). However, those who are widowed or orphaned may qualify from the age of 21, but only for resale Prime flats, unclassified resale flats, and new Standard and Plus flats.

For the purposes of this piece, we consider joint single households to be living arrangements involving two to four unmarried individuals of any gender. Additionally, if you intend to apply under the Joint Singles Scheme, it is important to take note of the following requirements:

Table 1: Joint singles eligibility criteria for HDB and EC flat purchases

Source: HDB, ERA Research and Market Intelligence

*Unclassified resale flats refer to HDB homes sold before the October 2024 sales exercise that do not fall under either Standard, Plus, or Prime classification categories.

Private home ownership is less cumbersome.

Unlike HDB flats or Executive Condominiums, purchasing private property as co-owners is not subject to specific eligibility criteria. However, co-buyers must consider the manner of holding or, more simply, how ownership is legally shared. This is particularly important for inheritance, as the selected holding method determines how the property is passed on after a co-owner’s death.

What are the different manners of holding or ownership types, and how do they matter in inheritance planning?

So, there are two property ownership types in Singapore, namely holding the property in Joint Tenancy and Tenancy-in-common. For HDBs, applicants under the Joint Singles Scheme must be registered as co-owners (i.e. the owner-occupier structure is not allowed).

While joint tenancy is the default holding method for HDB flats, buyers can opt for tenancy-in-common. However, this may come with higher legal fees due to the higher complexity of arrangements and the potential for disagreements.

- Joint Tenancy

Under a joint tenancy structure, there is an undivided interest in the property. All owners are regarded as owning the entire property collectively, with no separate or distinct shares. When one owner passes away, the rights of survivorship come into effect. This means that the surviving owner automatically inherits the rights to the full share of the property, irrespective of any existing will.

This is with the exception of when both parties pass away at the same time. In such cases, the order of death becomes legally significant. However, when it is impossible to determine (e.g., simultaneous death in an accident), Singapore law presumes that the younger person passes away later. Hence, the younger party will inherit the entire property before passing it on to their next of kin or will beneficiaries.

For example, Jamie and Ashley are both unmarried 35-year-old singles with no family, who decide to buy an HDB flat together under a joint tenancy arrangement. If Jamie passes away, Ashley will inherit full ownership of the flat.

Below, we have summarised the characteristics of both manners of holding:

Table 2: Summary of manner of holding of property

Source: ERA Research and Market Intelligence

- Tenancy-in-Common

Under the tenancy-in-common structure, owners can agree on their respective ownership percentages, provided they total 100%. For instance, if one party pays for 70% of the property and the other covers 30%, they hold a 70-30% share. These shares are detailed in the title deed. Upon death, each owner’s share will pass to their respective estate rather than to the surviving owner.

If all owners pass away simultaneously, each owner’s share will be allocated to their respective beneficiaries under their wills or according to the Intestate Succession Act if no will exists. The assets will be divided in accordance with the act.

Table 3: Common beneficiaries under the Intestate Succession Act*

Source: Singapore Statutes online (sso.agc.gov.sg)

* The Intestate Succession Act does not apply to Muslims. The estate of a Muslim is governed by Muslim law. ** ‘Issue’ is a legal term referring to one’s direct descendants.

The Tenancy-in-Common ownership structure would be ideal for two parties who have their own estates to pass on the property to, such as divorcees or widows with children, coming together to jointly purchase a property.

For instance, Lewis and Jesse own 70% and 30% of a condominium unit, respectively. If Jesse were to pass away, his share (70%) would go to his estate according to his will, while Lewis would continue owning 30% of the property.

Beyond legalities, what else should you consider before co-owning a residential property?

For many, the legal, emotional, and financial advantages of co-owning a property outside of marriage are very real. Still, it is equally important to recognise the responsibilities and risks that come with it.

Firstly, just as in marriages, breakdowns in relationships between co-owners can make living together challenging. However, unlike most relationships, where it is possible to walk away from the other party, you will be tied to the shared property unless both parties reach a consensus on future ownership.

The same goes for scenarios where financial difficulty is a concern. If one party is unable to cover their share of costs (e.g., mortgage, maintenance fees), the financial pressure may unfairly fall on the rest.

Lastly, inheritance disputes could arise even if a manner of holding or inheritance has been specified. For instance, in an emotionally charged situation, family members of a deceased co-owner may still choose to contest a will despite its legal standing.

For these reasons and more, all parties involved should establish a shared understanding and make definitive arrangements on how ownership should be handled in good times and in bad, before proceeding with a purchase.

Beyond formalising the manner of holding, prudent buyers may also consider drafting a will to facilitate smooth and unambiguous future transfers, particularly when a joint tenancy is involved. Likewise, a consultation with legal and real estate professionals is recommended for more precise understanding and informed guidance. Because just as with the people you love, those you share a roof with deserve nothing less than care and clarity.

Disclaimer

This information is provided solely on a goodwill basis. It does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For the avoidance of doubt, ERA Realty Network and its salesperson accept no responsibility for the accuracy, reliability and/or completeness of the information provided. ERA owns the copyright in this publication, and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.

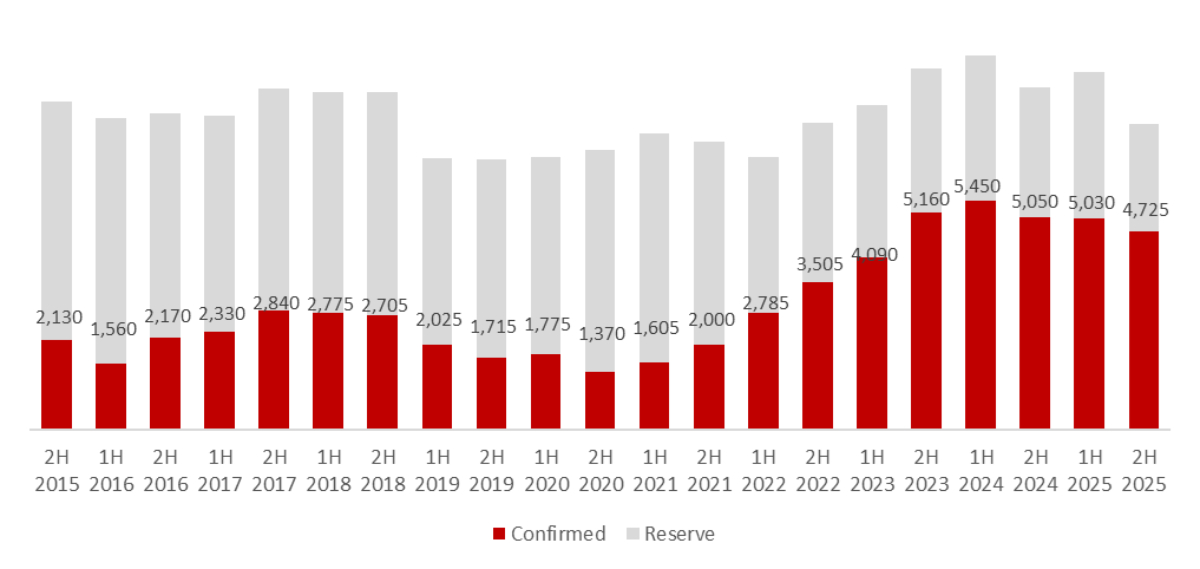

The 2H 2025 Government Land Sales (GLS) program introduced 4,725 private residential units in the Confirmed List. This brings our total annual Confirmed List supply close to 10,000 units. A total of ten sites were placed on the Confirmed List, comprising five private residential sites, three Commercial and Residential sites, and two EC sites.

Collectively, the 2H 2025 GLS Confirmed List totals an estimated 4,725 private homes, which encompass 990 Executive Condominium (EC) units, while the Reserve List will yield an additional 2,460 residential units. Overall, the private home supply (on the Confirmed List) slated for 2H 2025 fell by 6.7% compared to 1H 2025.

“The continued release of private housing supply aims to moderate recent bullish land bids in selected locations that have seen overwhelming interest. The release of sites, such as Dunearn Road and Woodlands Drive 17 (EC) could ease competition for nearby sites and potentially moderate land bids.”

Chart 1: Residential GLS Sites (No. of Units)

Source: URA, ERA Research and Market Intelligence

Where are the promising sites?

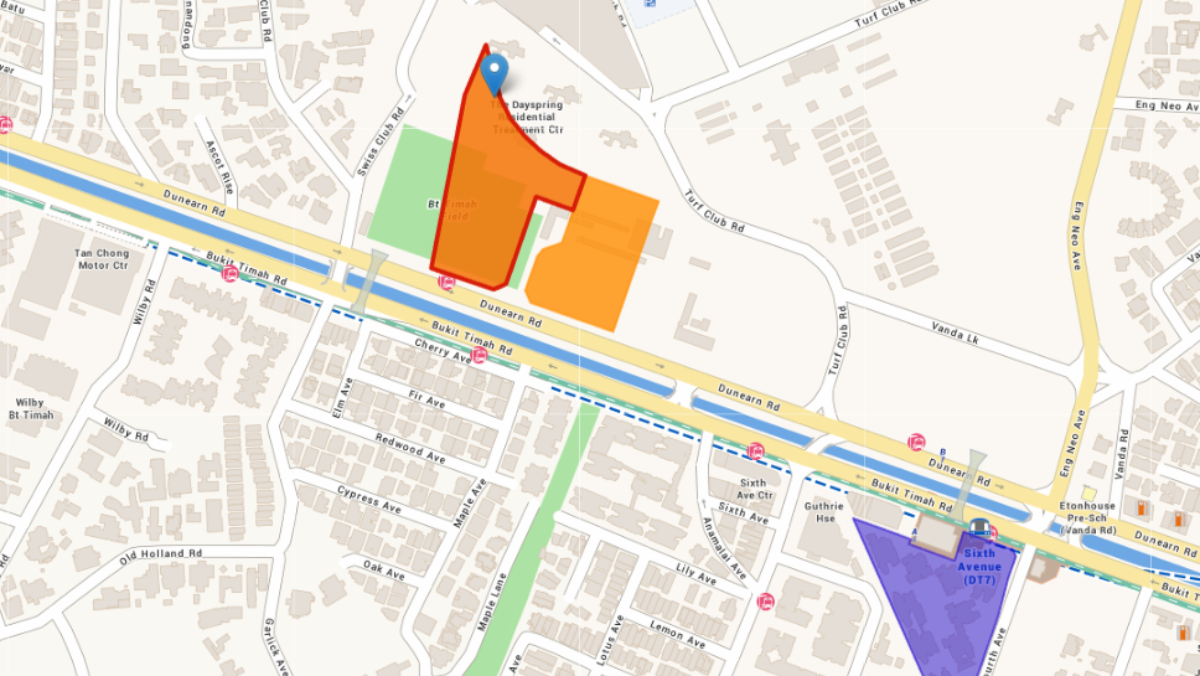

The Dunearn Road site will be the second private residential development launched following the announcement of Bukit Timah Turf City’s redevelopment plans earlier this year. The private residential site is nestled among the first upcoming HDB flats in Bukit Timah, and we expect the future residents to benefit from ample amenities as the area undergoes transformation. Demand for this site will be interesting to watched based off the performance of the prior Dunearn Road site that will close in late June.

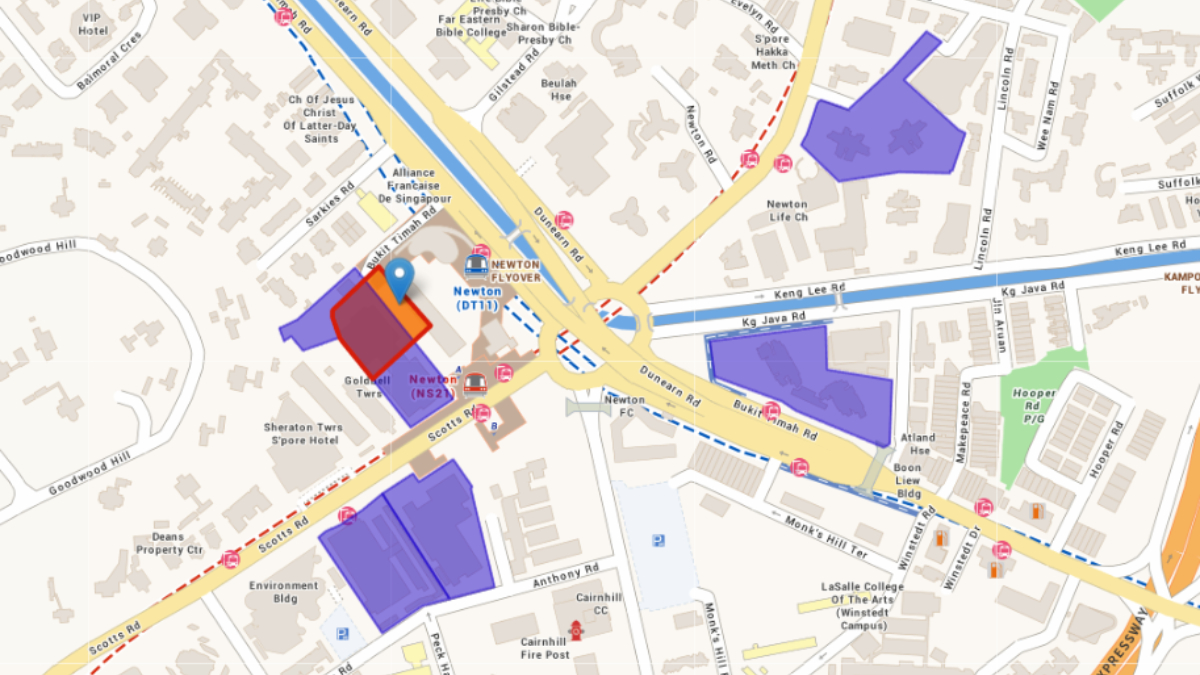

The other CCR site in Newton at Bukit Timah Road will also draw in developer’s interest due to its strong location adjacent to Newton MRT interchange. The location will draw in both owner occupiers and investment buyers, due to its unique central location located not only near offices and the CBD, but also family friendly amenities and a good nearby primary school in ACS Junior.

Among the sites unveiled in the 2H 2025 GLS slate, Dover Road stands out with the highest estimated residential yield of approximately 625 units, along with a commercial component of 3,000 sqm, which will introduce crucial amenities for residents. The site is suited likely for owner-occupiers and working families as its location offers better access to one-north MRT station and a cluster of well-regarded schools. These include Anglo Chinese Junior College and Fairfield Methodist School (Primary and Secondary).

Lastly, the two EC sites at Woodlands Drive 17 and Miltonia Close will also be on the radar for developers. There has been a large influx of EC supply in the North, and developers will have to balance and consider their strategy when it comes to choosing the right site for development.

Bukit Timah Road – 340 units

Source: URA

This site is located adjacent to Newton MRT, which is a key stop for commuters travelling to and from the North-South and Downtown lines.

This CCR site boasts a medium to large size of 340 units and could see demand from both owner occupiers and investment buyers, due to its proximity to the city centre, and for those working in the finance sector, which hold offices in the Newton/Buki Timah Road area.

The site will be within the 1km priority enrolment distance from Anglo Chinese School (Junior), which is a definite plus for owner-occupier families. Amenities located close by are dense, with immediate dining options at Newton food centre, and access to multiple shopping malls in Novena, and Orchard just one stop away respectively.

Developers may show a warm interest in this prime Bukit Timah Road site, given limited competition due to the scarcity of new private home supply in the immediate vicinity. However, interest in the site could be moderated by its prime CCR location, and larger project size, which could spell higher risk than the other sites on this Confirmed List.

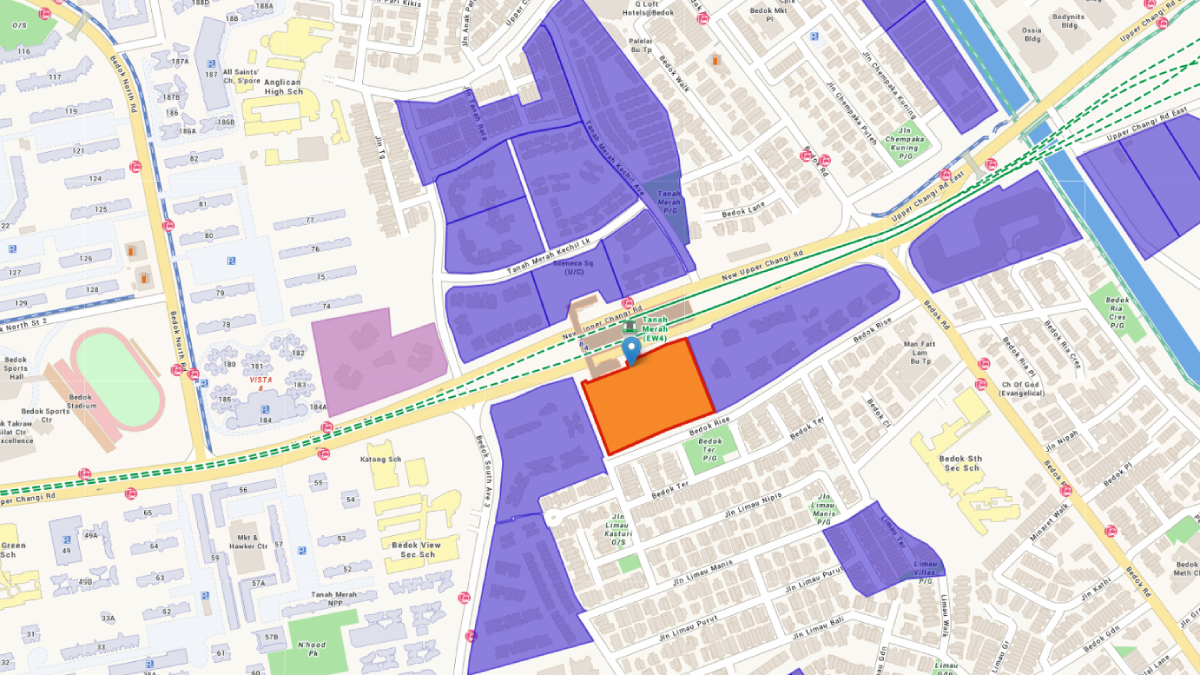

Bedok Rise – 380 units

Source: URA

Bedok Rise, located just beside Tanah Merah MRT Station, is largely a private residential estate surrounded by condominiums and landed homes. It provides strong connectivity, being an interchange on the East-West Line and towards Changi Airport.

There is a shortage of new homes in Bedok, the last major launch was in January 2023, when Sceneca Residence made its debut. It has since sold 98.1% of its 268 units. Demand for homes in Bedok has been high, with the latest site at Bayshore Road setting a new record price psf for an OCR site when awarded for $1,420 psf ppr in March 2025.

The new mall at Sceneca Residence located across the street provides amenities while there are several schools in its vicinity, including Temasek Primary School, Bedok View Secondary School, Bedok South Secondary School and the Singapore University of Technology and Design (SUTD). There are also several commercial and industrial nodes such as Changi Business Park, Changi Airport and the future Changi East Urban District close by. Therefore, developers’ keen interest is expected for this site.

Woodlands Drive 17 (EC) – 560 units

Source: URA

Among the two EC sites announced in this round’s GLS programme, this Woodlands Drive 17 site stands out as the premier option for upgraders in the North region. The location and name of this site might ring a bell, as a nearby EC site along the same road was launched for tender in 1H 2025.

Traditionally, ECs are located in less-prime areas relative to private developments, making them a more budget-friendly option in exchange for further distances from key amenities. However, this site will be located a walk away from Woodlands South MRT station, which enhances its connectivity to other locations on the Thomson-East Coast Line. Residents can also enjoy dining options at Woodlands Health Campus just next door.

The popularity of this site will largely depend on the bids received for the closing of the earlier Woodlands Drive EC, which would take place in August. Developers could wait for the results of the bidding process to plan or adjust their bidding strategy respectively. Additionally, this is the 4th EC site launched in the North region in the same year, which could further pace the demand. However, despite all this, we should definitely see a fairly competitive bidding process for this site, as EC sites generally offer lower risk for developers.

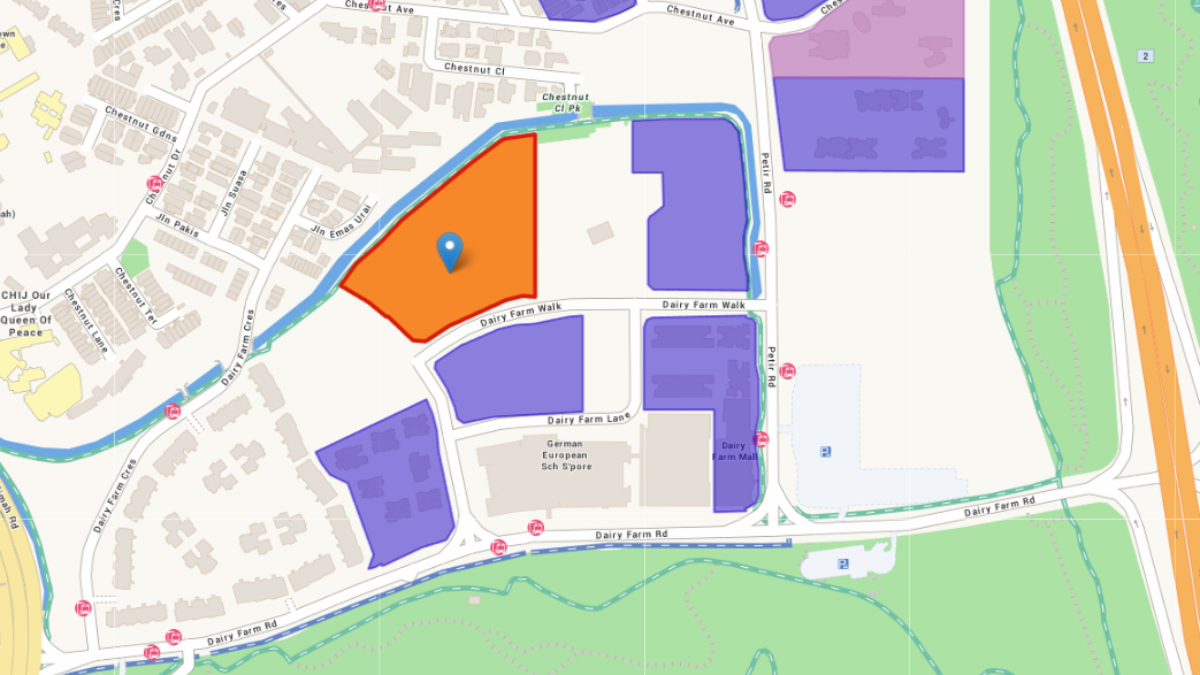

Dairy Farm Walk – 500 units

Source: URA

Located near Hillview MRT station, Dairy Farm has been transformed to become a new housing cluster. Amenities there include HillV2 and Dairy Farm Mall, with the Rail Mall being slightly further away.

Presently, there are eight private developments surrounding the MRT station. The last site, also along Dairy Farm Walk, was awarded in January 2025 for $1,020 psf ppr. It had drawn two bidders and when completed, it can yield up to 540 units. This would mean competition for buyers, with more than 1,000 units available.

It is unlikely for developers to be competing strongly for this site.

Dunearn Road – 370 units

Source: URA

The Dunearn Road is the second site to be announced in the vicinity, following the debut of a previous site in the 1H 2025 Confirmed List. The tender for the earlier site will close in late-June this year, and developers could take cue from the results in their bids for this plot.

Demand for this site will be fuelled mainly by the Turf City transformation. This could encourage older residents from nearby landed estates to consider this as a right-sizing opportunity. The site is also close to Sixth Avenue MRT station.

Dover Road – 625 units

Source: URA

Among the sites unveiled in the 2H 2025 GLS slate, Dover Road stands out with the highest estimated residential yield of approximately 625 units, along with a commercial component of 3,000 sqm. The site is also situated closely to the one-north innovation district, much like recent GLS sites, such as Media Circle (Parcels A and B).

However, Dover Road is more likely to appeal to aspiring owner-occupiers and working families as its location offers better access to one-north MRT station and a cluster of well-regarded schools. These include Anglo Chinese Junior College and Fairfield Methodist School (Primar and Secondary).

The site also carries historical value as it sits on the former Dover HDB estate which consisted of Blocks 30-39. This marks the maiden residential development on the plot since its demolition in 2018 – 2019.

Tanjong Rhu Road – 525 units

Source: URA

This is the first residential GLS plot to be released along Tanjong Rhu Road in nearly three decades since 1997, making it a rare opportunity for developers seeking to cater to sustained upgrader demand in the city-fringe locale.

Its attractiveness is further enhanced by its proximity to key infrastructure and amenities. These include Tanjong Rhu MRT station on the Thomson-East Coast Line, offering seamless access to the CBD, and the nearby Singapore Sports Hub, which is part of the Kallang Alive master plan that is transforming the precinct into a major sports and lifestyle destination.

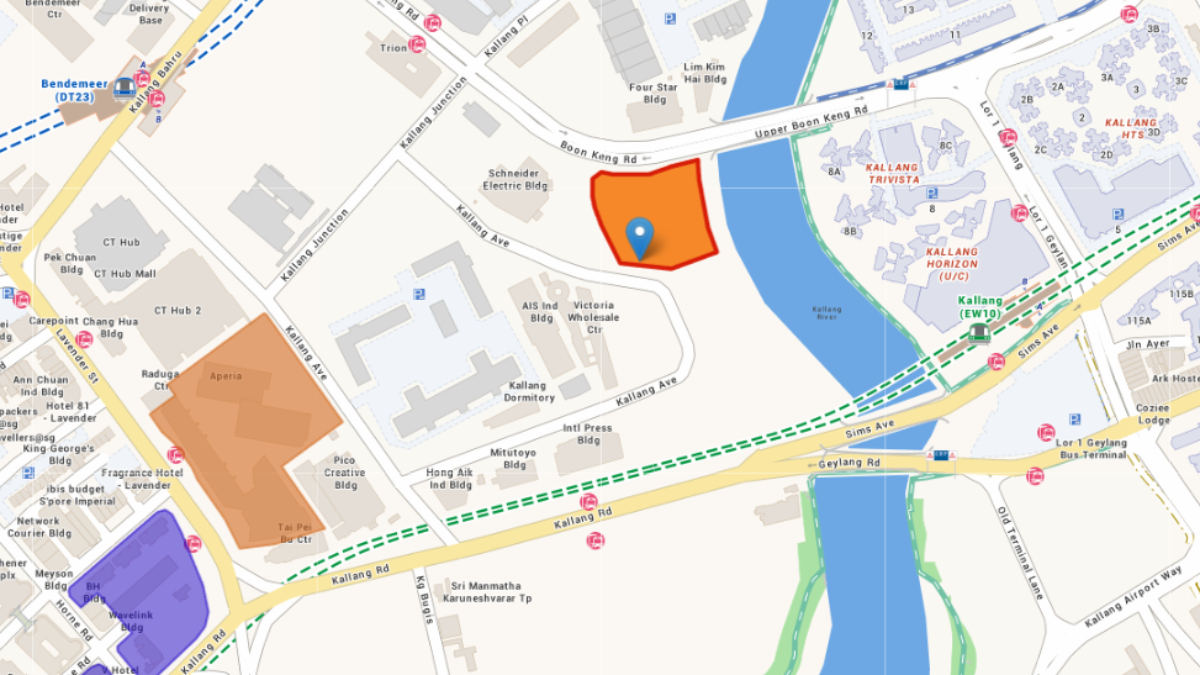

Kallang Avenue – 450 units

Source: URA

The Kallang Avenue site is within a 10-minute walk to both Kallang and Bendemeer MRT Stations. Some units will have unblocked waterfront views, overlooking Kallang River. There will also be a small commercial section within the development, that will provide amenities for residents.

Located between Kallang Avenue and Boon Keng Road, this site would be a potential site for HDB upgraders. The newer HDB estates have yielded several million-dollar flat in the past few years.

Despite being located within an industrial estate, developers are likely to be keen on this site.

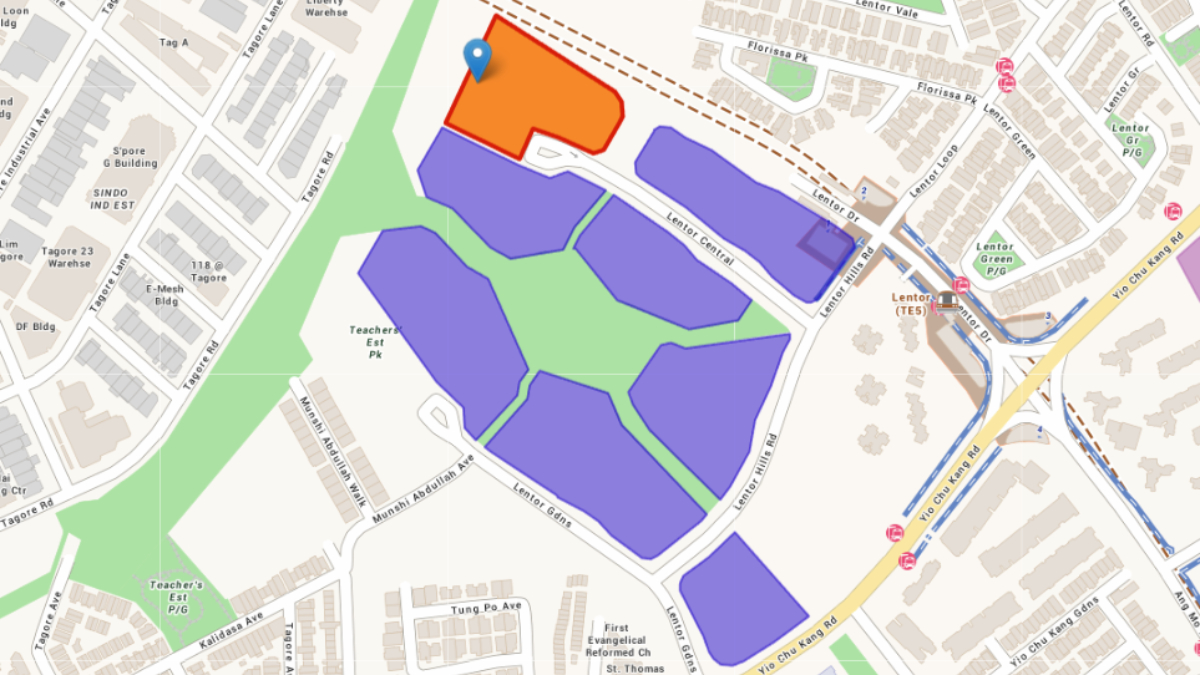

Lentor Central – 580 units

Source: URA

Lentor, being located within the established and centrally located Ang Mo Kio town, has ample amenities and strong connectivity. All seven sites that were previously launched have been sold. Hence, the Lentor Hills estate saw a fresh injection of seven GLS sites initially. Despite yielding close to 3,500 units in total, there was still steady demand across all the projects.

Most recently, Lentor Central Residences sold 93% of its 477 units at its launch. Till date, excluding the latest Lentor Gardens site that was awarded in April 2025, there are less than 100 units remaining.

We can expect developers to closely watch this site, as it has promised a strong demand from both HDB upgraders in nearby towns, and right-sizers from the surrounding landed estates, due to its convenient location and nearby MRT within walking distance.

Miltonia Close (EC) – 430 units

Source: URA

The second EC GLS site of this half, the Miltonia Close EC site will be located off Yishun Ave 1, adjacent to Lower Seletar Reservoir Park.