GFA Harmonisation Explained: What We Observed One Year After the First ‘Harmonised’ Project?

- Egan Mah Jixiang

- 6 min read

- Blog

- 22 May 2025

This is part one of a two-part series covering the analysis of the homes that have launched in the wake of the GFA harmonisation changes that took effect from June 2023.

It has been slightly more than a year ago, the first project that was subjected to the new Harmonisation of Gross Floor Area (GFA) rule, Lentor Mansion, was launched in March 2024. What was a simple tweak to the rules on paper has radically transformed the real estate development industry, forcing developers to change their approach in areas such as bidding for the land, and the subsequent pricing and marketing of the resulting projects.

This has led to a mix of positive and negative effects, as well as some confusion among both developers and homebuyers.

With no previous case studies to fall back upon, developers may not be completely sure about their land bids and their subsequent launch prices. Buyers, on the other hand may not be fully informed of the value of the property, as the commonly used method of comparing neighbouring or recent projects would yield inaccurate results. This is because these referenced past projects have units of ‘larger’ sizes - on paper.

With a year in the rearview mirror, it makes a fitting time to reflect on the impact of the GFA harmonisation rule.

Recap: What is Harmonisation of GFA?

In September 2022, the Urban and Redevelopment Authority (URA) announced that the definition of GFA would be standardised across several statutory boards including URA, Singapore Land Authority (SLA), Building and Construction Authority (BCA) and Singapore Civil Defence Force (SCDF). The key changes are summarised as follows:

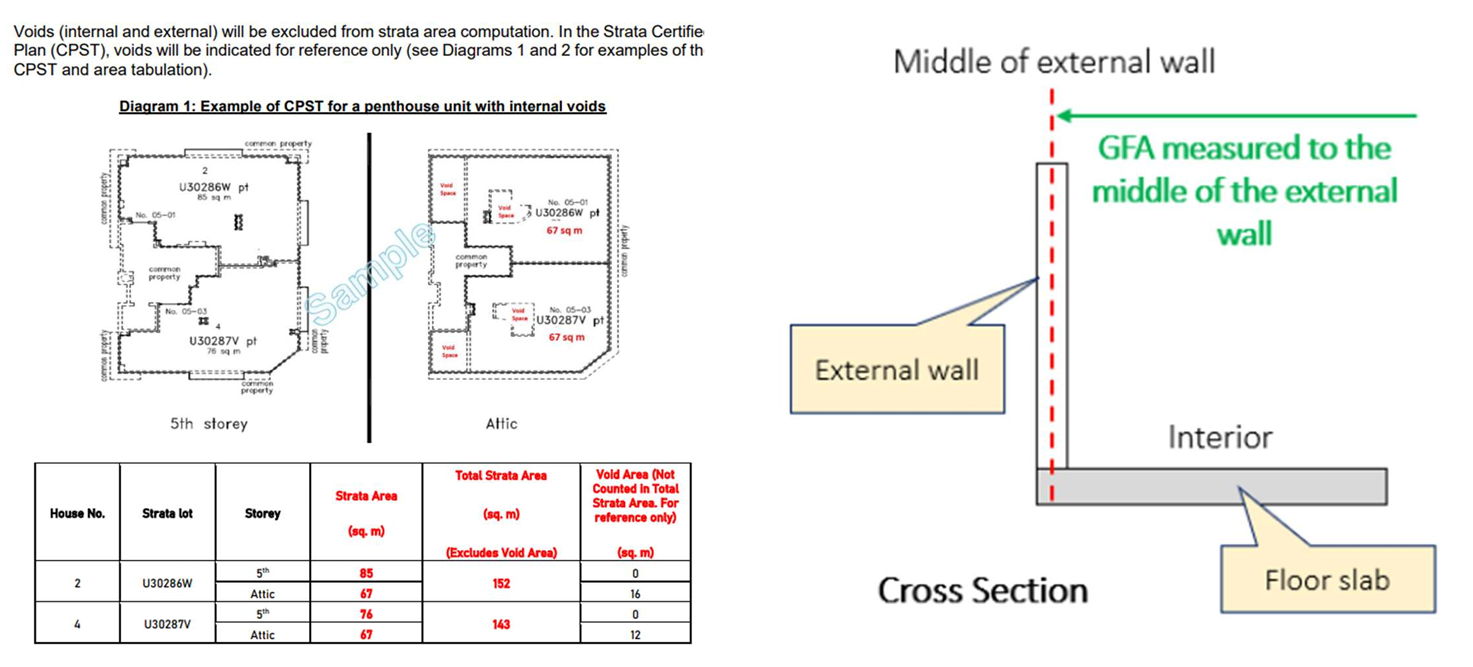

- All agencies’ floor areas will be measured to the middle of the wall

- All strata areas will be included as GFA

- All voids will be excluded from strata area

Image 1: Changes in the definition of GFA

Source: URA

This rule change ultimately ‘closed this loophole’ and increases the transparency of the liveable space that buyers pay for. Buyers are more aware about the space they get and no longer need to pay for large void spaces such as air-con ledges. Developers, on the other hand, will have to rework their pricing strategies to account for the cost of building these areas and factoring them into the overall price quantum.

In addition, standardising the floor area to the middle of the wall was essential. Previously, various agencies had different definition. For example, URA’s GFA is measured to include the full thickness of external walls but excludes voids, whereas SLA’s strata area is only measured up to the middle of the wall and may include voids.

How did property developers adjust to the Harmonisation of GFA rule

Before we discuss the impact of the harmonisation of GFA rule for developers, let us understand the mechanics of their pricing strategy.

Developers will typically aim to maximise the GFA that they can build in a development, which includes strata areas (saleable space such as individual units), and non-strata areas (non-saleable space such as common properties such as car park/playground/roads/common corridors). As a result, constructing non-saleable spaces increases overall building costs for developers, who will need to factor and quantify these costs into the eventual selling price.

In a way, charging for void spaces such as air-con ledges and high-ceiling voids spaces, which were not part of GFA calculations, helps developers to offset part of the cost incurred in building the non-saleable space. But in recent years, some developments have seen “larger-than-necessary” void spaces that were charged to buyers, which have begun to raise concerns.

Image 2: Illustration of the effects of strata areas being part of GFA and voids excluded from strata area

Source: ERA Research and Market Intelligence

1. Site efficiency reduced for the three post-harmonised projects

With the changes, the site efficiency for new developments subjected to the new GFA harmonisation is now reduced. The site efficiency is typically derived based on the proportion of strata area (i.e. sellable area) to the total GFA, which includes non-strata areas (i.e. non-sellable area) such as corridors, lift shafts, swimming pools, landscaping, roads, and car parks etc.

We will understudy three locations, which have developments affected by GFA harmonisation and those that are not, to evaluate the impact of harmonisation on site efficiency. A quick study revealed that developments under the harmonisation rule see less than 10% reduction in site efficiency.

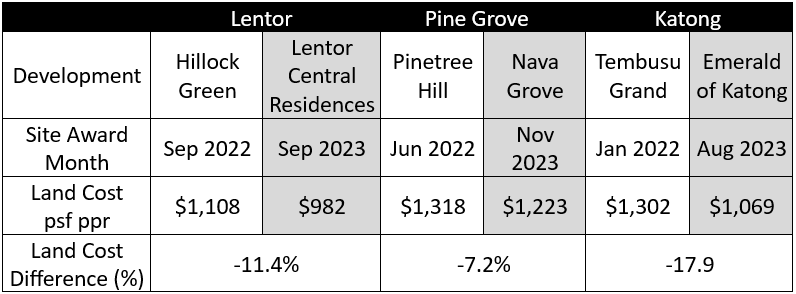

Table 1: Land cost and site efficiency for adjacent projects, pre-and post-harmonisation

Source: URA, ERA Research and Market Intelligence, shaded projects are post-GFA harmonisation

(Developments can see an efficiency of above 100% if they are eligible for certain Bonus GFA Incentive Schemes offered by URA, capped at 10%. This is to promote certain sustainability features or for units to include balconies.)

2. Land cost adjusted lower for the three post harmonised projects

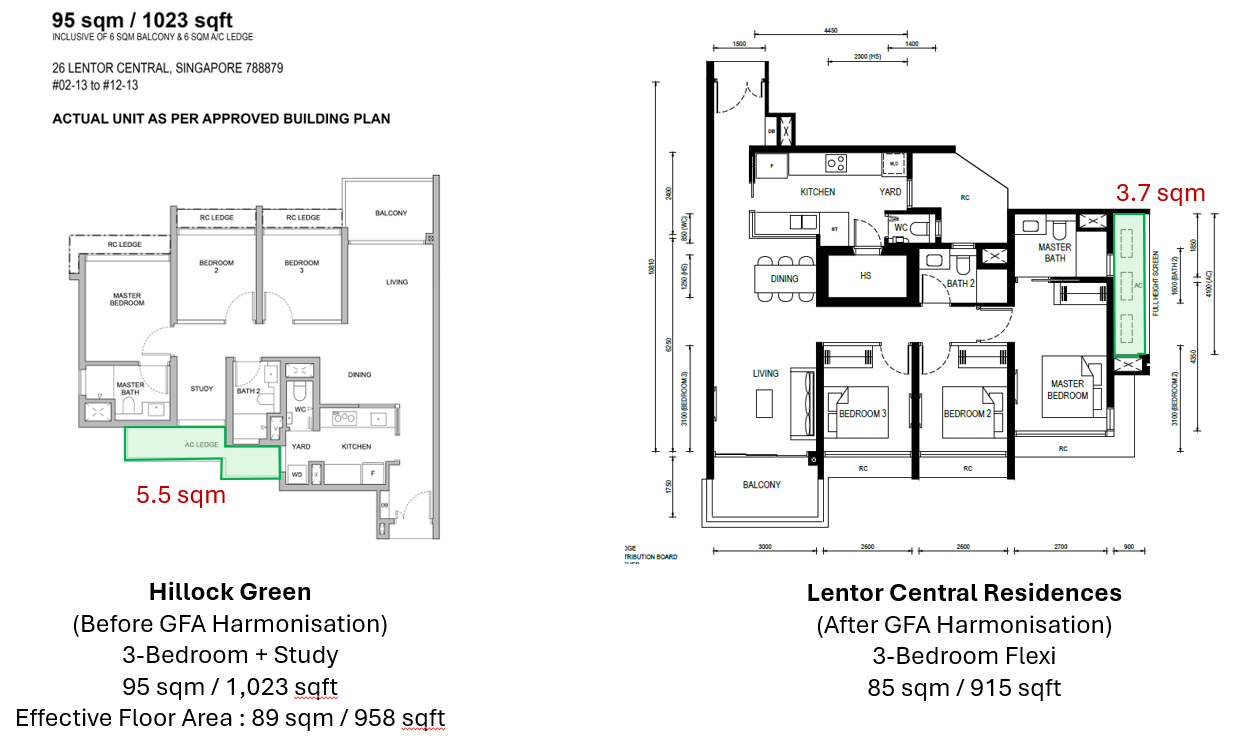

Since void spaces are now not part of the total GFA, home sizes (at least on paper) are now smaller. An example would be 3-bedroom units having a floor area of 915 sqft sq ft instead of 1,023 sq ft before.

Image 3: Floor plans of similar units pre- and post-harmonisation

Source: ERApro, ERA Research and Market Intelligence

In addition, with a reduced site efficiency, developers have thus adjusted their land bids downwards too as they have less sellable area. Using the same three case studies, we found that land costs have decreased across various areas with adjacent sites launching pre- and post-harmonisation of floor area.

Table 2: Land cost for adjacent projects, pre-and post-harmonisation

Source: URA, ERA Research and Market Intelligence, shaded projects are post-GFA harmonisation

New land valuations, especially during this transition period

One short-term challenge arising from GFA harmonisation is land valuation. During this transition period, differing interpretations of site efficiency between the Chief Valuer, who determines the reserve price, and developers may lead to mismatched land valuations.

Consequently, reserve prices or developers’ bids for affected sites may be significantly lower compared to nearby plots not subject to the new GFA definitions. This could result in units being either underpriced (if developers bid conservatively) or overpriced (if bids are aggressive). In the former case, buyers may benefit from more attractive pricing; in the latter, it could lead to new benchmark launch prices.

As more bids emerge, government agencies must consider developers’ revised valuation methodologies and factor in developers’ bids to align reserve prices across harmonised and non-harmonised sites.

Conclusion: Can we expect lower prices?

While units may appear smaller (at least on paper), this new harmonisation of GFA brings about greater transparency to buyers. Buyers are aware of the liveable space that they are paying for. Moreover, developers are also less likely to include larger-than-usual air-con ledges or unusable void spaces. This will ensure that floor plates and designs are more efficient for homeowners.

During this transition phase of GFA harmonisation, it does present some opportunities as some new launches may be attractively priced because of the difference in land cost. Buyers who can spot these opportunities and act before the market fully reconciles land valuations and site efficiencies may be able to capitalise on these pricing gaps.

Are you keen to find out where these opportunities lie, or understand more about the harmonization of GFA rule? If so, speak to an ERA Trusted Adviser today.

I confirm that I have read theprivacy policy and allow my information to be shared with this agent who may contact me later.