1Q 2026 HDB Quarterly Report: Demand for Resale Flats Holds Firm Even as Prices Moderate

- ERA Singapore

- 5 min read

- PressRelease

- 24 Apr 2026

SINGAPORE, 24 April 2026 – According to the Housing and Development Board (HDB)’s quarterly figures, HDB resale prices fell in 1Q 2026, with the HDB Resale Price Index (RPI) moderating by 0.1% quarter on quarter (q-o-q). This follows a flat reading in the previous quarter and marks the first decline in resale prices in nearly seven years, since 2Q 2019.

This marginal dip in the HDB RPI suggests the market may be entering a more balanced phase after several years of sustained growth.

“We are likely seeing the snowball effect of previous cooling measures, such as the 15-month wait-out period for private-property right-sizers, alongside the sustained ramp-up in BTO supply. These policy moves have successfully tempered resale price growth by dampening demand and expanding supply for first- and second-timers,” said Eugene Lim, Key Executive Officer, ERA Singapore.

“While a broader correction in HDB prices might be underway, growth could persist in specific segments of the resale market, such as million-dollar HDB flats.

Even in a more selective market, some buyers may still be willing to pay a premium for well-located flats near amenities, particularly those with long remaining leases."

Resale transaction volume rises on a sharp increase in MOP flat supply

“In 1Q 2026, 6,285 resale applications were recorded, marking a 19.6% q-o-q increase. This also represents a 4.6% year-on-year (y-o-y) decline from the same period in 1Q 2025.

Resale activity increased on the quarter in 1Q 2026, coinciding with a quieter February BTO exercise. Demand during the BTO exercise was mainly centred on Shorter Waiting Times (SWT) flats, while overall application figures were more modest at around 15,000, compared to the 33,000-strong response in October last year because of the concurrent SBF exercise.

The resale market continues to act as a crucial outlet for unmet housing demand, especially for buyers who value immediacy or are not keen on the locations announced for the upcoming BTO exercises.

The increase in flats exiting their Minimum Occupation Period (MOP) this year has also expanded the resale pool, offering buyers a broader range of choices across locations and flat types. This will help sustain transaction volumes even as price growth remains moderate.”

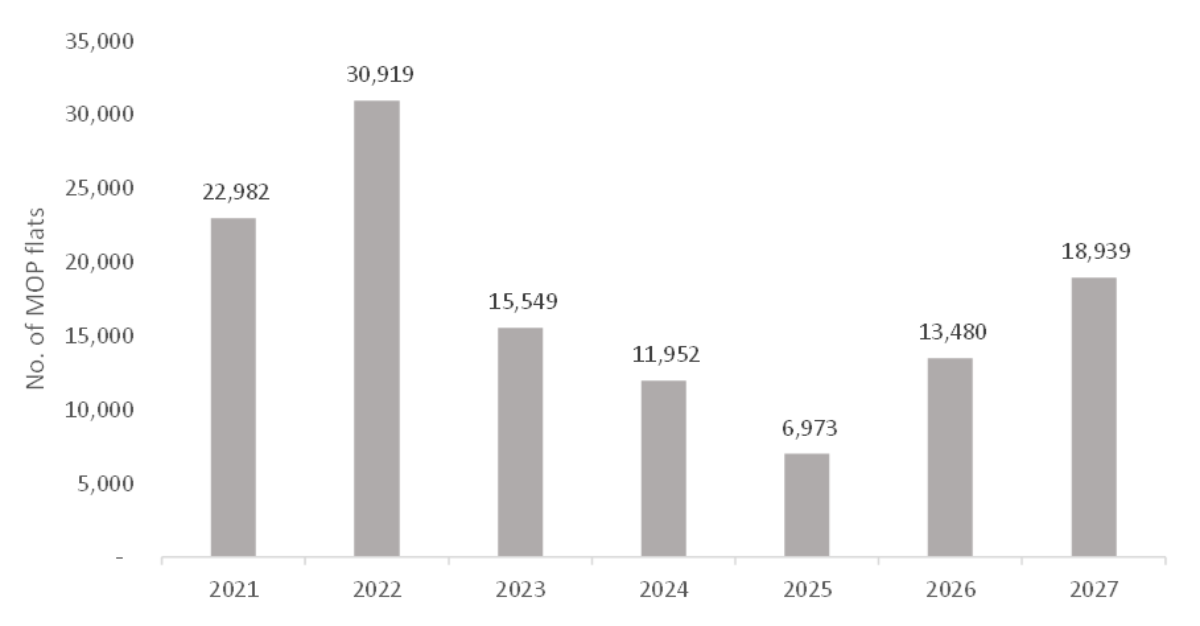

Significant Increase in MOP Flats Anticipated in 2026

"Resale supply is set to expand significantly in 2026, with an estimated 13,480 flats reaching their MOP, nearly double the 6,973 units in 2025.

This influx will broaden buyers' choices across locations and flat types, while reducing competition in the resale market.

Coupled with a steady pipeline of BTO launches, the increase in MOP flats is expected to keep price growth at a measured pace, thereby stabilising the market."

Chart 1: Number of MOP Flats by year

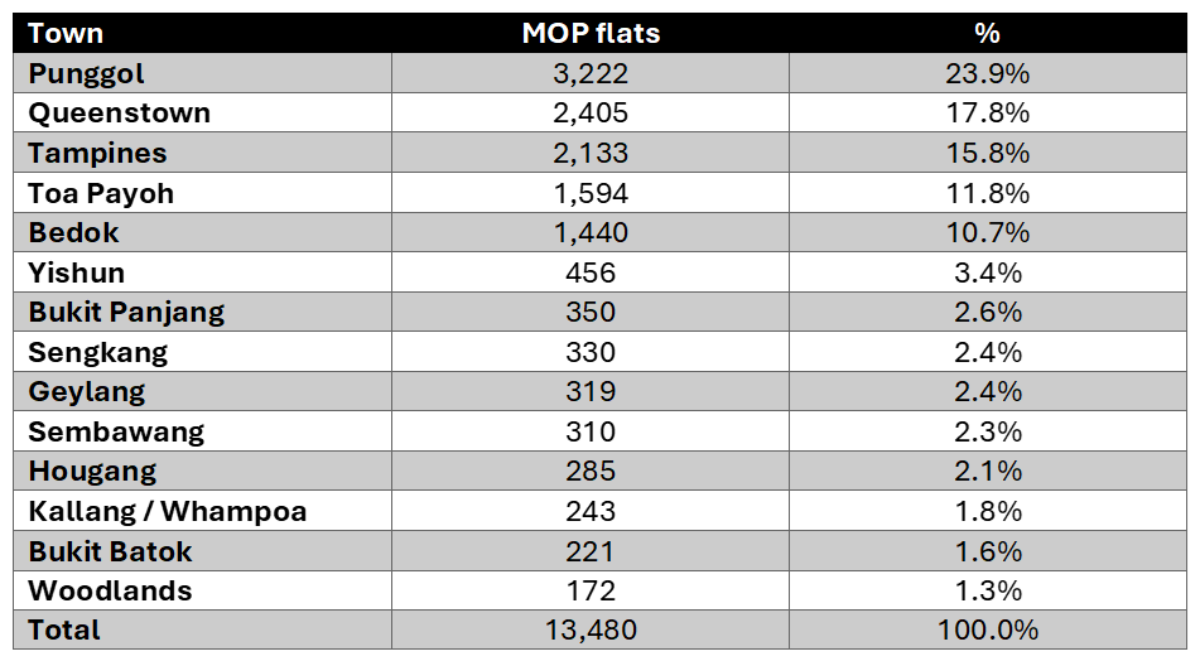

Table 1: Distribution of MOP Flats by Town in 2026

"Nearly 70% of flats reaching their MOP this year are in popular estates such as Punggol, Tampines, Toa Payoh, and Queenstown. Flats that are reaching MOP in these locations are likely to command higher asking prices, supported by their strong location appeal and relatively longer remaining leases.

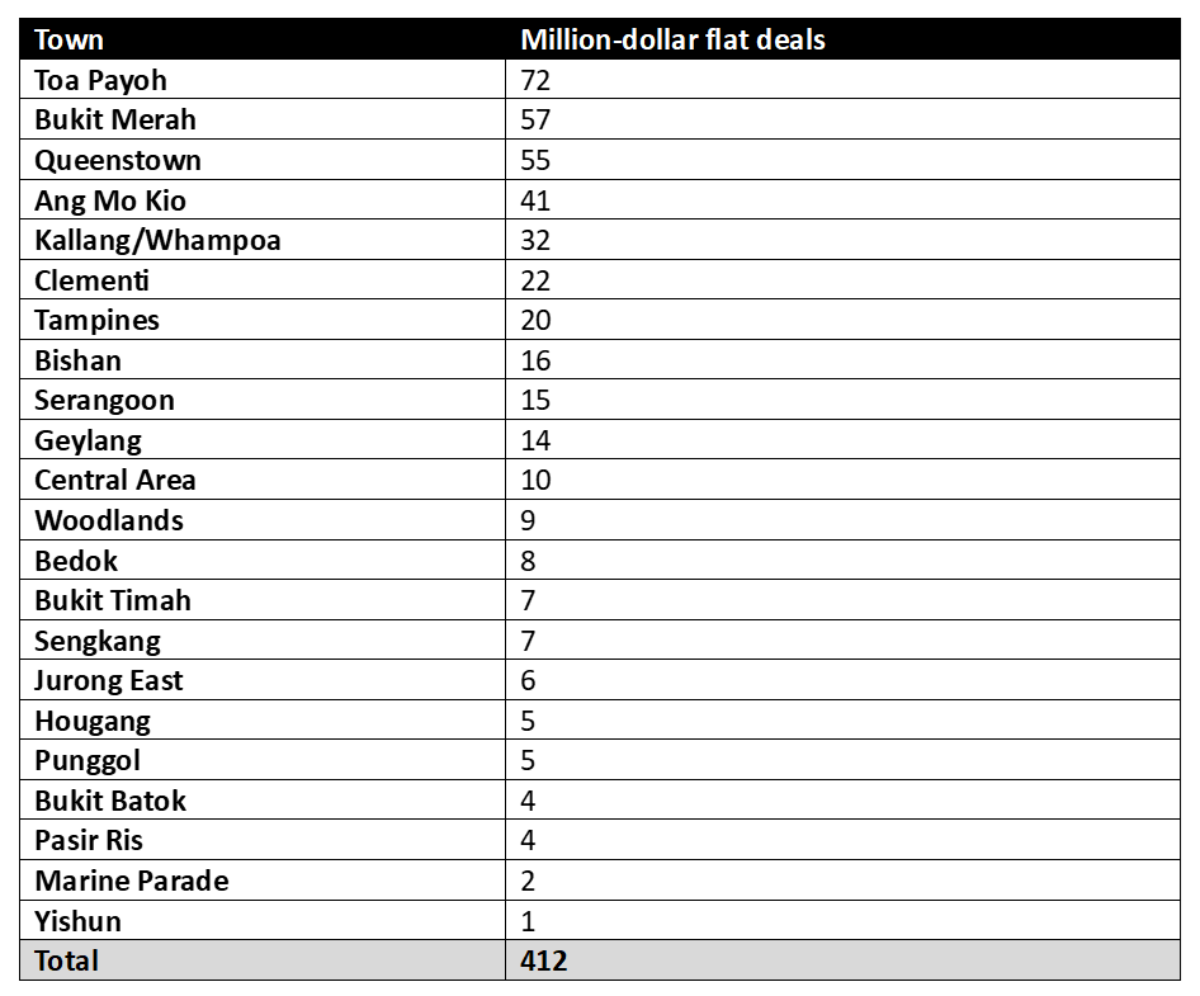

Million-dollar flat transactions are rising, but overall HDB resale transaction prices remain affordable.

For 1Q 2026, the market for million-dollar HDB flats remained active, with some 412 cases recorded. This is 17.7% higher than the 350 cases in 4Q 2025, but still accounts for just 6.6% of total quarterly transactions.

This shows that although high-value transactions are growing, they remain a relatively small share of the overall resale market, which remains broadly accessible to the typical homebuyer.

At least 63 deals, or 15% of million-dollar HDB transactions in 1Q 2026, involved newly MOP-ed units with remaining leases of 94 years or more. The bulk of these transactions were concentrated in newer projects such as Alkaff Courtview and Ang Mo Kio Court, which recorded 24 and 20 deals, respectively.

Million-dollar transactions in 1Q 2026 also remained concentrated in popular towns such as Toa Payoh, Queenstown, Bukit Merah and Ang Mo Kio. This reflects persistent demand for newer HDB homes in central locations, which are not subject to the tighter resale conditions applied to Plus and Prime flats.”

Table 2: Distribution of Million-Dollar HDB Deals by Town

Rental

“HDB rental activity remained broadly stable in 1Q 2026, with approved applications dipping just 0.2% q-o-q to 9,535 cases. On an annual basis, rental activity also eased slightly by 1.3% compared to the 9,662 applications recorded for 1Q 2025.

This suggests that rental demand remains resilient, underpinned by a steady foreign workforce and private property owners affected by the 15-month wait-out period.”

Outlook for 2026

“With HDB planning to launch 19,600 BTO flats across three exercises this year, including more than 4,000 Shorter Waiting Time (SWT) flats, the housing supply will increase substantially. This expansion aims to diversify options and support more stable growth in resale prices.

Another 15,000 new flats are also set to be released in the upcoming June and October 2026 BTO exercises, including flats in popular areas such as Bishan, Berlayar and Pearl Hill. As a result, the attractiveness of these offerings might draw some attention away from the HDB resale market.

Despite the slight decline in 1Q 2026, the HDB RPI is expected to continue its steady climb of 2-5% for the rest of 2026, supported by the higher price base established in 2025. At the same time, a larger pool of more than 13,000 flats reaching their MOP in 2026 should help sustain both resale price growth and transaction activity.”

For media enquiries, please contact:

Lisha Rodney

Public Relations Manager, ERA Singapore

Email: [email protected]

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.