1Q 2026 URA Real Estate Statistics: Transactions Moderate to Start 2026 Amid Global Uncertainty

- ERA Singapore

- 10 min read

- PressRelease

- 24 Apr 2026

SINGAPORE, 24 April 2026 – “According to the Urban Redevelopment Authority (URA), private home prices rose by 0.9% quarter-on-quarter (q-o-q) in 1Q 2026, continuing the steady pace of growth, comparable to the previous quarterly increase of 0.6%.”

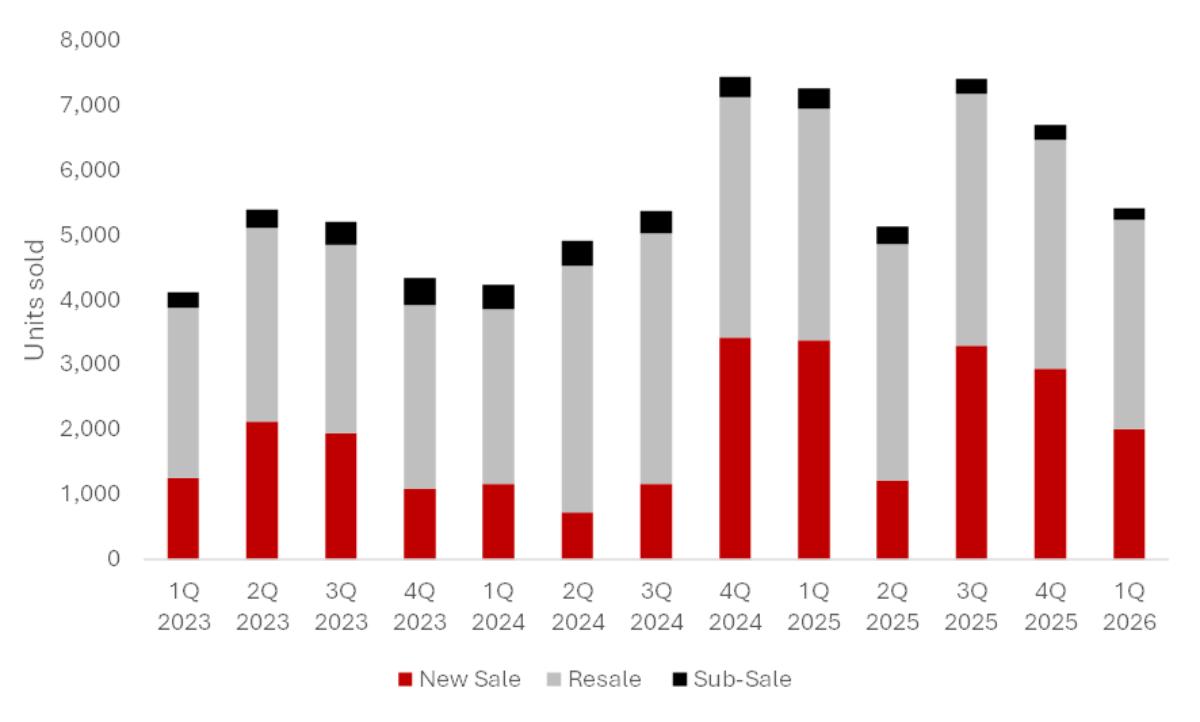

The total volume of private home transactions in 1Q 2026 fell by 19.2% to 5,413 units. This comes after a strong 4Q 2025 showing, which was supported by a surge in new supply from eight project launches. The softer performance in 1Q 2026 was largely due to a reduced launch pipeline and the typical Lunar New Year seasonal lull.

“Following the bumper crop of new launches that propelled private property price growth in the latter quarters of 2025, we have witnessed a moderation in the market to start 2026. This can be attributed to a lower volume of launches in the quarter and global uncertainty amid geopolitical tensions stemming from the war in the Middle East,” said Marcus Chu, Chief Executive Officer, ERA Singapore.

“The moderation in 1Q 2026 is not a sign of weakening demand, but a reflection of fewer project launches and seasonal factors. What we are seeing is a more selective market, buyers remain active, but they are more deliberate in their decisions.

Some buyers may have opted for a wait-and-see approach, anticipating heightened risk in homebuying and upgrading amid economic uncertainty.

An additional 4,575 private residential units on the 1H 2026 GLS Confirmed List, which is 50% above the average half-yearly Confirmed List supply, will continue to support the Government’s aim to stabilise land prices and ensure a steady flow of new homes over the coming years. This aligns with efforts to maintain a stable and sustainable property market.

Resale and subsale transactions fell to 3,225 units (8.6% q-o-q) and to 175 units (23.9% q-o-q) in 1Q 2026, respectively. This follows supply completions falling to just 7,034 units between 1Q 2025 and 1Q 2026, prompting buyers towards the new home market.”

Chart 1: Breakdown of private home transactions (excluding ECs) by type of sale

"Unsold stock fell 7.5% q-o-q to 16,219 units in 1Q 2026. This follows the successful launch of eight new projects during the quarter. Strong take-up rates also signal sustained market confidence and have created a ripple effect, boosting sales momentum in previously launched developments.

1Q 2026 saw 911 private home completions (excluding ECs). Excluding ECs, the full-year total for 2026 is expected to be 6,282 units, marginally higher than 2025’s count of 6,123 units.”

Prices

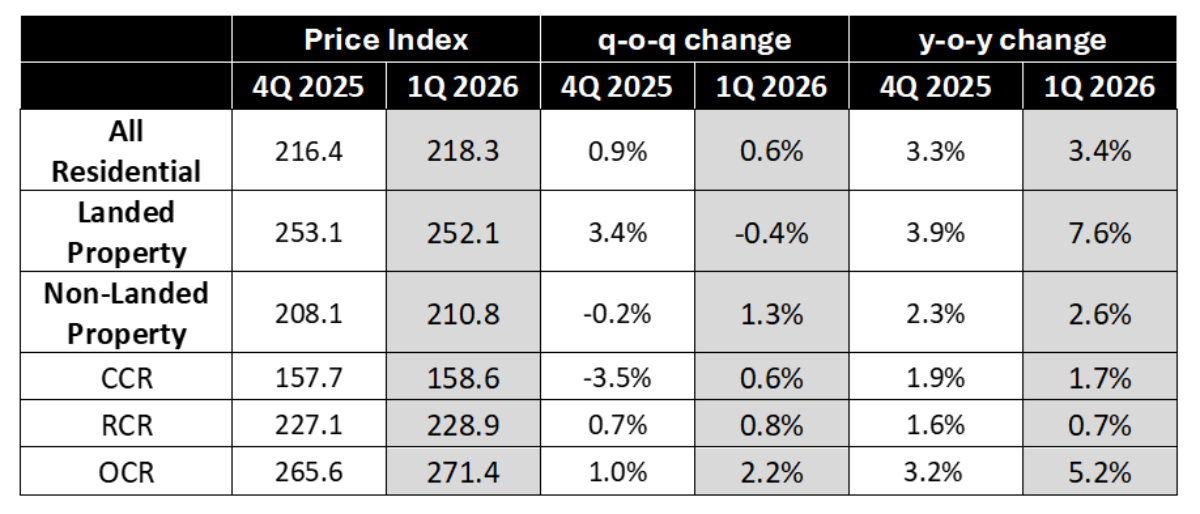

“The All-Residential Private Price Index rose 0.9% q-o-q in 1Q 2026. This is an uptick from the slight 0.6% increment in 4Q 2025.

This is driven by non-landed prices in the Outside Central Region (OCR), where prices rose by 2.2% q-o-q. The uptick in OCR prices could be attributed to stellar sales at Pinery Residences, which sold over 90% of its units at precedent prices for condos launched in Tampines. Concurrently, the Rest of Central Region (RCR) recorded a 0.8% increase, and the Core Central Region (CCR) a slight 0.6% increase due to the warm reception for Newport Residences and River Modern, which established new benchmark prices. The strong price growth in the OCR reflects the depth of upgrader demand in suburban markets. Many homeowners are sitting on substantial housing equity, and when the right opportunity comes, they are ready to move.”

Table 1: Change in URA Private Property Price Indexes for 4Q 2025 and 1Q 2026

Transaction Volume

New Sales

“In total, developers sold 2,013 new homes in 1Q 2026, a 31.5% decline from 2,940 units in the previous quarter. Developers also launched fewer homes, totalling 1,844 units, down from 2,632 units in 4Q 2025. Amid a smaller pipeline of new launches in 1Q 2026, buyers’ interest remained firm, signalling the strength of Singapore’s new home market.

Despite the decline in volume, underlying demand remained firm, with projects continuing to attract strong take-up. Projects entering the market continued to attract substantial interest, reflecting sustained buyer confidence despite global uncertainty. This has contributed to a 0.9% increase in the price index, despite muted transaction volumes relative to the previous quarter.

Buyers who were unable to secure their preferred option during the launches in the latter half of 2025 could also have turned to projects launched in 1Q 2026.

1Q 2026 saw the launch of two EC projects, Rivelle Tampines and Coastal Cabana in Pasir Ris, both of which attracted strong demand. As the final EC launches in the East for the foreseeable pipeline, buyers moved decisively, with the two projects launched in the quarter accounting for a total of 1,117 units to date.”

Resale & Sub Sale

“In the resale segment, 3,225 transactions were recorded in 1Q 2026, representing a 8.6% q-o-q decline from the 3,529 private homes sold in 4Q 2025. This marks the lowest level since 1Q 2024. The slowdown indicates a clear shift in buyer focus towards the new home market. A strong pipeline of new launches in desirable locations has reduced demand in the resale segment.

Sub-sale transactions slipped further to 175 units in 1Q 2026, down from 230 units in the previous quarter. The pullback was largely due to a smaller pool of private home completions, with 6,123 units (excluding ECs) in 2025 and just 911 units in 1Q 2026. This has limited the flow of new resale and subsale stock, further contributing to the decline in transactions.

This divergence between volumes and prices suggests that although buyers are more selective, sellers remain firm, supported by strong underlying fundamentals. Well-located, competitively priced resale units continue to attract buyers.

As new launch activity accelerates in the coming quarters, resale volumes may remain subdued in the short term, but price stability is expected to continue, supported by strong fundamentals and limited supply."

Landed

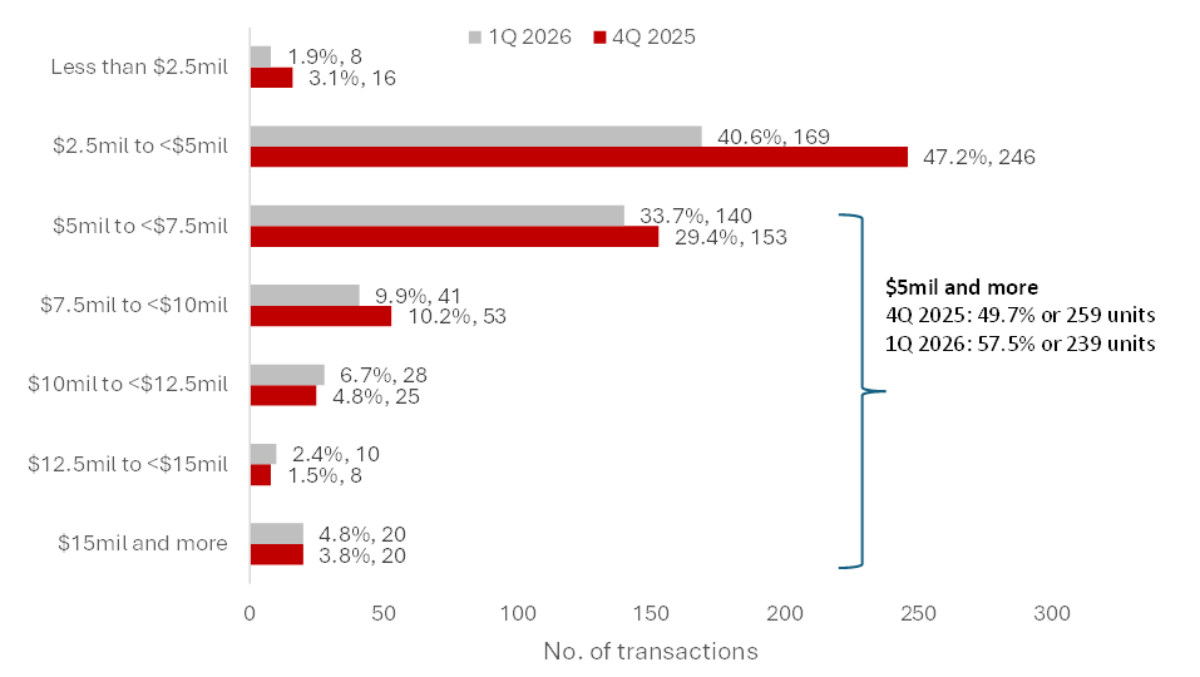

“The landed housing market witnessed a decline of 0.4% in prices this quarter, in-line with transactions falling by 20.2% q-o-q to 416 units in 1Q 2026. Despite the moderation, the landed market remains resilient, with the downturn being attributed to a seasonal dip consistent with historical trends where activity typically slows in the first quarter.

The landed segment is currently in a pricing stand-off, sellers are holding firm, while buyers remain cautious. However, this is a short-term dynamic. Demand for landed homes remains fundamentally strong given their long-term value.

Despite the near-term slowdown, demand for landed homes remains fundamentally strong. These properties continue to be regarded as a long-term store of value and a vital wealth asset.

Additionally, the prevailing interest rate environment sustains buying confidence among high-income earners, thereby boosting demand for landed homes.

Demand for landed homes remains steady. Beyond their prestige, they are valued for long-term capital preservation and growth, with the current lower interest rate environment further boosting demand among high-net-worth and high-income buyers."

Chart 2: Landed Price Quantum 4Q 2025 versus 1Q 2026

Rental

“The All-Residential Rental Price Index recorded a 0.3% q-o-q increase in 1Q 2026, reversing the 0.5% q-o-q decline seen last quarter. Overall rents for non-landed properties also inched down up 0.4% q-o-q in the same period, reversing a dip of 0.1% q-o-q in the previous quarter. Meanwhile, landed property rents recorded an increase of 0.1% after the steep decline of 3.0% in 4Q 2025.

Among market segments, only the RCR non-landed market saw a decline, falling 0.2% q-o-q. This can be attributed to the higher base from 4Q 2025, after the significantly larger increase of 0.6% the last quarter.

This quarter saw just two large private residential projects completed – Sceneca Residence and The Botany at Dairy Farm. Investors may put these units up for rent in the coming months. This may result in higher rents as tenants may be willing to pay more for a newly completed development, due to the unit’s condition and new features in the development.

The growing supply pipeline is expected to keep rent growth in check. In 2026, non-landed private home completions are also set to reach 6,282 units, with a further 8,489 units forecast for 2027 (excluding ECs). With this fresh supply, tenants may expect more stable rents for the foreseeable future."

Upcoming Launches

“2026 kicked off with the successful launch of Coastal Cabana EC. Since its launch on 17 January 2026, more than two-thirds of units have been sold. We saw the launch of two more private developments in January 2026 - Newport Residences and Narra Residences. These three developments, which yielded 1,534 units, cater to different buyer profiles.

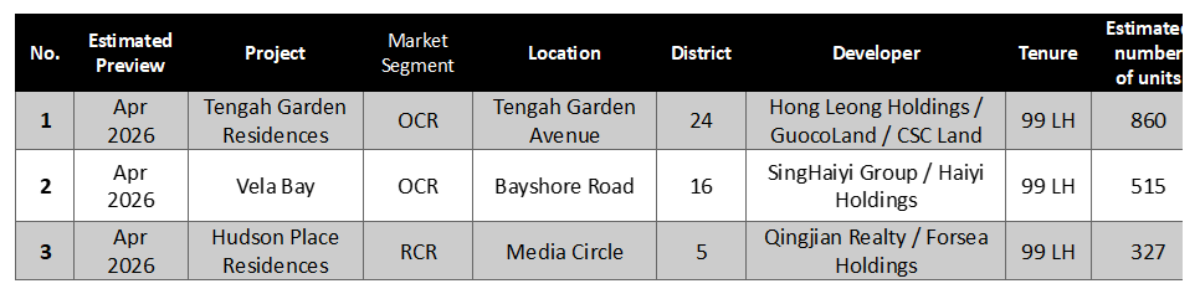

For the whole of 2026, we can expect another 18 new private developments and five ECs to be launched. These projects are located across all regions, offering a range of product niches that cater to buyers’ varied needs, such as affordability and locational preferences."

Table 2: New Home Launches in 2Q 2026

Market Outlook

“The dip in transactions in 1Q 2026 was largely due to the seasonal lull. Developers typically hold back their launches until after the Lunar New Year festivities, which occurred in February this year.

Following the festive period, we have noted the market regaining momentum following the launch of Pinery Residences and Rivelle Tampines (EC) in March. Both achieved a stellar 92% sales rate during their respective launch weekends. The three highly anticipated launches in 2Q 2026 are also expected to perform well, building on the strong momentum from the first quarter.

In 2026, the private residential market is expected to remain resilient, supported by moderate price growth driven by strong owner-occupier demand and ongoing right-sizing trends. Healthy take-up rates from recent project launches reinforce this positive outlook. This underlying demand has also prompted developers to commit to new projects, as evidenced by aggressive, higher bids submitted for recent Government Land Sales (GLS) tenders.

Following the URA Quarterly Statistics, overall private property prices increased by 0.9%. It remains on track to reach ERA’s projected 2026 forecast of 3% to 5% growth.

With a total of 5,413 transactions recorded, (including 2,013 primary market and 3,400 secondary market transactions), and a pipeline of 24 residential projects, including one landed project and 5 EC launches this year, ERA Singapore projects new home sales to be between 9,000 and 10,000 units, while the secondary market is expected to record 13,000 to 14,000 transactions, indicating stable underlying demand in the year ahead.

Looking ahead, we expect market momentum to pick up in the coming quarters as more projects are launched. Singapore’s property market remains underpinned by strong local demand, disciplined supply, and stable economic fundamentals. Barring major external shocks, we remain confident in achieving our full-year projections."

For media enquiries, please contact:

Lisha Rodney

Public Relations Manager, ERA Singapore

Email: [email protected]

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.