3Q 2025 URA Private Residential Report: Sustained Price Growth Amid Wave of New Launches

- ERA Singapore

- 7 min read

- PressRelease

- 1 Oct 2025

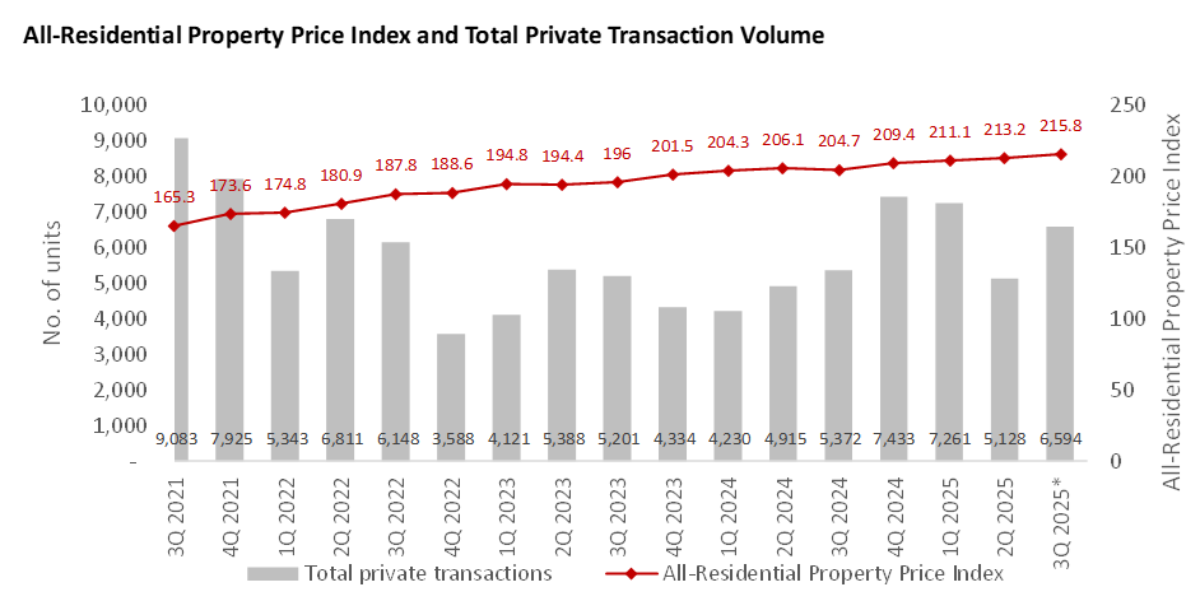

SINGAPORE, 1 October 2025 – According to flash estimates released by the Urban Redevelopment Authority (URA) for 3Q 2025, the All-Residential Property Price Index exhibited a modest increase of 1.2% quarter-on-quarter (q-o-q), while the total transaction volume of private homes rose 28.6% q-o-q to 6,594 units.

The overall non-landed property price index rose 1.1% q-o-q, reaching 209.1 in 3Q 2025. Both private home demand and price growth were boosted by a bumper slate of new launches, concentrated in locations that either experienced a hiatus in fresh supply or saw inaugural launches.

- The Core Central Region (CCR) non-landed price index registered the sharpest increase, reflecting a 2.4% q-o-q uptick due to benchmark pricing at new launches that lifted prices.

- This was followed by the Outside Central Region (OCR), which grew by 1.0% q-o-q, and the Rest of Central Region (RCR), which saw a 0.4% q-o-q increase in corresponding prices.

Meanwhile, the landed property price index rose 1.4% q-o-q, extending last quarter’s uptick. Prices rose amid stronger demand for landed homes from condo upgraders.

However, with buyers focusing on new launches, the secondary market saw a dip in resale and sub-sale transactions during the quarter.

Chart 1: All-Residential Property Price Index and Total Private Transaction Volume

Source: URA, ERA Research and Market Intelligence *Based on flash estimates

“A bumper slate of new launches largely propelled the appreciation of private home prices in 3Q 2025. Demand was particularly strong in areas that had either experienced a pause in new supply or welcomed their first project. The surge in primary market activity, however, drew buyer interest away from the resale market, dampening its performance,” said Marcus Chu, CEO, ERA Singapore.

“Based on the current pace of new private home sales, 2025 has already surpassed the full-year total of 6,469 units in 2024. With this momentum, 2025 is on track to meet ERA’s forecast of 8,500 to 9,500 units, marking the highest annual transaction volume since 2021.”

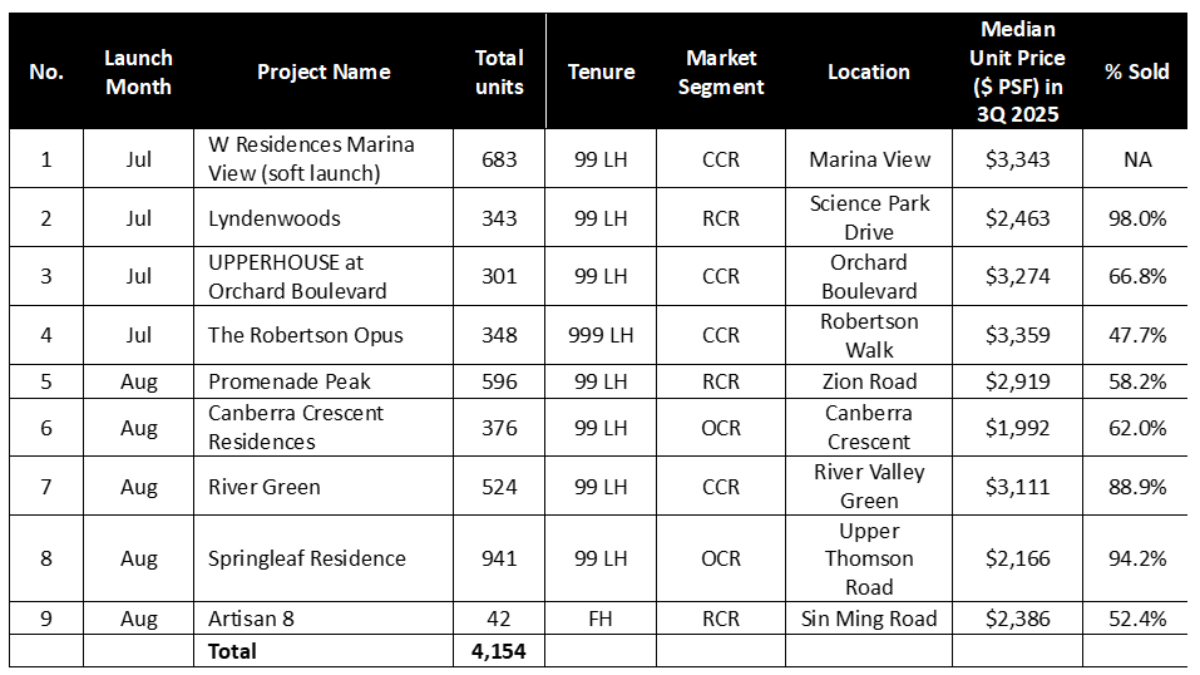

Table 1: List of new launches in 3Q 2025

Source: URA, ERApro as at 18 Sep 2025, ERA Research and Market Intelligence

“The CCR saw renewed interest with four launches, namely UPPERHOUSE at Orchard Boulevard, The Robertson Opus, River Green, and the soft-launched W Residences Marina View. This new wave contrasts with a subdued year for the CCR in 2024, when developers introduced just 680 new units in total.”

“Caveat data (as at 30 Sept 2025) shows that the CCR recorded approximately 894 non-landed private home sales (excluding ECs) in 3Q 2025. This marks the highest quarterly total for the CCR in 15 years since 2Q 2010, when 1,066 units were sold.”

“Furthermore, nearly two-thirds of CCR’s new private homes sold in 3Q 2025 were priced below $2.5 million. This ‘sweet spot’ pricing has made the CCR more accessible to local buyers, despite the segment’s traditional positioning as a luxury market.”

“Buyers were attracted to UPPERHOUSE at Orchard Boulevard for its prime location directly above Orchard Boulevard MRT station. Demand was also reinforced by confidence in Paterson’s transformation, outlined in the 2025 Draft Master Plan. Similarly, River Green’s attractive pricing and direct sheltered access to the Great World MRT made it appealing to Singaporean and PR buyers. Meanwhile, The Robertson Opus, which offers a 999-year tenure, was keenly pursued as a legacy asset.”

“In the RCR, Lyndenwoods emerged as the best-seller, with 94.5% of its 343 units sold during its launch weekend. Its appeal lay in being the first residential project in Singapore Science Park, which is set to benefit from the Greater one-north master plan. Modern amenities and proximity to Kent Ridge MRT station further enhance this desirability.”

“At 63 storeys high, Promenade Peak attracted buyers looking for panoramic views of Singapore’s city skyline, while also offering a first-mover advantage within the River Valley – Zion Road precinct.”

“More than half of Artisan 8’s 42 units have been sold so far. This boutique, freehold development at Sin Ming is conveniently situated near Upper Thomson MRT Station and popular shophouse eateries in the area. This appeal has generated buying interest, especially among existing residents living nearby.”

“The OCR saw two new launches in 3Q 2025 – Springleaf Residence and Canberra Crescent Residences. Both launches attracted strong interest from buyers on the sidelines, taking advantage of the limited new supply in their respective areas. Springleaf Residence became notable as the first high-rise condominium in the Springleaf estate. Meanwhile, Canberra Crescent Residences marked the first launch in Canberra in four years, benefiting from pent-up demand.”

“Unlike the previous quarter, the EC segment experienced a significant increase in transactions, with 569 units sold according to caveat data as of 30 September 2025. This marks more than double the 147 units sold in the last quarter. The jump was mainly driven by the launch of Otto Place at Tengah, where approximately 559 units have been sold to date, accounting for 93.2% of its total supply.”

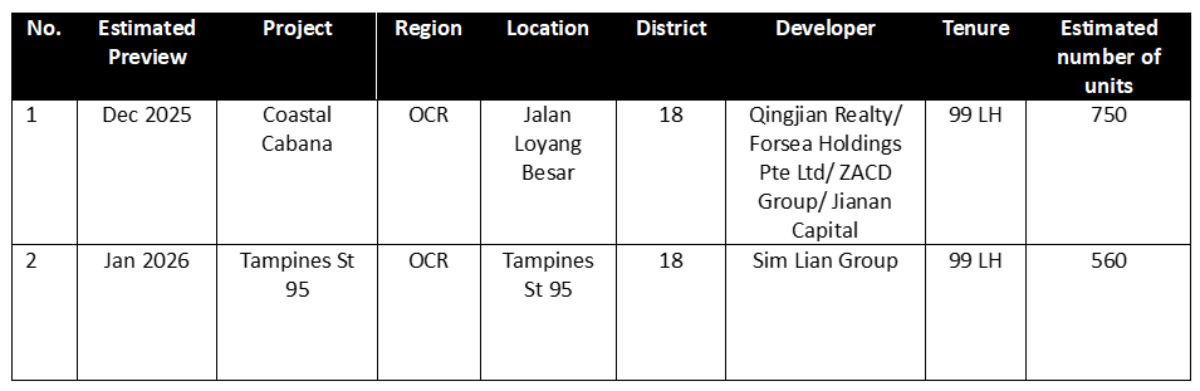

“With the current EC launches completely sold out, buyers will have to wait for the 748-unit Coastal Cabana at Jalan Loyang Besar, set to launch in January 2026.”

“In 3Q 2025, resale transactions for non-landed private homes (excluding ECs) decreased by 12.5% quarter-on-quarter to 2,762 units. This also marks a deviation from the consistent pattern of resale transaction volumes, which has remained steady around the 3,000-unit level for the past five quarters.”

“Buyer attention moved away from the resale market mainly due to the bumper supply of new home launches in desirable locations, which provided new opportunities and more choices.”

“Meanwhile, sub-sale activity decreased by 26.8% q-o-q to 169 deals, mainly due to fewer completions. Private home completions (excluding ECs) are forecasted to reach 4,949 units by the end of 2025, compared to 8,460 units in 2024.”

“The upward revision of Singapore’s 2025 GDP forecast from 0–2% to 1.5–2.5% has boosted consumer confidence, supporting homebuying demand in 3Q 2025.”

“Buyer confidence may receive further support from new housing neighbourhoods in Dover, Defu, Newton, and Paterson, as well as integrated community hubs in Sengkang, Woodlands North, and Yio Chu Kang. These developments indicate long-term urban renewal and improved liveability, which could boost market optimism.”

“Resale and sub-sale activity in the secondary market is expected to moderate further amid limited completions. At the same time, a strong pipeline of new launches is likely to draw buyer attention to the primary market, as reflected in 3Q 2025’s performance.”

“Barring any unforeseen circumstances, ERA Singapore projects new home sales to be between 8,500 – 9,500 units for the whole of 2025. In conjunction, sub-sale and resale transactions are also expected to reach between 1,100 to 1,300 units and 14,000 to 15,000 units respectively by the end of 2025.”

Table 2: Upcoming launches in 4Q 2025 and 1Q 2026

Source: ERA Project Marketing

Table 3: Executive Condominiums

Source: ERA Project Marketing

For media enquiries, please contact:

Lisha Rodney

Public Relations Manager, ERA Singapore

Email: [email protected]

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.