3Q 2025 URA Real Estate Statistics: Private Home Demand Rebounds, Led by a Wave of Blockbuster New Launches and a Robust Resale Market

- ERA Singapore

- 9 min read

- PressRelease

- 24 Oct 2025

SINGAPORE, 24 October 2025 – According to the Urban Redevelopment Authority (URA), private home prices rose by 0.9% quarter-on-quarter (q-o-q) in 3Q 2025, maintaining a steady pace of growth comparable to the previous quarterly increase of 1.0%.

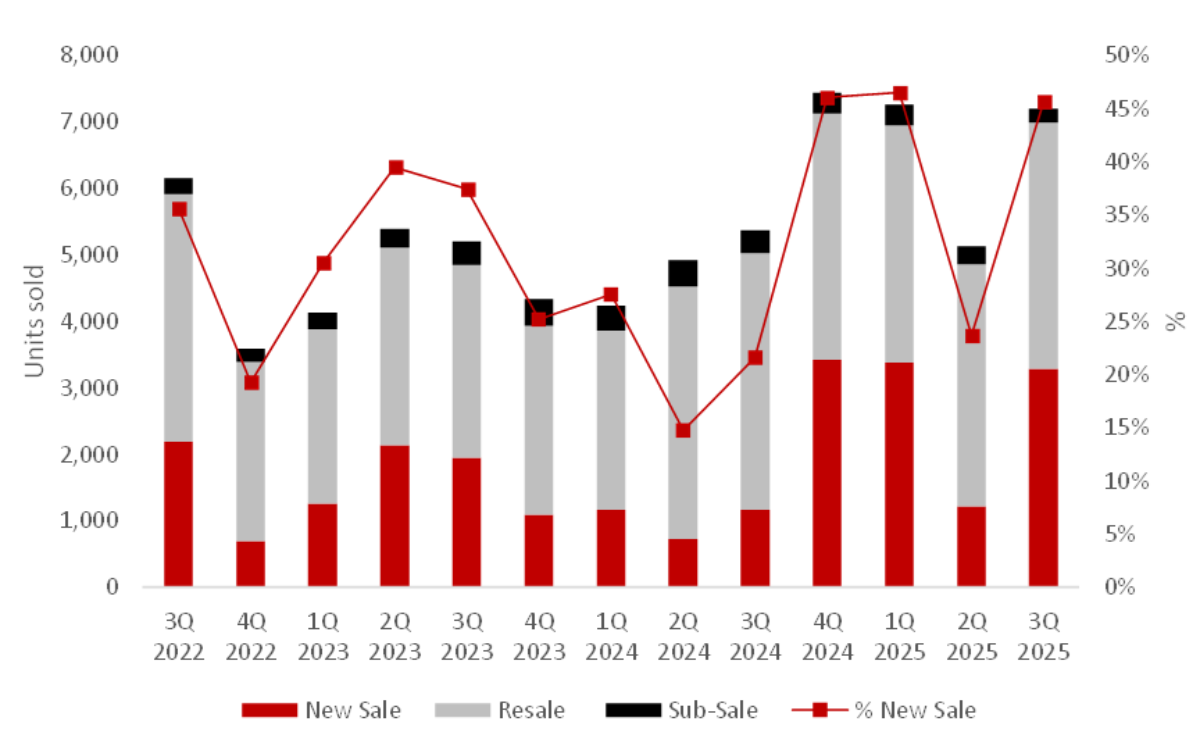

The total volume of private homes transactions in 3Q 2025 rose a staggering 44.4% from 5,128 in 2Q 2025 to 7,404 units due to a surge in supply from eight new launches. This rebound helped offset the slower activity seen in 2Q 2025, which had been dampened by the General Elections and June school holidays.

“Homebuyers came out in full force in 3Q 2025, driven by lower interest rates, more sanguine economic sentiment despite lingering uncertain macroeconomic outlook, and potential gains from the financial markets – showcasing their continued confidence in Singapore’s property market,” said Marcus Chu, CEO, ERA Singapore.

“Some buyers may have chosen to enter the market earlier, anticipating that new home prices will see another wave of increase in line with the recent upward trajectory of land prices.”

“With the availability of new launches across all market segments, new private home sales (excluding ECs) saw a recovery in 3Q 2025. In total, 3,288 new homes were sold over the quarter, representing a 171.3% q-o-q uptick in transaction volumes. Moreover, cumulative new home sales have reached 7,875 units as of 3Q 2025, already exceeding 2024’s full-year total of 6,469 units.”

“Resale transactions rose 6.4% q-o-q to 3,881 units, pointing to sustained activity in the resale segment. This reflects resilient market sentiment, despite competing new launches and seasonal factors, such as the Hungry Ghost Festival and September school holidays.”

Chart 1: Breakdown of private home transactions (excluding ECs) by type of sale

“Unsold stock fell 7.9% q-o-q to 17,029 units in 3Q 2025. This comes after the successful launch of eight new projects during the quarter. The strong take-up rates also signal sustained market confidence and have also created a ripple effect, boosting sales momentum in previously launched developments.”

“3Q 2025 saw 1,776 private home completions (excluding ECs), with an additional 1,144 units expected by year-end. Excluding ECs, this would bring the full-year total to 5,249 units for 2025 – which is markedly lower than 2024’s count of 8,460 units.”

Prices

“We saw price momentum picking up in the non-landed segment this quarter, particularly in the CCR, where new project launches helped lift overall price growth.”

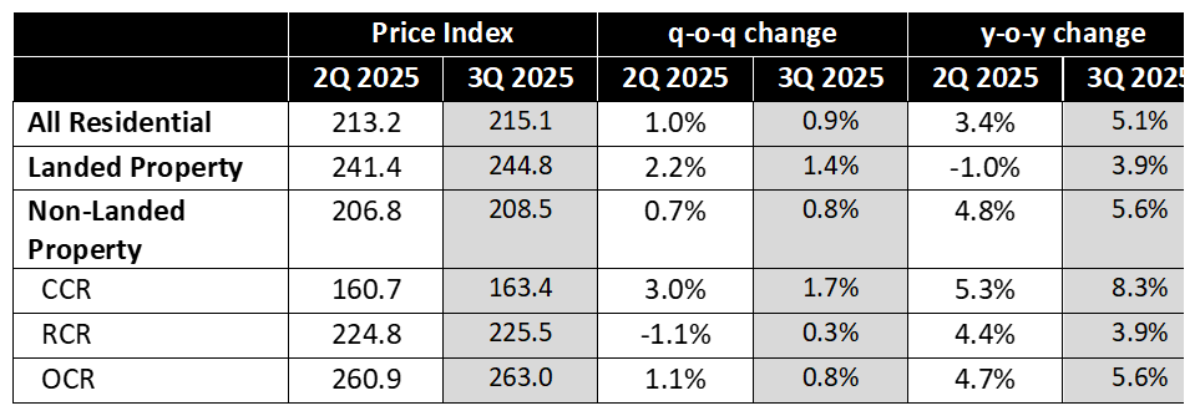

“The All-Residential Private Price Index rose 0.9% q-o-q in 3Q 2025, slightly slower than the 1.0% seen in 2Q 2025. On a year-on-year (y-o-y) basis, the All-Residential Private Price Index rose 5.1%.”

“The Landed price index registered a faster pace of growth by 1.4% q-o-q compared to 2.2% q-o-q growth in 2Q 2025. This marks the third consecutive quarter of price growth for landed homes. Compared to same period last year, landed property prices rose by 3.9%.”

“The Non-Landed Property Price Index registered a faster pace of growth at 0.8% q-o-q in 3Q 2025, compared to the 0.7% q-o-q growth seen in 2Q 2025. On a y-o-y basis, non-landed property prices rose 5.6%.”

“Among the market segments, non-landed homes in the Core Central Region (CCR) recorded the fastest pace of growth at 1.7% q-o-q in 3Q 2025.”

“This was followed by the Outside Central Region (OCR), which grew by 0.8% q-o-q, and the Rest of Central Region (RCR), which saw a 0.3% q-o-q increase in corresponding prices. Non-landed home prices held firm, underpinned by healthy demand for launches across all market segments.”

Table 1: Change in URA Private Property Price Indexes for 2Q 2025 and 3Q 2025

Transaction Volume

New Sales

“In total, developers sold 3,288 new homes in 3Q 2025, representing a 171.3% increase over the 1,212 units last quarter. Developers also launched more homes, totalling 4,191 units, up from 1,520 units in 2Q 2025. These increases coincide with firm buyer interest amid a robust pipeline of new launches in 3Q 2025.”

“Three projects sold above 85% on their launch day, namely Lyndenwoods (94%), River Green (88%) and Springleaf Residence (92%). This can be attributed to pent-up demand as they are in areas that either saw the first ever launch, or first in a long time in their respective estate.”

“Among market segments, the Core Central Region (CCR) saw the strongest rebound in demand, with 903 new homes sold. Notably, this also marks the CCR’s highest quarterly sales since 4Q 2010, when 994 new homes were transacted. This resurgence was fuelled by a string of fresh projects, including The Robertson Opus, UPPERHOUSE at Orchard Boulevard, River Green, and the soft-launched W Residences Marina View.”

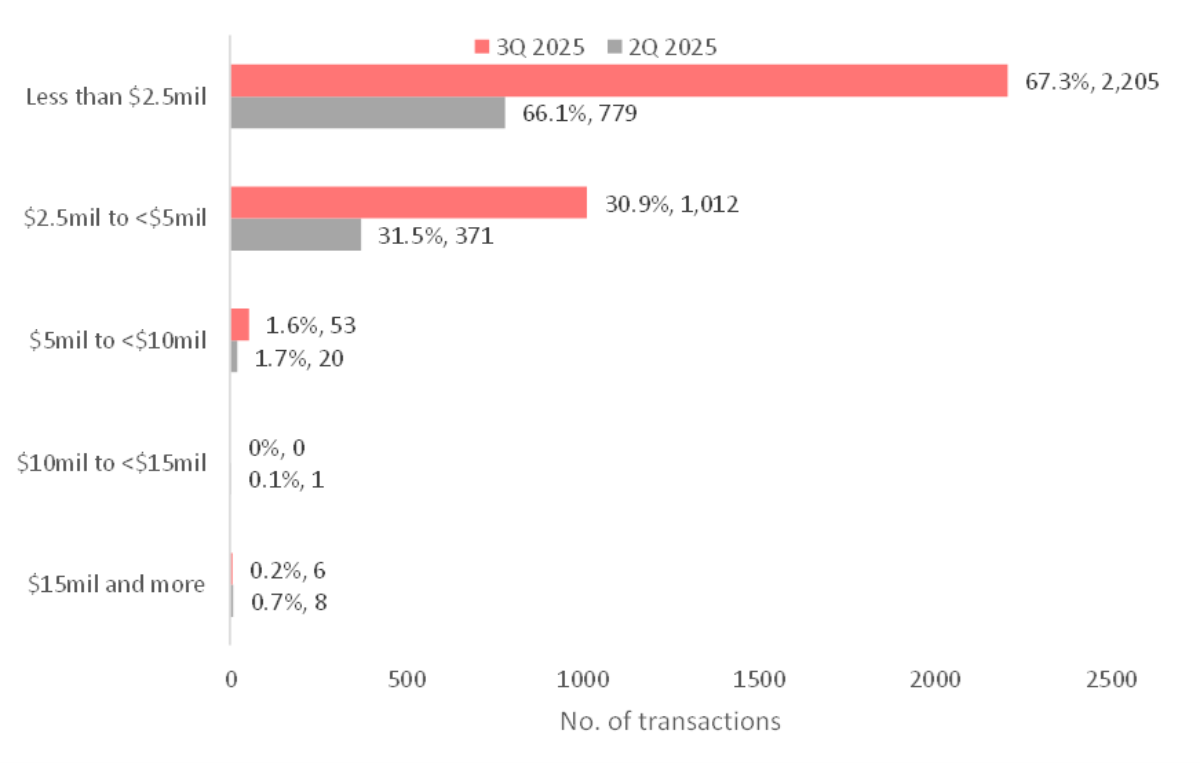

“Similar to last quarter, the majority (67.3%) of new non-landed private home sales were concentrated in the sweet spot range of $2.5 million or less. However, a notable 30.9% of transactions were also in the $2.5 million to $5.0 million range, a result of the high price points of CCR new launches.”

Chart 2: New Non-landed Home Transactions by Price Quantum

“In 3Q 2025, EC transactions more than doubled q-o-q, reaching 571 units compared with just 149 units in 2Q 2025. The jump was mainly driven by the launch of Otto Place at Tengah, where approximately 568 units have been sold to date, accounting for roughly 95% of its total supply.”

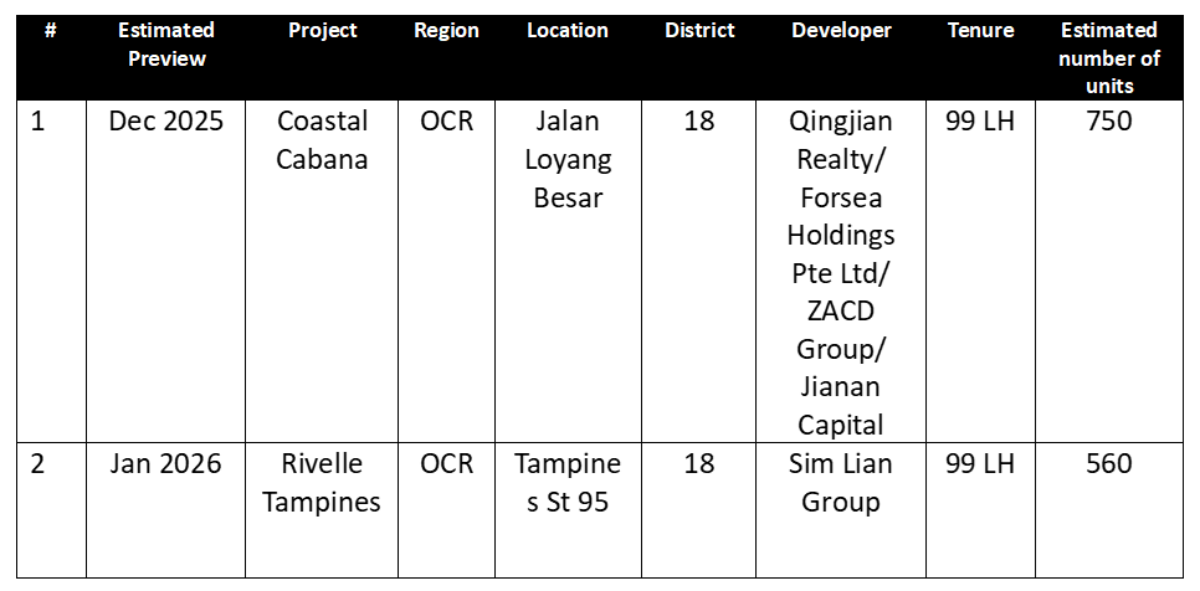

“With the current EC launches completely sold out, buyers will have to wait for the 748-unit Coastal Cabana at Jalan Loyang Besar, set to launch in January 2026.”

Resale & Sub-Sale

“In the resale segment, 3,881 transactions were recorded in 3Q 2025, representing a further 6.4% q-o-q uptick from the 3,647 private homes sold in 2Q 2025. This points towards the resale segment’s continued resilience, despite the challenges posed by competing new launches and seasonal factors, like the Hungry Ghost Festival and September school holidays.”

“Sub-sale transactions slipped further to 235 units in 3Q 2025, down from 269 units in the previous quarter. The pullback was largely due to a smaller pool of private home completions with just 5,249 units by year’s end; this is about 38.0% lower than the 8,460 units completed in 2024.”

Landed

“The landed housing market remained broadly resilient in 3Q 2025, underpinned by steady overall demand despite some signs of slowing momentum in the RCR and OCR. Rising home prices have begun to weigh on affordability, particularly for condominium upgraders, leading to a moderation in sales activity within these regions.”

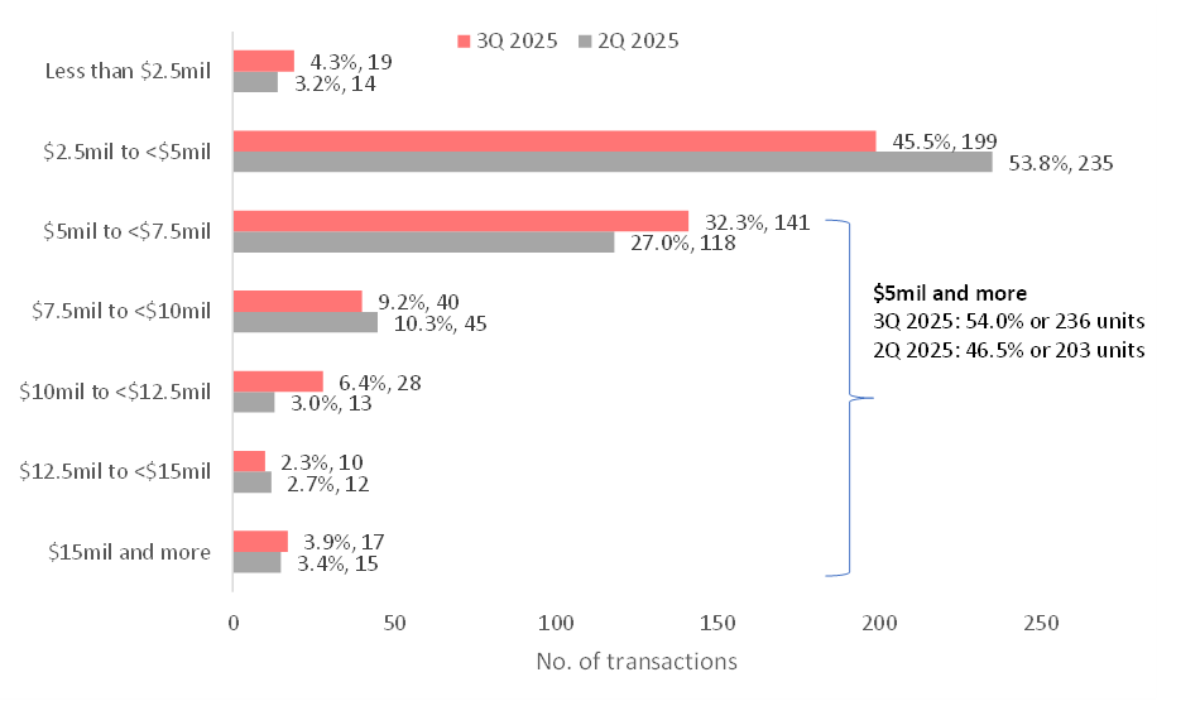

“In contrast, the CCR emerged as a bright spot, with landed transactions almost doubling to 33 units in 3Q 2025 from 18 units in both the previous quarter and a year ago. This resurgence reflects renewed appetite for prime landed properties, which continue to be viewed by high-net-worth individuals as stable, long-term assets offering both capital preservation and appreciation potential.”

Chart 3: Landed Price Quantum 2Q 2025 versus 3Q 2025

Rental

“The All-Residential Rental Price Index saw a 1.2% q-o-q uptick in 3Q 2025, higher than the 0.8% uptick observed last quarter. This growth was led by a 2.4% q-o-q increase in rents for landed properties, whereas overall rents for non-landed properties grew at a more measured pace of 1.1% q-o-q.”

“The limited availability of larger non-landed units for rent has prompted tenants seeking more spacious homes to turn to the landed housing market. Consequently, rents for landed homes have risen 3.5% since 1Q 2025.”

“Meanwhile, the non-landed property rental index rose 1.1% q-o-q in 3Q 2025, surpassing the 0.8% growth in the previous quarter. This movement corresponds with the increase in private home completions in 3Q 2025.

In particular, the OCR saw the completion of Lentor Modern, Sky Eden @ Bedok, and The Arden, while Piccadilly Grand was completed in the RCR. As newly-completed homes tend to achieve higher rental rates, this helped to support overall growth in rents.”

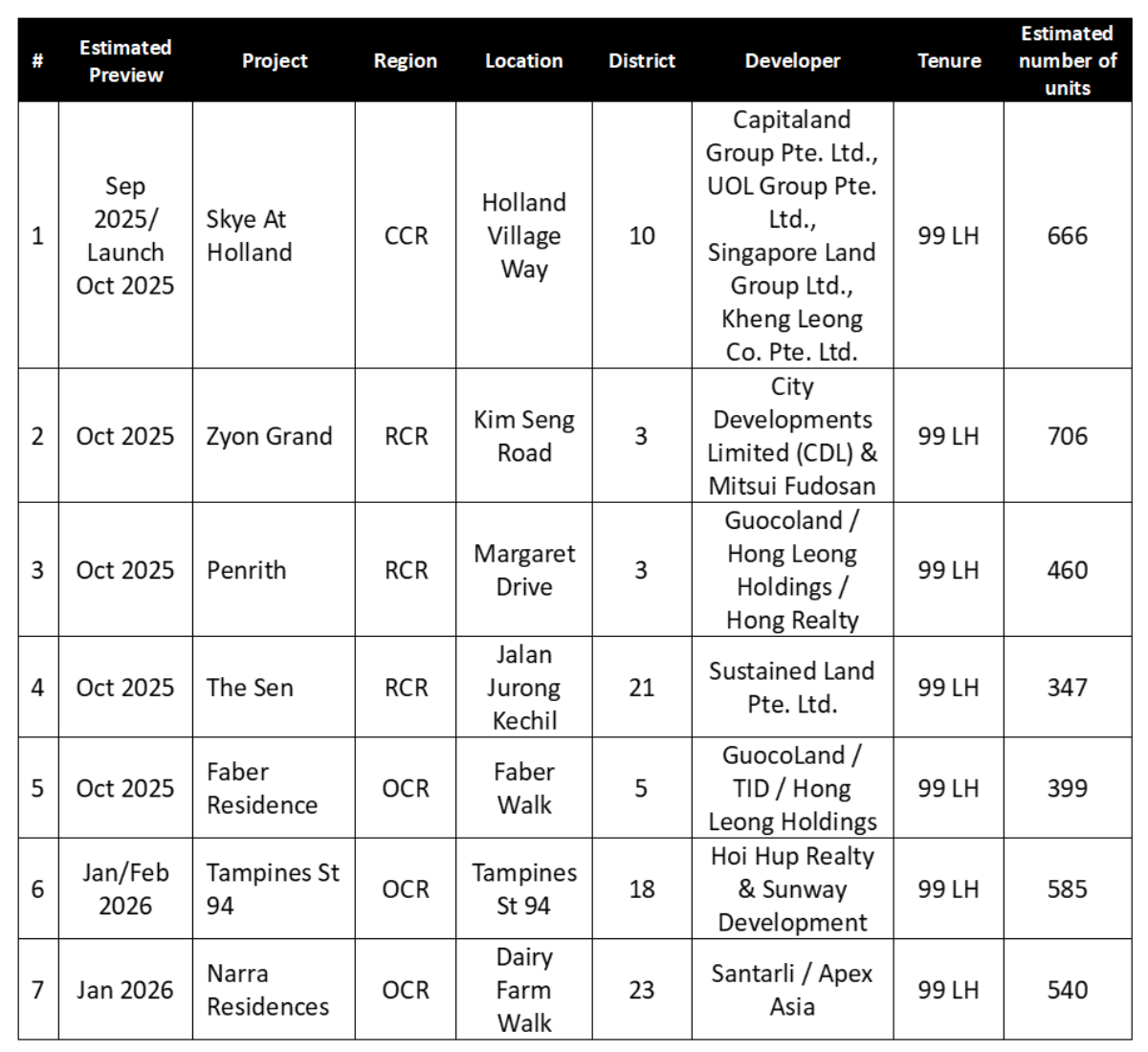

Upcoming Launches

“With five private residential launches introducing 2,578 new units in 4Q 2025, new homebuying activity is expected to stay firm. With most upcoming projects located in the RCR, pricing momentum in the segment could strengthen further. New launches along the RCR-CCR border are also likely to establish new pricing benchmarks, owing to their desirability.”

“The sales momentum from 3Q 2025 carried into 4Q 2025. At present, three projects have been launched and saw stellar launch day performance. Skye at Holland has emerged as the standout launch of 2025, selling 99% of its 666 units during its October debut. This was followed by Penrith (97%) and Faber Residence (86%) underscoring buyers’ firm belief of properties being a safe asset amid global uncertainty.”

Table 2: New Home Launches in 4Q 2025 and 1Q 2026

Table 3: Executive Condominium

Outlook

“The upward revision of Singapore’s 2025 GDP forecast from 0–2% to 1.5–2.5%, along with the low-interest rate environment has boosted consumer confidence, supporting homebuying demand in 3Q 2025.”

“While resale and sub-sale activity in the secondary market is expected to moderate further amid limited completions, a strong pipeline of new launches is likely to draw buyer attention to the primary market in 4Q 2025.”

“Looking ahead, buyer interest in private homes is expected to remain strong – supported by a combination of low interest rates, an attractive pipeline of new launches, and positive economic sentiment despite lingering global uncertainties.”

“Barring any unforeseen circumstances, ERA Singapore has revised our new home sales forecast upwards - from the earlier projection of 8,500-9,500, to over 10,000 units for the whole of 2025. This would mark the highest annual new home sales volume since 2021.

In tandem, sub-sale and resale transactions are expected to reach 1,100-1,300 units and 14,000-15,000 units respectively by the end of 2025.”

For media enquiries, please contact:

Lisha Rodney

Public Relations Manager, ERA Singapore

Email: [email protected]

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.