4Q 2025 URA Real Estate Statistics: Private Home Demand Momentum Carries From 3Q 2025, Sets Firm Outlook for 2026

- ERA Singapore

- 11 min read

- PressRelease

- 23 Jan 2026

SINGAPORE, 23 January 2026 – “According to the Urban Redevelopment Authority (URA), private home prices rose by 0.6% quarter-on-quarter (q-o-q) in 4Q 2025, extending the steady pace of growth comparable to the previous quarterly increase of 0.9%.

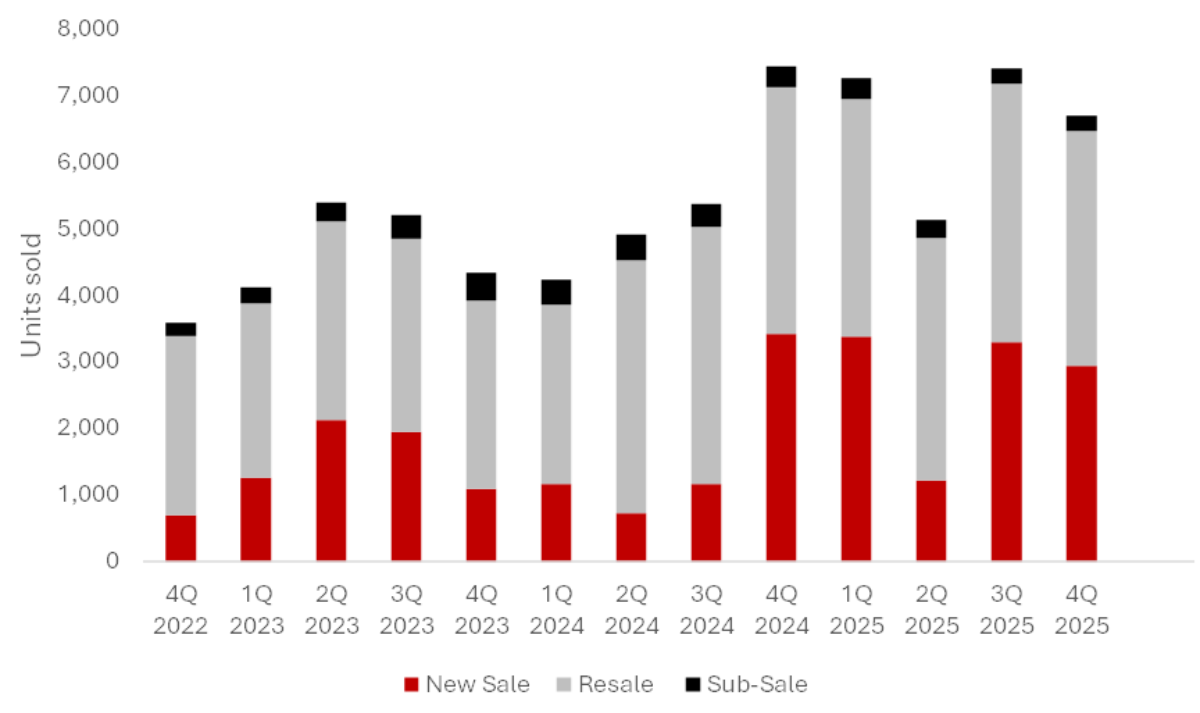

The total volume of private home transactions in 4Q 2025 fell by 9.5% to 6,699 units. This comes after a strong 3Q 2025 showing, which was supported by a surge in new supply from eight project launches. The softer performance in 4Q 2025 was largely due to a reduced launch pipeline and the typical year-end seasonal slowdown. Nonetheless, overall market activity remained resilient, with total private home sales for the full year reaching 26,492 units.”

“Following the bumper slate of new launches that propelled private property price growth in 3Q 2025, this momentum carried into 4Q, largely underpinned by strong new home sales, with 2,940 units sold during the quarter. Overall, the primary market delivered a stellar performance in 2025, with 10,815 units sold, marking the best performing year since 2021,” said Marcus Chu, Chief Executive Officer, ERA Singapore.

“Despite heightened uncertainty earlier in 2025, including the Liberation Day announcement that briefly dampened sentiment in April, confidence recovered swiftly as Singapore proved largely insulated from tariff-related risks. Stronger-than-expected economic performance in 3Q 2025, alongside low unemployment and easing inflation, reinforced buyers’ sense of stability.”

“Some buyers may have chosen to enter the market before 2026 comes, anticipating that new home prices will see another wave of increase in line with the recent upward trajectory of land prices.”

“With an additional 4,575 private residential units in the 1H 2026 GLS Confirmed List, the fresh supply will continue to reinforce the Government’s aim to stabilise land prices and maintain a steady flow of new homes over the coming years. This is in line with efforts to maintain a stable and sustainable property market.”

“Resale and sub-sale transactions fell to 3,529 units (9.1% q-o-q fall) and to 230 units (2.1% q-o-q fall) in 4Q 2025, respectively. This comes as supply completions fell to just 6,123 units in 2025, prompting buyers towards the new home market.”

Chart 1: Breakdown of private home transactions (excluding ECs) by type of sale

“Unsold stock fell 5.2% q-o-q to 16,193 units in 4Q 2025. This comes after the successful launch of eight new projects during the quarter. The strong take-up rates also signal sustained market confidence and have also created a ripple effect, boosting sales momentum in previously launched developments.

4Q 2025 saw 2,018 private home completions (excluding ECs). Excluding ECs, this would bring the full-year total to 6,123 units for 2025, which is markedly lower than 2024’s count of 8,460 units.”

Prices

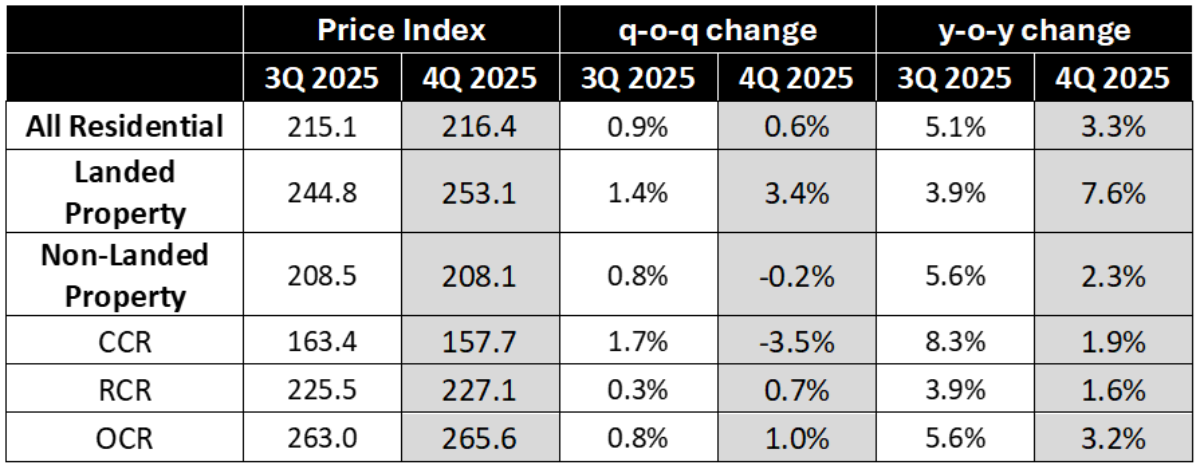

“The All-Residential Private Price Index rose 0.6% q-o-q in 4Q 2025. Although slightly slower than the 0.9% seen in 3Q 2025. It still marked the fifth consecutive quarter of price growth. On a year-on-year (y-o-y) basis, the All-Residential Private Price Index rose 3.3%, with growth mainly driven by the landed housing segment.

We saw price momentum fall marginally by 0.2% for non-landed homes in 4Q 2025, after the 0.8% growth seen in the previous quarter. This comes after just five new launches in 4Q 2025, compared to eight in 3Q that resulted in the uplift.

In 4Q 2025, the Landed Property Price Index registered a faster pace of growth by 3.4% q-o-q, compared to 1.4% q-o-q growth in 3Q 2025. This marks the fourth consecutive quarter of price growth for landed homes. Compared to the same period last year, landed property prices rose by 7.7%, significantly higher than the 0.9% seen in 2024. With rising non-landed prices, some condo owners may have taken the opportunity to upgrade to a landed home.

Among the market segments, non-landed homes in the Outside Central Region (OCR) recorded the fastest pace of growth, rising 1.0% q-o-q in 4Q 2025. This followed the strong performance of Faber Residence, the sole new OCR launch during the quarter, which sold 363 of its 391 units (91.0%) in 4Q 2025.

The Rest of Central Region (RCR) also saw prices inch up 0.7% q-o-q in 4Q 2025, carrying the momentum of the 0.3% rise in 3Q 2025. This comes after the strong take-up rates of the three RCR launches – Zyon Grand, The Sen and Penrith. Cumulatively, 1,138 of the 1,515 units were sold in 4Q 2025.

In contrast, the Core Central Region (CCR) saw a reversal after four consecutive quarters of price growth. Prices fell 3.5% q-o-q in 4Q 2025, with fewer CCR homes being transacted. Just 1,475 non-landed CCR homes were sold in 4Q 2025, down 10.1% from the 1,640 sold in 3Q 2025. This comes despite the stellar performance of Skye at Holland, selling out all but six units.”

Table 1: Change in URA Private Property Price Indexes for 3Q 2025 and 4Q 2025

Transaction Volume

New Sales

“In total, developers sold 2,940 new homes in 4Q 2025, representing a 10.6% decline over 3,288 units last quarter. Developers also launched fewer homes, totalling 2,632 units, down from 4,191 units in 3Q 2025. Amid the smaller pipeline of new launches in 4Q 2025, buyers’ interest was still firm, signalling the strength of Singapore’s new home market.

Carrying the momentum from 3Q 2025, when three projects sold above 80% on their launch day, we saw a similar trend in 4Q 2025. Four of the five launches in 4Q 2025 achieved take-up rates of over 80% on their respective launch days. The tighter supply, arising from fewer new home completions in 2025, led to spillover demand into the primary market. In addition, easing interest rates and rising HDB prices have strengthened buyers’ financial capacity to enter the private residential market. As a result, strong sales momentum is likely to carry into 2026.

The strong market conditions in 3Q 2025 gave buyers the confidence to commit to higher-valued homes, including those in the Central Region, despite higher prices. At the same time, rising new home prices and strong take-up rates in other regions made city-fringe and central locations increasingly compelling. This helped drive the strong performance of projects such as Skye at Holland, Penrith and Zyon Grand.

Buyers who were unable to get their choice during the launches in 3Q 2025 could have also turned to projects launched in 4Q 2025."

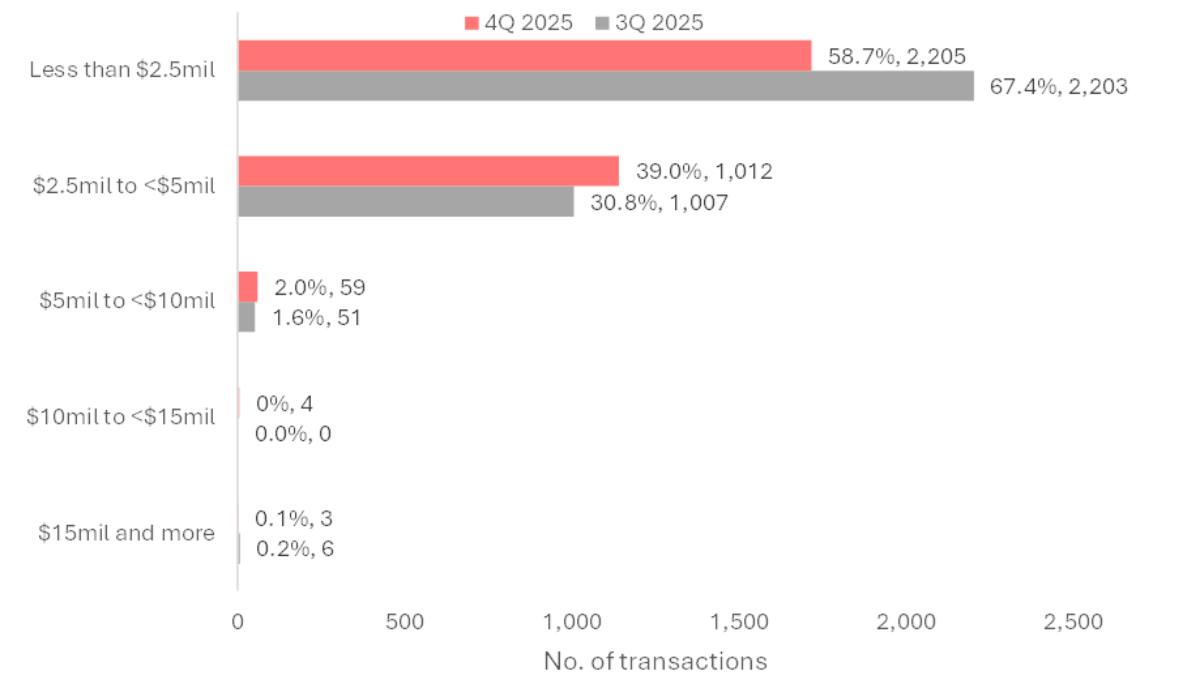

Chart 2: New Non-landed Home Transactions by Price Quantum

“With no new EC launches in 4Q 2025, new EC sales fell to just 80 units, down 86.0% q-o-q. Since then, prior to the launch of Coastal Cabana, all new ECs had been fully sold out. Although Rivelle Tampines is expected to launch in 1Q 2025, overall EC supply is expected to remain tight, with another three projects only slated for launch in 4Q 2025.”

Resale & Sub Sale

“In the resale segment, 3,529 transactions were recorded in 4Q 2025, representing a 9.1% q-o-q uptick from the 3,881 private homes sold in 3Q 2025. Despite this dip, resale transactions in 2025 stand at 14,622, which have remained largely similar to 2024, when there were 14,053 transactions. This points towards the resale segment’s continued resilience, despite the challenges posed by competing new launches and seasonal factors like the December school holidays.

Sub-sale transactions slipped further to 230 units in 4Q 2025, down from 235 units in the previous quarter. The pullback was largely due to a smaller pool of private home completions with just 6,123 units (excluding ECs) in 2025; this is about 38.0% lower than the 8,460 units completed in 2024.”

Landed

“The landed housing market remained broadly resilient in 4Q 2025, underpinned by steady overall demand from condominium upgraders. Rising non-landed home prices have enabled them to upgrade, leading to an increase of 3.4% in prices.

Based on caveats, landed home transactions rose 4.0% q-o-q to 491 transactions in 4Q 2025. This brings 2025’s total to 1,852 transactions, 11.2% more than the whole of 2024.

The OCR and RCR saw an increase in the number of landed transactions, reversing the trend of 3Q 2025. Buyers could have looked at homes further from the city centre, as they balanced between their locational preference, spatial needs and affordability.

In contrast, the CCR saw fewer transactions due to higher prices, as buyers and sellers faced an impasse on prices. CCR landed home sellers, typically with higher holding power, are less inclined to reduce their prices.

Landed homes continue to be viewed highly by local high-net-worth individuals due to their stability, offering both long-term capital preservation and appreciation potential.”

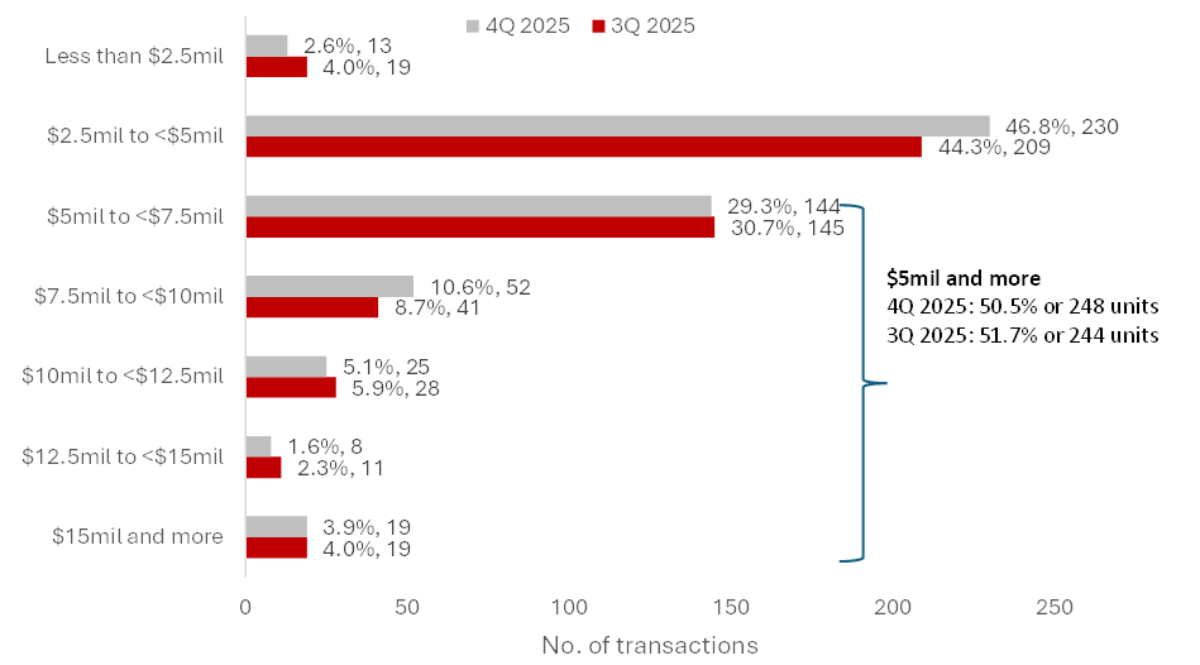

Chart 3: Landed Price Quantum 3Q 2025 versus 4Q 2025

Rental

“The All-Residential Rental Price Index saw a 0.5% q-o-q downtick in 4Q 2025, which reverses the 1.2% q-o-q uptick observed last quarter. Overall rents for non-landed properties also inched down by 0.1% q-o-q in the same period, while landed property rents saw a steeper decline of 3.0% q-o-q. Overall, private property rents continue to be on the uptrend, rising 1.9% in 2025.”

Among market segments, only the CCR and RCR saw a quarterly lift in rents in 4Q 2025. This could have been due to recent completions in both regions that helped boost rental activity, such as One Bernam and Midtown in the CCR, as well as Picadilly Grand in the RCR.

The recent extension of the temporary occupancy cap on rental properties, coupled with a growing supply pipeline, is expected to keep rent growth in check. In 2026, non-landed private home completions are also slated to hit 6,083 units, with a further 8,757 units forecasted for 2027 (excluding ECs). With this fresh supply, tenants may expect to see more stable rents for the foreseeable future.”

Upcoming Launches

“2026 kicked off with the successful launch of Coastal Cabana EC. Since its launch on 17 January 2026, more than two-thirds of units have been sold. We will see the launch of two more private developments in January 2026 - Newport Residences and Narra Residences. These three developments, yielding 1,534 units, cater to different buyer profiles. There could be similar interests in the new home market as seen in 2025.

For the whole of 2026, 19 new private residential developments, comprising about 9,852 units, and five Executive Condominium (EC) projects with around 1,972 units, are expected to be launched. These projects are spread across all regions and will offer a diverse range of product types, catering to varying buyer needs, including affordability considerations and locational preferences.”

Table 2: New Home Launches in 1Q 2026

Market Outlook

“The dip in transactions in 4Q 2025 was largely due to the stellar performance seen in 3Q 2025 and the seasonal year-end lull. Developers typically postpone launches in December, when buyers travel during the holiday season. This moderation does not signal a softening market, but rather reflects a seasonal pause.

2025 was a strong year for Singapore’s private residential market, underpinned by resilient demand, steady economic conditions and renewed confidence as global risks eased. Attention now turns to how far this momentum can be sustained into 2026.

In 2026, the private residential market is expected to remain resilient, with moderate price growth supported by strong owner-occupier demand and ongoing right-sizing trends. Buyers can expect a pipeline of 19 private residential projects and 5 EC launches this year. While this is fewer than 2025, which saw 24 private developments and 2 EC launches, overall homebuying demand is expected to remain healthy.

Barring any unforeseen circumstances, ERA Singapore projects new home sales to be between 9,000 and 10,000 units, while the secondary market is expected to record 13,000 and 14,000 transactions, pointing to stable underlying demand in the year ahead.”

For media enquiries, please contact:

Lisha Rodney

Public Relations Manager, ERA Singapore

Email: [email protected]

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.