1Q 2026 Rental Report: Private Residential Rents See Modest Recovery Amid Bump Up in Leasing Activity

- Stanley Lim

- 5 min read

- Research

- 25 May 2026

Private Residential Rental Market

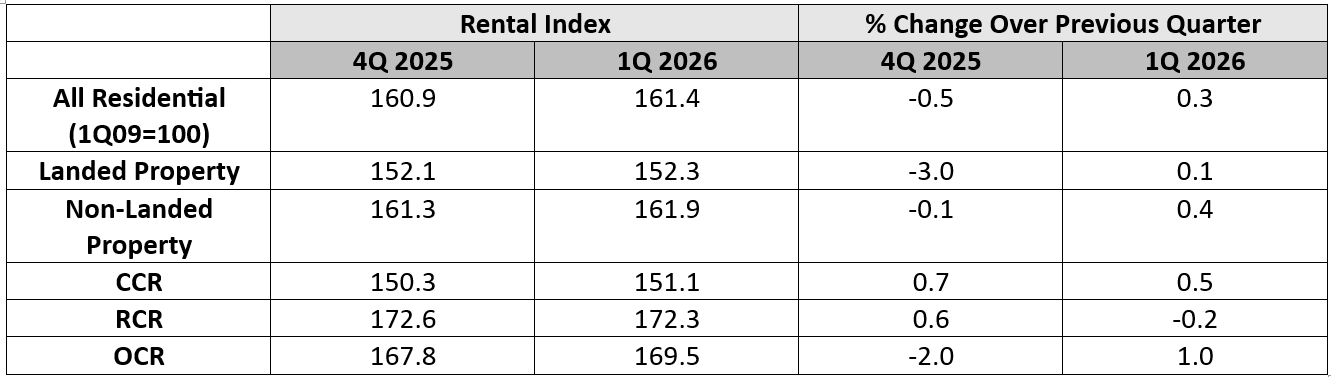

In the first quarter of 2026, Singapore’s private residential rental market, including Executive Condominiums (EC), experienced a slight increase in rents and leasing activity. The rental index for private residential properties went up by 0.3% quarter-on-quarter (q-o-q) to 161.4, partly recovering from the 0.5% q-o-q decline seen in the previous quarter. Compared to the same period last year, this indicates a 1.8% year-on-year (y-o-y) rise in islandwide rentals for private residential properties.

Table 1: Comparison of Private Property Rental Index for 4Q 2025 and 1Q 2026

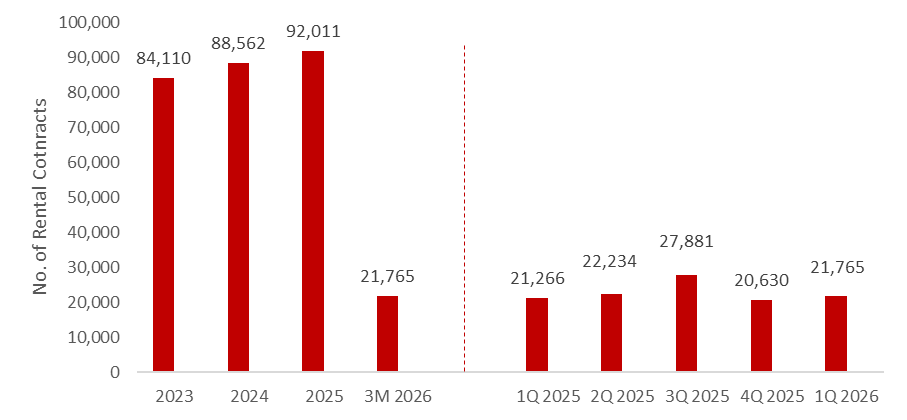

Leasing activity in the private residential sector also increased this quarter. As of 19 May 2026, URA data shows that the total rental volume for 1Q 2026 across landed homes, non-landed private properties, and ECs amounted to 21,765 contracts. In 4Q 2025, there were 20,630 rental contracts signed islandwide for these property types.

Amid increased leasing activity, the rental index for non-landed private properties grew by 0.4% this quarter. This offset the 0.1% decline in 4Q 2025, though the increase is modest and consistent with the sub-1% quarterly gains seen throughout most of last year.

Chart 1: Rental Contracts Across Landed, Non-Landed Private Properties and Executive Condominiums (Year and Quarter)

Leasing volumes for private properties and ECs increased by 5.5% quarter-on-quarter in 1Q 2026, indicating a solid recovery after the typical slowdown during the holiday season. Year-on-year, this reflects a modest 2.3% growth from the 21,266 rental contracts in 1Q 2025.

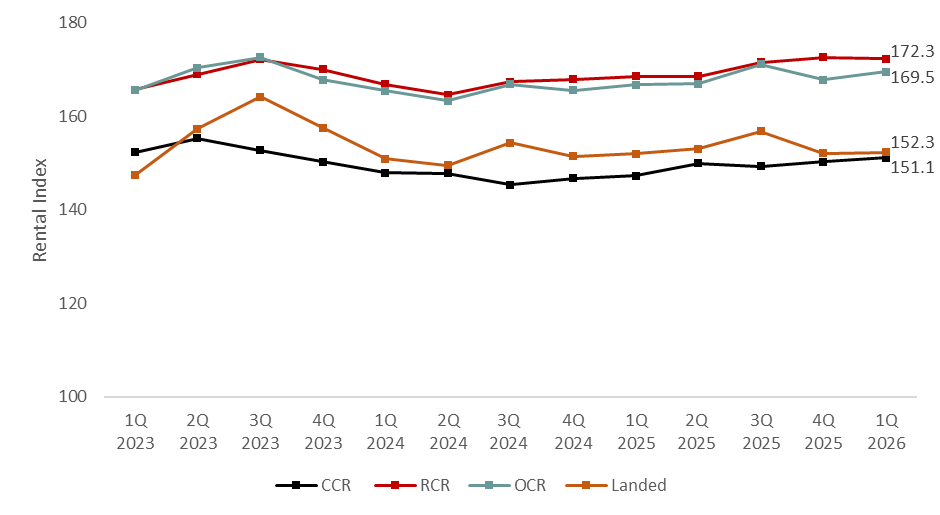

Chart 2: Rental Index of Non-Landed Private Properties (By Region) and Landed Properties

In the non-landed private property segment, the Outside Central Region (OCR) experienced the largest rent growth in 1Q 2026, increasing by 1% quarter-on-quarter to 169.5. The Core Central Region (CCR) also saw rents rise slightly by 0.5% quarter-on-quarter to 151.1. Meanwhile, the Rest of Central Region (RCR) experienced a small decline, decreasing by 0.2% quarter-on-quarter to 172.3.

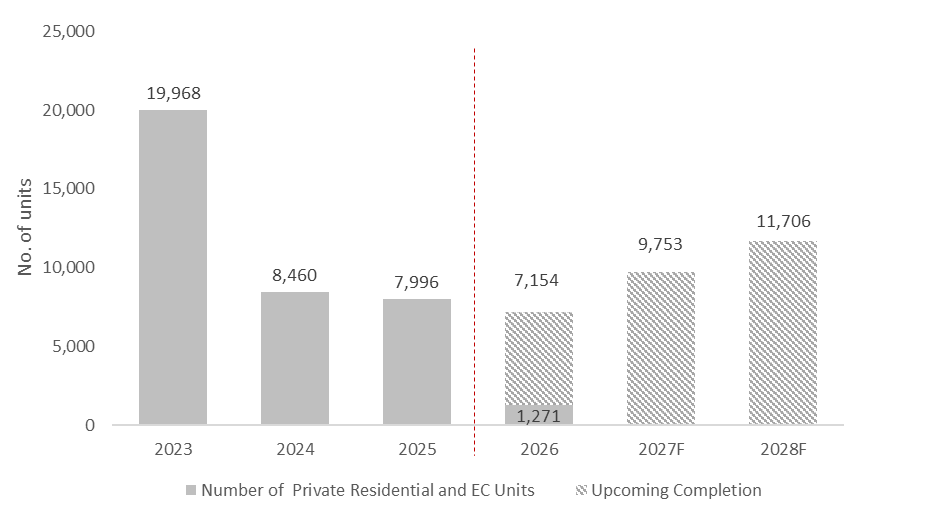

Chart 3: Private Residential and EC Completions and Expected Pipeline Supply

Alongside the overall rise in rents, private residential completions (including ECs) reached 1,271 units in 1Q 2026. This reduced number of completions, down from 2,018 units in 4Q 2025, probably contributed to the modest increase in rents during the same period.

Table 3: Projects Completed in 1Q 2026

Notable non-landed private residential projects completed in 1Q 2026 include Sceneca Residence and The Botany at Dairy Farm. Located in the OCR, these two developments total 654 units, contributing to a total of 424,165 private homes by the end of the quarter.

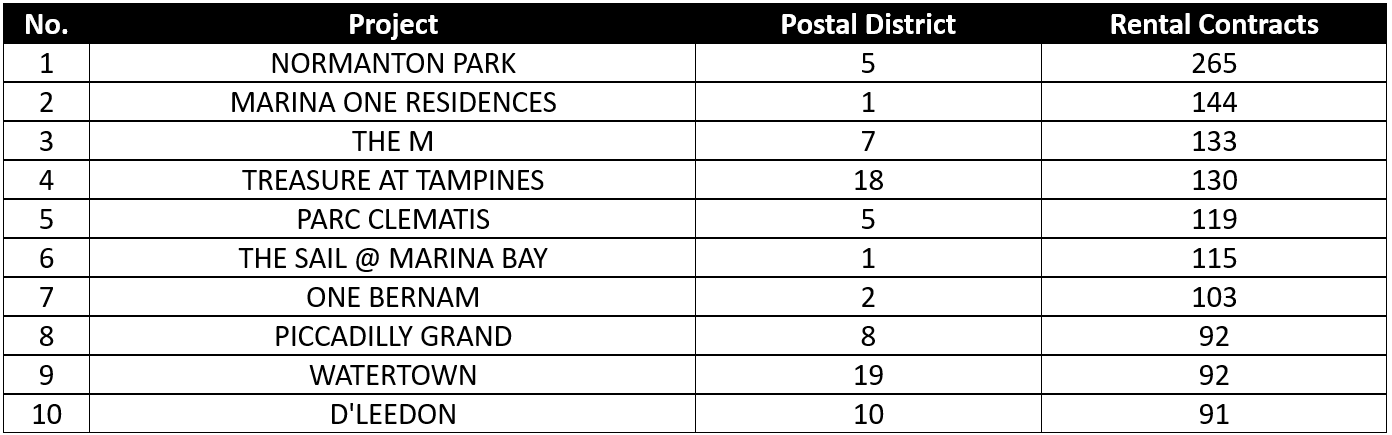

Table 4: Top 10 Non-Landed Private Projects Ranked by Rental Contracts

Normanton Park led non-landed private projects in rental activity, with 265 contracts in 1Q 2026. It is the second straight quarter since 4Q 2025 that Normanton Park has recorded the most rental contracts, indicating robust demand due to its close proximity to major tenant hubs at One-North, the National University of Singapore, and Singapore Science Park.

The next most popular rental developments were Marina One Residences and The M, which recorded 144 and 133 rental contracts, respectively, over the quarter.

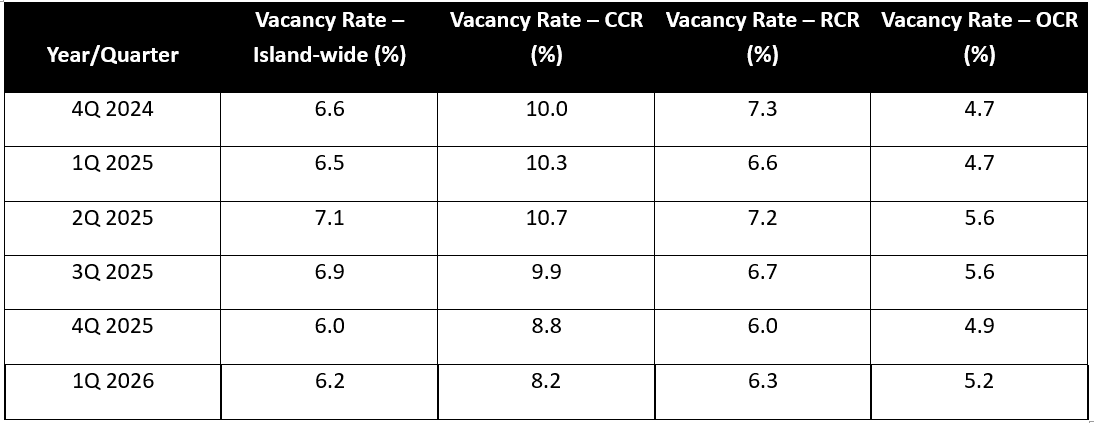

Table 5: Vacancy Rate of Private Residential Properties by Quarter and Market Segment

Vacancy rates varied across regions, with only the OCR and RCR experiencing increases during the quarter. In contrast, the CCR saw its vacancy rate decrease from 8.8% in 4Q 2025 to 8.2% in 1Q 2026. This variation may be due to recent new completions in the OCR and RCR, where the influx of supply has outpaced private home rental demand.

HDB Rental Market

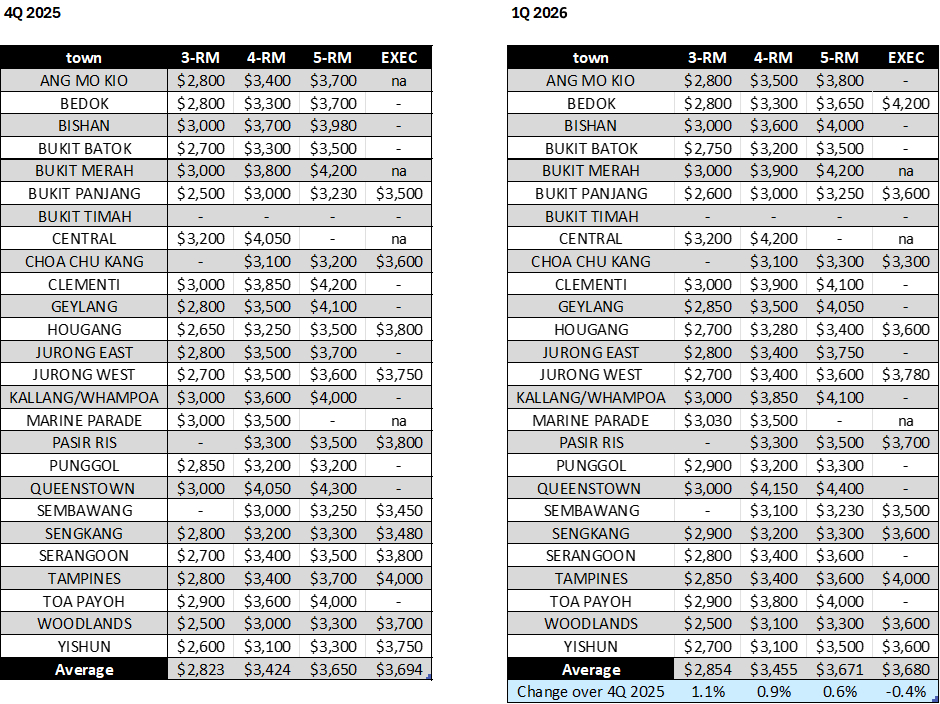

In the first quarter of 2026, median rents for HDB flats increased across most room types. Specifically, rents for 3-room, 4-room, and 5-room flats rose by 1.1%, 0.9%, and 0.6% quarter-over-quarter, respectively, while rents for Executive flats decreased by 0.4%.

Table 6: HDB median rents by town and q-o-q growth

(-) Indicates that there are no rental transactions in the quarter

* Indicates that the median rent is not shown because there are fewer than 20 rental transactions in the quarter for that particular town and flat type

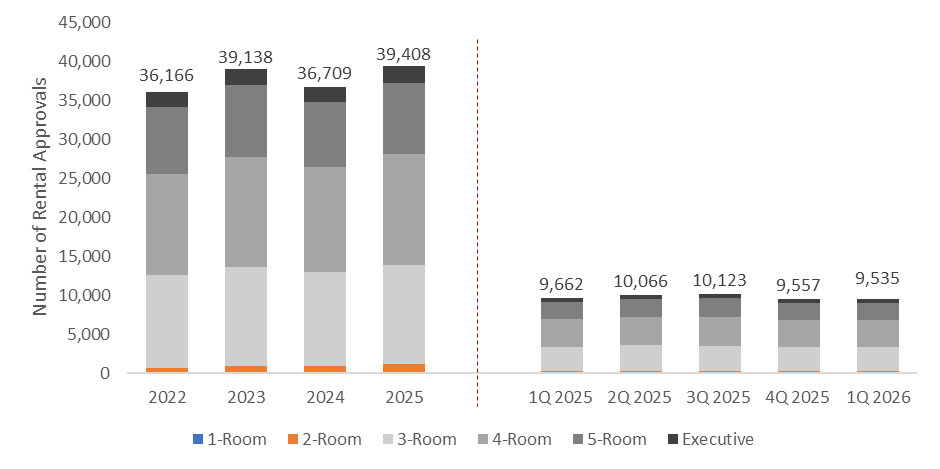

The number of approved HDB rental applications stayed relatively steady across different quarters. In 1Q 2026, there were 9,535 rental approvals, which is a slight decrease of 0.2% compared to 4Q 2025.

Chart 4: Number of rental approvals for HDBs

Resilience expected for Singapore’s rental market in 2026, even amidst growing tenant caution

Singapore’s residential rental market stayed generally healthy in the first quarter of 2026, with stable or rising rents and leasing activity in both HDB and private housing. Nevertheless, the modest rise in these figures may indicate increasing caution among renters, who are coping with a more uncertain global economy and possible job market volatility.

The main factors driving local housing demand continue to hold steady. According to the Ministry of Manpower, Singapore’s labour market expanded in 1Q 2026, marking the 18th straight quarter of employment growth since late 2021. Unemployment and retrenchment rates have stayed relatively stable, even as employers have become more cautious in hiring. These factors collectively sustain strong demand in the rental market, despite tenants being more mindful of costs.

Considering these prevailing conditions, ERA forecasts that rents for private homes (excluding ECs) may rise by 1% to 3% year-over-year in 2026, with the number of annual rental contracts reaching approximately 88,000 to 93,000 by the end of the year.

In the HDB segment, median rents are expected to rise by 2% to 6% year-over-year in 2026, with rental approvals potentially hitting 34,000 to 36,000 cases within that period.

I confirm that I have read theprivacy policy and allow my information to be shared with this agent who may contact me later.