1Q 2026 URA Private Residential Report: Fall in transactions after a high number of launches in 2H 2025

- Egan Mah and Ethan Hariyono

- 12 min read

- Research

- 1 Apr 2026

Figures are based on the official flash estimates for URA quarterly statistics, released on 1 April 2026.

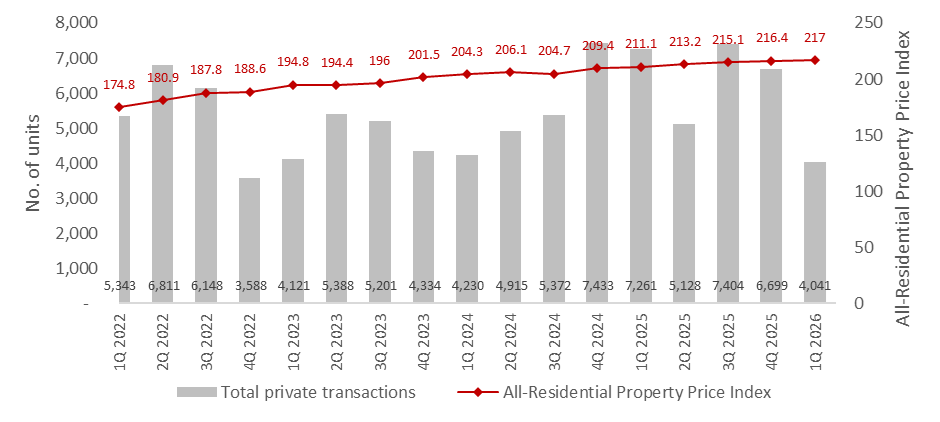

According to flash estimates released by URA for 1Q 2026, the All-Residential Property Price Index rose modestly by 0.3% quarter-on-quarter. Total private home transactions declined by 39.7% q-o-q to 4,041 units, from 6,699 units in 4Q 2025.

Chart 1: All-Residential Property Price Index and Total Private Transaction Volume

The overall non-landed private property price index rose by 1.0% quarter-on-quarter to 210.2 in 1Q 2026, reversing the 0.2% decline in 4Q 2025. This is driven by non-landed prices in the Outside Central Region (OCR).

- Prices in the OCR continued to rise, increasing by a sharp 1.0% q-o-q, while the Rest of Central Region (RCR) recorded a 0.9% increase.

- The Core Central Region (CCR) experienced a slight increase of 0.4% due to the two launches, Newport Residences and River Modern, that performed well despite new benchmark prices.

- Landed property prices reversed the 3.4% quarter-on-quarter increase in 4Q 2025. This quarter saw a 1.8% decrease as transactions fell.

However, as buyers shifted their focus to new launches, resale and sub-sale activities in the secondary market slowed down during the quarter.

With an extra 4,575 private residential units added to the 1H 2026 GLS Confirmed List, the new supply will help the Government pursue its goal of stabilising land prices and ensuring a consistent pipeline of new homes in the upcoming years. Developers still show a strong interest in acquiring sites. In the four GLS sites that closed in 1Q 2026, each attracted an average of 4.8 bidders.

Private home prices remained broadly stable in 1Q 2026, even as transaction volumes pulled back sharply. This reflects a market that is consolidating following the strong launch-driven momentum in the second half of 2025. The moderation in activity was largely due to seasonal factors and a tighter launch pipeline, which limited immediate buying opportunities.

The decline in volumes was mainly due to seasonal factors and supply constraints. With fewer new launches in the quarter, buyers faced limited immediate choices, resulting in a natural decrease in transactions.

At the same time, demand remained focused on new launches. Projects that entered the market continued to attract strong interest, pulling buyers away from the resale and sub-sale sectors, which experienced softer activity.

The divergence between regions also reflects shifting buyer preferences. Demand in the OCR and RCR remains resilient, supported by HDB upgraders and owner-occupiers, while the CCR is more sensitive to launch timing and pricing benchmarks.

Looking ahead, transaction volumes are expected to rebound alongside a healthier pipeline of launches. With underlying demand still strong and economic fundamentals resilient, price growth is projected to stay gradual and sustainable throughout the year.

New Sale (Non-Landed Homes, Excluding ECs)

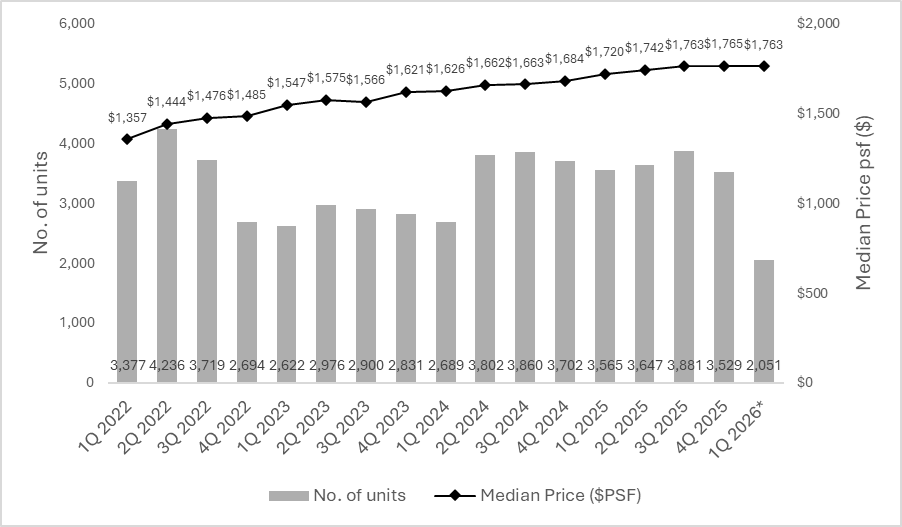

According to caveats as of 26 March 2026, new sale transactions declined by 60.0% quarter-on-quarter to 1,294 (excluding EC) units in 1Q 2026. The slowdown was mainly due to a smaller launch pipeline, with only six developments launched during the quarter, including two ECs.

Despite the decline in volumes, underlying demand remained firm, with projects continuing to attract strong take-up rates. Projects entering the market continued to attract substantial interest, reflecting sustained buyer confidence despite global uncertainty. This has contributed to the slight increase in price index of 0.3% despite muted transaction quantity in reference to the previous quarter.

Chart 2: New Sale Transactions and Median Price for Non-Landed Homes (excluding ECs)

*Based on flash estimates

Notably, half of the launches in 1Q 2026 achieved take-up rates of at least 90% at launch. This highlights the strong demand in Singapore’s housing market, especially for well-located and competitively priced developments.

The performance also highlights an important trend. Buyers today are more selective, but remain highly decisive when a project meets their expectations on pricing, location, and product quality

Although there is a slight increase in new home completions in 2026, total completions will still be 30% below the 10-year average for the decade. This shortfall has caused spillover demand into the primary market. Additionally, lower interest rates and rising HDB prices have boosted buyers’ financial ability to purchase private residential properties. Consequently, strong sales momentum is expected to continue into 2026.

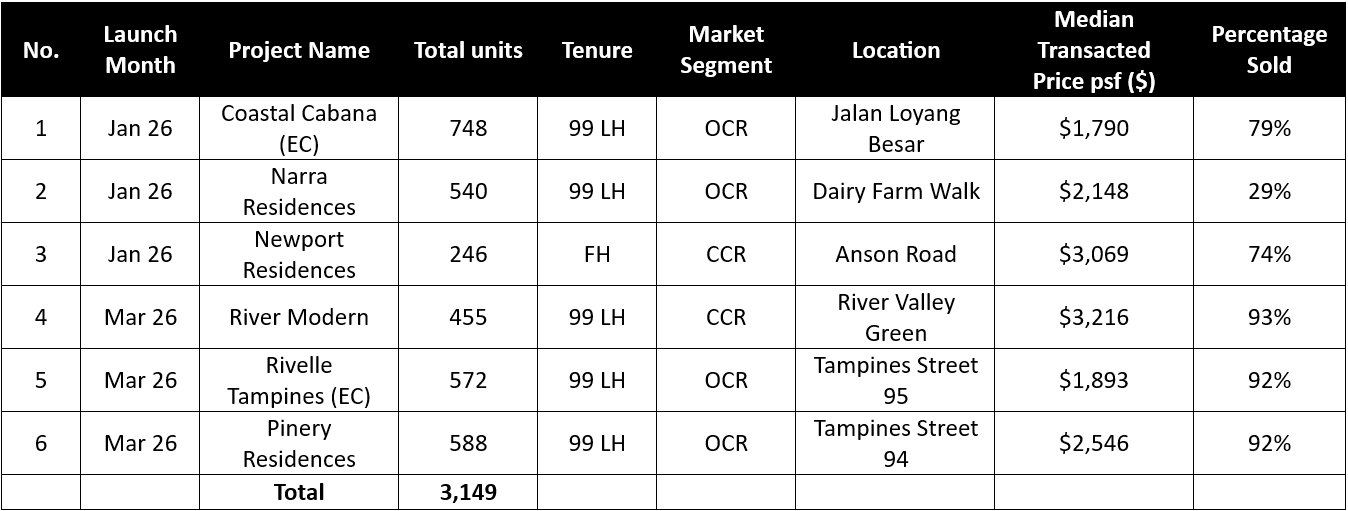

Table 1: List of new launches in 1Q 2026

Core Central Region (CCR)

CCR prices increased by 0.4% in 1Q 2026, reversing the 3.5% decline from the previous quarter. This is largely due to the strong sales performance of the two CCR launches in the first quarter, with Newport Residences and River Modern achieving take-up rates of 74% and 92% so far.

Compared to 2025, the CCR market segment is expected to see lower new-home supply this year. With only about 1,465 CCR units scheduled to be launched in 2026, nearly half of that supply was already introduced in the first quarter. This early rollout of launches provided price support for the CCR segment.

River Modern’s robust sales performance, selling 93% of its units in the quarter, highlights the sustained appeal of well-positioned CCR developments. Its high demand reflects interest from upgraders and young families looking for family-friendly layouts, integrated commercial spaces, MRT access, and proximity to good schools, balancing liveability with investment value in a prime District 09 location.

The project’s higher median price of $3,216 psf, compared to $2,949 psf at Skye at Holland in the previous quarter, also lifted overall CCR price benchmarks.

Rest of Central Region (RCR)

Despite no new launches in the RCR in 1Q 2026, prices still increased by 0.9%. This is despite new sales transactions in the RCR falling 76.6% to 357 transactions.

With new OCR launches entering the market at benchmark prices, previously launched RCR projects have become comparatively more attractive to buyers. For instance, 99-year leasehold projects such as Bloomsbury Residences and Pinetree Hill both sold 36 units each, at a median of $2,549 psf and $2,571 psf respectively, lower than the RCR median of $2,672 psf.

In District 15, where no new launches are expected in 2026, buyers have also been drawn to remaining inventory at developments such as The Continuum, Arina East Residences and Grand Dunman. Against the backdrop of rising OCR price benchmarks in the East, these projects present a relative value proposition, supporting steady absorption and underpinning price resilience within the RCR segment.

Outside of Central Region (OCR)

1Q 2026 saw two OCR launches, marking a relatively cautious start to the year. The OCR continues to be supported by a strong upgrader pool, particularly from HDB owners unlocking significant housing equity.

OCR projects are attractive due to their affordability and closeness to established HDB estates. Most buyers favour upgrading within the same town, attracted by familiarity, available amenities, and community connections.

Among the launches, Pinery Residences was the top performer, with over 92% take-up at launch. This highlights the strong demand for well-sited OCR developments in mature estates.

Its success was driven by a compelling value proposition - a mixed-use development with direct MRT access, located in Tampines, one of Singapore’s most established regional centres. Such attributes continue to resonate strongly with young families and owner-occupiers. The strong take-up was also supported by healthy growth.

HDB resale activity in Tampines included 88 million-dollar flat transactions and 2,660 MOP flats in 2025 and 2026. With a large supply of recently MOP-ed flats and a steady stream of million-dollar transactions, many upgraders are entering the market with significant housing equity.

Looking ahead, OCR price growth is expected to remain resilient. With nearly two-thirds of upcoming launches concentrated in this segment, projects in established estates such as Serangoon, Bishan and Bedok are likely to see healthy demand, supported by strong connectivity, amenities and a deep upgrader pool.

Executive Condominium (EC)

1Q 2026 saw the launch of two EC projects, Rivelle Tampines and Coastal Cabana in Pasir Ris, both of which were met with strong demand. As the final EC launches in the East for the foreseeable pipeline, buyers moved decisively, with the two projects launched in the quarter tallying a total of 1,133 units to date.”

The strong demand underscores the enduring appeal of ECs as a more affordable option for accessing private housing. Despite rising prices, ECs still offer a substantial price difference from private condominiums, attracting HDB upgraders. Schemes such as the Deferred Payment Scheme and CPF Housing Grants enhance affordability, aiding buyers in managing initial costs and securing a new home more easily.

Rivelle Tampines’ 92% take-up at launch highlights the significant pent-up demand, especially in mature estates where new EC supply is scarce. Moving forward, the next phase of EC launches will mainly be in the North and West, with no immediate plans for supply in the East. This geographical change underscores the limited EC options in mature eastern estates, which have been a key factor driving demand in recent launches.

Resale and Sub-Sale (Non-Landed Homes, Excluding EC)

In the first quarter of 2026, resale transactions for non-landed private homes (excluding ECs) declined by 41.9% quarter-on-quarter to 2,051 units, according to URA caveats. This is the lowest level since the second quarter of 2020 and represents a departure from the stable pattern of approximately 3,000 resale units per quarter seen over the previous seven quarters.

Buyer interest moved away from the resale market mainly because of the surge in new home launches in sought-after locations, giving buyers more options. Additionally, there were fewer new home completions in 2025, leading to a reduced supply of resale homes.

Chart 3: Resale Transactions and Median Price for Non-Landed Homes (excluding ECs)

Source: URA as of 26 March 2026, ERA Research and Market Intelligence *Based on flash estimates and caveats

Despite a decline in transaction volume, median unit prices for resale non-landed private properties (excluding ECs) stayed almost unchanged, slightly decreasing to $1,763 psf in 4Q 2025 from $1,765 psf in the previous quarter. This indicates that resale home prices have remained stable over recent quarters, as buyers have shifted focus to the new sale market.

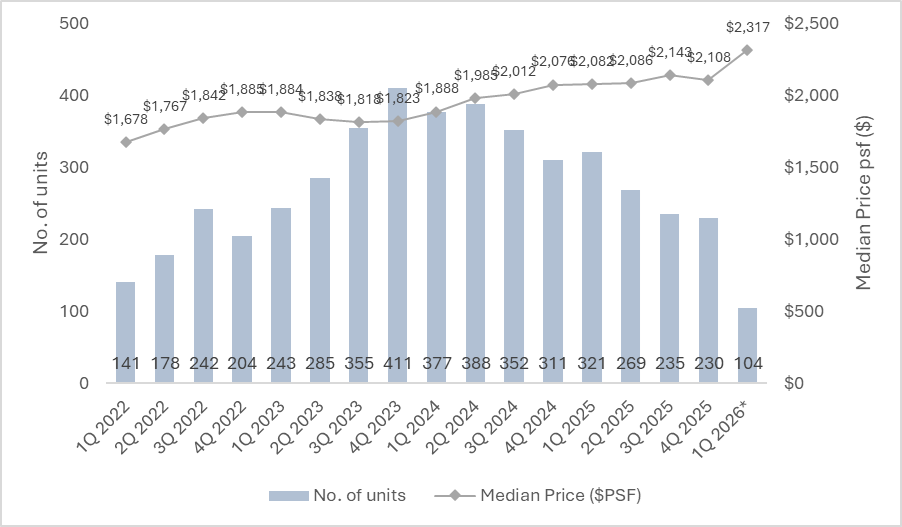

Chart 5: Sub-Sale Transactions and Median Price for Non-Landed Homes (excluding ECs)

Within the sub-sale segment, transaction volumes dropped sharply by 54.8% quarter-on-quarter to 104 deals, according to caveat data. This represents 3.0% of all non-landed private property deals (excluding ECs) in 1Q 2026. Although sub-sale transactions have generally declined, the 104 deals were the fewest in a quarter since 1Q 2021.

On the other hand, the median unit price for sub-sales increased by 9.9% quarter-on-quarter to $2,317 psf. Although only 12.5% of transactions occurred in the CCR, which generally commands higher prices, 2025 saw the completion of seven integrated developments. These projects are residential units directly linked to malls and MRT stations. Among those completed are Lentor Modern, Woodleigh Residences, Pasir Ris 8, and Sengkang Grand Residences. Such developments often command a premium due to their added convenience and accessibility for residents. With 30.8% of subsale transactions involving integrated developments, median subsale prices experienced an uplift.

Nonetheless, with many new CCR launches since 2H 2025, buyers of CCR properties have turned towards new launches instead of subsale units due to their attractive prices and longer remaining tenures.

Market Outlook

Based on the 1Q 2026 flash estimates, overall private property prices increased by 0.3%. It remains on track to reach ERA’s earlier forecast of 3% to 5%.

As geopolitical tensions escalate globally, stability may be further challenged by conflicts involving Israel, Iran, and the United States, heightening concerns about economic instability. So far, oil prices have risen, and financial markets have shown volatility. If supply disruptions persist, this could result in higher costs for energy, construction, and living expenses.

Singapore is recognized as a safe haven amid global uncertainties thanks to stable governance, a strong Singapore Dollar, and a resilient property market. Despite global market challenges, the residential property sector in Singapore maintains a predominantly optimistic outlook for the near future. Over time, Singapore has built a reputation as a leading wealth hub in the region, with its real estate regarded as a high-quality asset that provides steady rental income for investors.

The country is experiencing a significant increase in wealth transfer, mainly driven by a wealthy middle class whose assets have risen rapidly due to increasing property values. With an aging population, this transfer is expected to speed up. Although this influx of capital will benefit future generations financially, it may also widen the societal wealth gap. As tensions in the Middle East escalate, more wealth transfers and investments could flow into Singapore.

With Singaporeans' strong belief in real estate investment, much of the expected increase in wealth transfer will likely benefit this market. We already see this as older homeowners downsize to unlock housing equity for liquidity, and younger buyers receive parental support for property acquisitions. Consequently, this flow of capital will sustain long-term demand and price growth across Singapore's residential market.

In 2026, the private residential market is expected to remain resilient, supported by moderate price growth driven by strong owner-occupier demand and ongoing right-sizing trends. Healthy take-up rates from recent project launches reinforce this positive outlook. This underlying demand has also encouraged developers to commit to new projects, suggesting that the development pipeline and future housing supply will continue to be supported by strong market fundamentals.

Buyers can also look forward to a pipeline of 18 private residential projects, including one landed project, and 5 EC launches this year. Barring any unforeseen circumstances, ERA Singapore projects new home sales to be between 9,000 and 10,000 units, while the secondary market is expected to record 13,000 to 14,000 transactions, indicating stable underlying demand in the year ahead.

Table 2: Upcoming launches in 2Q 2026

I confirm that I have read theprivacy policy and allow my information to be shared with this agent who may contact me later.