2Q 2025 Rental Report: Private Home Rents Poised to Stabilise After Mild Correction; Rental Take-Up Rates Inch Up

- kwongseongping

- 7 min read

- Research

- 1 Sep 2025

Private residential rentals rose for the second straight quarter in 2Q 2025, underpinned by new home completions that expanded rental supply, particularly in the Core Central Region (CCR).

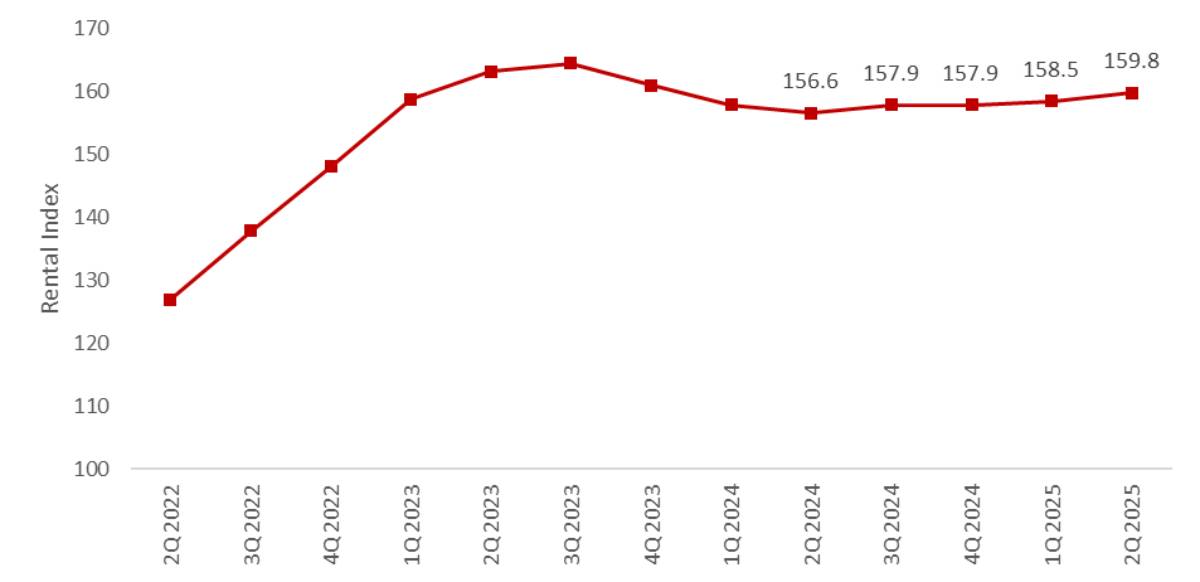

Private residential rents rose, led by growth in the CCR & Landed segments.

The Private Residential property rental index increased to 159.8, indicating a slight 0.8% quarter-on-quarter (q-o-q) and 2.0% year-on-year (y-o-y) growth. Rents across the island rose more rapidly compared to 1Q 2024, mainly driven by higher rental growth for non-landed properties in the CCR non-landed sector, as well as landed properties across all market segments.

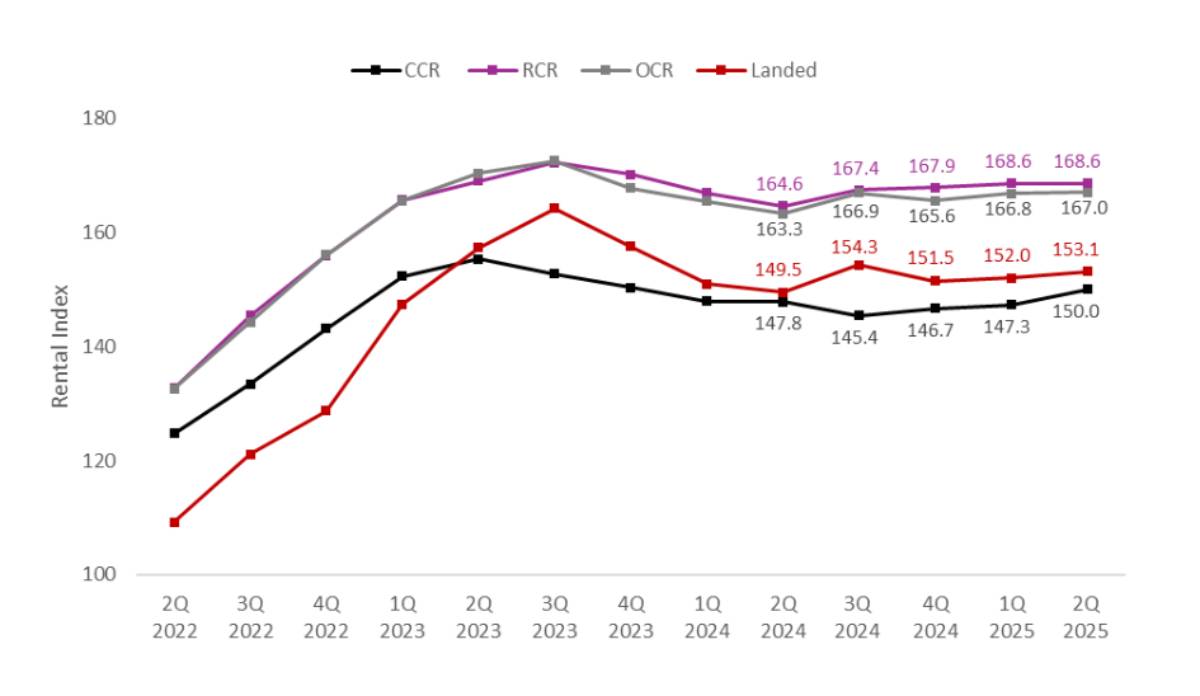

The non-landed CCR index increased by 1.8% quarter-on-quarter in 2Q 2025, driven by higher rental transactions at newly completed projects such as Midtown Bay and One Holland Village Residences. Meanwhile, the Rest of Central Region (RCR) and Outside Central Region (OCR) remained largely unchanged, with growth of 0.0% and 0.1% quarter-on-quarter, respectively.

Separately, landed properties experienced a quicker rate of rental growth at 0.7% quarter-on-quarter, driven by increasing demand for larger spaces and the narrowing price gap between landed homes and larger condominium units.

Chart 1: Rental Index of Private Residential Properties

Chart 2: Rental Index of Private Residential Properties by Market Segment

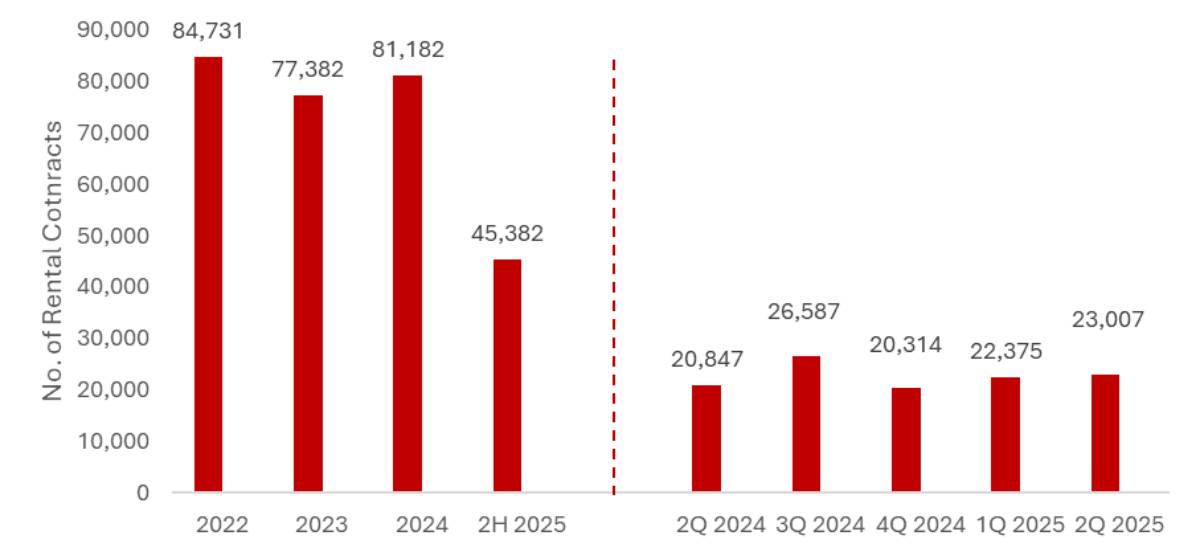

Marginal uptick in rental contracts, along with more rental supply

The increase in rental prices also aligns with the upward trend observed for private residential rental contracts since 4Q 2024. This quarter, a total of 23,007 rental agreements were signed, showing a 2.8% quarter-on-quarter rise and a 10.4% year-on-year increase. The increase in rental agreements may mainly be due to the new completions of private residential homes in 2H 2024 and 1Q 2025, which were subsequently introduced into the rental market.

Chart 3: Private residential rental contracts

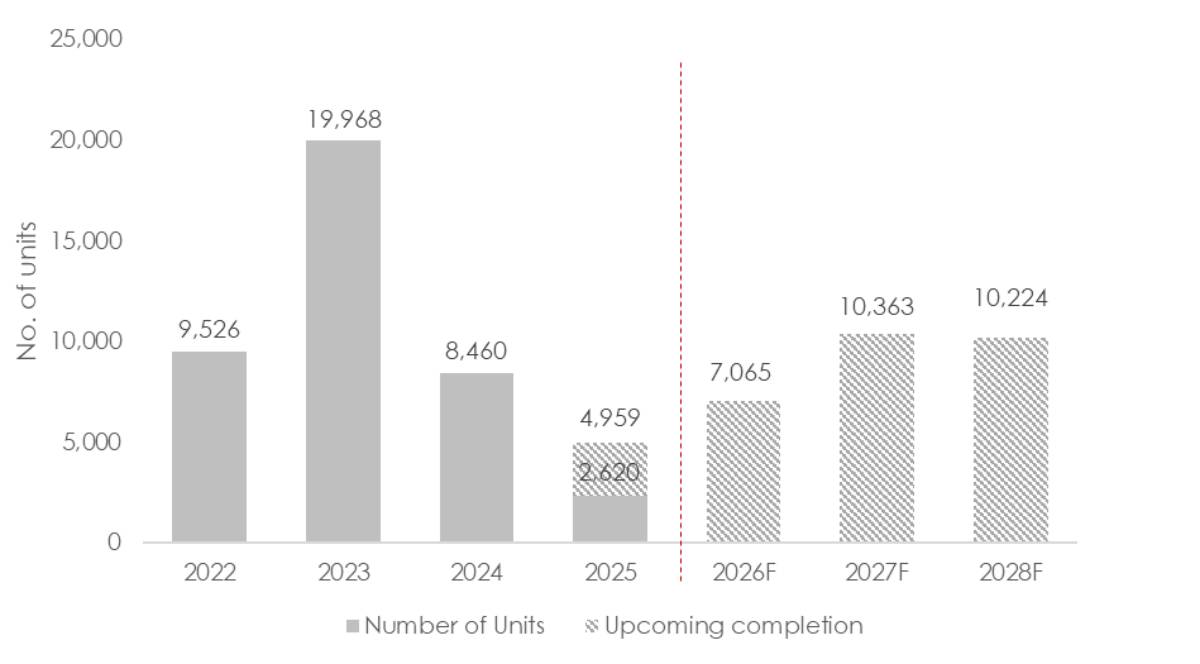

New Private Homes Completion in Prime District Supports CCR Rental Growth

In 2Q 2025, only 341 private homes were completed. This marks an 82.8% decline from 1Q 2025, which saw a total of 1,988 private home completions. This significant reduction in supply is likely to push rental prices higher in the coming months, leading to slow and steady growth in the short to medium term.

New private home completions are expected to decline further, with only 2,620 units forecast in 2H 2025, which could continue to support rental growth in the private residential sector. An estimated 4,959 non-landed private homes are expected to reach their Temporary Occupation Period (TOP) in 2025. This figure is significantly lower than the 8,460 non-landed private home completions during the same period in 2024.

The notable decline in completions this quarter is expected to exert upward pressure on private home rents, likely resulting in a gradual rise towards the end of the year.

Midtown Modern (558 units), completed in 1Q 2025, contributed to an increase in new units on the market. Owners of these recently completed units are seeking higher rental rates. Projects in prime districts not only boost the supply of rentable units but also put upward pressure on rents in the CCR. Since new units usually command premium rental rates, this has led to the CCR experiencing the highest growth in median rental across all market segments this quarter.

Chart 4: Private residential completions (excluding EC)

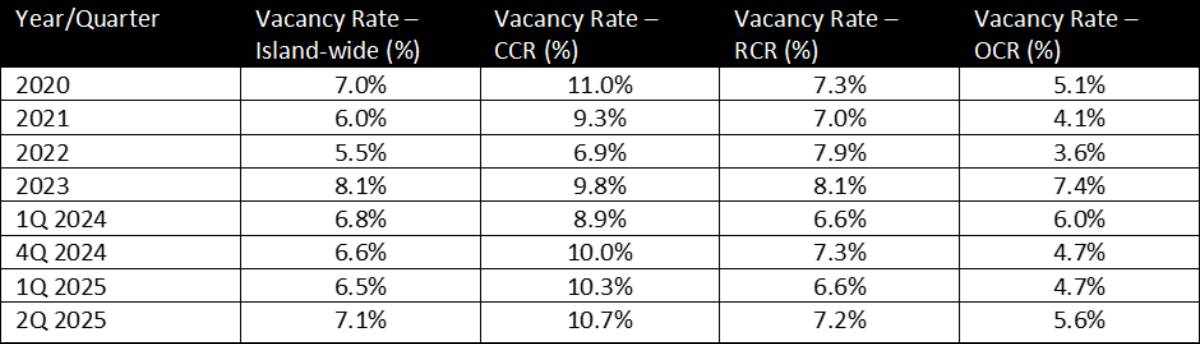

Higher Vacancy rates across market segments may be a short-term correction

The vacancy rate across all market segments of completed private residential properties increased to 7.1%, up from 6.5% quarter-on-quarter. Vacancy rates for private homes in the CCR, RCR, and OCR grew by 10.7%, 7.2%, and 5.6% quarter-on-quarter, respectively. Despite the relatively few completions in 2Q 2025 (341 units) compared with 1,988 units in 1Q 2025, vacancy rates continued to rise this quarter. This indicates that the increase in vacancy rates may be temporary and is likely to slow down in the near future.

Since 4Q 2025, islandwide rents have increased by 1.2%, with a total of 45,382 rental contracts. For 2H 2025, we maintain our forecast for islandwide rents at 3% – 5% as the market continues to adjust to increased supply. With rental contracts already exceeding expectations, ERA is revising its initial forecast for private home rental contracts from 80,000 to 85,000 and then to 88,000 to 95,000 for 2025.

Table 1: Historical vacancy rate of completed private residential properties by market segment

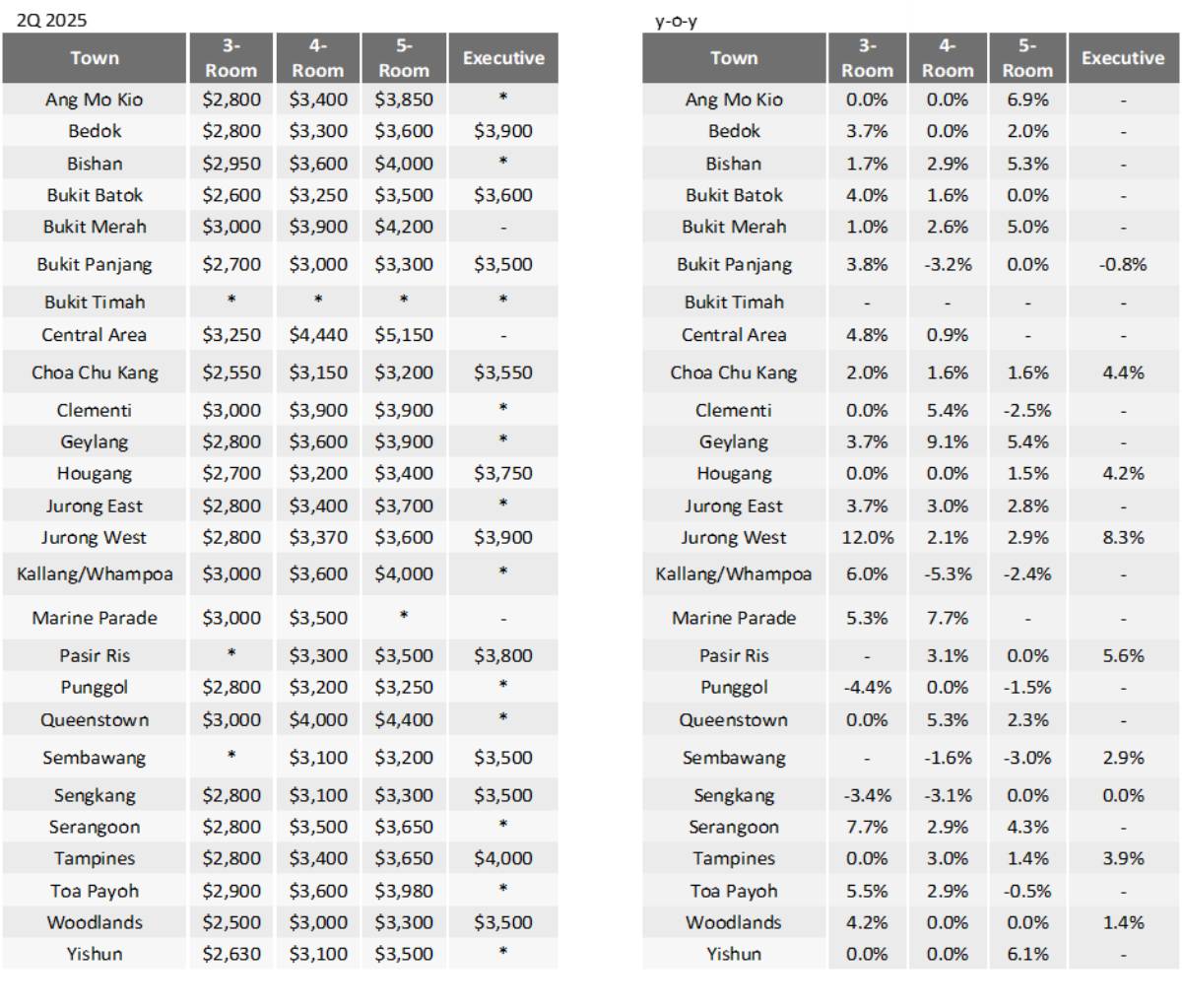

Median HDB rents continue to increase across all towns in 2Q 2025

In 2Q 2025, median rents for HDB flats increased across all room sizes. On average, median rents for 3-, 4-, and 5-room flats rose slightly by 2.7%, 1.6%, and 1.6% year-on-year, respectively. The highest annual growth in rental was seen in executive flats at 3.3%. This rise was mainly driven by a 3.3% increase in rents for executive flats.

Limited new supply in the private rental market has caused some tenants to turn to HDB rentals as an alternative, putting upward pressure on rents. These tenants typically have a higher budget and are often willing to pay a premium for well-located or desirable units.

The combined impact of higher demand for HDB flats and limited supply in the private rental market has led to a modest increase in HDB rents. Despite this rise, HDB flats continue to be the most affordable housing option for prospective tenants.

Table 2: 2Q 2025 HDB median rents by town and y-o-y growth

* Indicates that the median rent is not shown because there are fewer than 20 rental transactions in the quarter for that particular town and flat type

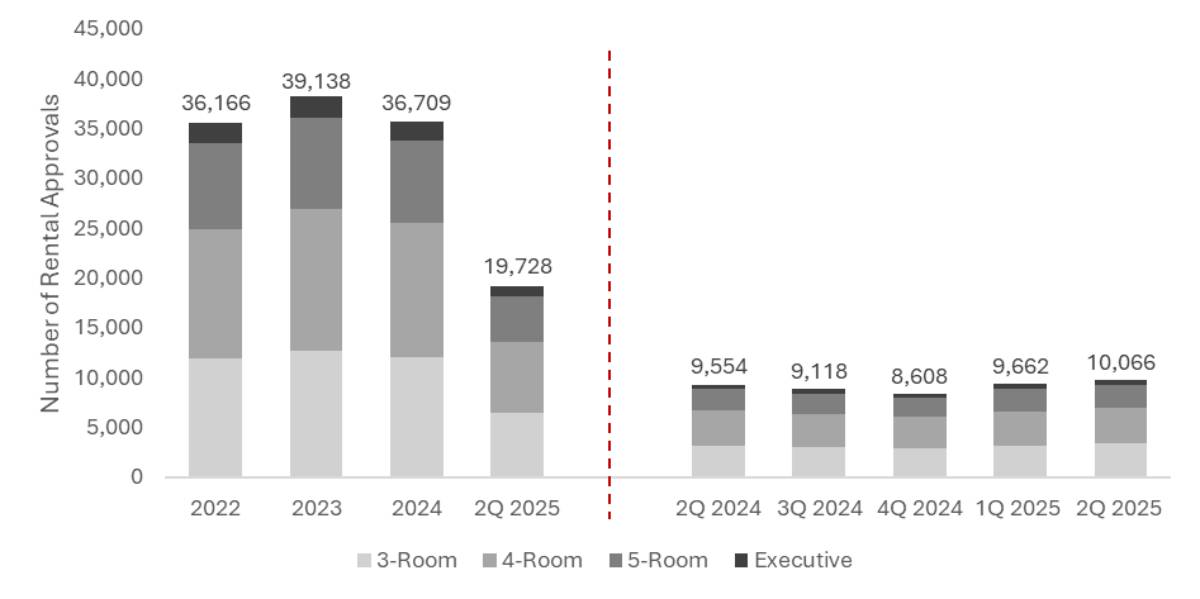

In 2Q 2025, 10,066 HDB flats were rented out, marking a 5.4% increase from the 9,662 units leased in the same period last year.

Chart 5: Number of rental approvals for HDBs

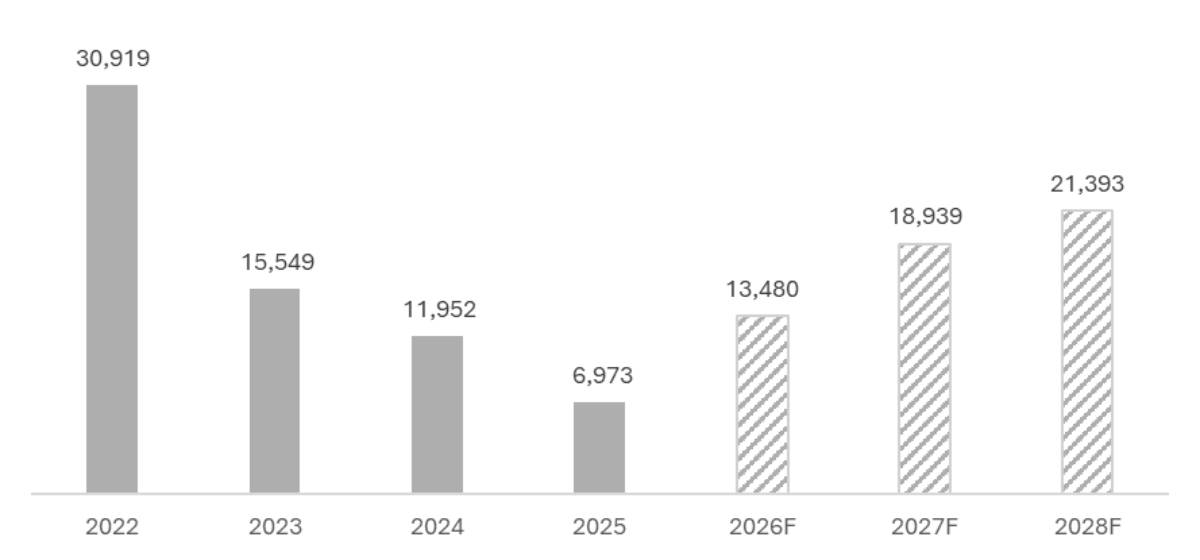

Rental Growth Amid Fewer Flats Reaching Minimum Occupation Period in 2025

In 2025, an estimated total of 6,973 HDB flats are expected to reach the end of their Minimum Occupation Period (MOP). This represents a significant 41.7% decrease from 2024 (11,952 MOP units) and is the lowest number of MOP flats since 2015, when only 8,443 flats reached MOP. This also continues a decline from the peak of 30,919 MOP flats recorded in 2022. The reduced overall flat supply has led to increased rental rates.

Chart 6: No. of HDB flats achieving MOP status by year

The HDB leasing market is expected to see gradual price increases towards the end of 2025 due to the limited supply of flats reaching MOP. With the ongoing decline in the number of HDB flats attaining MOP status, coupled with global economic uncertainties, ERA estimates that HDB rents could rise by 2%–5% year-on-year this year.

In 1H 2025, the number of HDB rental approvals exceeded expectations, reaching 19,726 units. Consequently, ERA has revised its previous rental forecast from 34,000 to 36,000 units to a higher range of 36,000 to 38,000 units.

Singapore’s rental market is projected to remain resilient in the short to medium term.

As the supply of newly completed private homes and HDB flats continues to decline, rental rates are projected to increase through 2025 and into 2026. Rental growth is expected to be moderate, supported by limited supply and a gradual rise in rental take-up rates. This is likely to help sustain steady growth in the rental market.

Given the ongoing macroeconomic uncertainties and global trade tensions, many companies may adopt a cautious approach to hiring, which could potentially slow the intake of foreign workers. Assuming no major shifts in economic conditions or foreign worker numbers, rental demand is likely to remain steady next year, without significant spikes or declines.

Overall, Singapore’s rental market is expected to stay steady, with gradual rent increases driven by strong demand and limited new supply. The consistent rental demand, along with cautiously optimistic market behaviour, indicates the market will remain resilient in the short to medium term, benefiting both landlords and tenants.

I confirm that I have read theprivacy policy and allow my information to be shared with this agent who may contact me later.