3Q 2025 HDB Quarterly Report: Price Growth Flattens Amid Softer Resale Activity

- Ethan Hariyono

- 6 min read

- Research

- 1 Oct 2025

Figures are based off the official flash estimates for HDB quarterly statistics, released on 1 October 2025. HDB transactions are based on data.gov.sg as of 30 September 2025.

Resale Price Index (RPI) Sees Moderate Growth

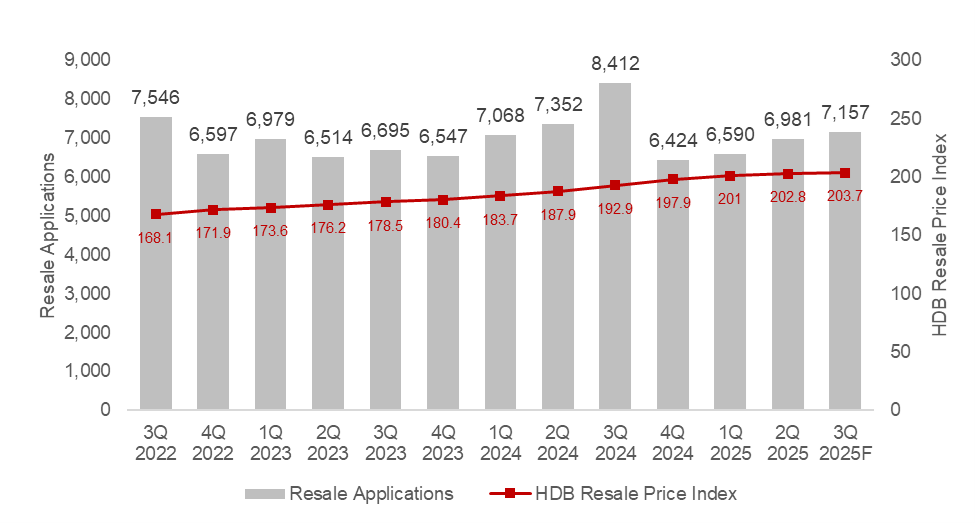

According to the Housing and Development Board (HDB)’s flash estimates, the HDB Resale Price Index rose to 203.7, a 0.4% increase quarter-on-quarter (q-o-q) in 3Q 2025.

This is the 23rd consecutive quarter of growth of the RPI, in line with ERA’s forecast of 3-6% annual price growth by the end of 2025.

Chart 1: HDB RPI vs Number of Transactions

Source: data.gov.sg as at 30 Sept 2025, ERA Research and Market Intelligence

HDB Resale Transactions

There were a reported 7,157 HDB resale transactions recorded in 3Q 2025. This marked a 2.5% increase from the previous quarter and 17.5% decline y-o-y.

Although the third quarter typically marks the peak of HDB resale transactions for the year, 2025 seems to be an exception with resale transaction numbers remaining relatively flat at a similar volume to 2Q.

This may be largely due to the July BTO and SBF launches which siphoned buyers away from the resale market. Collectively, July BTO and SBF offered 10,209 units and were in popular locations such as Toa Payoh and Bukit Merah.

Some Buyers Holding Out for the last BTO Exercise in October

Lying ahead in Oct is the final BTO exercise of the year, which will put forth around 9,100 BTO flats for sale across eight housing towns, the largest supply of the year, by far. This is on top of the over 20,000 BTO and SBF flats that were already offered in the prior February and July BTO launches.

This bumper crop of 9,100 BTO units is likely to alleviate some of the demand for HDB flats.

The upcoming BTO launches present prospective buyers with the opportunity to be first movers into emerging housing precincts, such as in Toa Payoh (the first housing located in Mount Pleasant), as well as the new Berlayar Estate (located at the former Keppel Club), under the residential town of Bukit Merah, and part of the Greater Southern Waterfront transformation.

Therefore, certain buyers may choose to defer immediate purchasing decisions until ballot results are known. A proportion of unsuccessful applicants are then likely to re-enter the resale market in subsequent months.

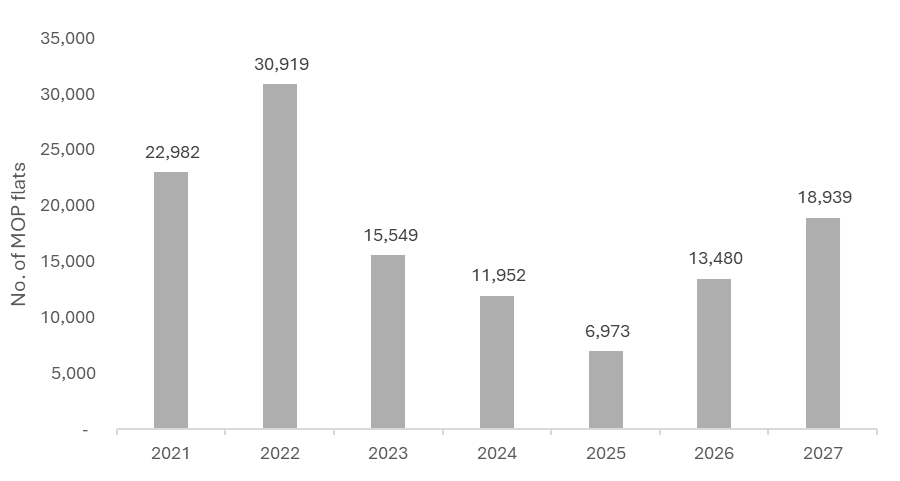

Fewer MOP flats compared to 2024

In 2025, we will see 6,974 HDB flats fulfil their Minimum Occupation Period (MOP), the lowest in 11 years since 5,301 units reached their MOP in 2014.

This has exerted upward pressure on resale prices, particularly in central locations and mature estates. However, the supply of MOP flats is projected to more than double in 2026, which may help to provide some relief for future buyers.

Chart 2: Number of MOP Flats by year

Source: data.gov.sg, ERA Research and Market Intelligence

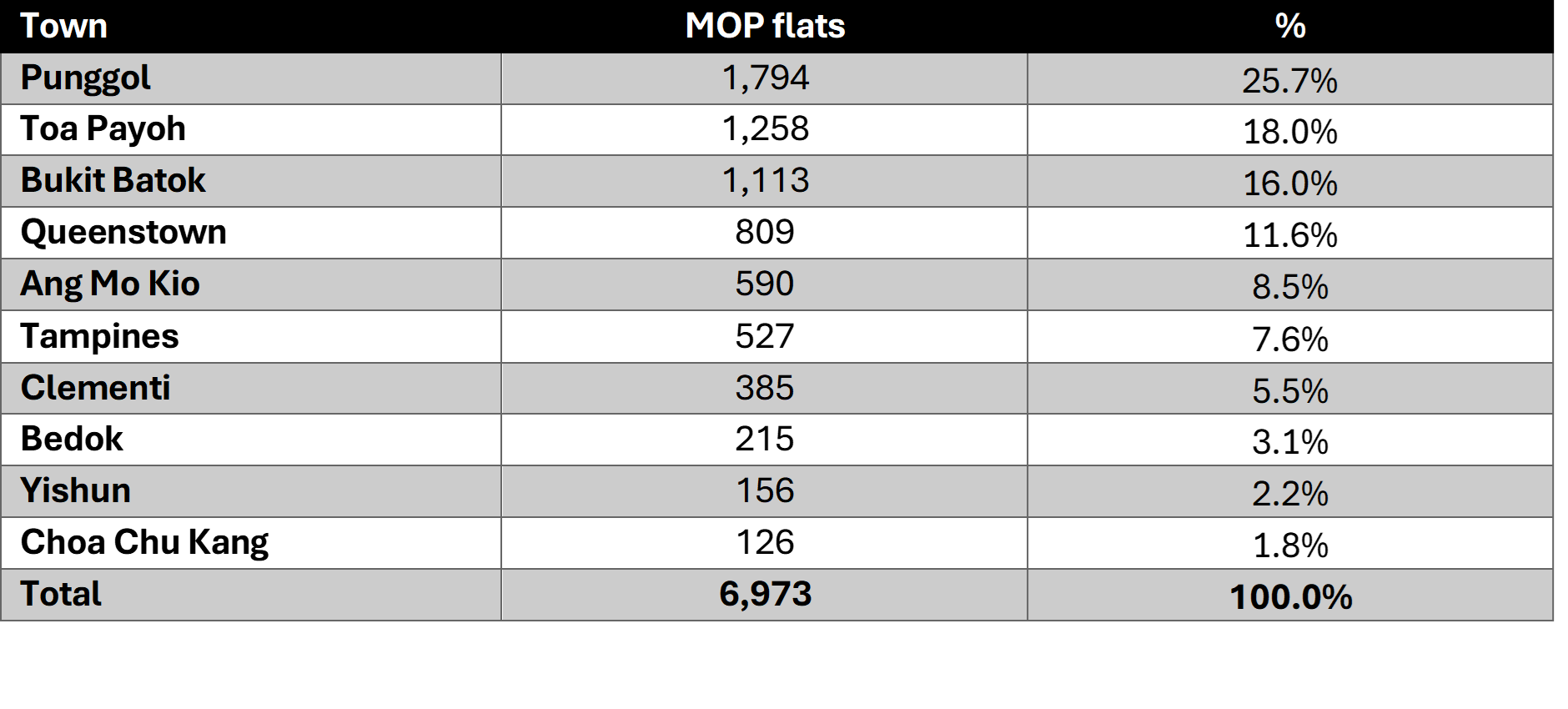

Table 1: Distribution of MOP Flats by Town in 2025

Source: data.gov.sg, ERA Research and Market Intelligence

Among the flats reaching MOP in 2025, 30% of them are in popular, centrally located housing estates such as Toa Payoh and Queenstown, which tend to command higher resale prices. They are popular among buyers, since they are not subject to the more stringent resale restrictions under the new “Plus” and “Prime” classification.

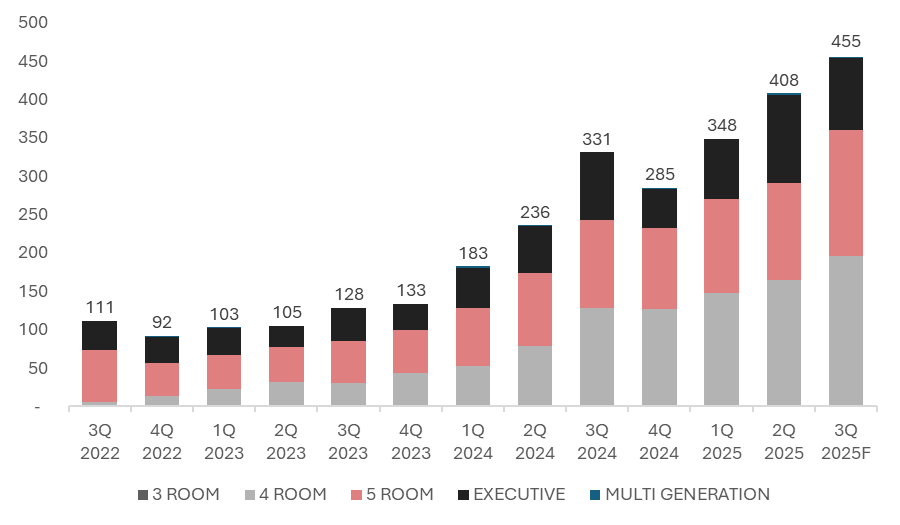

An Uptick in Million-Dollar Flats, Newer Flats Pick Up in Popularity

Million-dollar flat transactions reached a record high of 472 in 3Q 2025, up from 415 in 2Q 2025. The percentage of million-dollar flat transactions in 3Q 2025 accounted for 6.8% of all transactions, an increase from 4.4% in 1Q 2025.

The uptick in million-dollar flat transactions is apparent when compared to the same period last year (3Q 2024), which saw a total of 331 million-dollar flat transactions.

Flats in mature estates continue to make up the bulk of the million-dollar flat transactions, highlighting the demand for homes in more centrally located towns, and/or with more comprehensive amenities.

Apart from private home downgraders, there are increasingly more HDB dwellers willingto shell out a premium for a newer and centrally located flats.

Some households may choose to upgrade within the HDB market, targeting larger flats in central locations with relatively longer remaining leases, such as flats that have recently fulfilled their MOP status. These units are particularly attractive given their strong locational attributes, including established transport connectivity, access to amenities, and proximity to reputable schools.

Chart 3: HDB Flat Transactions over $1m

Source: data.gov.sg as at 30 Sep 2025, ERA Research and Market Intelligence

Flats under 15 years of age are starting to make up a larger share of HDB million-dollar transactions. In 3Q 2025, 246 of such transactions were recorded, making up over half of all million-dollar flat transactions.

This quarter, we saw 11 transactions over the $1.5m mark, with 10 of them being flats under 15 years of age. These transactions included homes in Toa Payoh and Bukit Merah, which fetch the highest demand in the million-dollar flat market. Coincidentally, these two residential towns were also selected as project sites for the upcoming October BTO exercise, signalling efforts to cool the demand for HDB flats in these sought-after estates.

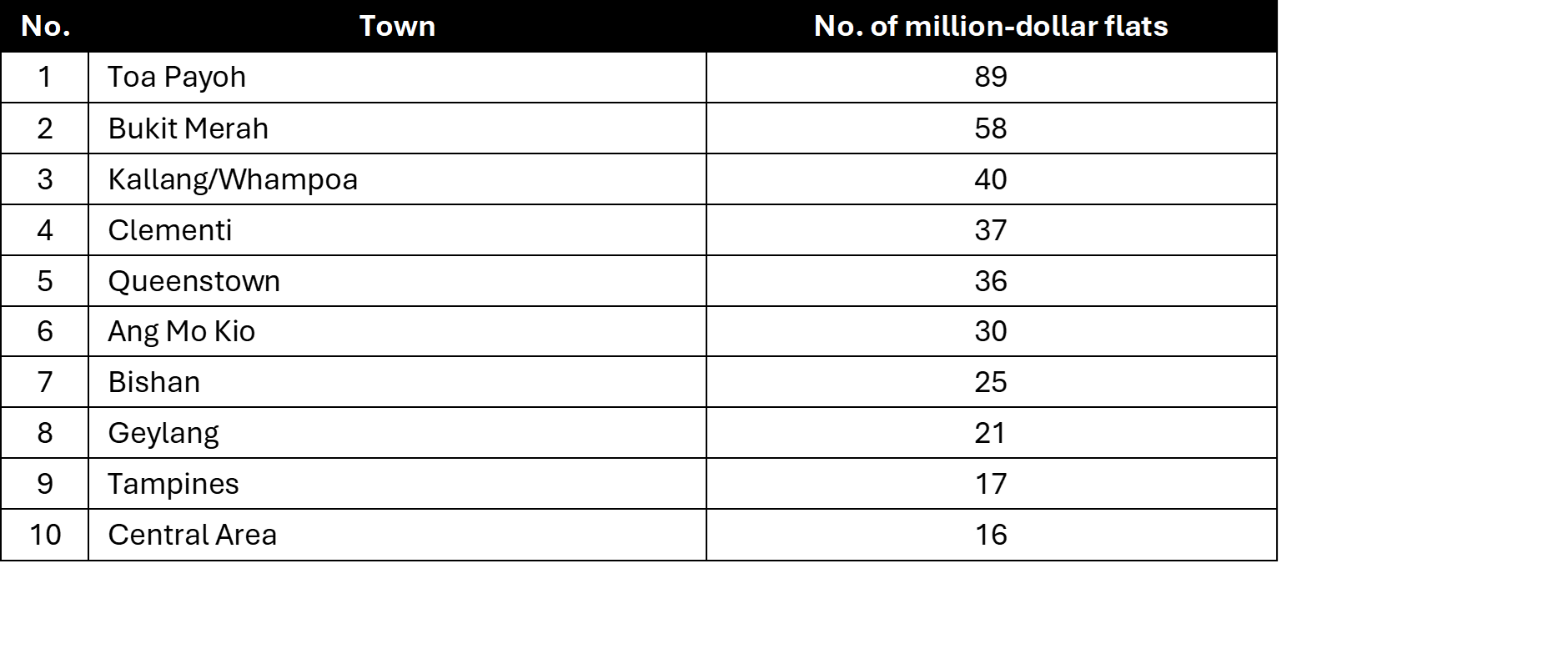

Table 2: Top 10 Towns with the Highest Million-Dollar Flats In 3Q 2025

Source: data.gov.sg, ERA Research and Market Intelligence

With the decline in the number of MOP flats in 2025, and with demand holding firm, we expect to see prices of these flats continue to rise, and around 1,500 – 1,600 of such transactions by end-2025.

Overall HDB Prices Remain Affordable

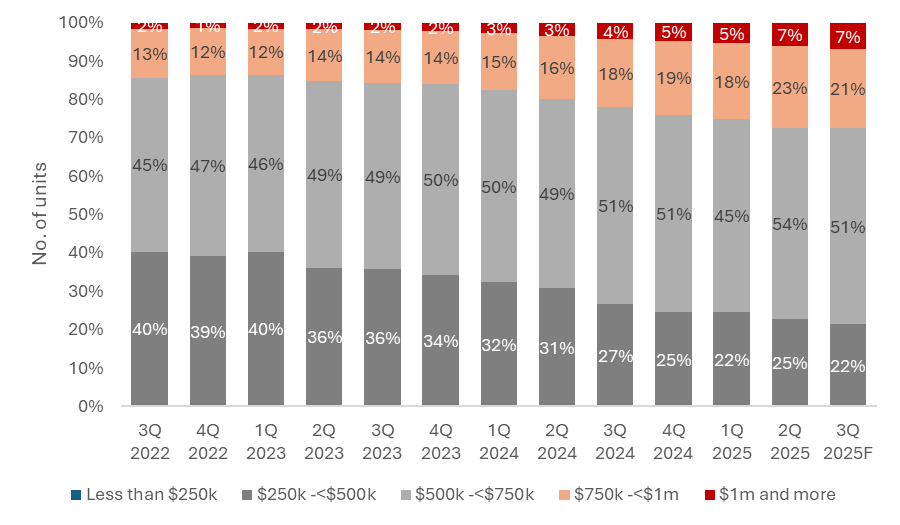

Chart 4: HDB Transactions by Price Ranges

Source: data.gov.sg as at 30 Sept 2025, ERA Research and Market Intelligence

Despite this, the majority of HDB resale flats remain affordable. Half of all HDB resale transactions in 3Q 2025 were priced between $500,000 and $750,000, a range considered affordable for many local buyers. Meanwhile, an additional 22% of HDB flats were transacted between $250,000 and $500,000.

Together, this reflects that close to three-quarters of HDB resale transactions remain affordable for the average homebuyer.

ERA’s Outlook and Forecast for the Rest of the Year

To close out the year in 4Q 2025, we expect to see fewer transactions compared to 3Q2024, due to the seasonal lull in the school holiday season, will take place in December. This period normally leads to a decrease in homebuying activity.

With a reduced supply of MOP flats in 2025, which have been a key driver of price growth in recent years, we should see a moderate price growth, and fewer transactions to close out the year. We anticipate an overall 3% – 6% price growth, with 26,000 – 27,000 resale HDB flat transactions by end-2025.

I confirm that I have read theprivacy policy and allow my information to be shared with this agent who may contact me later.