3Q 2025 Landed Report: Steady Demand Despite Rising Landed Prices with Bright Spots Emerging In CCR

- Wong Shanting

- 4 min read

- Research

- 24 Oct 2025

The landed housing market remained broadly resilient in 3Q 2025, underpinned by steady overall demand despite some signs of slowing momentum in the Rest of Central Region (RCR) and Outside Central Region (OCR). Rising home prices have begun to weigh on affordability, particularly for condominium upgraders, leading to a moderation in sales activity within these regions.

In contrast, the Core Central Region (CCR) emerged as a bright spot, with landed transactions almost doubling to 33 units in 3Q 2025 from 18 units in both the previous quarter and a year ago. This resurgence reflects renewed appetite for prime landed properties, which continue to be viewed by high-net-worth individuals as stable, long-term assets offering both capital preservation and appreciation potential.

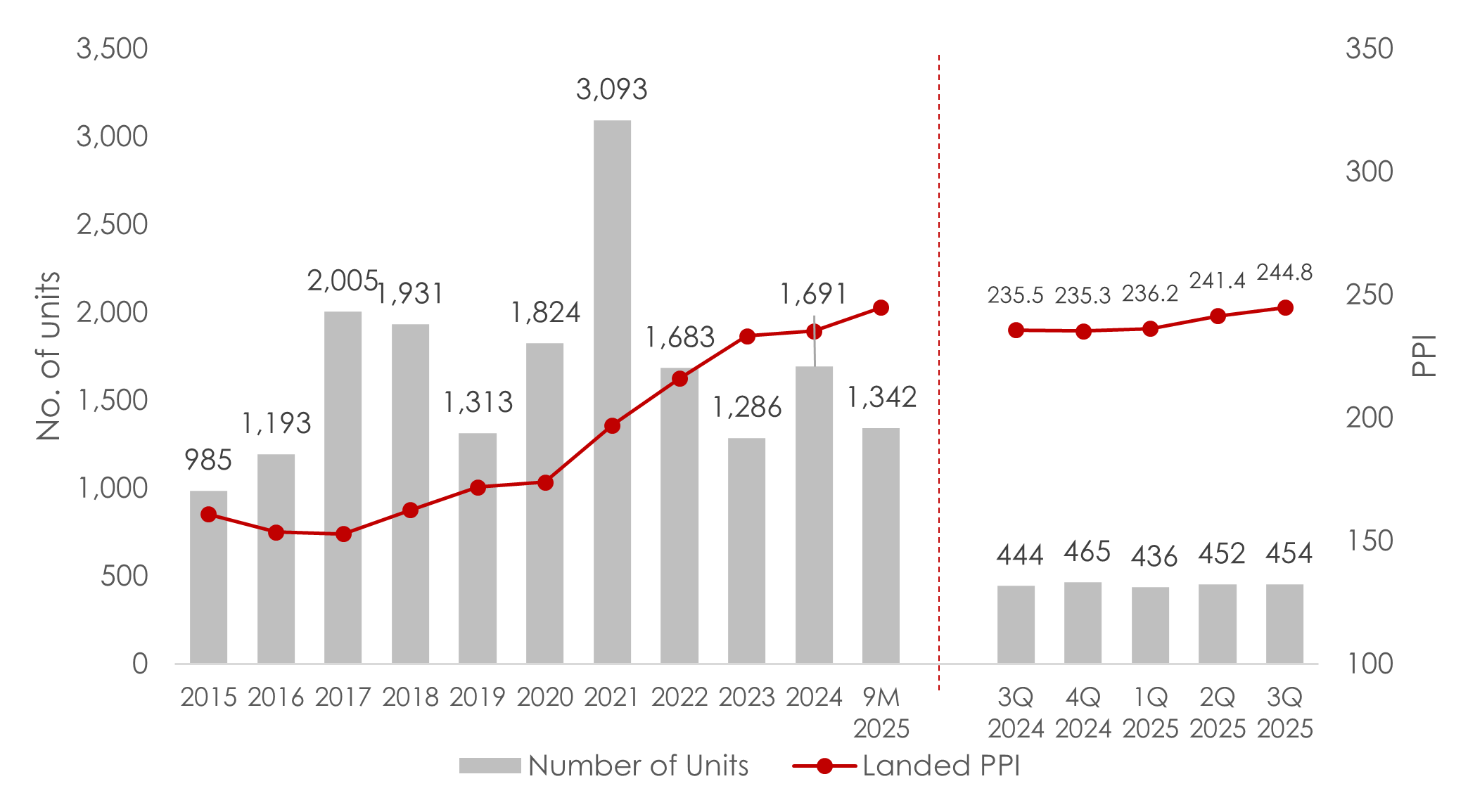

Landed Property Price Index and Transactions

The Landed Property Price Index rose to 244.8, reporting a 1.4% quarter-on-quarter (q-o-q) or 3.9% year-on-year (y-o-y). This marked the third consecutive quarter of price growth since 4Q 2024. Transaction volume has remained largely stable, with 3Q 2025 recording 454 units transacted. This represents 0.4% q-o-q and 2.3% y-o-y increase.

The rise in landed prices and steady transaction activity underscores the continued resilience of Singapore’s landed housing segment, buoyed by local homebuyers’ relentless drive to upgrade despite higher price entry barriers.

Chart 1: Landed Property Price Index and Transactions

Source: URA as of 23 October 2025, ERA Research and Market Intelligence

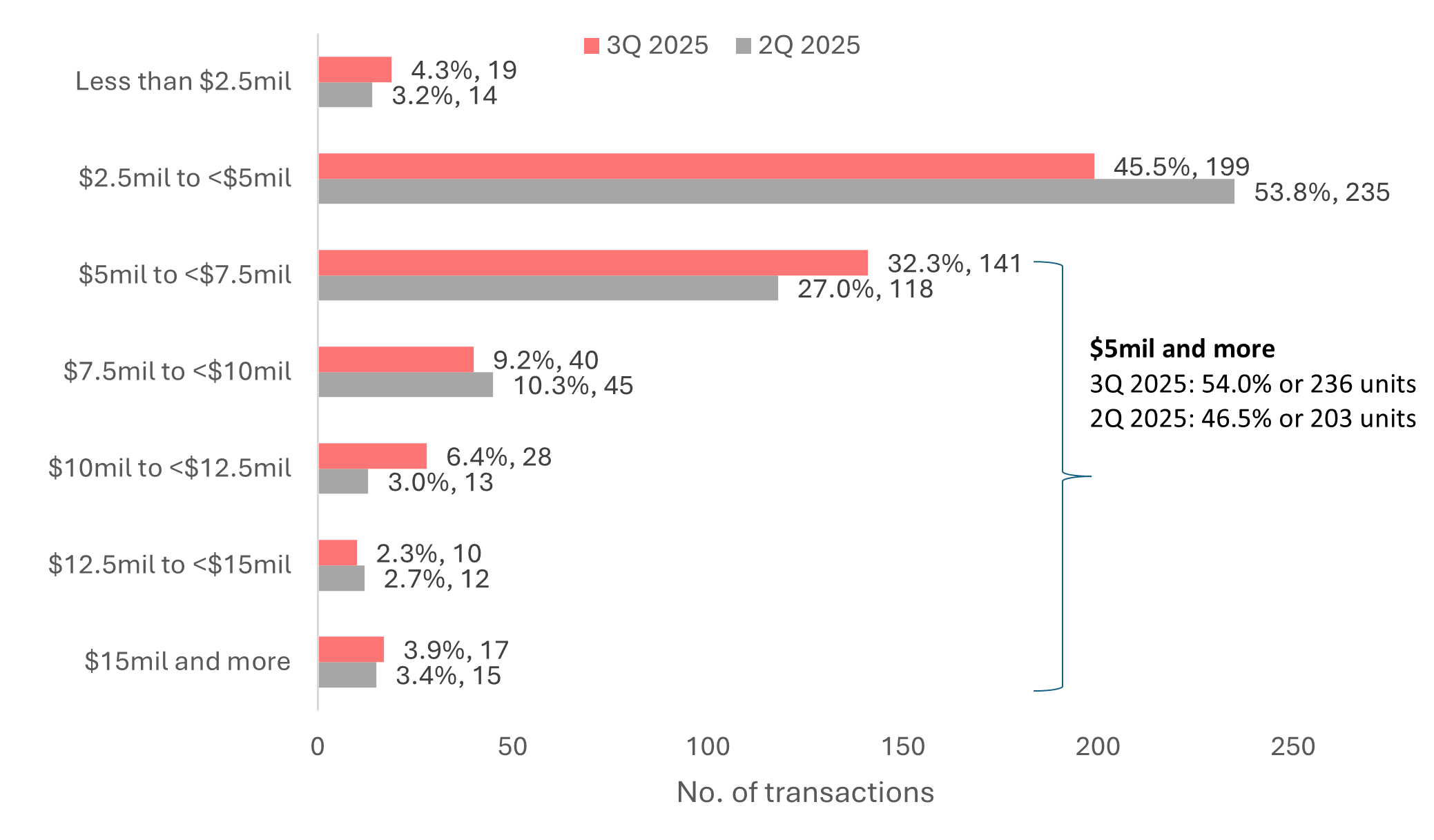

Price Quantum

Overall, 3Q 2025 saw more landed homes sold at a higher price quantum compared to 2Q 2025, affirming the rising landed prices. Over half (54%) or 236 units of the landed homes transacted in 3Q 2025 were priced above $5 million compared to 46.5% or 203 units in 2Q 2025.

A growing share of these higher-value transactions, nearly one-third, fell within the $5 million to $7.5 million range, compared to 27% in 2Q 2025. Meanwhile, 45.5% of landed homes were sold between $2.5mil and below $5mil fell to 45.5% in 3Q 2024 compared to 53.8% in 2Q 2025.

Chart 2: Price Quantum 2Q 2025 versus 3Q 2025

Source: URA, ERA Research and Market Intelligence

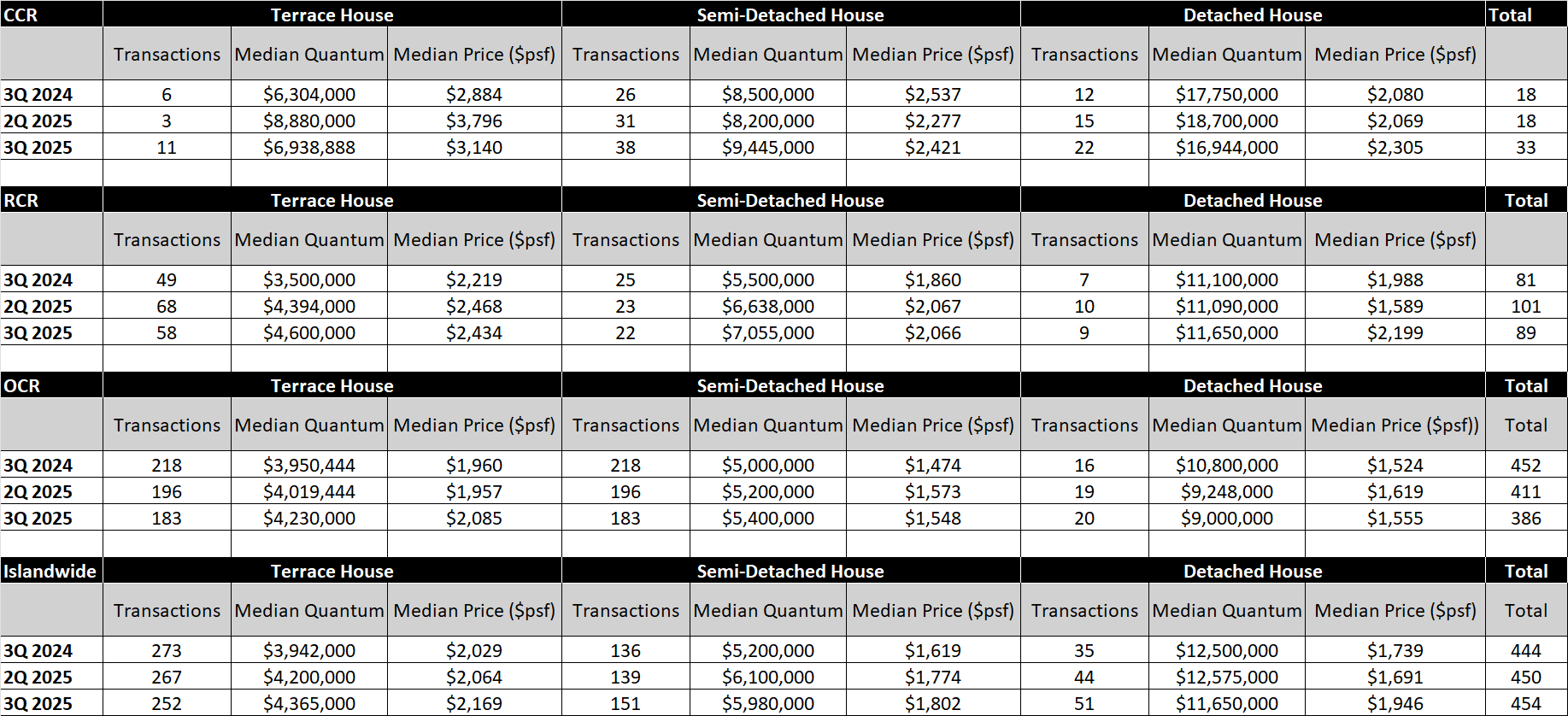

Landed home prices have seen broad-based increases, potentially constraining affordability and moderating buyer demand, particularly in the Rest of Central Region (RCR) and Outside Central Region (OCR) which had benefited from rising home prices that enabled condominium upgraders to enter the landed market.

Landed home transactions in RCR fell 11.9% q-o-q, reflecting rising median prices that may have weighed on affordability. Although facing a similar trend of increasing prices, demand for landed homes in the OCR remained relatively stable, with transaction volume holding steady despite higher entry prices. This echoed the earlier findings where a growing share of these higher-value transactions fell within the $5 million to below $7.5 million range seen in 3Q 2025.

The silver lining lies in the Core Central Region (CCR), where landed home transactions almost doubled to 33 units in 3Q 2025, up from 18 units in both the previous quarter and the same period a year ago, reflecting renewed demand for prime landed properties as they continue to be viewed as stable assets that offer long term appreciation.

Table 1: Transaction Volume and Median Price by Landed Property Type and Market Segment

Source: URA as of 23 October 2025, ERA Research and Market Intelligence

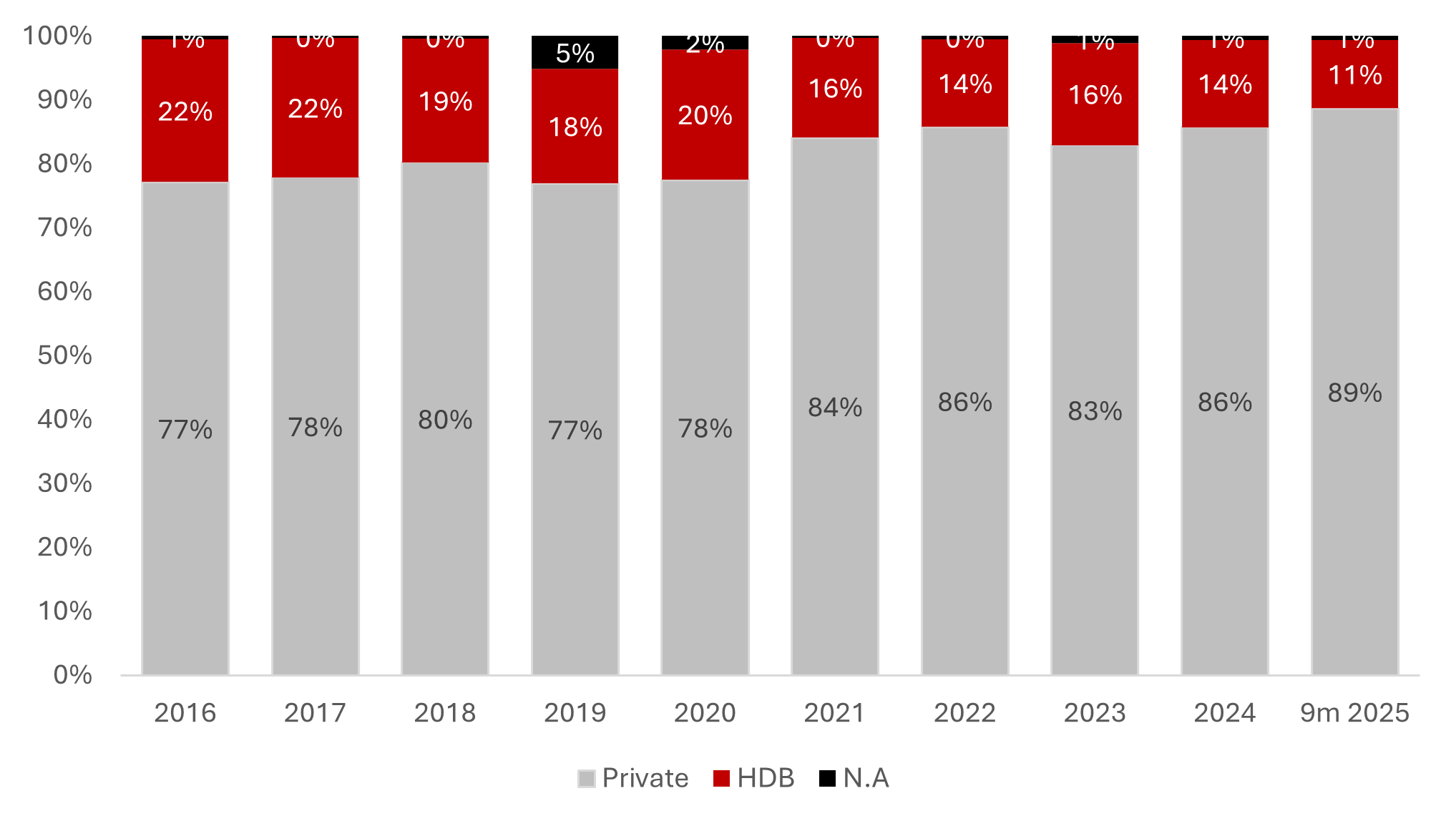

Purchasers Address Indicator

Amid rising landed housing prices, the proportion of HDB owners upgrading to landed properties continues to shrink further. In the first nine months of 2025, just 11% of landed home buyers recorded a HDB address, down from 14% in 2024 and 16% in 2023.

Chart 3: Landed home buyer profile

Source: URA as of 23 Oct 2025, ERA Research and Market Intelligence

In conclusion

Overall demand landed home has held steady, but the sale momentum has gradually slowed in RCR and OCR, marked by rising home prices that have impacted accessibility for condo upgraders.

The silver lining lies in the Core Central Region (CCR), where landed home transactions almost doubled to 33 units in 3Q 2025, up from 18 units in both the previous quarter and the same period a year ago, reflecting renewed demand for prime landed properties as they continue to be viewed as stable assets that offer long term appreciation.

For the first nine months of 2025, 1,342 landed homes changed hands, with prices up 4.0% from 4Q 2024. This places the market on track to meet ERA’s full-year projection of 3–5% price growth and 1,500–1,800 transactions for the landed segment.

I confirm that I have read theprivacy policy and allow my information to be shared with this agent who may contact me later.