4Q 2025 Landed Report: Strong End to 2025 As Upgraders Support Landed Home Demand

- Egan Mah

- 5 min read

- Research

- 28 Jan 2026

The landed housing market remained broadly resilient in 4Q 2025, underpinned by steady overall demand from condominium upgraders. Rising non-landed home prices have enabled them to upgrade, leading to an increase of 2.3% in prices. This rise can be largely attributed to more transactions in the Rest of Central Region (RCR) and Outside Central Region (OCR). However, the Core Central Region (CCR) saw fewer transactions due to higher prices, as buyers and sellers face a mismatch in price expectations.

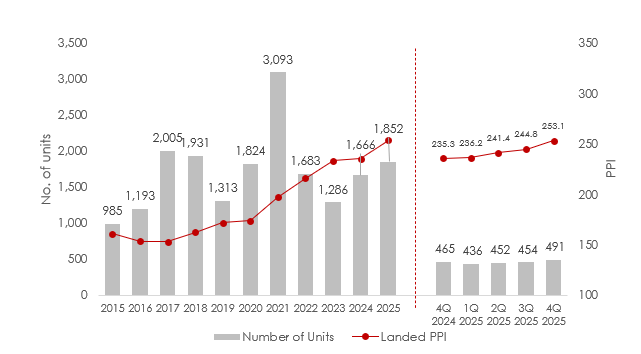

Based on URA caveats, landed home transactions rose 4.0% q-o-q to 491 transactions in 4Q 2025. It also marked the quarter with the highest number of landed home transactions since 2Q 2022. This brings 2025’s total to 1,852 transactions, 11.2% more than the whole of 2024.

Landed homes continue to be viewed highly by local high-net-worth individuals due to its stability, offering both long-term capital preservation and appreciation potential.

Landed Property Price Index and Transactions

The Landed Property Price Index rose to 253.1, reporting a 3.4% quarter-on-quarter (q-o-q) or 7.6% year-on-year (y-o-y). This marked the fourth consecutive quarter of price growth since 4Q 2024. Based on URA caveats, transaction volume has remained largely stable, with 4Q 2025 recording 491 units transacted. This represents 4.0% q-o-q and 5.8% y-o-y increase.

The rise in landed prices and transaction activity underscores the continued resilience of Singapore’s landed housing segment. Seen as an aspirational target amongst local homebuyers, prospective buyers would take the opportunity to upgrade should the opportunity arise.

Chart 1: Landed property price index and transactions

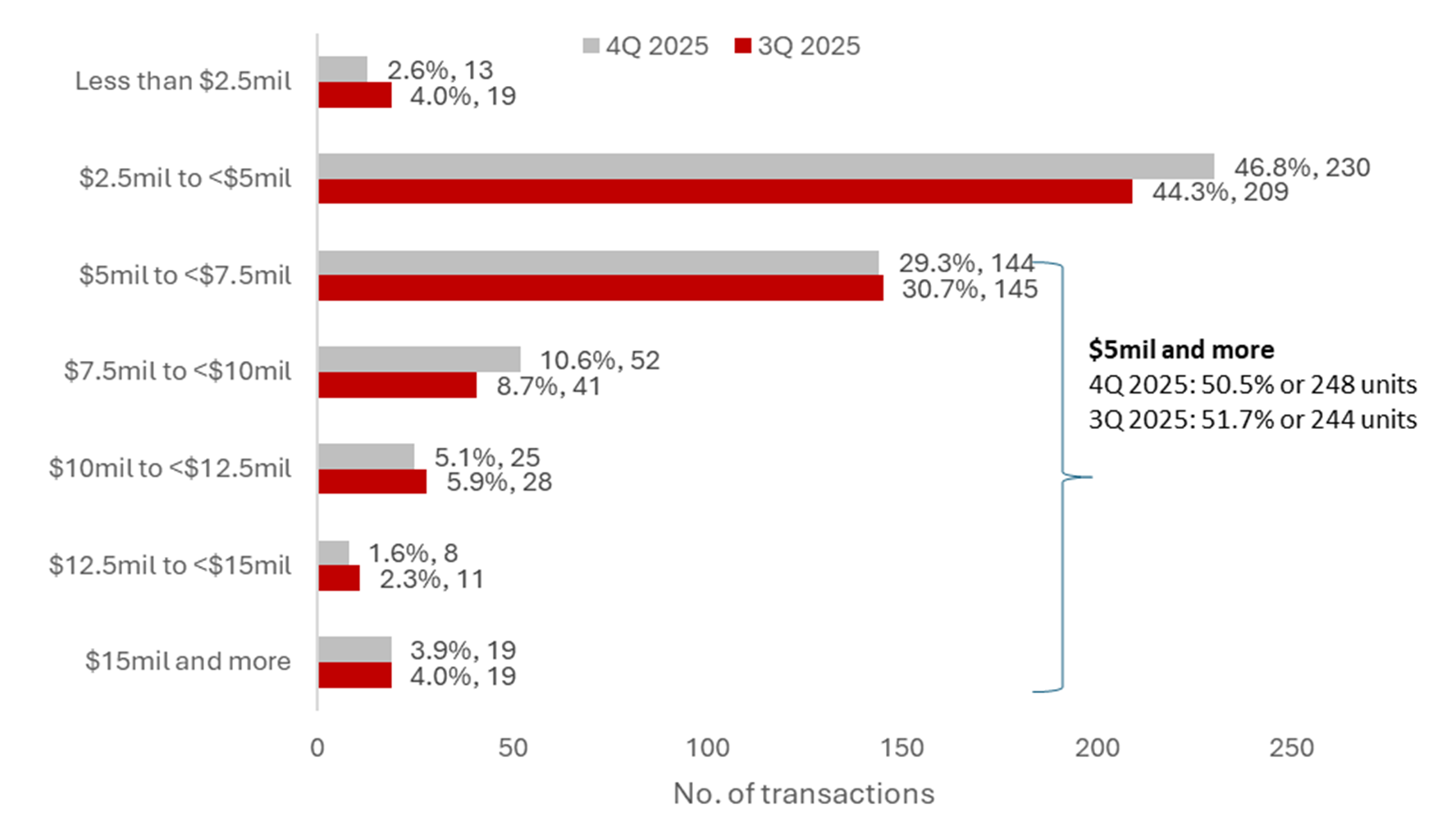

Price Quantum

Overall, 4Q 2025 saw more landed homes sold at a higher price quantum compared to 3Q 2025, affirming the rising landed prices. About half (50.5%) or 248 units of the landed homes transacted in 4Q 2025 were priced above $5 million, similar to the 51.5% or 244 units in 3Q 2025. In terms of proportion, the price range of landed home transactions remained largely similar.

Chart 2: Landed price quantum 3Q 2025 versus 4Q 2025

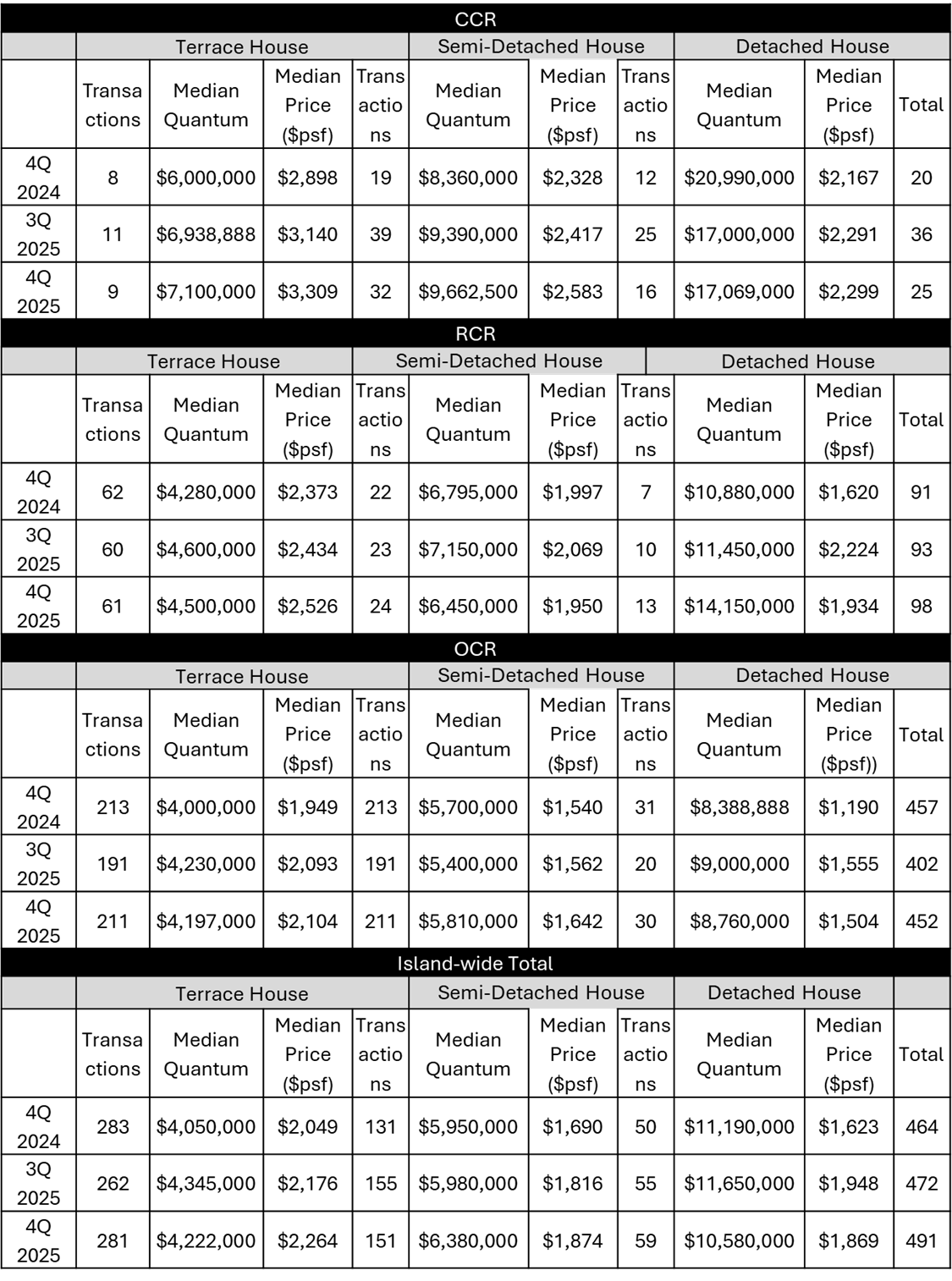

Rising non-landed home prices have resulted in greater affordability for condominium upgraders. Despite higher price barriers, we have seen more Rest of Central Region (RCR) and Outside Central Region (OCR) transactions. With the ability to command higher prices for their condominiums, these homeowners have greater accessibility to the landed market.

Landed home transactions in the OCR and RCR rose 12.4% and 5.4% respectively q-o-q in 4Q 2025. Lower prices of less centrally located homes provided a more attractive price point for upgraders, as the seek to balance between their locational preference, spatial needs and affordability.

The bulk of landed home transactions (57.2%) were Terrace House in the OCR, which proved to be a good entry point into the landed market. This echoed the earlier findings where the highest proportion of transactions (46.8%) between the $2.5 million to $5 million price range. The median price quantum of such homes was $4.22 million in 4Q 2025, 2.8% lower than the $4.35 million in the previous quarter.

However, the CCR landed home market saw a 30.6% q-o-q decline to 25 transactions in 4Q 2025. This comes as the median price psf and median quantum of homes transacted have risen, reflecting renewed demand for prime landed properties. Such homes are viewed as stable assets that offer long term appreciation due to their finite supply and prestigious status. Moreover, CCR landed home sellers, typically with higher holding power, are less inclined to reducing their prices. Thus, buyers and sellers faced an impasse on prices.

Table 1: Transaction volume and median price by landed property type and market segment

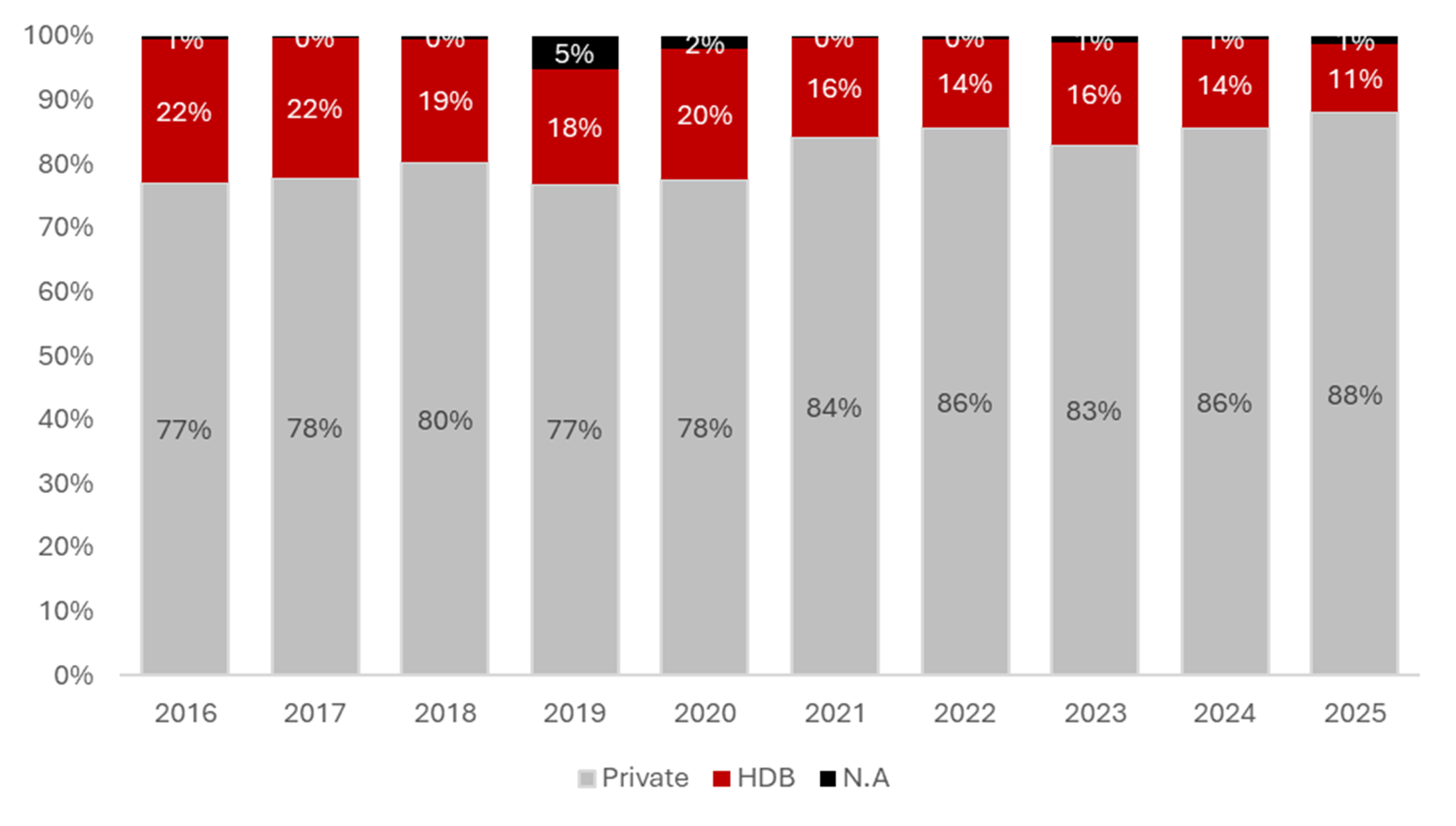

Purchasers Address Indicator

Amid rising landed housing prices, the proportion of HDB owners upgrading to landed properties continues to shrink further. In 2025, just 11% of landed home buyers recorded a HDB address, down from 14% in 2024 and 16% in 2023.

Chart 3: Landed home buyer profile

In conclusion

Overall demand landed home has been steady in 4Q 2025, with strong sale momentum in the OCR and RCR. Condominium upgraders have fueled the market, as they have benefited from higher sales proceeds. However, CCR landed homes has gradually slowed, marked by differing price expectations between buyers and sellers.

The strong performance in the final quarter wrapped up a stellar 2025 for the landed home market. Overall, the landed segment performed remarkably well with 1,852 transactions in 2025, the highest since 2021. It had also surpassed ERA’s initial forecast of 1,500 to 1,800 transactions for the full year. In terms of prices, the Landed Property Price Index grew 7.6% in 2025, also exceeding ERA’s full-year projection of 3% – 5% price growth.

We do foresee the sales momentum to carry into 2026, projecting between 1,750 – 1,950 transactions, with price growth between 5% - 7% for the full year.

I confirm that I have read theprivacy policy and allow my information to be shared with this agent who may contact me later.