April 2026 Monthly Developer Sales Report: Popular OCR Launches Mark Strong Start to 2Q 2026

- Stanley Lim & Ethan Hariyono

- 9 min read

- Research

- 15 May 2026

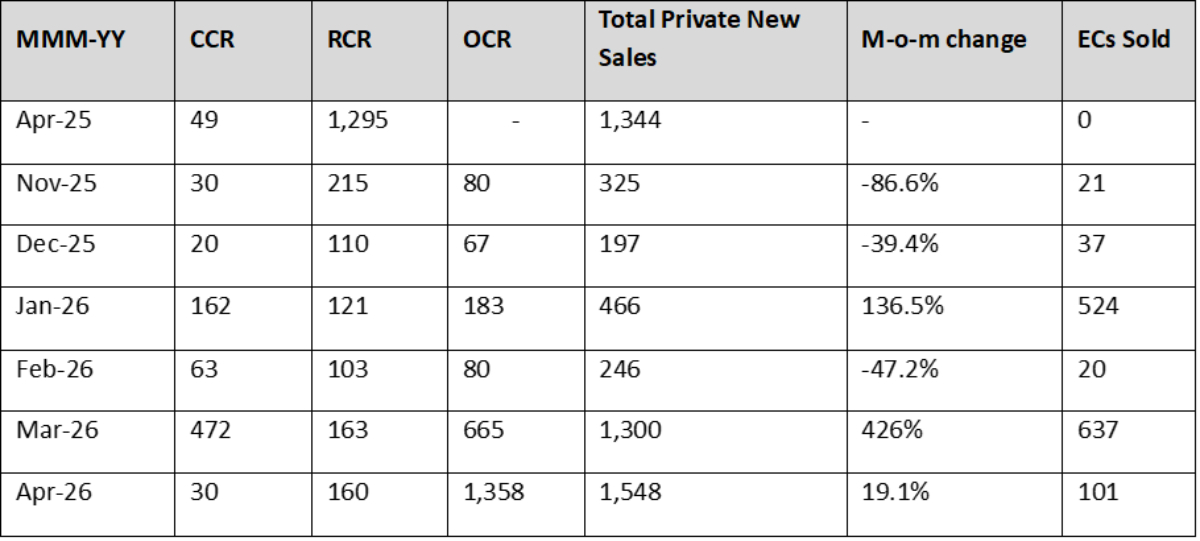

In April 2026, the new private home market saw a total of 1,548 units (excluding ECs) sold by developers. This marks a 19.1% month-on-month (m-o-m) uptick in transaction volume, and a further improvement over March’s performance of 1,300 units.

This increase was largely driven by the strong take-up rates seen at two launches: Vela Bay and Tengah Garden Residences. The former is a 515-unit leasehold development in the emerging Bayshore precinct, while the latter is an 863-unit leasehold project located in Tengah.

Strong launch day demand reflective of ongoing demand for Outside Central Region (OCR) private housing was observed at both projects. During their respective weekend debuts in late-April, Vela Bay achieved a 72% take-up rate, while Tengah Garden Residences saw a near complete sell-out with 99% of its inventory snapped up.

Table 1: New home sales over the last six months (excluding ECs)

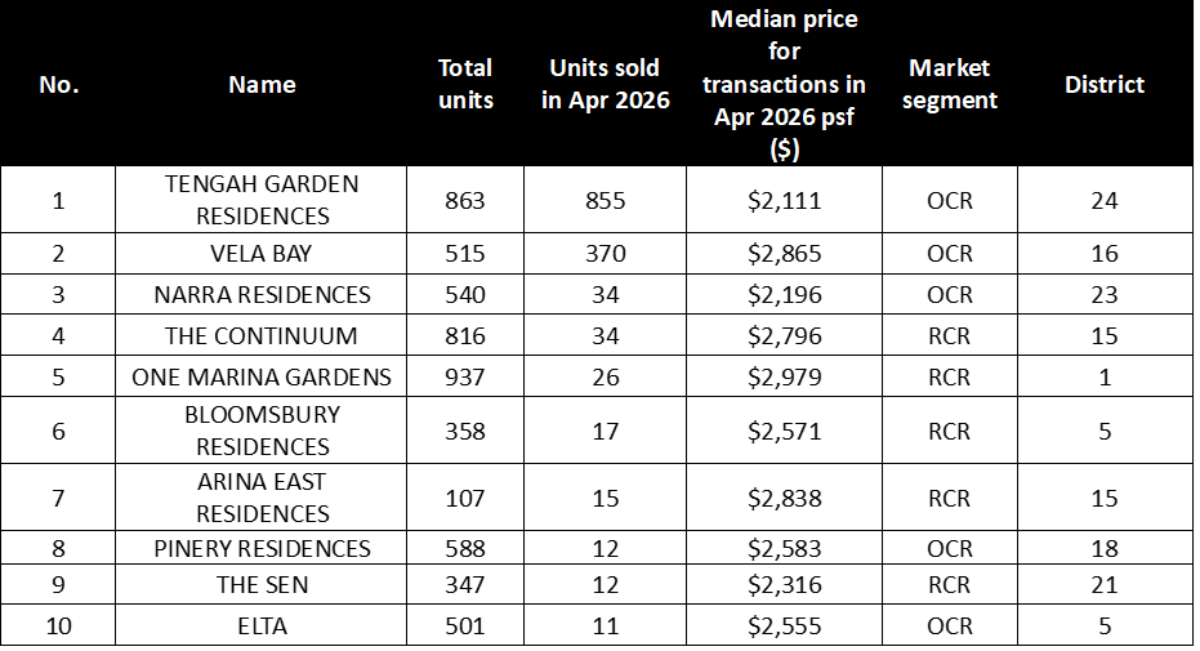

Beyond fresh supply at new projects, buyers also moved quickly on existing stock in April. Against current prices set by new launches, earlier projects were seen to offer strong value. As such, existing developments, like Narra Residences and The Continuum, moved 34 units each.

Tengah Garden Residences Leads Monthly Sales with 99% of Inventory Sold at Launch

Tengah Garden Residences was April’s best-selling project, with 853 of its 863 units sold during its debut in the last week of April. This translates to a 99% take-up rate, while also making it the best-selling condominium launch in 2026 so far, by both sales percentage and number of units sold.

Launch-day sales was strongly supported by HDB upgraders, including those living in Bukit Batok and Choa Chu Kang. Between 2025 and 2028, over 2,100 three-room and larger HDB flats in both towns are expected to reach the end of their minimum occupation period, making it a key factor in anchoring buying activity from aspiring upgraders.

Demand for Tengah Garden Residences was also supported by its first-mover advantage as Tengah’s first private condominium launch. Likewise, its attractive entry pricing, proximity to regional transport infrastructure, and access to key employment nodes in the West helped support buyer interest.

Units at Tengah Garden Residences sold offered a strong value proposition, with median unit pricing and quantum of $2,111 psf and $1.81 million respectively. These price points are relatively accessible in today’s market, which was a major draw for affordability-focused buyer segments, including HDB upgraders.

In addition, buyers were likely drawn to Tengah Garden Residences’ proximity to the upcoming Hong Kah MRT station. Slated for completion in 2028, the station will be part of the Jurong Region Line and will provide convenient access to key work-and-learn destinations in the West, including the Jurong Lake District, Jurong Innovation District and NTU.

Adding to the project's appeal for families is its proximity to several reputable schools, such as the upcoming Anglo-Chinese School (Primary), Princess Elizabeth Primary, and Swiss Cottage Secondary

These attractive locational attributes are also complemented by a viable exit strategy for first-movers. With Tengah planned to house approximately 30,000 HDB flats when it reaches full development, homeowners at Tengah Garden Residences can look forward to a ready buyer pool once nearby flats exit their MOP.

Firm Demand Seen at Vela Bay, Bayshore’s First Private Condominium Launch

Similar to Tengah Garden Residences, Vela Bay delivered a strong performance as the first private residential offering in the Bayshore precinct. Over its late-April launch weekend, Vela Bay moved 371 of its 515 units, representing a 72% take-up rate. This success follows Pinery Residences, another OCR development in the East, which also enjoyed a strong debut earlier in March this year.

Interested buyers, including right-sizers from nearby landed enclaves in District 16, were largely driven by pent-up demand. This stems from a prolonged absence of new private residential supply in Bayshore; the last major launch in the vicinity was Seaside Residences in 2017, which reached completion in 2021.

Both owner-occupiers and investors were drawn to Vela Bay’s desirable locational attributes and long-term development potential. This appeal is primarily anchored by its doorstep access to the Bayshore MRT station on the Thomson-East Coast Line (TEL), which offers future residents a direct transit route to the Central Business District, Marina Bay, and Orchard Road.

Looking ahead, the TEL’s connectivity will be further boosted by the 2030s when the interchange station at Changi Airport Terminal 5 is completed. This will link the TEL with the Cross Island Line, further strengthening Vela Bay’s connectivity advantage and long-term appeal.

Discerning buyers were also keen on capitalising on Vela Bay’s first-mover advantage, especially in a precinct where private residential supply will remain limited. Upon completion, private housing is expected to constitute only about 30% of the total housing mix in Bayshore; this relative scarcity enhances Vela Bay’s appeal for those seeking to secure an early foothold ahead of the district’s transformation over the longer term.

In terms of education, family buyers with school-going children likely found Vela Bay appealing for its proximity to Temasek Primary, which falls within a 1km radius. Other nearby schools also include Bedok Green Primary, Victoria School, and Temasek Junior College.

Table 2: Top performing new non-landed projects in April 2026 (excluding ECs)

Monthly EC Sales Slow, But Rule Changes Could Drum Up Interest for Upcoming Projects

In April, EC sales declined 84.1% m-o-m to 101 transactions. The sharp drop was mainly due to the high base in the previous month, which saw 637 deals recorded, owing to the successful launch of Rivelle Tampines.

The month’s EC transactions consisted mainly of buyers snapping up leftover stock from Rivelle Tampines, constituting approximately 75% of all deals made. Units transacted were primarily 4- and 5-bedroom units, given that the most popular 3-bedroom layouts were largely sold out at launch.

The second-best selling EC was Coastal Cabana, moving 19 units, behind the successful launch of Rivelle Tampines. Buyers interested in an East region EC could have been waiting for Rivelle Tampines launch prices to be revealed before making their informed decision between the two projects.

With new rules giving priority to first-timers at future EC launches, second-timer interest at upcoming projects could rise further. This could be driven for those unwilling to wait out the two-year priority window for first-timers that applies to EC sites launched under the latest measures from 8 May onwards.

The three possible EC launches expected to be launched in the fourth quarter are located in Woodlands Drive 17, Senja Close, and Sembawang Road. We can expect strong interest among buyers for these projects as well, since they are also governed by the previous set of EC restrictions. They should receive strong buyer interest, particularly among second-timers.

Buyer Profile

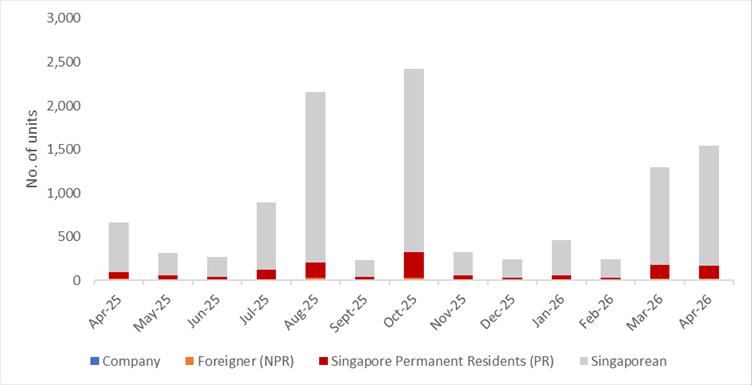

Chart 1: Buyer profile for all new non-landed private homes (excluding ECs)

Amid a strong showing in the new private home segment, foreign buying activity held firm in April. Comparable to the 24 cases recorded in March, foreigners accounted for 23 new non-landed private home transactions (excluding ECs) as of 13 May 2026. This works out to around a 1.5% share of all equivalent deals that took place within the month.

In comparison, Singapore Permanent Residents (SPRs) were responsible for 148 transactions or 9.6% of total monthly sales in April. At the same time, Singaporeans continued to dominate the new launch market, accounting for 1,372 transactions or 88.9% of all sales.

Luxury Homes

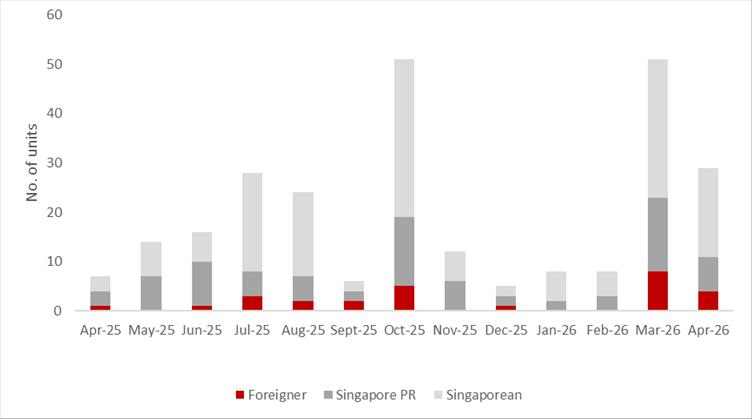

Chart 2: Buyer profile for non-landed private homes (excluding ECs) transacted at $5mil and more

Despite the uptick in developer sales in April, sales of luxury homes slipped compared to March. Based on URA caveat data as of 13 May 2026, a total of 29 new non-landed private homes (excluding ECs) were sold at the $5 million or higher price point during the month, with Singaporeans making up the bulk of such purchases with 18 transactions. On the other hand, foreigners were responsible for four of these high-value transactions in April, while SPRs accounted for seven cases.

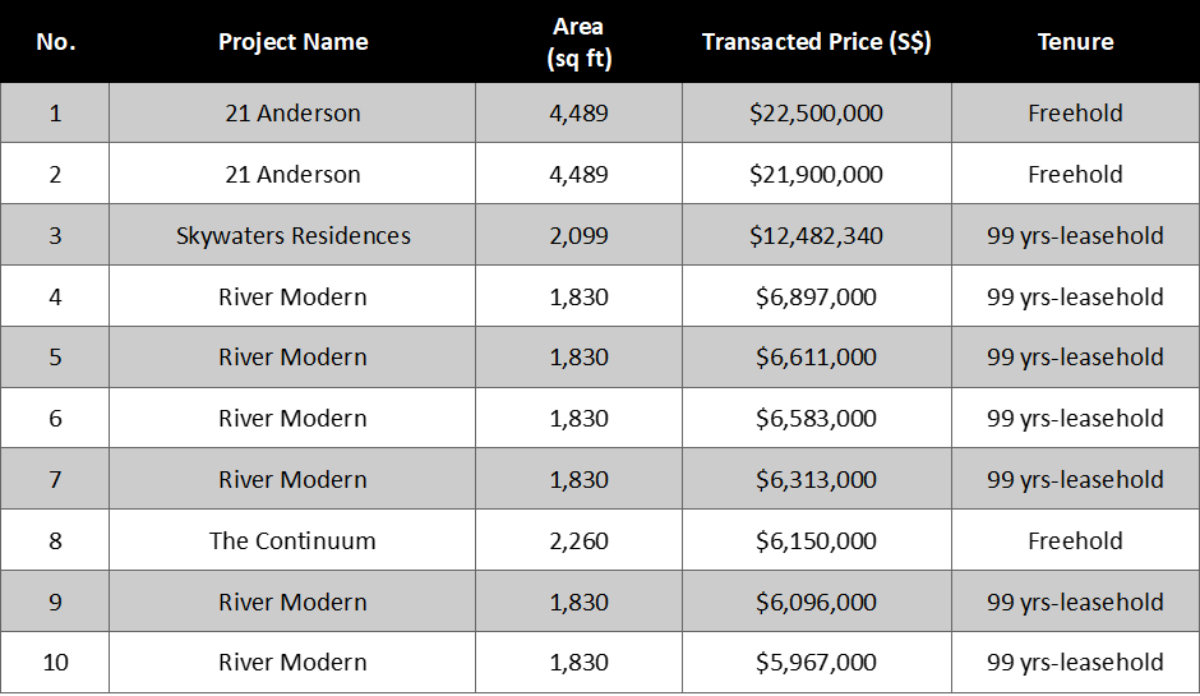

The two priciest deals for April occurred at 21 Anderson and involved 4‑bedroom units measuring 4,489 sq ft. Both units were sold to SPRs for $22.5 million and $21.9 million respectively. According to URA caveats (as of 13 May 2026), these transactions also rank as the second‑ and third‑priciest non-landed private residential transactions so far this year.

The bulk of high-value transactions during the month occurred at The Continuum, which accounted for seven deals, or 24.1% of the total count. Except for one 2,260 sq ft unit sold for $6.15 million, most transactions at the project fell within the $5.0 million to $5.5 million range.

Table 3: Top Luxury Transactions for March 2026

Closing Thoughts and Forecast

Despite heightened geopolitical tensions and their potential implications for the global economy, Singapore’s property market has stayed resilient. The steady take-up rates seen in 2026 thus far point to a selective yet confident buyer pool. Rather than broad-based enthusiasm, demand is increasingly focused on projects that combine strong locational advantages with a compelling value proposition.

At the same time, Singapore is relatively well-placed to weather external risks, supported by stable governance, a strong currency and a resilient economy.

Key drivers of local housing demand also remain intact. According to the Ministry of Manpower, Singapore’s labour market continued to expand in 1Q 2026, marking the 18th consecutive quarter of employment growth since end-2021. Unemployment and retrenchment rates have also stayed broadly stable, even as local employers have expressed greater hiring caution. Together, these factors have supported a market where buyers remain ready to commit.

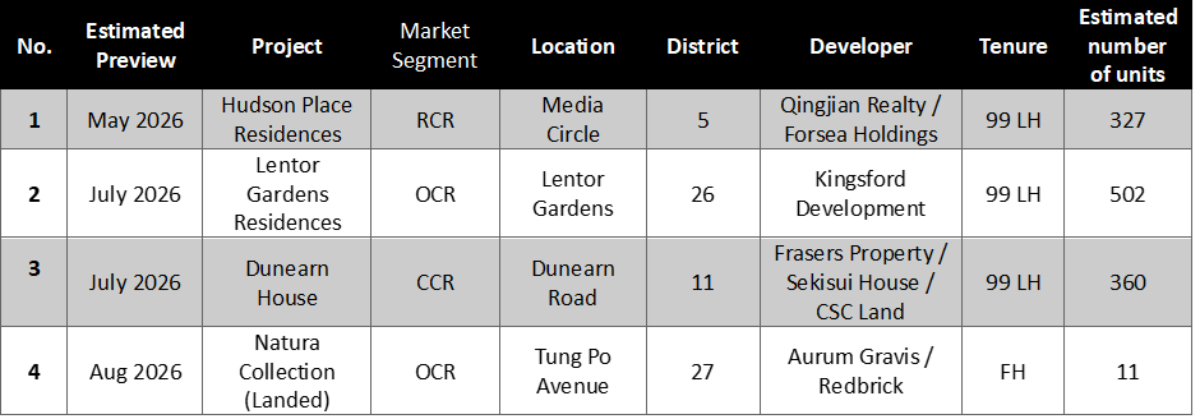

For the full year, buyers can expect a pipeline of 18 private residential projects, and five executive condominium launches in 2026. Barring unforeseen developments, ERA Singapore projects new home sales to reach between 9,000 and 10,000 units by year’s end.

Table 4: Upcoming launches in 2026

I confirm that I have read theprivacy policy and allow my information to be shared with this agent who may contact me later.