August 2025 Monthly Developer Sales Report: August New Home Sale Hit a high note, CCR saw the highest transaction since Mar 2021

- kwong seong ping

- 9 min read

- Research

- 15 Sep 2025

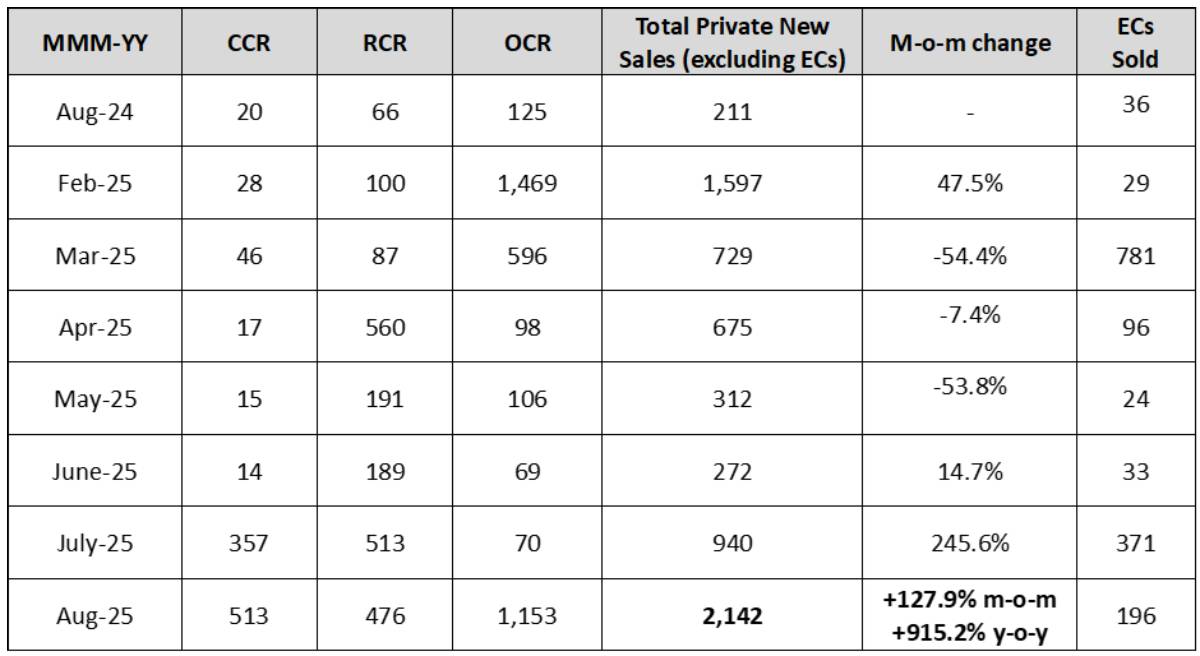

August 2025 saw developer sales coming in at 2,142 new private homes (excluding ECs), reflecting a 127.9% month-on-month (m-o-m) increase in transaction volume. This is the highest number of new homes sold in a month since November 2024 (2,560 units).

The higher number of new home sales was largely driven by five new project launches in the month – namely Springleaf Residence, River Green, Promenade Peak, Artisan 8 and Canberra Crescent Residences. August also marks the highest number of CCR new homes sold in a month since March 2021, with the launch of River Green (524 units).

Collectively, this puts the total number of new private homes (excluding ECs) sold in the first eight months of 2025 at 7,669 units, surpassing the 6,469 new sale units transacted in the whole of 2024. The surge was largely driven by a strong pipeline of new home launches in August, particularly in underserved areas in recent years, and alongside moderating interest rate.

Outside of Central Region (OCR) projects accounted for 1,153 new homes sold in August, marking the highest number of units sold since February 2025 (1,469 units). Strong sales in the OCR were driven mainly first-time buyers and HDB upgraders seeking new homes.

Meanwhile, the Executive Condominium (EC) market saw a 47.2% m-o-m decrease to 196 units. EC sales in August were primarily led by Otto Place after balloting was opened for second timers, selling another 191 units. As of Aug, the supply of EC remains tight, with only 73 units remaining unsold.

Table 1: New Home Sales Over the Last Six Months

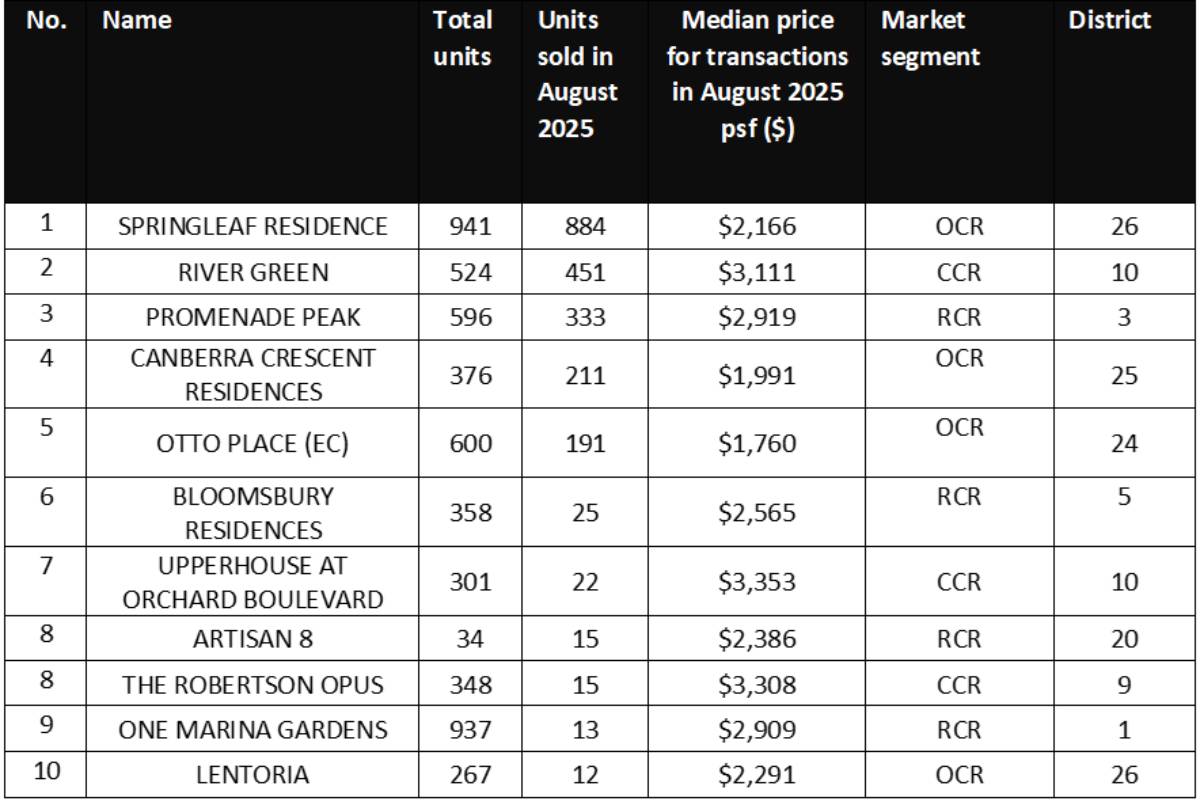

August saw the launch some 2,479 units including five new projects – Springleaf Residence (OCR), River Green (CCR), Promenade Peak (RCR), Canberra Crescent Residences (OCR) and Artisan 8 (RCR).

Best Performing New Launches

Springleaf Residence Achieved 92% Take-Up at Launch Day

Springleaf Residence is the first private condominium to launch within the Springleaf housing estate. Jointly developed by GuocoLand and Hong Leong Holdings, the project achieved a strong take-up. The project comprising of 941 units, sold 884 units or 92% at a median price of $2,166 psf.

Sales at Springleaf Residence were mostly transacted at less than $2 million, which accounted for approximately 57% of all new homes sold this month. This can be attributed to nearby HDB upgraders and existing residents in the Upper Thomson and Springleaf area seeking an upgrade within a familiar neighbourhood.

As the pioneering new project within the region, Springleaf Residence enjoys a first-mover advantage. It is also located next to Springleaf MRT station, providing residents access to major work nodes, and reputable schools across the island. The development sits beside Singapore’s largest nature reserve, offering lush green spaces and easy access to hiking trails and outdoor activities.

Nearly 800 units new launches sold in River Valley area on launch weekend

Two new projects were launched in August within the River Valley area, namely River Green (524 units) in CCR and Promenade Peak (596 units) in the RCR, adding a total of 1,120 new launches in the region. Both developments saw strong take-up over their launch weekends, with River Green and Promenade Peak achieving 88% and 54% sales respectively.

Although located in close proximity, River Green falls within the CCR while Promenade Peak is within the RCR. River Green saw 345 out of its 451 units were sold at $2.5 million and below, at a median price of $3,111 psf. This entry price quantum is relatively affordable in a prime CCR location, combined with direct sheltered access to Great World MRT, making it particularly attractive to majority Singaporean and PR buyers.

Promenade Peak (596 units) leaned into exclusivity, appealing to families seeking practical and larger layouts over price accessibility. Positioned as the tallest residential tower in the area, it offers luxury features such as a rooftop infinity pool. Till date, the project sold 333 of its units at a median price of $2,919 psf. The project sold 185 out of its 320 2-bedroom units (58%) and 86 out of 118 3-bedroom units (73%). Notably, about 217 of its 333 units were sold at $2.5 million.

Canberra Crescent Residences

Canberra Crescent Residences is a 376-unit private condominium. The project marks the first new launch project in the north since the launch of Norwood Grand in Q4 2024 and the first in Canberra in four years. The project sold 211 of its 376 units at a median price of $1,991 psf .

The project site was acquired in July 2024 for approximately S$793 psf ppr. In comparison to the other transacted EC GLS sites, namely Otto Place GLS land site at S$703 psf ppr and the Jalan Loyang Besar GLS land site at $729 psf ppr. This allows the new launch units psf prices to be set close to EC median psf prices, attracting HDB upgraders within the region and northern areas, particularly Sembawang, many of the units had reached their Minimum Occupation Period (MOP).

Canberra Crescent Residences is strategically located between Canberra Plaza and the Bukit Canberra hub, and is within walking distance of Canberra MRT Station. The development is aligned with the proposed future transformation outlined in the 2025 URA Draft Master Plan, which includes the redevelopment of Sembawang Shipyard into a vibrant new housing estate.

Table 2: Top ten performing new launch project (excluding ECs) in August

Otto Place 92% sold after second-timer balloting

Otto Place saw a total of 351 out of 600 units sold in July new launch, with a take-up rate of 59.7%. Following the second-timer balloting in August, sales rose to 543 units, achieving 91% take up. All four-bedroom units were fully sold, reflecting strong demand from second-timer buyers who typically have larger families and require a larger home. The project also attracted nearby HDB upgraders seeking enhanced lifestyle and facilities.

The robust demand was also fuelled by limited supply of new EC launches and rising GLS land costs. The next expected EC launch is the 748-unit project at Jalan Loyang Besar, acquired by Qingjian Realty in August 2024 at $729 psf prr, slated to launch next year. These upcoming EC prices are expected to be higher, as Otto GLS site was previously awarded at a record low of $701 psf ppr.

Buyer Profile

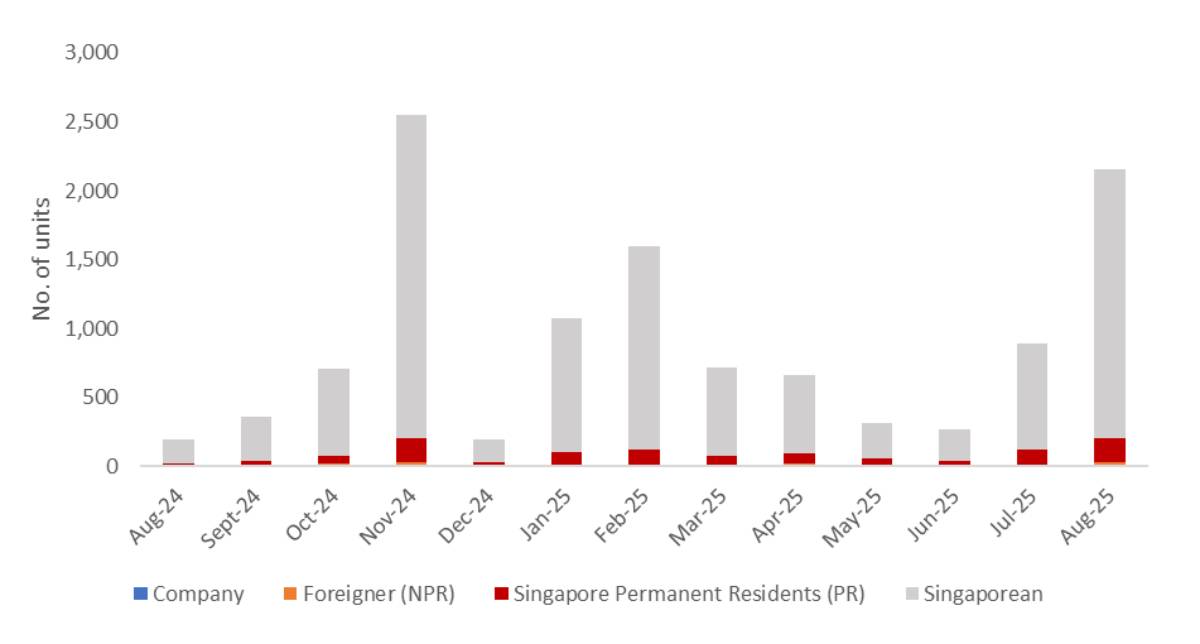

Chart 1: Buyer profile for all new non-landed homes (excluding EC)

With the steep Additional Buyer’s Stamp Duty still in place, demand from foreign buyers for new private homes remained subdued. August saw a total of 29 non-landed private home (excluding ECs) transactions made by foreign buyers, making up just 1.3% of the month’s total deals. Meanwhile, Singapore Permanent Resident buyers clocked 173 transactions in June, accounting for 8.0% of all new private home (excluding ECs) purchases in the month.

Lastly, Singaporeans continued to dominate the market in August, with new private home sales (excluding ECs) sharp increased by 253.7% quarter-on-quarter to 1,951 units, the highest since February 2025. This surge was mainly driven by the Springleaf Residence. This project alone accounted for 38% of the new launch sales in August.

Luxury Homes

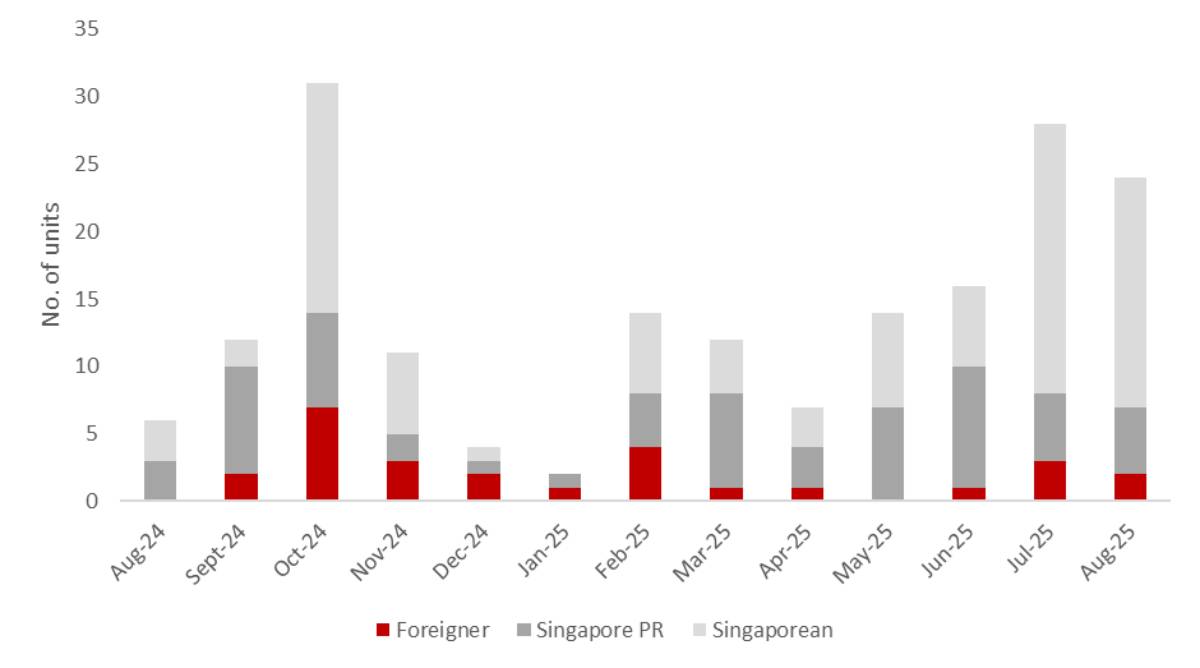

Chart 2: Buyer profile for homes transacted at $5mil and more

In August, the luxury home market saw a slight decrease in activity, maintaining a stable trend and recording the second-highest take-up since November 2024. A total of 24 new private residential transactions were recorded for homes priced at S$5 million and above. These were primarily driven by locals and Singapore Permanent Residents, who accounted for 5 and 17 transactions each.

This month saw two transactions exceeding the S$20 million. Both were ultra-luxury freehold units within the same development at 21 Anderson, each purchased by a Singaporean and a Singapore Permanent Resident. The highest-value transaction was a 10,452 sq ft, five-bedroom duplex penthouse unit with a roof terrace, which sold for approximately S$52.25 million. The second-highest sale was a 4,489 sq ft, four-bedroom unit that sold for about S$21 million. These transactions suggest that buyers seeking high-end properties may be attracted to the expansive floor plates and coveted addresses offered by such ultra-luxury projects.

Notably, within the S$5-6 million price range, a total of 18 units were sold in the month of July. Promenade Peak dominated this segment with units sold (83.3%), while Amber House, One Marina Gardens and Terra Hill each recorded one sale. The majority of these buyers were Singaporeans, accounting for 83.3% of all purchasers. This can be attributed to being a new launch project coupled up with the pent-up demand for new private homes in the CCR.

Closing Thoughts and Forecast

August sales remain brisk in the new private home sales market, aligning with the number of new launches this month. Sales hit 2,153 units, led Springleaf Residence in the north region, which sold 870 out of 941 units (92%) and accounted for 40% of monthly transactions. River Green (524 units) in CCR and Promenade Peak (596 units) also performed well, with take-up rates achieving 88% and 54% respectively.

The new launches spread across CCR, RCR, and OCR also highlights a broader buyer demand in Singapore private residential with all regions seeing a very healthy take up. River Green new launch result shows that CCR projects can still be successful when priced and positioned strategically and buyer sentiment being mostly Singaporean or PRs. Its strong demand also reflects renewed confidence in the CCR market, which had slowed drastically after the April 2023 ABSD hike.

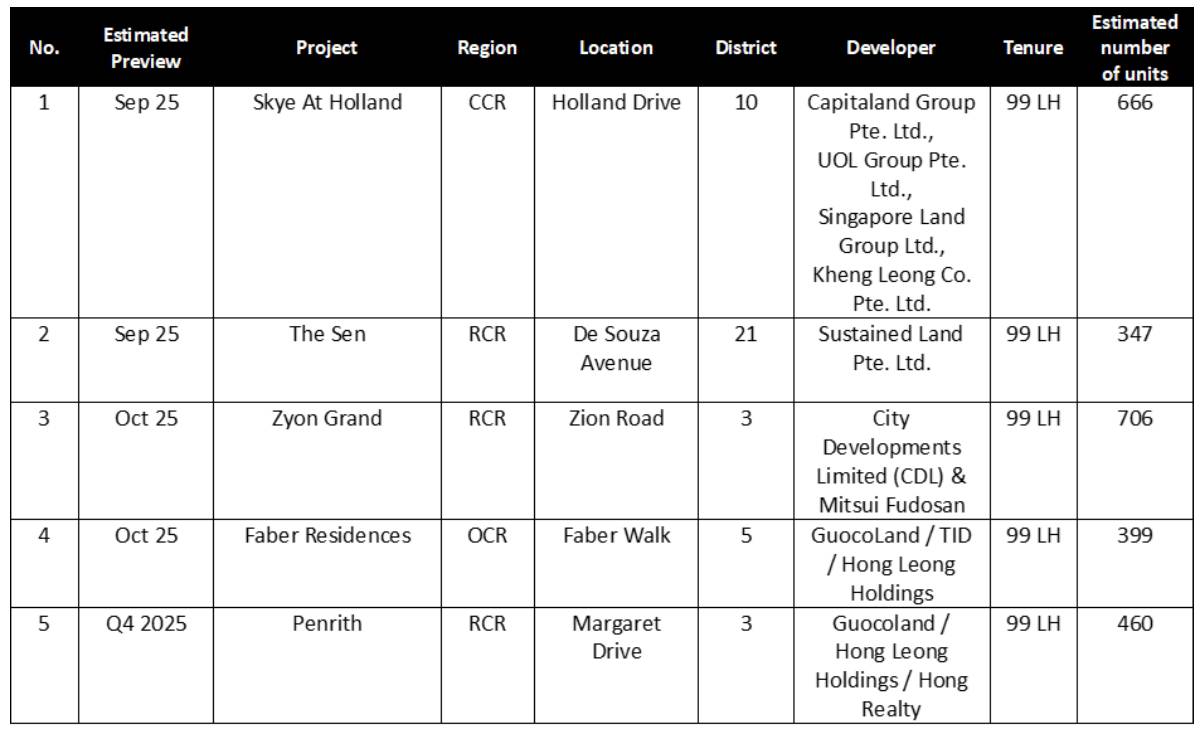

Moving forward into the second half of 2025, five new launches are expected, with three new launches in the RCR namely Zyon Grand, Penrith, and The Sen, alongside Skye at Holland in the CCR and Faber Residences in the OCR. Demand is expected to remain resilient, with robust take-up rates expected across these projects, supported by strong buyer interest heading into year-end.

Collectively, the total number of new private homes (excluding ECs) sold in the first eight months of 2025 at 7,669 units, surpassing the 6,469 new sale units transacted in the whole of 2024. Barring any unforeseen circumstances, ERA Singapore projects new home sales to be between 8,500 - 9,500 units for the whole of 2025.

Table 3: Upcoming launches in 2025

I confirm that I have read theprivacy policy and allow my information to be shared with this agent who may contact me later.