February 2026 Monthly Developer Sales Report: Muted Sales Amid Seasonal Lull

- Kwong Seong Ping

- 8 min read

- Research

- 16 Mar 2026

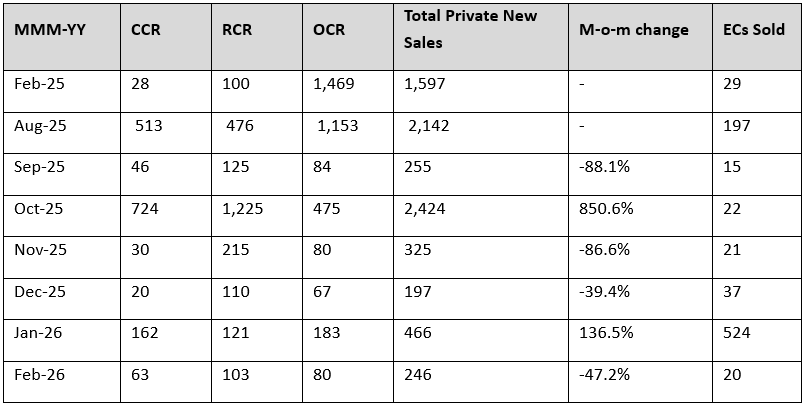

For February 2026, a total of 246 new private homes (excluding ECs) were sold by developers, reflecting a 47.2% month-on-month (m-o-m) decrease in transaction volume. The fall in new home sales was primarily due to the lack of new launches in the month amid the Chinese New Year festivities. In contrast, January saw the launches of two new private home projects (Newport Residences and Narra Residences), as well as an Executive Condominium (EC), namely Coastal Cabana.

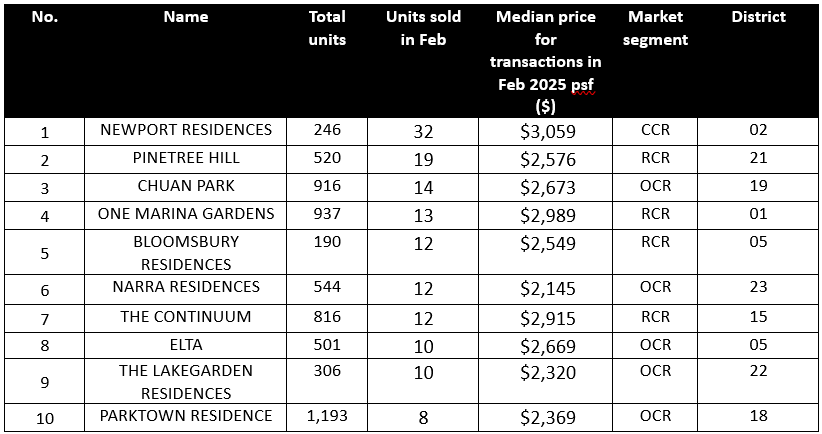

February 2026 also saw Newport Residences (32 units sold), Pinetree Hill (19 units sold), Chuan Park (14 units sold), and One Marina Gardens (13 units sold) taking the top spots for projects with the most units sold during the month.

Similarly, the Executive Condominium (EC) segment saw a decline in developer sales, from 524 units last month to just 20 units in February 2026. This downtick was mainly due to the absence of EC launches over the month. Amid this absence of fresh supply, Otto Place sold 10 units, accounting for 50% of the total monthly EC transactions. This was followed by Coastal Cabana, which saw 9 units sold.

Following these transactions, Coastal Cabana is the only EC with new stock available in the market. EC buyers can look out for the next EC launches in coming months, such as Rivelle Tampines and Woodlands Drive 17.

Table 1: New home sales over the last six months (excluding ECs)

Newport Residences leads February new home sales

Newport Residences, located in the Central Business District (CBD) continued to see new sales activity in February. While new residential projects in the CBD typically take longer to gain traction, Newport Residences recorded the sale of another 32 units during the month, bringing its total take-up to approximately 74% as at 13 March 2026, according to ERApro.

The development’s rare freehold tenure provides a longer-term value proposition for both investors and owner-occupiers seeking properties in the CBD. Freehold residential projects in prime central locations are relatively limited in supply, which can enhance their appeal among buyers looking for asset preservation and long-term capital value.

Another major factor supporting buyer interest is its relative pricing position within the CCR segment. With a median purchase price of around $3,059 psf, Newport Residences [SL1] offered buyers the opportunity to acquire a freehold property at a price point slightly below the Core Central Region (CCR) median of $3,063 psf recorded in February. This pricing positions the project as comparatively attractive within the prime market.

Taken together, its competitive pricing relative to the wider CCR market, coupled with its rare freehold tenure and prime CBD location, has supported Newport Residences’ continued sales momentum even in a month without new launches.

RCR Developments Continue to Draw Stable Demand

Four of the top ten projects sold during the month were located in the Rest of Central Region (RCR), highlighting sustained buyer interest despite the quieter festive period. These projects [SL2] (Pinetree Hill, One Marina Gardens, Bloomsbury Residences and The Continuum) collectively recorded 56 units sold, accounting for about 40% of all new sale transactions among the top-performing non-landed developments.

This steady uptake suggests that buyers remain confident in the RCR market segment even as overall transaction volumes moderated in February. The continued preference for RCR developments may stem from their ability to offer a balanced proposition in terms of pricing, accessibility, and lifestyle amenities, positioning them as an attractive middle ground between the more expensive Core Central Region (CCR) and the suburban Outside Central Region (OCR).

In addition, many RCR projects benefit from proximity to city fringe locations, established amenities, and well-connected transport networks. This makes them appealing to both owner-occupiers seeking convenient access to the city as well as investors looking for properties with strong rental demand, particularly from professionals working in nearby business districts.

Table 2: Top performing new non-landed projects in February (excluding ECs)

Otto Place EC achieves near full take up in February

Otto Place sold a total of 10 units in February 2026, and according to ERApro as of 16 March, the EC project has been fully sold. The strong take-up reflects sustained demand for Executive Condominiums (ECs), particularly among HDB upgraders seeking a more affordable entry into private housing.

With Otto Place fully sold, Coastal Cabana remains the only EC project with available units in the market. As at 12 March 2026, 515 out of 748 units at Coastal Cabana have been sold, translating to 69% of the development taken up, according to ERApro. The development continues to draw interest from buyers in the East region, particularly households upgrading from nearby HDB estates such as Tampines and Pasir Ris.

Looking ahead, the next EC launch expected in early 2026 is Rivelle Tampines. Located within the mature Tampines estate and supported by MRT connectivity and nearby amenities, the upcoming project is likely to attract significant attention from buyers in the East. Moreover, with Rivelle Tampines set to launch soon, some EC buyers may delay their purchasing decision until its pricing is announced.

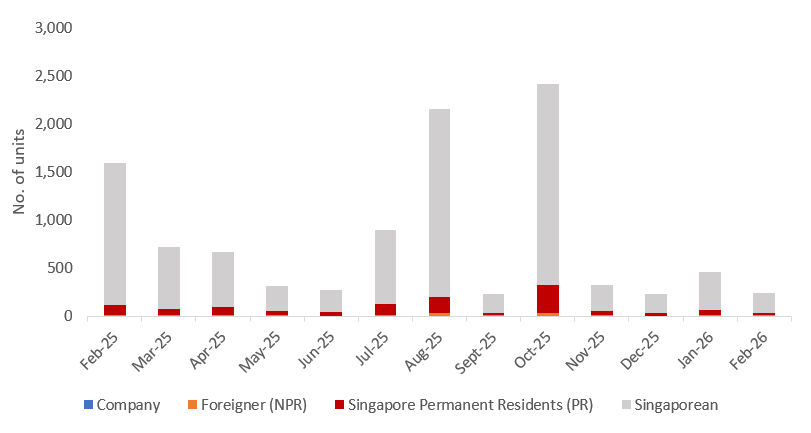

Buyer Profile

Chart 1: Buyer profile for all new non-landed homes

With the steep Additional Buyer’s Stamp Duty still in place, demand from foreign buyers for new private homes remained subdued. February saw only eight non-landed private home transactions made by foreign buyers, making up a meagre 3.3% of the month’s total deals. Meanwhile, Singapore Permanent Resident buyers purchased 23 new non-landed private homes, accounting for 9.5% of all new private home (excluding ECs) purchases in the month.

Lastly, Singaporeans continued to dominate the market in February, accounting for 87.2% of new private home sales (excluding ECs), or 212 units.

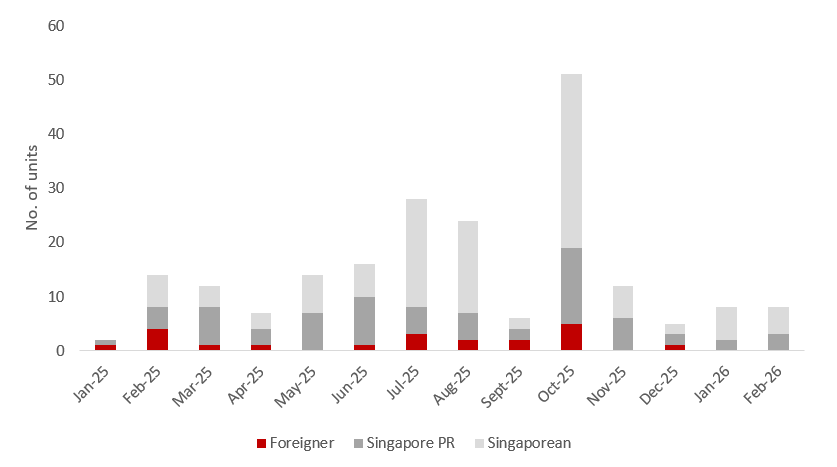

Luxury Homes

Chart 2: Buyer profile for homes transacted at $5mil and more

Luxury home transactions picked up in January, with eight new non-landed private homes (excluding ECs) transacting at $5 million and above. Of these transactions, none were made by foreigners, while Singapore Permanent Residents (SPRs) and locals accounted for three and five transactions respectively.

Two luxury residential units transacted within the $15 million to $20 million price range were both purchased by Singapore Permanent Residents (SPRs). The highest-value transaction was a 5-bedroom penthouse (4,833 sq ft) at Union Square Residences for $18.5 million, followed by a 4-bedroom premium unit (2,906 sq ft) at Park Nova for $15 million.

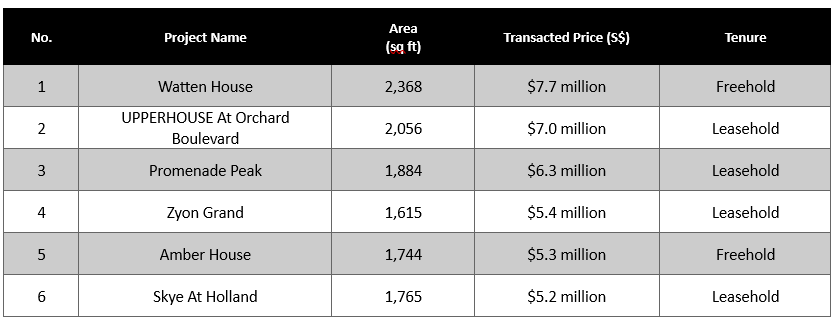

Meanwhile, a total of six luxury transactions recorded in February were within the $5 million to $8 million price range. Three of these transactions are located in the Core Central Region (CCR) namely Watten House, UPPERHOUSE at Orchard Boulevard, and Skye at Holland. The remaining three transactions took place in the Rest of Central Region (RCR), at Promenade Peak, Zyon Grand, and Amber House (see Table 3).

Table 3: Luxury Transactions between $5 million to $8 million

Closing Thoughts and Forecast

With greater geopolitical tensions worldwide, global stability could be further tested by global conflicts between Israel, Iran and the United States, possibly triggering fears of economic uncertainty. Thus far, oil prices have been driven higher while financial markets have been rattled. This could translate into higher energy, construction and living costs if supply disruptions persist.

Nonetheless, Singapore has been known to be a safe haven amidst global risks due to stable governance, the strong Singapore Dollar and a tested property market. Despite challenges faced by global markets, Singapore’s residential property market maintains a largely positive outlook for the foreseeable future. Over the years, Singapore has built a name for itself as a reputable wealth hub in the region, with local real estate being perceived as a quality asset offering stable rental yield for investors.

Separately, Singapore is experiencing a significant wave of wealth transfer. This is largely fuelled by an affluent middle class whose wealth base has been solidified by the rapid appreciation of their housing assets. With Singapore’s aging population, an acceleration in wealth transfer is to be expected. However, while this influx of capital will empower future generations financially, it could also widen the existing societal wealth gap. With the rising instability in the middle east, we could see further wealth transfers and investments coming to our shores.

With Singaporeans' strong belief in real estate investment, much of the anticipated acceleration in wealth transfer will likely benefit this market. We already see this as older homeowners right-size to unlock housing equity for liquidity, and younger buyers receive parental support for property purchases. Accordingly, this influx of capital will sustain long-term demand and price appreciation across Singapore's residential market.

In 2026, the private residential market is expected to remain resilient, with moderate price growth supported by strong owner-occupier demand and ongoing right-sizing trends. Healthy take-up rates from recent project launches reinforce this positive outlook. This underlying demand has also encouraged developers to commit to new projects, indicating that the development pipeline and future housing supply will continue to be supported by strong market fundamentals.

Buyers can also look forward to a pipeline of 18 private residential projects, and 5 EC launches this year. Barring any unforeseen circumstances, ERA Singapore projects new home sales to be between 9,000 and 10,000 units.

Table 4: Upcoming launches in 2026

I confirm that I have read theprivacy policy and allow my information to be shared with this agent who may contact me later.