Hougang Central - Government Land Sale (GLS) Site Analysis

- ERA Singapore

- 9 min read

- Research

- 16 Dec 2025

URA launched the tender for the Government Land Sale (GLS) parcel at Hougang Central for a commercial and residential (non-landed) development on 29 May 2025. The tender subsequently closed on 27 November 2025. It drew attention from three bidders, with the top bid of $1.50 billion (or $1,179 psf ppr) submitted by Horizon Residential Pte. Ltd. and Horizon Commercial Trustee Pte. Ltd., a consortium comprising of CapitaLand Development and UOL Group.

The last mixed-use GLS site sold in the Hougang area was along Upper Serangoon Road, which was later developed into Stars of Kovan. The site was fiercely contested by 11 bidders, reflecting bullish sentiment stemming from its location near Kovan MRT station. It was subsequently awarded to Asset Legend Limited at $276.8 million or $848 psf ppr in November 2014.

Site Details

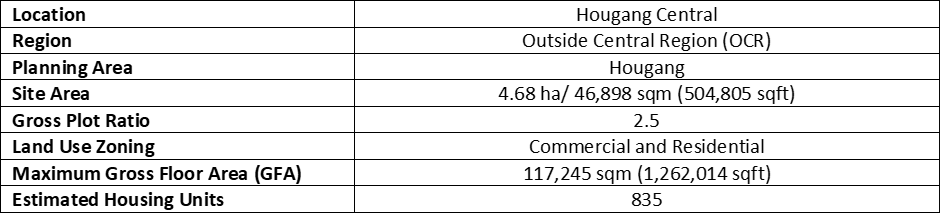

Table 1: Details of Hougang Central GLS site

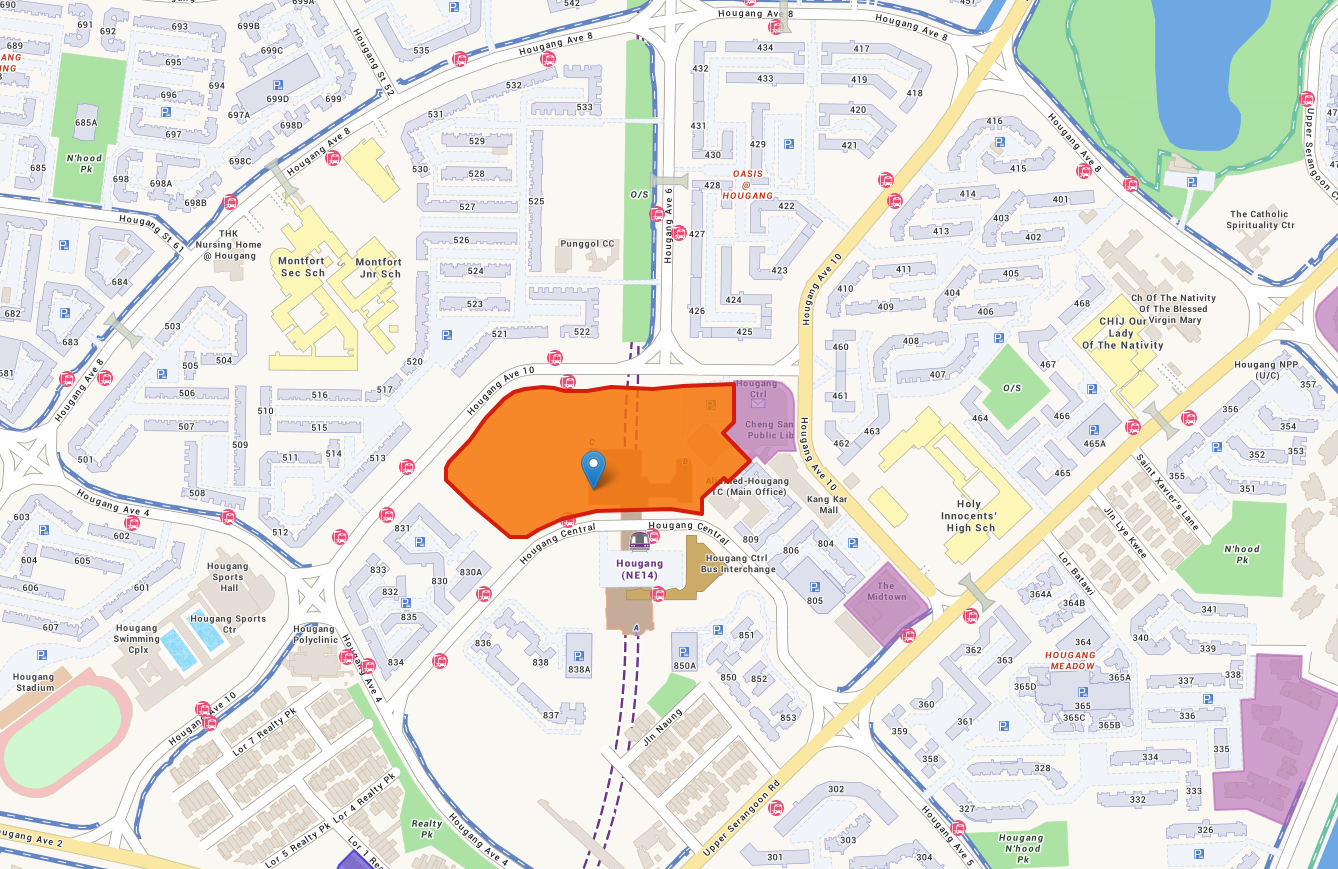

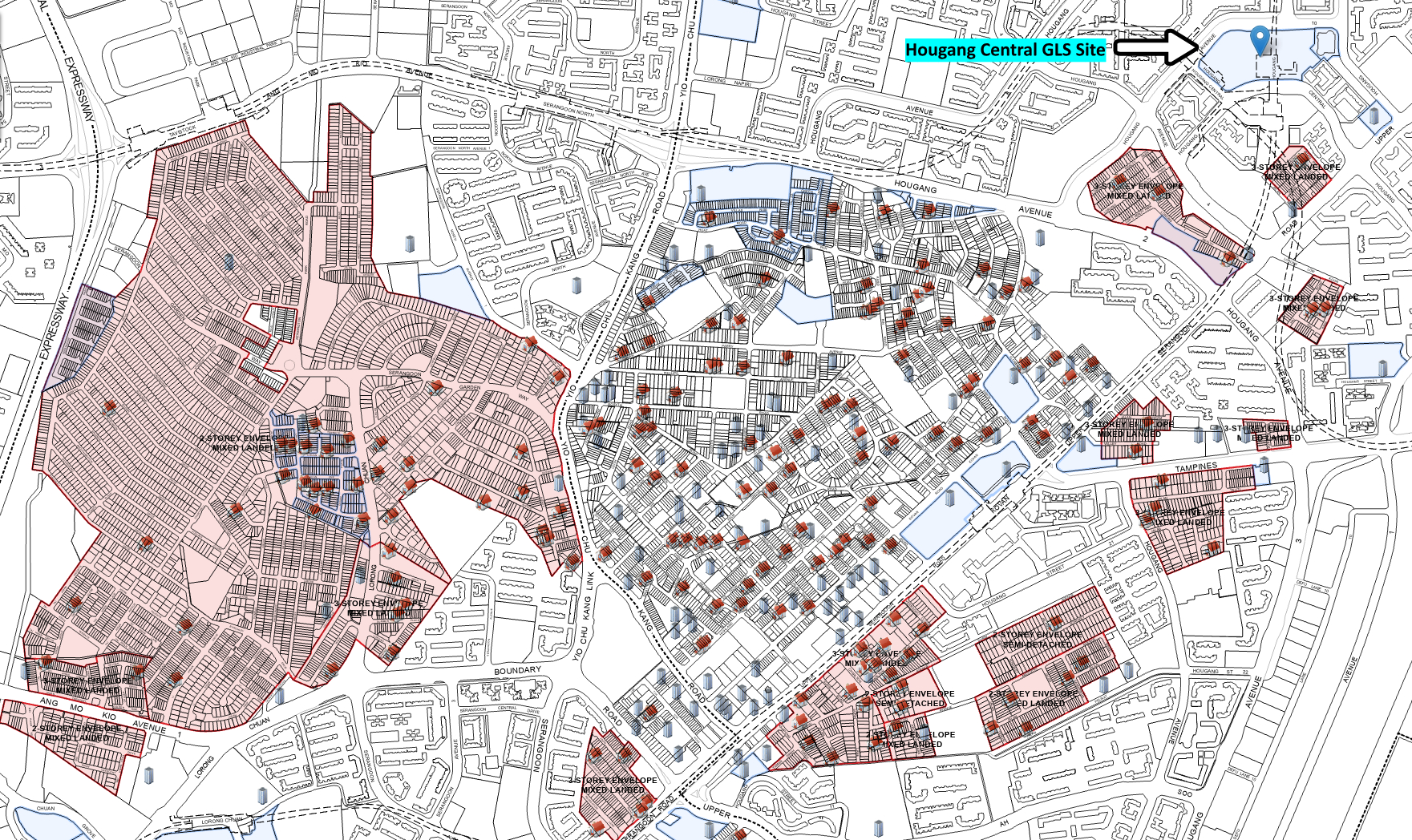

Figure 1: Map of Hougang Central

The Hougang Central plot is situated within the town’s centre and this puts it in close proximity to key neighbourhood amenities, including Hougang MRT station, Hougang Bus Interchange, and Hougang Mall.

The site is also within walking distance of several HDB precincts, such as Hougang RiverCourt, Hougang Meadow, and Oasis@Hougang.

Although there is only one non-landed private development (The Midtown) in the vicinity of the site and Hougang Mall, several landed and condominium enclaves lie within a broader 1-2 km radius. These include various condo projects bounded by Hougang Avenue 7 and Upper Serangoon Road (e.g., Riverfront Residences, Rio Vista), as well as landed clusters around Lowland Road, Parry Avenue, and extending further out toward Serangoon Gardens.

Site and Locational Attributes

Neighbourhood amenities

Hougang Central is primarily anchored by Hougang Mall, which offers a range of eateries, retail options, and an NTUC supermarket for residents. The mall is currently undergoing phased renovations that began in 2Q 2025, with completion targeted for 3Q 2026. This refresh is expected to modernise its interiors and enhance connectivity ahead of Hougang MRT station’s integration with the Cross Island Line.

In addition to Hougang Mall, the area’s retail mix is supported by small-scale retailers and service providers, (e.g., neighbourhood bank branches and GP clinics) operating out of nearby shophouse rows.

Neighbourhood convenience will be further enhanced once the future mixed-use development on the Hougang Central plot is completed. It is expected to offer about 40,000 sqm of commercial space, which is nearly double Hougang Mall’s gross floor area (GFA) of just over 21,000 sqm. The larger footprint will allow it to support future retail demand, especially with the likelihood of a larger neighbourhood population taking root in Hougang.

Furthermore, several educational institutions in the neighbourhood are likely to fall within a 1 km radius of Hougang Central’s future development. These include CHIJ (Our Lady of the Nativity) Primary School, Punggol Primary School, Montfort Junior School, Yio Chu Kang Primary School, Holy Innocents’ High School, and Anderson Serangoon Junior College.

Transport and connectivity

Connectivity in Hougang Central is currently supported by both Hougang MRT Station and Hougang Bus Interchange, which are linked by an underground walkway. This will change when both facilities are merged within the future Integrated Transport Hub (ITH) on the Hougang Central plot, giving residents a more seamless commuting experience with both MRT and bus services under one roof.

Upon completion of Phase 1 of the Cross Island Line (CRL) by 2030, Hougang MRT station will also become an interchange between the CRL and the existing North-East Line (NEL). This will enable Hougang residents to reach key stops in east and north-east Singapore more easily, such as Pasir Ris and Ang Mo Kio, which will likewise see CRL integrations.

Price and Market Trends

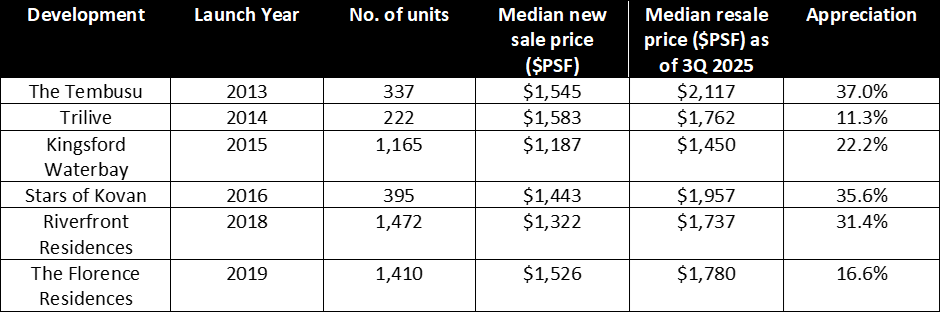

Through the years, recent condominium developments in Hougang have performed well, as evidenced by resale values appreciating beyond initial new sale prices. This trend is most pronounced in mainstream, non-boutique projects with over 100 units, which have seen price gains of between 11.3% and 37.0% since their respective launches.

Table 2: Price performance of condominium developments (with > 100 units) in Hougang

Home price appreciation in the area is likely supported by the robust suite of amenities in Hougang and nearby Serangoon. These conveniences include neighbourhood malls, such as Hougang Mall and Nex, along with MRT connectivity via the NEL. Moreover, with Phase 1 of the CRL slated for completion by 2030, Hougang is set to become an even more liveable location; this could further support residential demand and property prices in the area.

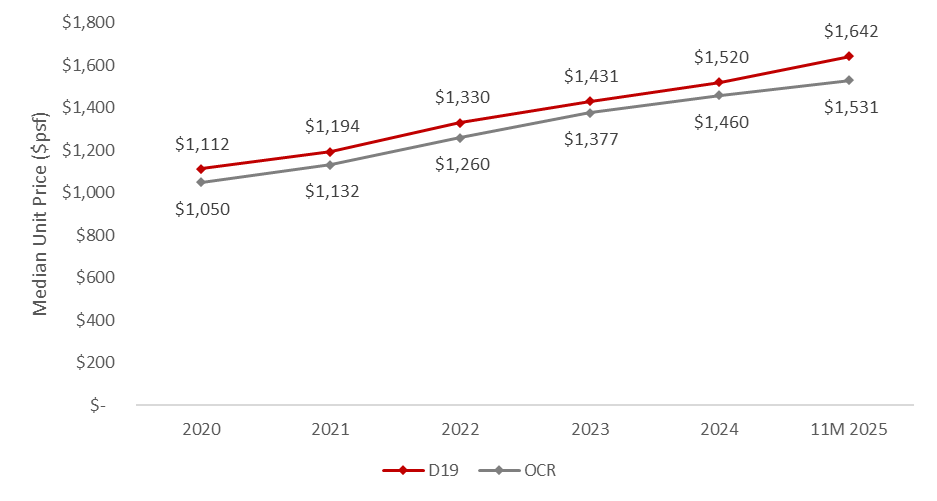

Steady Price Appreciation in District 19 vs OCR

Figure 2: Price performance of resale non-landed private homes in D19 vs Outside Central Region (OCR)

District 19 (D19) has maintained a steady track record of appreciation in the resale segment for non-landed private properties. Between 2020 and the first eleven months of 2025, median unit prices for resale condominiums in D19 rose from $1,112 psf to $1,642 psf, representing a growth of 47.7%. This performance closely matches and even slightly exceeds the uptick in median unit prices for OCR resale condominiums, which rose 45.8% over the same period, from $1,050 psf to $1,531 psf.

For interested homeowners, this steady growth trend could point to continued price appreciation in D19, especially if upcoming infrastructure projects improve overall liveability, both within Hougang and other regional towns.

Potential Demand/Buyer Profile

Table 3: Stock of non-landed and landed private properties in D19 towns

Given that Hougang’s last major condominium launches were Riverfront Residences (2018) and The Florence Residences (2019), there could be sufficient pent-up demand for a new non-landed project in the neighbourhood. In line with this, future interest and buying activity could reasonably come from private-property right-sizers and HDB upgraders, both within Hougang and across other D19 towns.

Figure 2: Landed home estates near Hougang Central

Within D19 itself, there are several landed property enclaves in Hougang and Serangoon where long-time owners might be interested in right-sizing into newer, more manageable homes. These neighbourhoods include pockets around Surin Avenue and Jalan Pelikat, as well as those along Parry Avenue and Kovan Road. Further west of the Hougang Central site lies Serangoon Garden, which is another longstanding landed estate in D19 where right-sizer demand could arise.

Table 4: Median quantum prices for D19 resale landed and new non-landed private homes in 3Q 2025

Moreover, based on recent median resale prices for D19 private properties, both landed right-sizers and owners of older condominiums should be well-positioned to purchase a new non-landed home in the area.

Table 5: Median resale HDB prices in D19 planning areas in 3Q 2025

Aspiring HDB upgraders in D19, especially those living in 5-room or executive flats, may also drive future demand. With median resale prices ranging from $700,000 to $1.05 million as of 3Q 2025, these flat owners will likely have sufficient starting capital for a new non-landed condominium in the area. Potential demand is also further amplified by the roughly 31,000 HDB flats (3-room or larger) in Hougang, Punggol, Sengkang, and Serangoon exiting their Minimum Occupation Period (MOP) between 2020 and 2026.

At the same time, Hougang Central’s strong locational attributes and upcoming infrastructure enhancements are expected to draw investors looking for strong rental prospects. Attractive upgrades that could interest future tenants include the CRL integration, future ITH, as well as additional retail options within the site’s future mixed-use development.

Conclusion

The Hougang Central site attracted only three bidders. This outcome was expected given its significant size and the extensive development considerations involved. The comparatively modest turnout reflects developers' measured and strategic approach to shaping a future landmark project in Hougang, and it is far from a reflection of soft sentiment.

While the land rate of $1,179 psf ppr appears modest when compared to other recently awarded sites, this is largely due to the sizeable land quantum. Despite nine sites being available on the 1H 2026 GLS Confirmed List, developers were not deterred from bidding for Hougang Central. Their interest signals continued confidence in the site’s strong attributes and positive market conditions.

If the site is awarded, this will mark CapitaLand and UOL’s latest foray into developing a mixed-use development integrated with a Bus Interchange. The two developers have a proven track record of executing such projects, exemplified by their successful partnership on Parktown Residence.

The narrow 2.1% price gap between the top two bids implies shared confidence among developers in the potential of the Hougang Central site. As the next anchor development in the North-East region, the project is well-positioned to capitalise on pent-up demand. It is likely to attract both HDB upgraders and landed right-sizers, considering that this is Hougang’s first private residential GLS plot in over a decade, since the Upper Serangoon Road site (now Stars of Kovan) was awarded in 2014.

Outlook

Singapore’s residential market is entering a renewed phase of optimism, underpinned by the exceptional sales performance of 2025’s launches. In the first eleven months of 2025 alone, developers have sold 10,754 new private homes (excluding Executive Condominiums), which is a significant 62.3% jump over the full-year count of 6,626 units for 2024. This momentum is likely to spur more developers to proactively replenish their land banks as they position themselves to capture the next wave of buyer demand.

Excluding ECs, six GLS sites currently remain open for tender, supplemented by another seven private residential plots on the 1H 2026 Confirmed List. By providing a diverse mix of sites across market segments, this pipeline ensures a consistent private housing supply, while supporting the Government’s efforts to stabilise land prices.

I confirm that I have read theprivacy policy and allow my information to be shared with this agent who may contact me later.