June 2025 Monthly Developer Sales Report: Investor Interest Persists for Smaller, Attractively-Priced Homes

- Stanley Lim

- 9 min read

- Research

- 15 Jul 2025

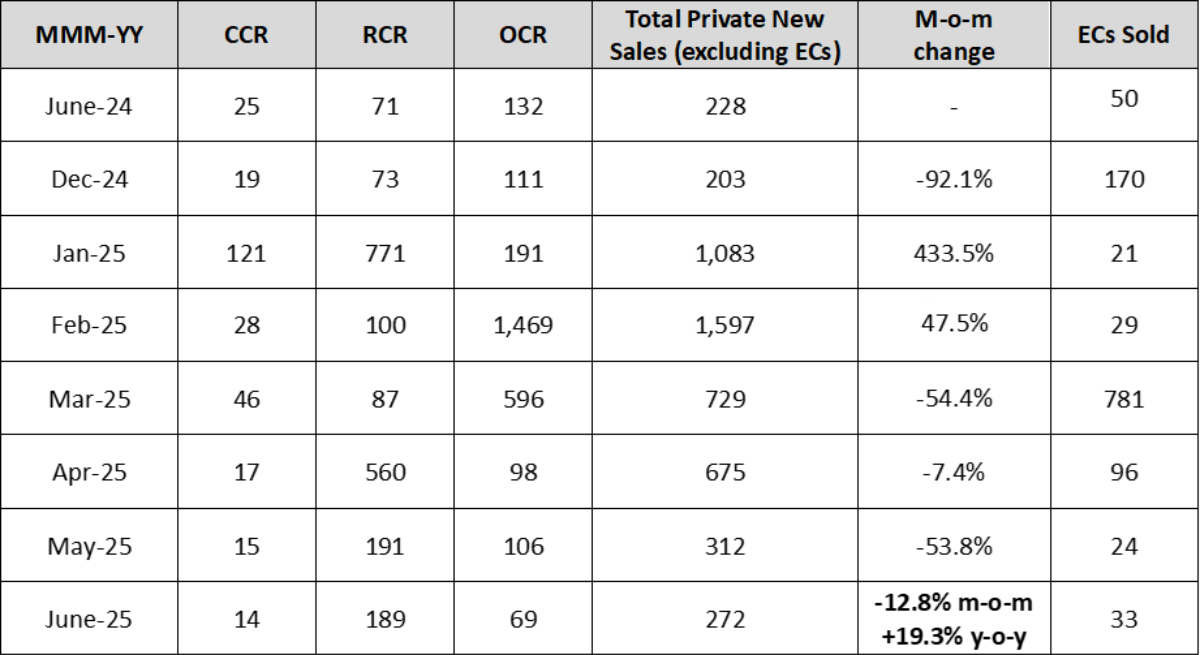

June 2025 saw developer sales coming in at 272 new private homes (excluding ECs), reflecting a consecutive 12.8% month-on-month (m-o-m) decline in transaction volume. The lower number of new home sales was chiefly due to developers holding back on new launches amid the traditional June school holidays.

The executive condominium (EC) market likewise saw muted sales due to a lack of launch activity, with just 33 units sold in June. While this performance reflects a sharp 37.5% m-o-m increase, the uptick comes off a low base in May, when just 24 new EC units were transacted.

Accounting for June’s developer sales, this puts the total number of new private homes (excluding ECs) sold in the first six months of 2025 at 4,622 units. This figure is a 144.7% increase on the 1,889 units sold across the same period in 2024.

Table 1: New Home Sales Over the Last Six Months

Source: URA as of 15 July 2025, ERA Research and Market Intelligence

Source: URA as of 15 July 2025, ERA Research and Market Intelligence

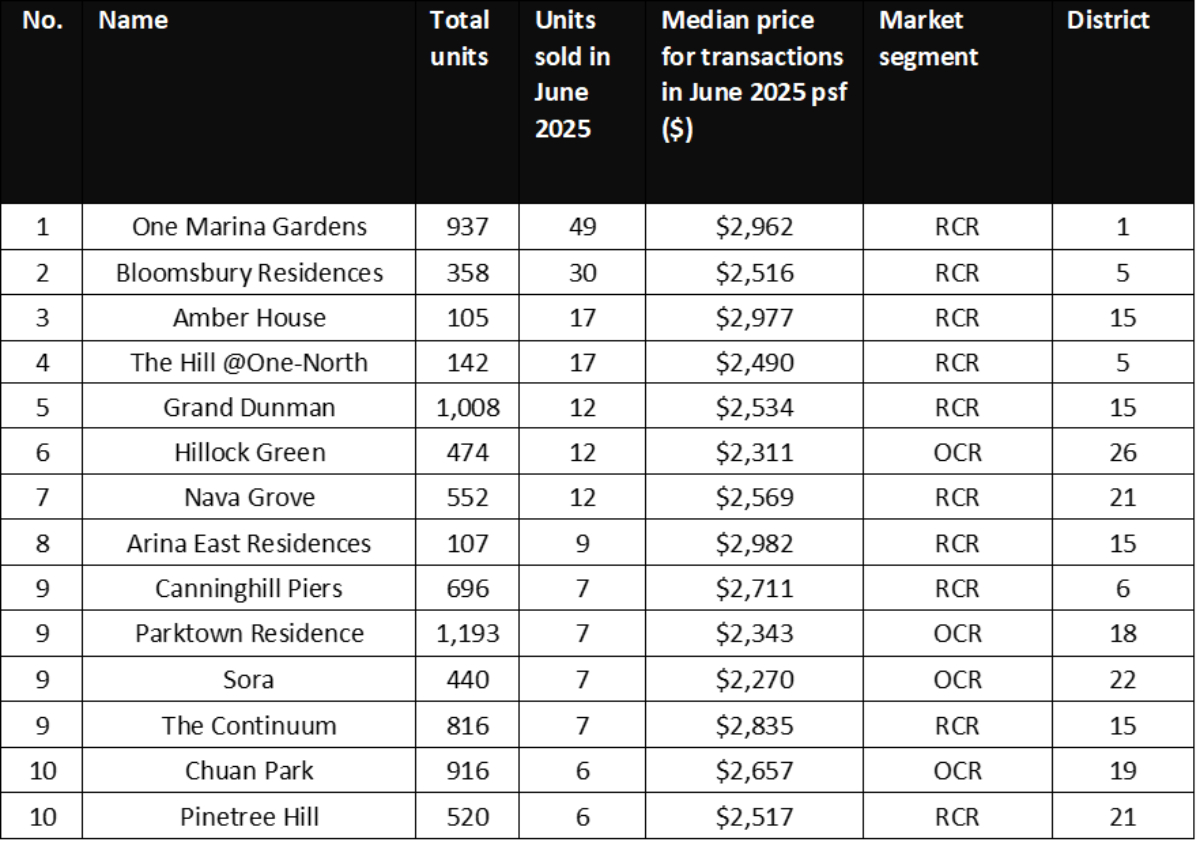

A total of two projects were launched in June, namely Arina East Residences by ZACD LV Development and Amber House by Far East Organization. Both developments are boutique in scale, comprising 107 and 105 residential units respectively.

Best Performing New Launches

Table 2: Top ten performing new launch project (excluding ECs) in June

Source: URA as of 15 July 2025, ERA Research and Market Intelligence

Source: URA as of 15 July 2025, ERA Research and Market Intelligence

Rest of Central Region (RCR) projects made up the majority of top-performing developments for June; this was largely due to depleting new stock in the Outside Central Region (OCR) and the relative lack of mass-market options in the Core Central Region (CCR).

For instance, popular OCR projects that launched earlier this year, such as Parktown Residence (1,193 units) and Lentor Central Residences (477 units) are close to being sold out, with take-up rates of 90.6% and 99.8% respectively. As a result, this led buyers to turn their attention towards available stock in the RCR.

One Marina Gardens maintains lead with smaller, attractively-priced units

Amid a quieter month characterised by smaller boutique launches, One Marina Gardens (937 units) continued to lead the new home market in sales during June. The Marina South project by Kingsford Group was launched in April, making it the maiden private residential project to debut in the area.

Of the 49 units sold at One Marina Gardens in June, over half (79.6% or 39 units) were smaller units in one- or two-bedroom configurations. June’s transactions also put One Marina Gardens at approximately 53.3% sold (499 out of 937 units), as of early July.

Caveat data also shows that one- and two-bedders at One Marina Gardens transacted at a median quantum of $1.2 million and $2.1 million respectively.

Such quantums likely appealed to investors, as they are in line with June’s median prices for similarly-sized new homes in District 1.

Additionally, One Marina Gardens is a RCR property near Singapore’s downtown core and just a short distance from Marina South MRT station. These locational advantages likely boosted its appeal to investors.

Bloomsbury Residences continues to see two-bedders snapped up

Mirroring its performance in May, Bloomsbury Residences once again emerged as the second top-performing new launch of June. As of early-July, the Media Circle development has sold 48.0%, or 172 out of its 186 available units.

Latest URA data shows that joint developers Qingjian Realty and Forsea Holdings moved a total of 30 units at Bloomsbury Residences in June. Furthermore, two-bedroom units made up the bulk of new home sales at Bloomsbury Residences, accounting for 63.0% or 19 units of its total monthly transactions.

Likewise, latest caveat data also shows that two-bedroom units at Bloomsbury Residences had a median quantum of $1.7 million. This falls in line with the median price for new non-landed private homes sized between 50 sqm to 70 sqm transacted in District 5 during June.

This palatable pricing, along with Bloomsbury Residences’ location within the one-north innovation district, likely drew buyers eyeing investment potential in the RCR market.

D15 properties see continued sales with launches of Arina East Residences and Amber House

Following earlier successful launches like Emerald of Katong and Grand Dunman, District 15 (D15) has continued to see a steady pipeline of new projects, with the latest being Arina East Residences and Amber House in June. Both are boutique freehold properties developed on en bloc sites, thus giving D15 buyers further options beyond larger mass-market leasehold projects.

Latest URA figures show that Arina East Residences sold a total of 9 units, representing about 8% of its 107-unit stock. At the same time, Amber House moved 17 units, or approximately 16.2% of its 105 available homes. Latest URA data also reflects a median unit price of $2,982 psf for Arina East Residences and $2,977 psf for Amber House.

Although take-up rates at Arina East Residences and Amber House were measured, such an outcome was anticipated due to the boutique nature and premium freehold price points of both projects. With no risk of lease decay, both freehold projects also present viable options for legacy planning.

Executive Condominiums (EC)

Owing to a lack of fresh supply, the EC market remained relatively quiet in June. In total, only 33 units were sold across existing developments including Aurelle of Tampines, Lumina Grand, North Gaia, and Novo Place. Additionally, following June’s sales, all EC projects in the existing pipeline have been fully taken up – barring a single unit at Lumina Grand as of early-July.

This exhaustion of available stock should create substantial demand for the upcoming launch of Otto Place at Tengah Plantation Close, which is expected to debut in July. This is in addition to the healthy response that neighbouring Novo Place saw during its November launch last year. Future EC supply will be further boosted by the yet-unnamed project at Jalan Loyang Besar, which could launch in 4Q 2025

Buyer Profile

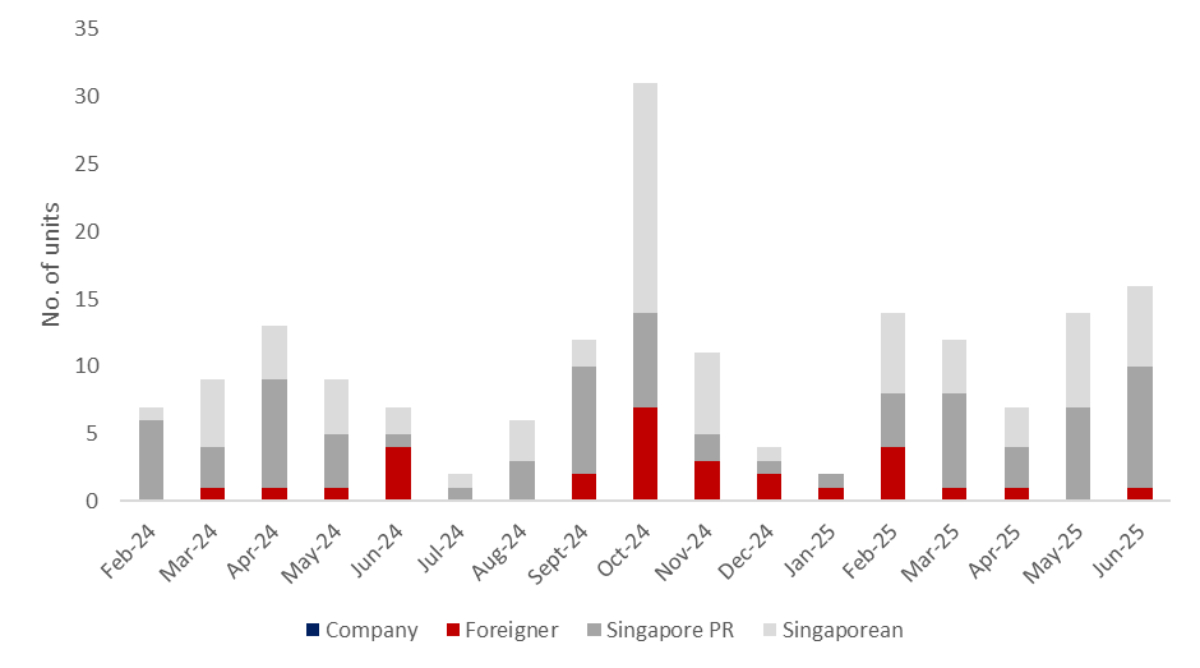

Chart 1: Buyer profile for all new non-landed homes excluding ECs

Source: URA as of 15 July 2025, ERA Research and Market Intelligence

Source: URA as of 15 July 2025, ERA Research and Market Intelligence

With the punitive Additional Buyer’s Stamp Duty still in effect, foreigner demand for new private homes continued to stay flat. June saw a total of four non-landed private home (excluding ECs) transactions made by foreign buyers, making up just 1.5% of the month’s total deals. Meanwhile, Singapore Permanent Resident (SPR) buyers clocked 36 transactions in June, accounting for 13.4% of all new private home (excluding ECs) purchases in the month.

Lastly, Singaporeans continued to dominate the market in June, accounting for 229 transactions or 85.1% of total new private home sales (excluding ECs) for the month.

Luxury Homes

Chart 2: Buyer profile for homes transacted at $5mil and more

Source: URA as of 15 July 2025, ERA Research and Market Intelligence

Source: URA as of 15 July 2025, ERA Research and Market Intelligence

In June, the luxury home market saw an uptick in activity with 16 new private residential transactions valued at $5 million and above. Demand in the month was primarily driven by locals and Singapore Permanent Residents, who accounted for six and nine transactions each. In contrast, only one high-end purchase was made by a foreigner within the $7 million to $8 million range.

The top three luxury transactions in June were all made by Singapore Permanent Residents (SPRs), involving ultra-luxury properties at Skywater Residences and 32 Gilstead.

The highest-value deal was for a 5,285 sq ft unit at Skywater Residences, which transacted at $30.8 million. The second and third priciest deals took place at 32 Gilstead, where two four-bedder units (both approx. 4,200 sq ft) were each sold for $15 million.

PR buyers seeking high-end properties may have been drawn to larger units at these ultra-luxury projects, both due to their large floor plates and coveted addresses. Homes at these projects also share several traits that appeal to high-net-worth buyers; these include freehold tenure, a small unit count, as well as greater privacy and exclusivity. Moreover, such properties are particularly attractive to affluent PR buyers, who face restrictions when purchasing landed homes in Singapore.

Closing Thoughts and Forecast

As it stands, July is poised to see a turnaround in May and June’s sales lull, with Lyndenwoods leading the rebound. Selling 324 out of 343 units (94%) during its launch weekend, the project at Science Park will be a major driver in lifting July’s developer sales. Likewise, the upcoming debut of Otto Place in July is also expected to revitalise the EC segment with much-needed fresh supply.

Come 3Q 2025, the market could see an estimated 4,154 new units launched for sale across various projects in Singapore. They will cater to a diverse range of buyer profiles, depending on their needs, lifestyles and preferred locations.

Looking towards the CCR, the region is set to see four new launches in 3Q 2025, following a relatively quiet pipeline in recent years. This fresh wave, which is also expected to support July’s developer sales, includes upcoming projects like UPPERHOUSE at Orchard Boulevard (301 units) and The Robertson Opus (376 units) that are slated to debut later in the month.

That said, new home sales in the CCR are still likely to progress at a more measured pace given their higher price point. Therefore, we expect the bulk of new home sales in 3Q 2025 to still come from upcoming RCR and OCR launches.

Collectively, 2H 2025 will see 15 new private home launches and 1 EC that will bring a total of 7,332 homes to market.

Shifting towards a broader perspective, we anticipate wider economic repercussions from ongoing global uncertainty and softer trade demand. These factors could dampen consumer sentiment, prompting homebuyers to exercise greater caution before committing to a purchase.

However, possible silver linings may be found in a potential interest rate cut by the Feds in July, as well as the recent 2025 Draft Master Plan announcements.

The latter saw the introduction of new housing neighbourhoods in areas such as Dover, Defu, Newton and Paterson, in addition to integrated community hubs in Sengkang, Woodlands North, and Yio Chu Kang on top of other initiatives. Together, these developments could help promote buyer confidence by reinforcing the Government's long-term plans for urban renewal and liveability.

Looking ahead, ERA projects new home sales to fall between 8,500 - 9,500 units for the whole of 2025.

Table 2: Upcoming launches in 2025

Executive Condominium

Source: ERA Project Marketing

Source: ERA Project Marketing

I confirm that I have read theprivacy policy and allow my information to be shared with this agent who may contact me later.