June 2026 Developer Sales: New Private Home Sales Fall by 65% Amid Absence of Fresh Stock

- Stanley Lim

- 6 min read

- Research

- 16 Jul 2026

June 2026 saw developer sales coming in at 156 new private homes (excluding ECs), reflecting a 65.1% month-on-month (m-o-m) decline in transaction volume. The lower number of new home sales was chiefly due to a sluggish launch calendar with developers holding back on new projects amid the seasonal school holidays.

As such, June joins February as the only months this year without a new project launch. This also represents the weakest monthly developer sales performance in four months, falling further from the 447 units sold in May.

In the EC segment, 28 new units were sold, marking a 39.1% decline on the month. Since May, EC sales have remained tepid following the gradual sell-out of recent launches, including Rivelle Tampines, which debuted in March this year. However, EC buying momentum could pick up towards the end of the year, with Wynwood Grand anticipated to debut in 4Q 2026.

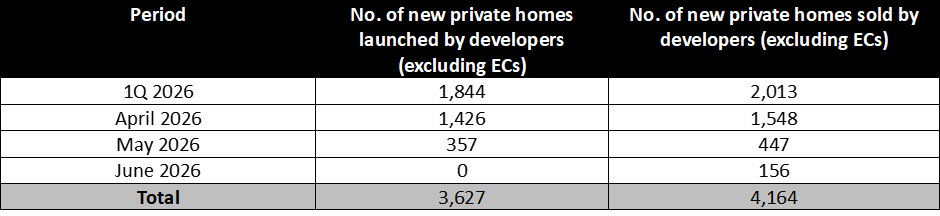

Table 1: New private home (excluding ECs) launched and sold by developers in first half of 2026

Based on URA's developer sales figures, developers have sold 4,164 private homes (excluding ECs) in the first half of 2026. This represents a 9.2% year-on-year (y-o-y) decline from the 4,587 units sold during the corresponding period last year.

Weaker sales in 1H 2026 were also accompanied by a sizeable decline in launch activity. Across the first six months of the year, developers launched a total of 3,627 units, which is 22.2% less than the 4,659 units recorded for 1H 2025. However, given that new home sales fell by a smaller margin relative to fresh supply, this suggests that underlying demand remains resilient.

June Sales Driven by Existing Launches, RCR Projects Continue to Dominate

With no new project launches in June, buying activity was largely concentrated in existing developments. RCR projects emerged as the main driver of sales, accounting for 84 units, or 53.8% of developer sales during the month. OCR projects followed with 57 units (36.5%), while CCR projects accounted for the remaining 15 units (9.6%). All ten of June’s best-selling developments were also comprised entirely of RCR and OCR projects.

Table 2: Top performing new non-landed projects in June 2026 (excluding ECs)

Hudson Place Residences topped developer sales in June, with 12 units sold at a median price of $2,577 psf. Of these, eight units, or two-thirds, were transacted below the $2.5 million mark, a pricing ‘sweet spot’ that continues to resonate with owner-occupiers.

Close behind were The Continuum and Union Square Residences, which each moved 11 units at median prices of $2,789 psf and $2,762 psf respectively. Chuan Park, an OCR project, also posted a similarly strong showing, with 11 units sold at a median price of $2,631 psf in June.

Similar to May, existing RCR projects continued to anchor monthly new private home sales. This trend could persist with the anticipated launch of Thomson Reserve in October. The 1,268-unit project at Bright Hill Drive is set to be the year’s largest new launch, and is expected to garner strong interest given its location in Bishan.

Lack of Fresh Launches Keeps EC Sales Tepid, Existing Stock Thins Further

In June, a total of 28 new EC sales were recorded, representing a 39.1% m-o-m decrease from the 46 units sold last month. Coastal Cabana continued to lead EC sales for the second month straight, recording 21 transactions at a median price of $1,836 psf. Meanwhile, Rivelle Tampines sold six units at a median price of $1,947 psf, while Lumina Grand recorded just one transaction at $1,732 psf.

This also marks the weakest monthly EC sales since February, when developers sold just 20 units amid shrinking stock. However, a turnaround could be on the cards by the end of the year with the anticipated launch of Wynwood Grand in Woodlands in 4Q 2026.

The project could see strong interest from second-timers, given that it is the first EC launch in the Woodlands planning area in almost a decade since Northwave debuted in 2016. It is also among the last EC projects to fall under the previous policy framework, meaning buyers will not be subject to the longer 10-year Minimum Occupation Period (MOP) and can still tap on the Deferred Payment Scheme (DPS).

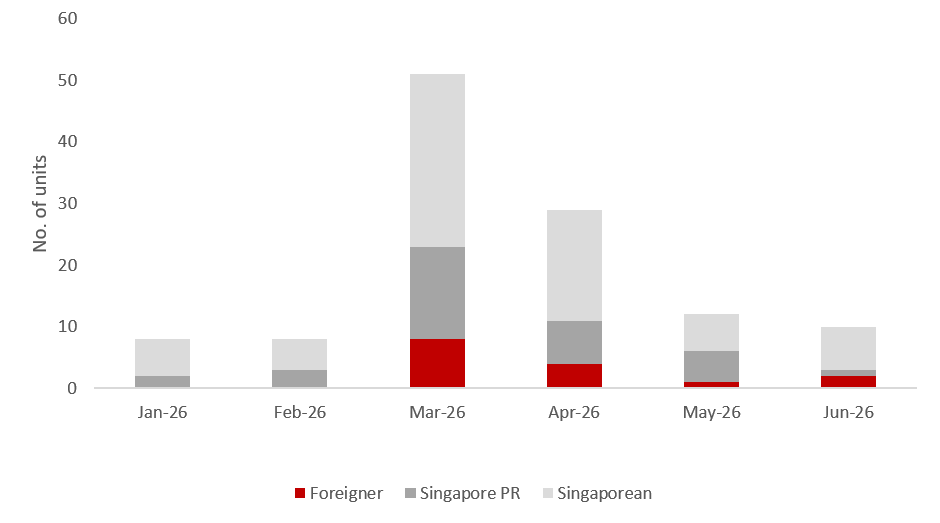

Chart 1: Buyer profile for all new non-landed private homes (excluding ECs)

Based on URA caveats data, foreign buying activity eased in June, accounting for just two transactions of units sold during the month. This was below the six-month average of 2.0% recorded for the first half of 2026.

In contrast, permanent residents accounted for about 20 transactions in June, while Singaporeans continued to dominate the market with approximately 128 transactions.

Luxury Homes

Chart 2: Buyer profile for non-landed private homes (excluding ECs) transacted at $5mil and more

Non-landed private luxury home transactions ($5M and above) fell from 12 transactions to 10 transactions in June. Singaporean Citizens (SC) made up half of the month’s luxury purchases, most of which were for large units in District 15 (D15), between the $5M to $6M price range.

The priciest non-landed private home transactions took place at Watten House ($7.75m, 5-bedroom, 2,368 sq ft) and Upperhouse at Orchard Boulevard ($7.18m, 4-bedroom, 2,055 sq ft), both CCR properties.

Prime residential properties in the CCR remain a strong draw for buyers who recognise the value of trophy assets in land-scarce districts. At the same time, Singapore’s political stability and regulatory transparency underpin its status as a safe haven, allowing luxury homes to serve as a long-term vehicle for wealth preservation.

Closing Thoughts and Forecast

As the year moves into its second half, Singapore’s property market is contending with a more challenging external backdrop, even as demand stays resilient. Following the recent flare-up in the US-Iran conflict in July, homebuyers and industry players may turn more cautious amid a more fragile global economic outlook. Higher energy prices could also translate into firmer launch prices over time, as rising costs work their way through the construction supply chain.

Even so, bright spots remain, including low mortgage rates and ongoing GDP growth, which continue to support homebuying sentiment. Moreover, with fresh offerings coming on stream in sought-after locations, July is poised to see a pickup in sales momentum, including Dunearn House (380 units) in the CCR and Lentor Garden Residences (499 units) in the OCR.

Both projects drew strong preview turnouts earlier this month and are expected to attract keen buyer interest, underpinned by their respective locational strengths. Dunearn House will be the first private residential launch in the highly-anticipated Bukit Timah Turf City, while Lentor Garden Residences enters a precinct that has consistently enjoyed strong buyer demand since its first launch in 2022.

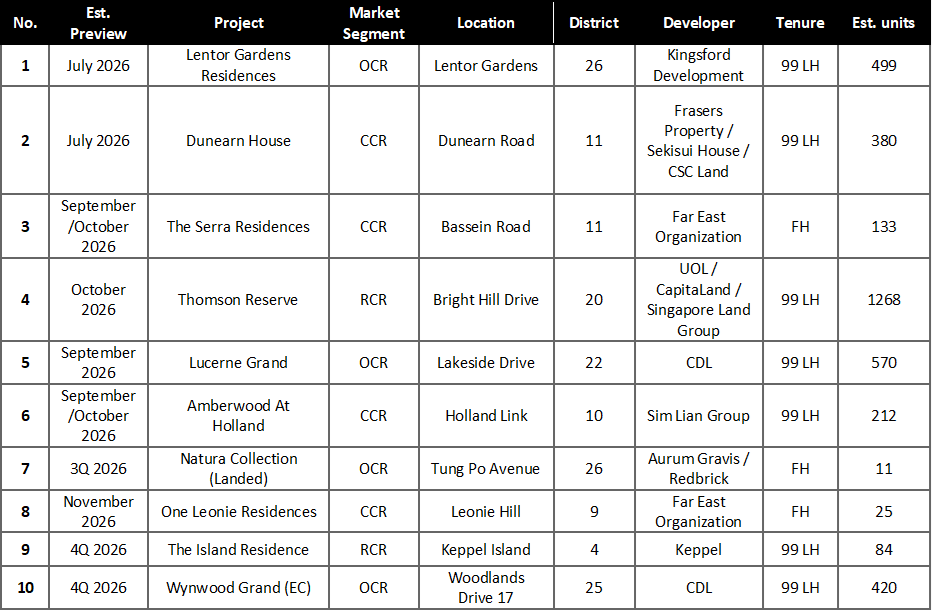

However, a leaner launch pipeline in 2H 2026 could cap overall annual transaction volume despite firm underlying interest this year. In the coming months, nine private residential projects and one EC development are slated to launch, adding close to 3,200 private homes and about 420 EC units to the market.

Against this backdrop, ERA Singapore expects new private home sales (excluding ECs) to reach around 9,000 units by year-end, barring any unforeseen circumstances.

Table 3: Upcoming launches in 2H 2026

I confirm that I have read theprivacy policy and allow my information to be shared with this agent who may contact me later.