Lentor Central - Government Land Sale (GLS) Site Analysis

- Stanley Lim

- 8 min read

- Research

- 4 Mar 2026

URA launched the tender for the Government Land Sale (GLS) parcel at Lentor Central for a residential development on 8 December 2025. It subsequently closed on 3 March 2026, and drew attention from five bidders. The top bid of $657.1 million (or $1,278 psf ppr) was submitted by a consortium comprising GuocoLand (Singapore) Pte. Ltd., Intrepid Investments Pte. Ltd. and TID Residential Pte. Ltd.

The site, situated in the Ang Mo Kio planning area, spans approximately 15,926 sqm and has an estimated yield of 560 private residential units.

Site Details

Table 1: Details of the GLS site

Location | Lentor Central |

Region | Outside Central Region (OCR) |

District/Planning Area | 26 / Ang Mo Kio |

Site Area | 15,926 sqm |

Land use zoning | Residential |

Maximum Gross Floor Area | 47,778 sqm |

Estimated housing units | 560 |

Source: URA, ERA Research and Market Intelligence.

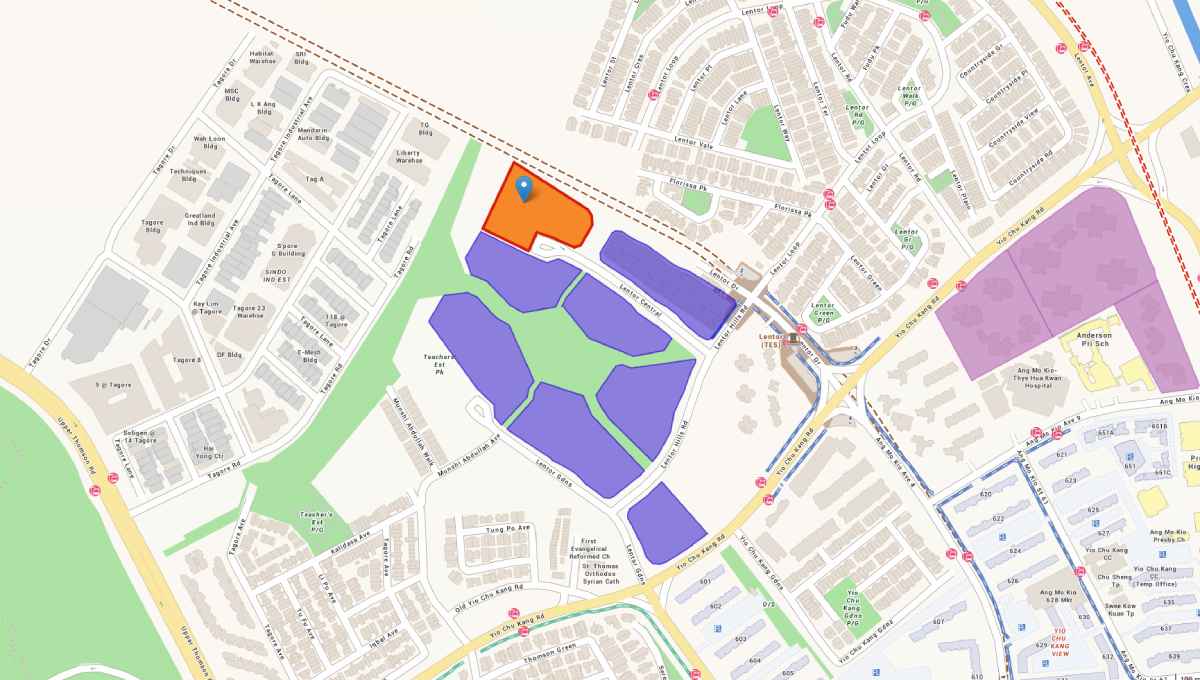

Figure 1: Map of Lentor Central

Locational Attributes

Like its predecessors, the Lentor Central site is located in District 26, where it is the eighth GLS parcel to be launched in the Lentor Hills estate. Barring further additions in future GLS programmes, it is also potentially the last plot to be made available in the neighbourhood at this point of time.

The site is located near the recently completed Lentor Modern, which includes an integrated retail component. It is also within a 10-minute walk of Lentor MRT station, enhancing connectivity and daily convenience.

The station’s location along the Thomson–East Coast Line provides direct access to key city destinations such as Maxwell, Orchard and Marina Bay, which could further strengthen the appeal of future homes to buyers working in the city.

Beyond its dedicated MRT station and integrated retail mall, Lentor’s appeal is further enhanced by its proximity to Ang Mo Kio. Residents benefit from easy access to key amenities such as Ang Mo Kio Bus Interchange, Ang Mo Kio Central Market & Food Centre, and Ang Mo Kio Polyclinic, as well as a wide array of everyday conveniences.

The future development at Lentor Central is also likely to be within a 1 km radius of Anderson Primary School, increasing its attractiveness for family buyers. From a lifestyle perspective, nature enthusiasts will value the precinct’s closeness to green spaces, such as Hillock Park and Thomson Nature Park, both offering accessible outdoor recreation facilities.

Residents can also walk, run and cycle at the nearby Thomson Nature Park located within a 15-minute walk (1km). The nature park spans over 50 hectares of land and is seamlessly connected to Upper Pierce Reservoir Park. Alternatively, Lower Pierce Reservoir Park is also a 7-minute drive away. Residents can appreciate the accessibility to these parks which offer green spaces for outdoor activities.

Price and Market Trends

Table 2: Sales performance of condominium developments in Lentor

Development | Launch Year | No. of units | Median new sale price ($PSF) | Percentage Sold |

Lentor Modern | 2022 | 605 | $2,108 | 100% |

Lentor Hills Residences | 2023 | 598 | $2,115 | 100% |

Hillock Green | 2023 | 474 | $2,168 | 98.3% |

Lentoria | 2024 | 267 | $2,207 | 89.9% |

Lentor Mansion | 2024 | 533 | $2,262 | 100% |

Lentor Central Residences | 2025 | 477 | $2,214 | 100% |

Lentor Gardens GLS | 2026 | 502 | N.A. | N.A. |

Source: URA as at 11 March 2026, ERAPro, ERA Research and Market Intelligence

Since the launch of Lentor Modern, new projects within the Lentor precinct have seen strong demand, with the six developments launched since 2022 now nearly fully taken up. Remaining inventory in the Lentor precinct is also limited, with Hillock Green and Lentoria together having only 35 units left.

This bodes well for upcoming launches, including the as-yet unnamed project at Lentor Gardens, as the limited remaining inventory in the precinct could translate into stronger sales potential. By the time the Lentor Central parcel is launched as fresh supply, this advantage could become even more pronounced as earlier projects are gradually sold out.

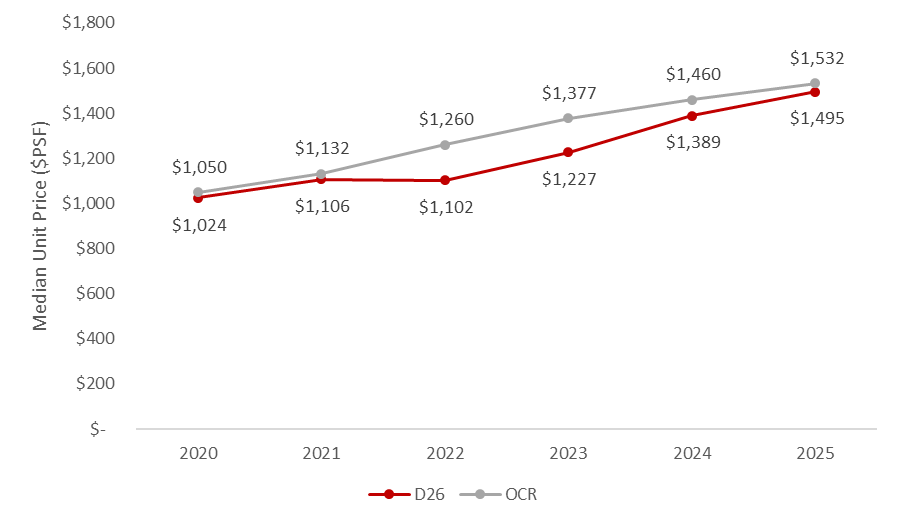

Figure 2: Price performance of resale non-landed private homes in D26 vs Outside Central Region (OCR)

From a broader perspective, prices of non-landed private homes in District 26 (D26), where the Lentor precinct is located, have also maintained an upwards trajectory over time. Between 2020 to 2025, median unit prices in the resale segment for D26 condominiums climbed by as much as 46.0%. This performance closely matches the uptick in median unit prices for OCR resale condominiums, which saw a 45.9% increase over the same period.

Potential Demand/Buyer Profile

Table 3: Stock of non-landed and landed private properties in D26 planning areas (4Q 2025)

| Planning areas | Non-landed private homes | Landed private homes |

| Ang Mo Kio | 6,321 | 4,551 |

| Yishun | 5,918 | 1,572 |

| Total | 12,239 | 6,123 |

Source: URA as at 11 Mar 2026, ERA Research and Market Intelligence

While Lentor has seen a string of condominium launches since 2022, demand for non-landed private homes in the area has remained resilient, as reflected in the healthy take-up rates across Lentor’s projects.

One possible reason is the sizeable stock of landed homes in nearby Ang Mo Kio and Yishun, which could provide a steady pool of potential right-sizers. As of 4Q 2025, these two planning areas have a combined total of about 6,123 landed homes. Examples of longstanding landed enclaves in both areas, include the Mayflower landed estate and Springleaf estate near Upper Thomson.

Table 4: Median quantum prices for D26 landed and new non-landed private homes in 2025

| Property type | Median quantum in 2025 |

| Landed (Resale) | $4,280,000 |

| Non-landed (Resale) | $1,778,000 |

| Non-landed (New) | $1,862,000 |

Source: URA as at 11 Mar 2026, ERA Research and Market Intelligence

Moreover, based on recent median resale prices for D26 private properties in 2025, both landed right-sizers and owners of older condominiums should be well-positioned to purchase a new non-landed home in the area.

Table 5: Median resale HDB prices in D26 planning areas in 2025

| Planning Area | 3-room | 4-room | 5-room | Executive |

| Ang Mo Kio | $440,000 | $597,944 | $910,000 | $1,105,000 |

| Yishun | $435,000 | $570,000 | $718,000 | $895,000 |

Source: HDB as at 11 Mar 2026, data.gov.sg, ERA Research and Market Intelligence

Aspiring HDB upgraders in D26, especially those living in 5-room or executive flats, may also drive future demand. With median resale prices ranging from $718,000 to $1.1 million as of 3Q 2025, these flat owners will likely have sufficient starting capital for a new non-landed condominium in the area.

Potential demand may also be supported by the roughly 1,834 and 6,534 HDB flats (3-room or larger) in Ang Mo Kio and Yishun respectively exiting their Minimum Occupation Period (MOP) between 2020 and 2026.

Conclusion

The turnout of five bidders for the Lentor Central parcel signals renewed appetite for Lentor sites, marking a notable turnaround from the prior Lentor Gardens tender, which saw only two bids submitted in April last year.

At $1,278 psf ppr, the top bid establishes a new benchmark for a fully residential site in Lentor, exceeding Lentoria’s land cost of $1,130 psf ppr in 2022. This likewise marks a return of developer confidence to the area, supported by current lean supply and healthy sales of past launches.

While some may have been skeptical about Lentor’s supply glut, it has proven otherwise. The new Lentor township has taken shape to be a choice estate for homebuyers, with ease of amenities and connectivity at its doorstep, with demand healthy, shown by the take-up rates of previous launches.

With most existing projects in the estate substantially sold and limited unsold inventory remaining, the upcoming development could set a new pricing benchmark for the neighbourhood. This likely underpinned the developer’s confidence in bidding, supported by the view that the project may represent the final new-launch opportunity in the area, barring any future land releases.

The modest turnout of five bidders, versus OCR tenders at Bedok Rise and Bayshore Road, may reflect careful strategy on the part of developers. Developers are likely calibrating their land acquisition strategies ahead of larger upcoming OCR GLS sites at Bayshore Drive and Upper Changi Road in the 1H 2026 Confirmed List, both of which are expected to yield over 1,000 units each.

Recent tenders in the OCR, including Bayshore and Bedok Rise, have achieved record land rates, signaling elevated entry costs in the region.

Market Outlook

With greater geopolitical tensions worldwide, with stability further being tested with global conflicts between Israel, Iran and the United States, there could be fears of further economic uncertainty. Thus far, oil prices have been driven higher while financial markets have been rattled. This could translate into higher energy, construction and living costs if supply disruptions persist.

Nonetheless, Singapore has been known to be a safe haven amidst global risks due to stable governance, the strong Singapore Dollar and a tested property market. Despite challenges faced by global markets, Singapore’s residential property market maintains a largely positive outlook for the foreseeable future. Over the years, Singapore has built a name for itself as a reputable wealth hub in the region, with local real estate being perceived as a quality asset offering stable rental yield for investors.

Separately, Singapore is experiencing a significant wave of wealth transfer. This is largely fueled by an affluent middle class whose wealth base has been solidified by the rapid appreciation of their housing assets. With Singapore’s aging population, an acceleration in wealth transfer is to be expected. However, while this influx of capital will empower future generations financially, it could also widen the existing societal wealth gap. With the rising instability in the middle east, we could see further wealth transfers and investments coming to our shores.

With Singaporeans' strong belief in real estate investment, much of the anticipated acceleration in wealth transfer will likely benefit this market. We already see this as older homeowners right-size to unlock housing equity for liquidity, and younger buyers receive parental support for property purchases. Accordingly, this influx of capital will sustain long-term demand and price appreciation across Singapore's residential market.

This has provided continued strong demand for sites from developers. Their strong appetite for land stems from a strong property market with genuine demand from buyers seeking a home for their own stay, rather than investors buying for speculation. Take up rates have been strong in recent launches despite new benchmarks.

I confirm that I have read theprivacy policy and allow my information to be shared with this agent who may contact me later.