March 2026 Monthly Developer Sales Report: 1Q Closes Out with Strong Sales Performance in the CCR and OCR

- Ethan Hariyono

- 9 min read

- Research

- 15 Apr 2026

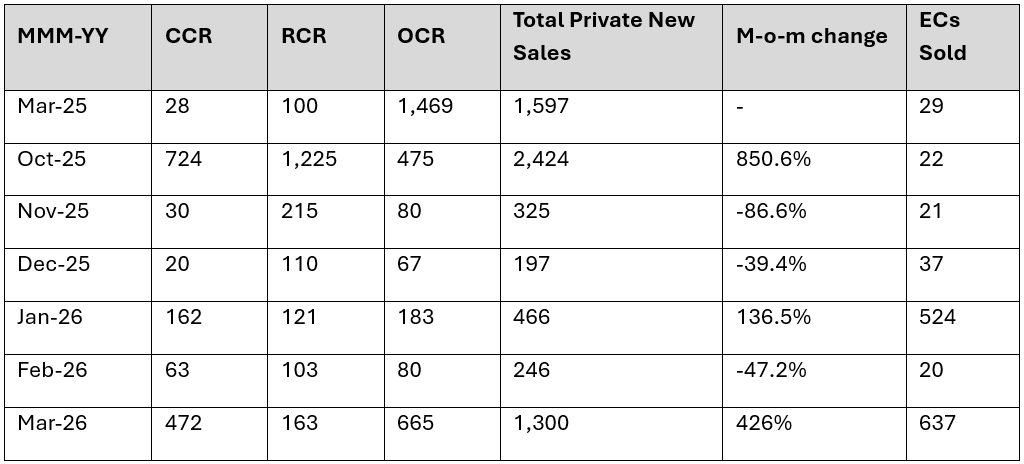

In March 2026, a total of 1,300 new private homes (excluding ECs) were sold by developers, marking a 428.5% month-on-month (m-o-m) uptick in transaction volume.

The primary market was galvanised by successful project launches during the month, including Pinery Residences, a mixed-use integrated project in Tampines West, and River Modern in the CCR River Valley precinct.

We saw voracious take-ups for these projects with Pinery Residences selling 543 (92.3% of its units) and River Modern selling 416 (91.4% of its 455 units), respectively.

The same sentiment was echoed in the Executive Condo (EC) market. Rivelle Tampines was the new EC launch in the month and saw 530 transactions, or 92.7% of its units sold. This brought the tally for new EC sales in March to 637 transactions, an increase of 3,085% m-o-m from the 266 units sold last month.

Following the March transactions, total new private home sales (excluding ECs) reached 2,012 units in 1Q 2026. Amid the typical festive slowdown associated with the Chinese New Year and Hari Raya, primary market sales have remained below ERA’s projected annual range of 9,000 to 10,000 units. However, momentum is expected to improve in subsequent quarters, supported by upcoming project launches.

Table 1: New home sales over the last six months (excluding ECs)

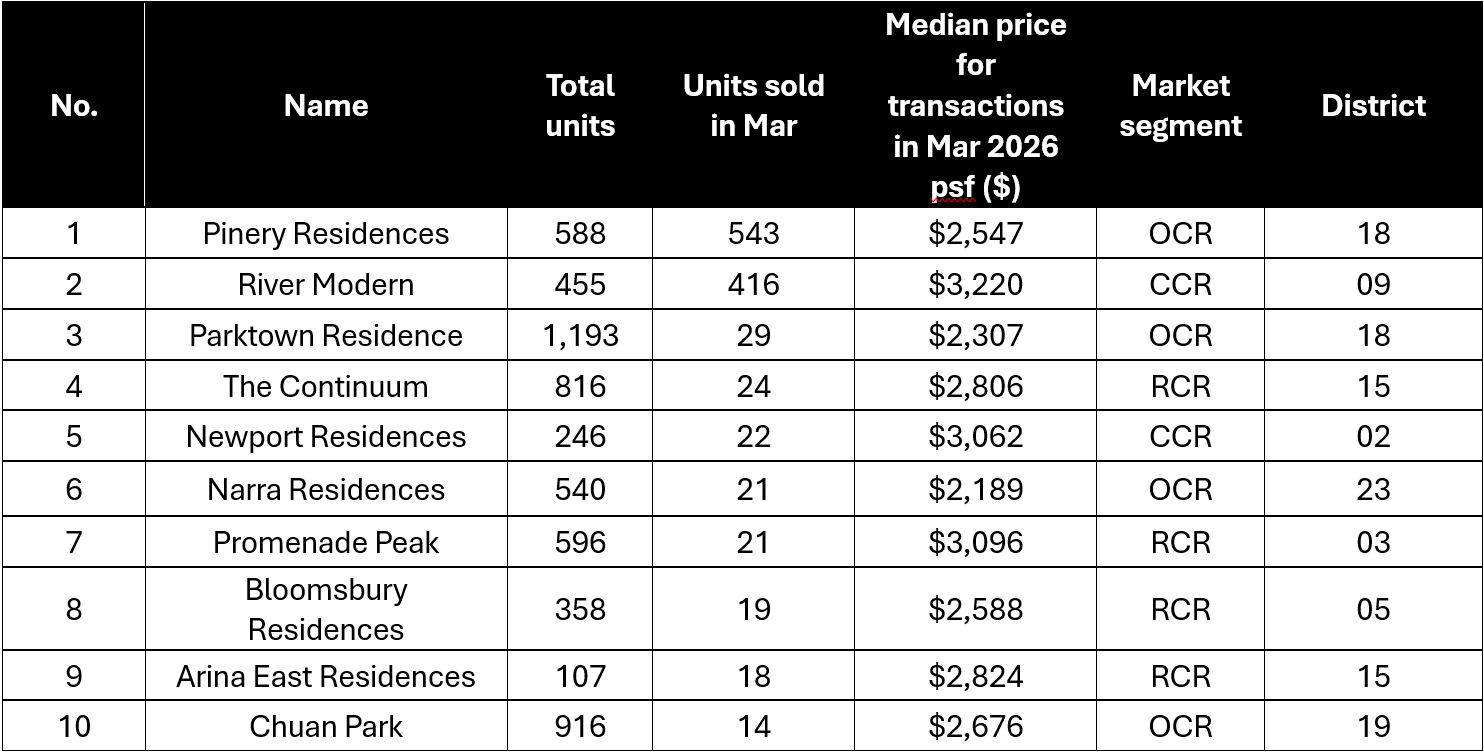

Mixed-Use Pinery Residences lead February new home sales

Pinery Residences was the best-selling project in March, with 543 (or 92.3%) of its total units sold. This highlights strong demand for well-sited OCR developments in mature estates.

The project is in Tampines, a mature estate and one of Singapore’s most established regional centres, with a steady supply of ready-upgraders.

HDB resale activity in Tampines included 88 million-dollar flat transactions and 2,660 MOP flats in 2025 and 2026. With a large supply of recently MOP-ed flats and a steady stream of million-dollar transactions, many upgraders are entering the market with substantial housing equity.

The project also features a 121,600 sq ft retail segment, Pinery Mall, which features underground integration to Tampines West MRT Station on the Downtown Line. These key attributes ensured that the project ticked most of the boxes for ready and willing upgraders.

The strong reception to the launch of Pinery Residences reflects demand for mixed-use developments in mature estates with MRT connectivity. A similar trend was observed at the launch of Parktown Residences in February 2025, a mixed-use development in Tampines that sold over 87% of its units on the launch weekend.

On the topic, Parktown Residences also moved a considerable 29 units, ranking third among new sale transactions. Movement at Pinery Residences resulted in spillover demand at Parktown Residences, with some buyers opting for the older project if they were unable to secure their choice unit at Pinery Residences, or due to a shorter completion timeline.

River Modern Impresses on Launch

River Modern was the sole other project launched in March and is also a mixed-use development. In contrast to Pinery Residences, which is situated within the Tampines heartland, River Modern occupies a prime CCR location in the District 9 River Valley enclave.

Despite this positioning, the development achieved a robust take-up rate of 91.4% by month-end, challenging the prevailing perception that CCR projects typically sell more slowly due to their higher price point. River Modern’s successful launch highlights the sustained appeal of well-positioned CCR developments.

Its strong demand reflects interest from upgraders and young families seeking family-friendly layouts, integrated commercial spaces, MRT access, and proximity to good schools, balancing liveability with investment value in a prime District 09 location.

Similar to Skye's launch performance in Holland the previous year, River Modern underscores that CCR developments with strong locational attributes and efficient unit configurations can remain compelling options for upgraders, despite their relatively higher price points.

Table 2: Top performing new non-landed projects in February (excluding ECs)

Rivelle Tampines Reinforces Demand for Executive Condominiums (ECs) in the East

March saw a total of 637 Executive Condominium (EC) units sold, a sharp 3,085% increase on the previous month.

The majority of the transactions took place at Rivelle Tampines, a highly anticipated EC launch in Tampines West, near the recently launched private condominium, Pinery Residences.

The performance of Rivelle at Tampines closely mirrors that of Aurelle of Tampines, another EC launched in March 2025, which sold over 90% of its units at launch. The projects share similar attributes, such as being located near an MRT station and an integrated development.

ECs in mature estates such as Tampines generally see higher demand, as reflected in its 92% take-up rate at launch. This can be attributed to its location in Tampines, one of Singapore’s largest and most-developed regional centres, as well as its proximity to an MRT station and the upcoming Pinery Mall.

The strong demand underscores the enduring appeal of ECs as a more affordable way to access private housing. Despite rising prices, ECs remain substantially cheaper than private condominiums, attracting HDB upgraders. Schemes such as the Deferred Payment Scheme and CPF Housing Grants enhance affordability, helping buyers manage initial costs and secure a new home more easily.

Rivelle Tampines’ 92% take-up at launch highlights significant pent-up demand, particularly in mature estates where new EC supply is scarce. Moving forward, the next phase of EC launches will focus on the North and West, with no immediate plans for supply in the East. This geographical shift underscores the limited EC options in mature eastern estates, a key factor driving demand in recent launches.

The remainder of the transactions mainly took place at Coastal Cabana, with 96 units sold. Buyers interested in a new East region EC may have been waiting for Rivelle at Tampines to launch, in order to weigh their options between Rivelle at Tampines and Coastal Cabana and make an informed decision.

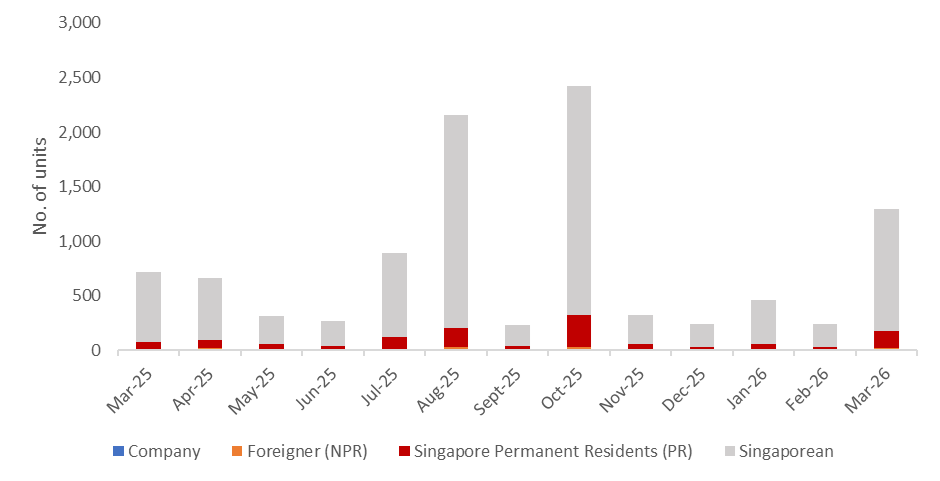

Buyer Profile

Chart 1: Buyer profile for all new non-landed homes

Alongside the pickup in developer sales, foreign buying activity also rose in March. As of 13 April 2026, foreigners accounted for 24 transactions in new non-landed private homes (excluding ECs). However, this figure still represents a small 1.9% share of total monthly sales, as the Additional Buyer’s Stamp Duty continues to weigh on foreign demand.

Meanwhile, Singapore Permanent Residents (SPR) accounted for 11.9% of March’s monthly sales, with 154 transactions recorded. Singaporeans also continued to dominate new private home market in March, making up 86.2% of monthly sales, or 1,116 transactions.

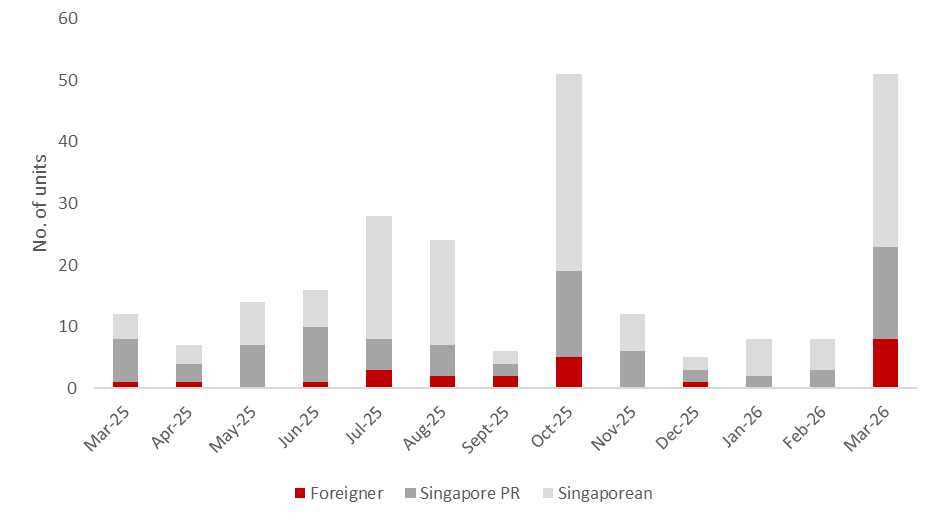

Luxury Homes

Chart 2: Buyer profile for homes transacted at $5mil and more

Luxury home transactions picked up sharply in March, with 51 new non-landed private homes (excluding ECs) transacting at $5 million and above. As of 13 April 2026, URA caveats indicate that eight of these high-value deals were made by foreigners, while SPRs accounted for 15 transactions. Singaporeans made up the bulk of luxury transactions in March, with 28 cases recorded.

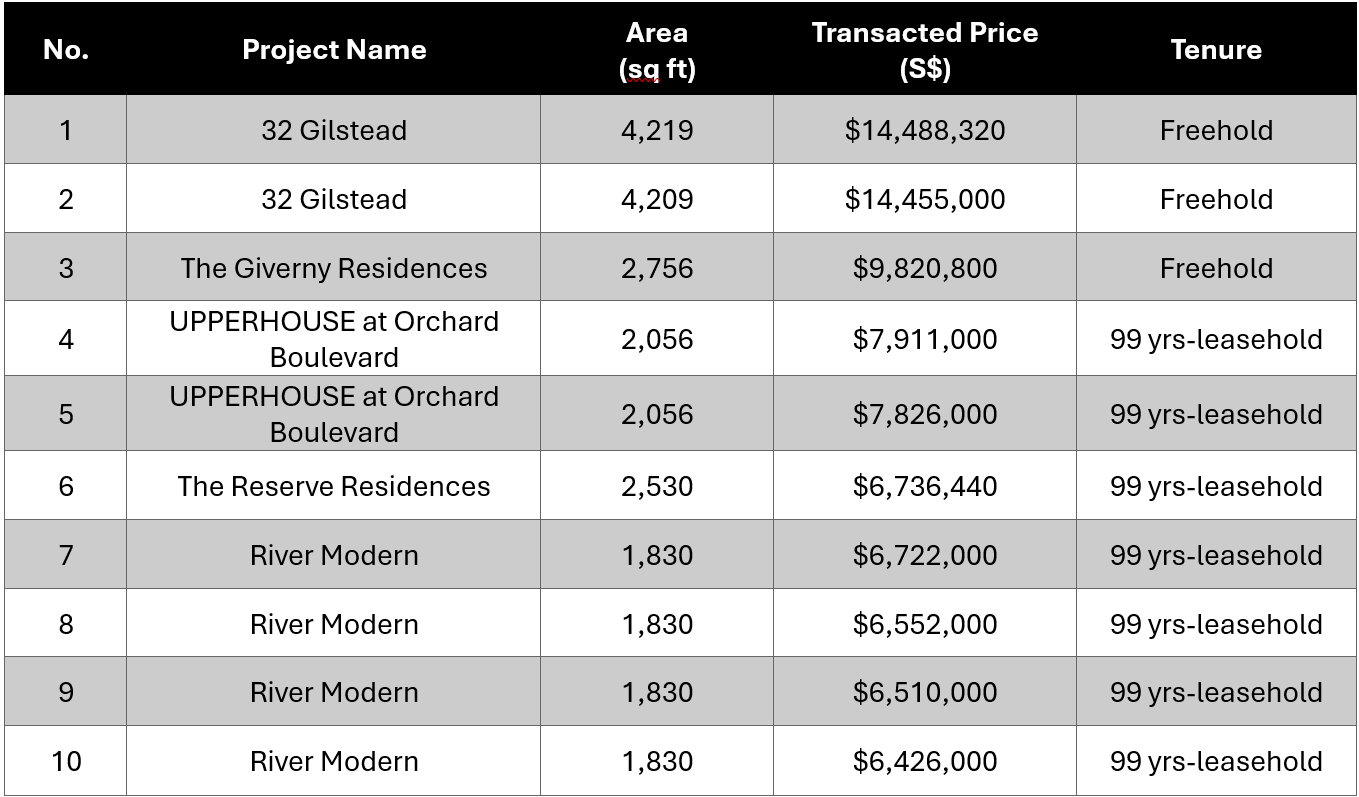

The two highest-value transactions in March were both recorded at 32 Gilstead and involved foreign buyers. Both deals were for four-bedroom units, with one 4,219 sq ft unit transacting at $14,488,320 and another 4,209 sq ft unit selling for $14,455,000.

The majority of March’s luxury transactions took place at River Modern, with 74.5% (38 out of 51) of such deals falling within the $5 million to $7 million range. These high-end purchases were also largely driven by the project’s four-bedroom (1,464 sq ft) and four-bedroom premium (1,830 sq ft) units.

This performance also indicates sustained local demand for well-located homes in the CCR, particularly given that River Modern is the only large-scale project in District 9 in 2026.

Table 3: Top Luxury Transactions for March 2026

Closing Thoughts and Forecast

With heightened geopolitical tensions worldwide, global stability could be further tested by conflicts between Israel, Iran and the United States, possibly triggering fears of economic uncertainty. Thus far, oil prices have been pushed higher, while financial markets have been rattled. This could translate into higher energy, construction and living costs if supply disruptions persist.

Nonetheless, Singapore is widely regarded as a safe haven amid global risks, thanks to stable governance, a strong Singapore Dollar and a tested property market. Despite challenges faced by global markets, Singapore’s residential property market maintains a largely positive outlook for the foreseeable future. Over the years, Singapore has built a reputation as a reputable wealth hub in the region, with local real estate perceived as a quality asset offering stable rental yields for investors.

Separately, Singapore is experiencing a significant wave of wealth transfer. This is largely fuelled by an affluent middle class whose wealth base has been strengthened by the rapid appreciation of their housing assets. With Singapore’s ageing population, an acceleration in wealth transfer is to be expected. However, while this influx of capital will empower future generations financially, it could also widen the existing societal wealth gap. With rising instability in the Middle East, we could see further wealth transfers and investments coming to our shores.

With Singaporeans' strong belief in real estate investment, much of the anticipated acceleration in wealth transfer will likely benefit this market. We already see this as older homeowners right-size to unlock housing equity for liquidity, and younger buyers receive parental support for property purchases. Accordingly, this influx of capital will sustain long-term demand and price appreciation across Singapore's residential market.

In 2026, the private residential market is expected to remain resilient, with moderate price growth supported by strong owner-occupier demand and ongoing right-sizing trends. Healthy take-up rates from recent project launches reinforce this positive outlook. This underlying demand has also encouraged developers to commit to new projects, indicating that the development pipeline and future housing supply will continue to be supported by strong market fundamentals.

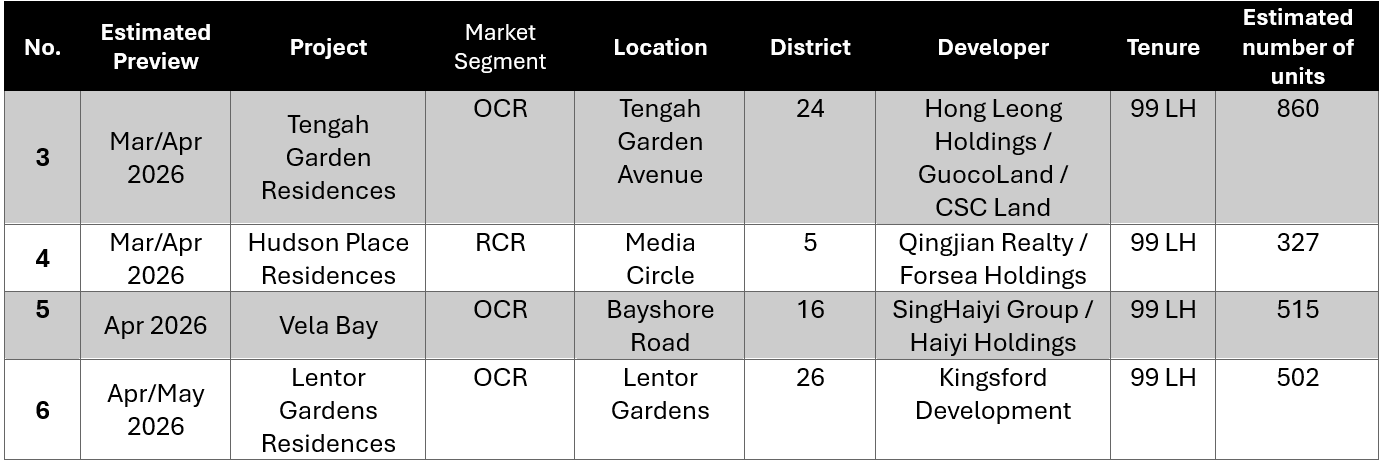

Buyers can also look forward to a pipeline of 18 private residential projects and 5 EC launches this year. Barring any unforeseen circumstances, ERA Singapore projects new home sales to be between 9,000 and 10,000 units.

Table 4: Upcoming launches in 2026

I confirm that I have read theprivacy policy and allow my information to be shared with this agent who may contact me later.