May 2026 Developer Sales: one-north’s RCR Value Proposition Draws Buyer Interest

- Ethan Hariyono

- 9 min read

- Research

- 15 Jun 2026

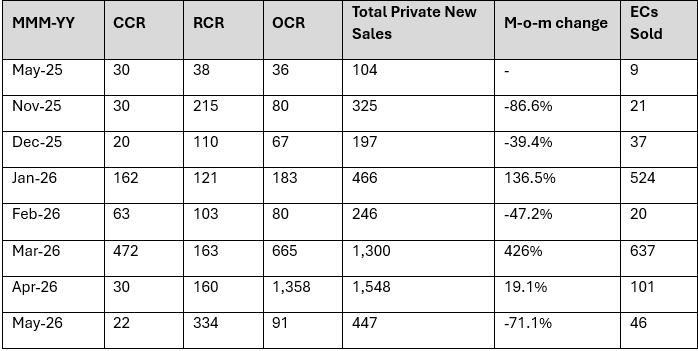

In May 2026, the new private home market saw a total of 447 units (excluding ECs) sold by developers. This marks a 71.1% month-on-month (m-o-m) decline in transaction volume.

This followed the high base in the preceding month of April, due to the tandem launches of Vela Bay and Tengah Garden Residences. The pair of Outside Central Region (OCR) projects saw strong take-up rates, resulting in over 1,500 new homes sold – the highest in 2026 so to date.

In May, we saw only one project launched, Hudson Place Residences located at Media Circle in District 5. The project launched to a positive reception, selling 209 (64%) of its 327 total units at a median price of $2,465 psf in the month.

In the EC market segment, 46 units were sold, marking a 54.5% m-o-m decline, as the stock of ECs under the previous set of measures continues to get snapped up.

Table 1: New home sales over the last six months (excluding ECs)

Hudson Place Residences Provides Strong Value Proposition Amidst a Backdrop of Growing RCR New Home Prices

Hudson Place Residences was May’s sole new launch, and subsequent best-selling project. Moving 209 (64%) of its 327 total units at a median price of $2,465 psf in the month, it represented 46.4% of all private new homes sold in the month.

Located at Media Circle in District 5 in the RCR, Hudson Place Residences is the second project launched in the neighbourhood, providing crucial private housing supply to support the growth of the one-north precinct. one-north is a key commercial and research node anchored by high-value, knowledge-based sectors including biomedical sciences, infocomm technology, media, science and engineering. This ecosystem is set to deepen further with the recently announced Kampong AI at LaunchPad @ one-north, which will bring together AI startups, researchers, corporates, capital partners and academia within Singapore’s first integrated startup community with both work and living spaces.

Beyond supporting the housing demand created by these robust and rapidly growing industries, Hudson Place Residences provides strong value proposition for buyers looking for new homes in the RCR market. The median new sale price of $2,465 psf reported at Hudson Place Residences was 6.5% lower than the 5-month RCR median of $2,635 psf, highlighting the underlying demand for affordably priced homes near in the city fringe, particularly among young families that hold jobs in one of one-north’s emerging industries.

This was further exemplified by the median price of the new homes sold – at just $1.71 million, units at Hudson Place Residences fell comfortably below the $2 million to $2.5 million sweet spot and a whopping 33% lower than the year-to-date $2.56 million median price for new RCR homes. This pricing strategy made the project appealing and affordable for HDB upgraders.

These upgraders may have identified the opportunity to purchase an RCR home in a market segment where new homes are growing increasingly more expensive. From April 2025 to April 2026, new home prices in the RCR have reported a year-on-year increase of 30% and an average increase of 5.7% per year over the last five years.

Furthermore, for the rest of 2026, we are likely to see only two more new launches in the RCR, namely Thomson Reserve (District 20), and the upcoming unnamed project at the Dorset Road GLS site (District 8). These projects, which tendered at a land rate of $1,178 psf ppr and $1,338 psf ppr respectively could launch at prices upward of $2,500 psf. The factor of affordability and limited stock in the market segment could then have spurred buyers to make a purchase at Hudson Place Residences this month.

Existing Stock in the RCR Continues to Move Amid Projected Low Supply

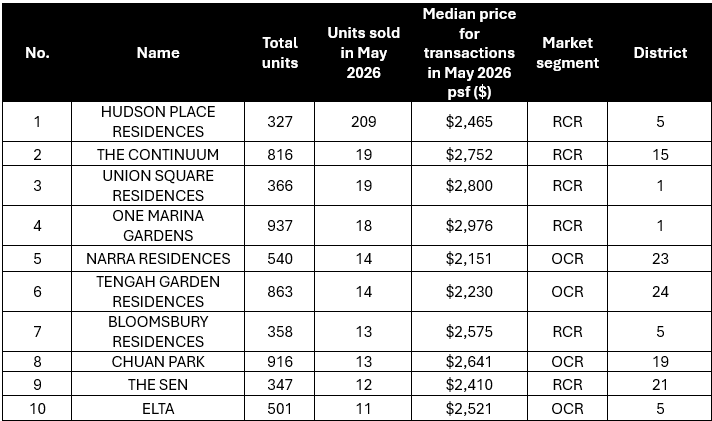

For the month of May, new home sales in the RCR made up a total of 64% of all primary market transactions. They also made up six out of the ten (or half of the) best-selling projects in the month.

The Continuum sold 19 units in the month, continuing its trend as a monthly top-seller. As RCR prices continue to grow, along with the market, its median price of $2,752 psf in the month has started to look more attractive to buyers given its freehold tenure in prime District 15, which has not seen a new project launch since 2024 and has no new projects in the supply pipeline.

Bloomsbury Residences also sold 13 units, benefitting from the momentum of the successful launch of Hudson Place Residences. The neighbouring project, also developed by QingJian Realty shares similar location attributes. Buyers could have been waiting to evaluate the different prices, project specific attributes, and floor plates before making an informed decision between the two projects, subsequently driving transactions.

Table 2: Top performing new non-landed projects in May 2026 (excluding ECs)

RCR new launch supply looks set to remain thin, with only the 1,268-unit Thomson Reserve and 428-unit (currently unnamed) project at Dorset Road GLS slated to launch by year-end. This resulted in the six RCR projects featuring in the top ten for new sale transactions in the month.

New launches in the RCR next year are likely to establish benchmark new home prices, following high land rates for GLS sites such as in Dover Drive and Tanjong Rhu Road (both 2H 2025 GLS). Buyers interested in making an upgrade to city fringe precincts might therefore be compelled to do so before the next wave of RCR new launches that look set to push the region’s prices upwards.

Remaining EC Stock Under Old Measures Continue to Gradually Sell Out Amidst Uncertainty Surrounding EC Scheme

In May, 36 EC sales were recorded, a 64.4% m-o-m decrease. This includes transactions for the last 11 units at Rivelle Tampines, which is now officially sold out.

The lower number of EC transactions in the month can be attributed to a dwindling overall stock of current EC supply. As of 15th June 2026, only 155 EC units are left on the market, which we can expect to be steadily snapped up by buyers in the coming months.

With new rules giving priority to first-timers at future EC launches, second-timer interest at upcoming projects, that are unaffected by the priority change, could rise further. This could be driven for those unwilling to wait out the two-year priority window for first-timers that applies to EC sites launched under the latest measures from 8 May onwards.

The three possible EC launches expected to be launched in the fourth quarter are located in Woodlands Drive 17, Senja Close, and Sembawang Road. We can expect strong interest among buyers for these projects as well, since they are also governed by the previous set of EC restrictions. They should receive strong buyer interest, particularly among second-timers.

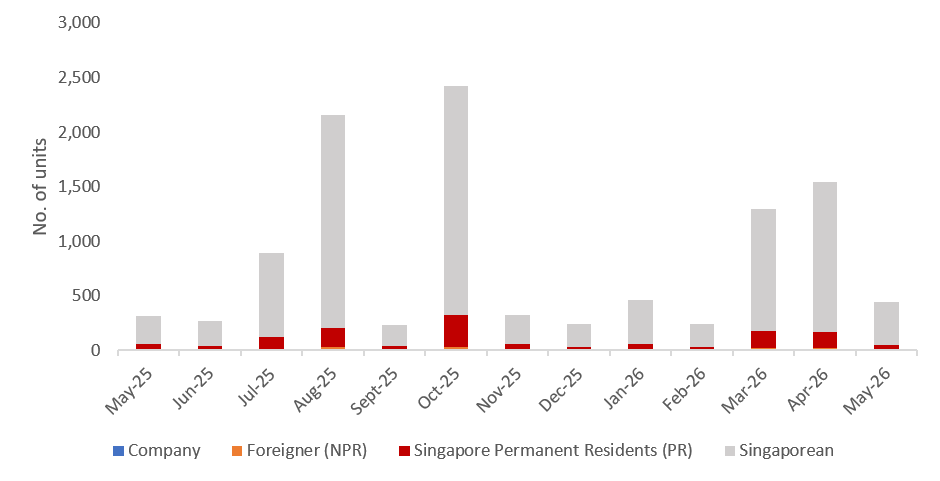

Buyer Profile

Chart 1: Buyer profile for all new non-landed private homes (excluding ECs)

Foreign buying activity remained firm for the month of May 2026, where foreign buyers made up eight transactions, or a 1.8% share of all equivalent deals that took place within the month. This is consistent with the 1.7% share recorded in the previous month and reinforces foreign buyers trust in Singapore’s firm economic fundamentals despite the prevalence of a high foreigner ABSD rate.

In comparison, Singapore Permanent Residents (SPRs) were responsible for 39 transactions or 8.7% of total monthly sales in May. At the same time, Singaporeans continued to dominate the new launch market, accounting for 403 transactions or 89.6% of all sales.

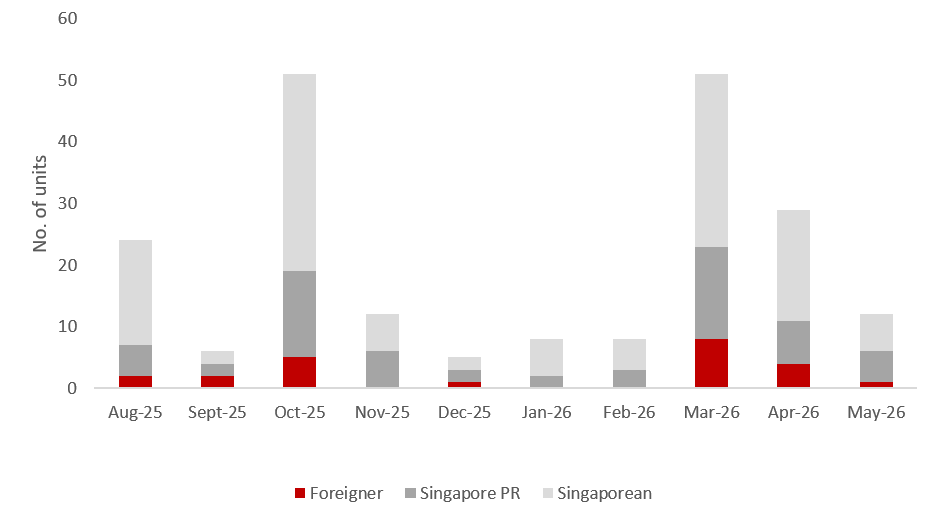

Luxury Homes

Chart 2: Buyer profile for non-landed private homes (excluding ECs) transacted at $5mil and more

Non-landed private luxury home transactions ($5m and above) fell from 29 transactions to just 12 transactions in May. Singaporean Citizens (SC) made up half of the month’s luxury purchases, most of which were for large units in District 15 (D15), between the $5m to $6m price range.

The transactions for these five-bedroom and larger units in the city fringe could be attributed to landed home right-sizers from the many landed enclaves in D15 who chose to purchase a new home with a longer lease and same number of rooms in a familiar estate.

Conversely, Singapore Permanent Residents (SPR) made up five transactions, almost on par with the number of luxury homes made by SCs. Purchases made by these SPRs include the two most expensive transactions in the month, north of the $14m mark.

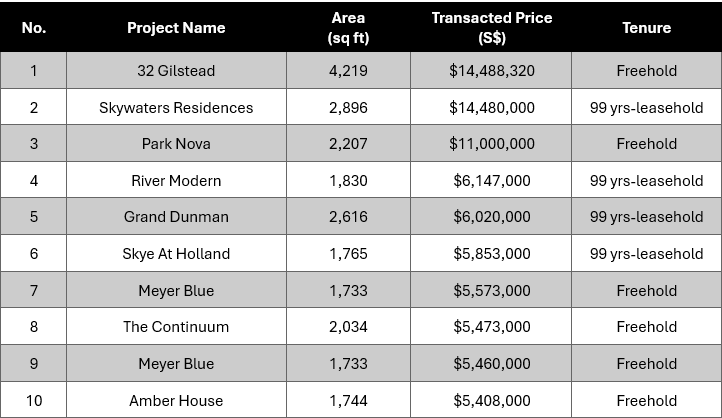

The highest record transaction in May was a 4-bedroom unit at 32 Gilstead which measuring 4,219 sq ft and transacting at $14.5 million ($3,434 psf). The premium pricing could be attributed to the sizable floor area, together with the limited availability of new private homes in the area which can be attributed to the lack of GLS sites – the last site tendered in Novena took place two decades ago) in 2006). Its coveted CCR location with proximity to reputable schools like Anglo-Chinese School (Junior), Anglo-Chinese School (Primary) and St. Joseph Institution Junior also contributed to its appeal.

Table 3: Top Luxury Transactions for May 2026

Closing Thoughts and Forecast

Despite heightened geopolitical tensions and their potential implications for the global economy, Singapore’s property market has stayed resilient. The steady take-up rates seen in 2026 thus far point to a selective yet confident buyer pool. Rather than broad-based enthusiasm, demand is increasingly focused on projects that combine strong locational advantages with a compelling value proposition.

At the same time, Singapore is relatively well-placed to weather external risks, supported by stable governance, a strong currency and a resilient economy.

Key drivers of local housing demand also remain intact. According to the Ministry of Manpower, Singapore’s labour market continued to expand in 1Q 2026, marking the 18th consecutive quarter of employment growth since end-2021. Unemployment and retrenchment rates have also stayed broadly stable, even as local employers have expressed greater hiring caution. Together, these factors have supported a market where buyers remain ready to commit.

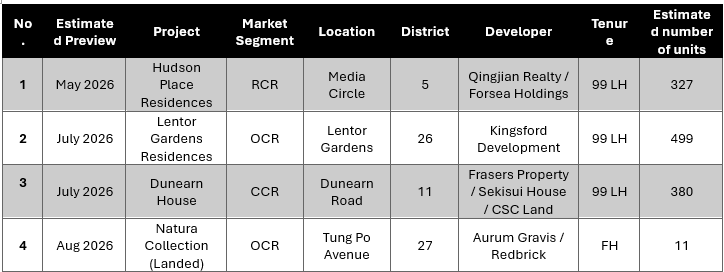

In the following month of June, we can expect tepid new sale performance, largely due to the seasonal lull, with families opting to travel during the June school holidays rather than participating in viewing and homebuying activities. The primary market should pick up its pace again come July and the start of 3Q 2026, with highly anticipated projects such as Dunearn House and possibly Lentor Gardens Residences slated for launch.

For the full year, buyers can expect a pipeline of 18 private residential projects, and five executive condominium launches in 2026. Barring unforeseen developments, ERA Singapore projects new home sales to reach between 9,000 and 10,000 units by year’s end.

Table 4: Upcoming launches in 2026

I confirm that I have read theprivacy policy and allow my information to be shared with this agent who may contact me later.