Miltonia Close - Government Land Sale (GLS) Site Analysis

- ERA Singapore

- 9 min read

- Research

- 15 Apr 2026

Site Details

| Location | Yishun (D27) |

| Region | Outside Central Region (OCR) |

| Planning Area | Yishun Ave 1 |

| Site Area | 1.54(HA)/15,451.2sqm |

| Gross Plot Ratio | 2.8 |

| Land Use Zoning | Executive Condominium |

| Maximum Gross Floor Area (GFA) | 43,264 sqm |

| Estimated Housing Units | 430 units |

Source: URA, ERA Research and Market Intelligence

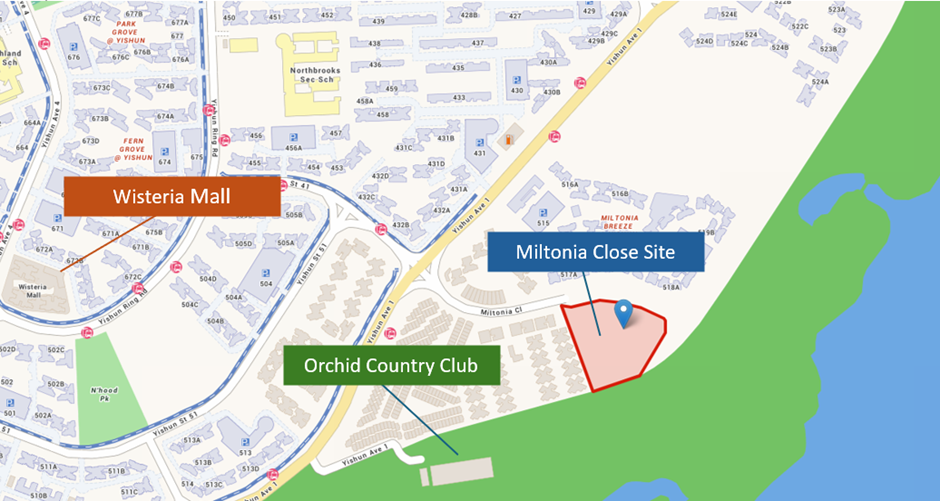

The Miltonia Close site is situated within commuting distance of two North South Line (NSL) MRT stations, being around a 15-to-20-minute bus ride from Khatib and Yishun stations. While this offers some level of connectivity, it also suggests that walkability to both stations is limited.

Nonetheless, this limitation is largely offset by connectivity via the NSL, as it enables direct connectivity to key central locations, including Orchard MRT station and the Central Business District (CBD), in under an hour. Yishun MRT station is also located in close proximity to Northpoint City shopping mall, which enables greater ease of access to dining, retail, and entertainment options.

The site also enjoys connectivity to the Seletar Expressway (SLE), which links directly to the Central Expressway (CTE), allowing future residents to reach the city in 20 minutes.

On a regional scale, Yishun will also undergo progressive transformation under URA’s Master Plan. For instance, the impending lease expiry for Orchid Country Club in 2030 will pave the way for its redevelopment into a residential site, subject to further planning. Similarly, the upcoming Chencharu housing precinct and proposed redevelopment of Yishun Industrial Estate along the Sungei Simpang Kiri waterfront could bring more residential projects and neighbourhood amenities to Yishun.

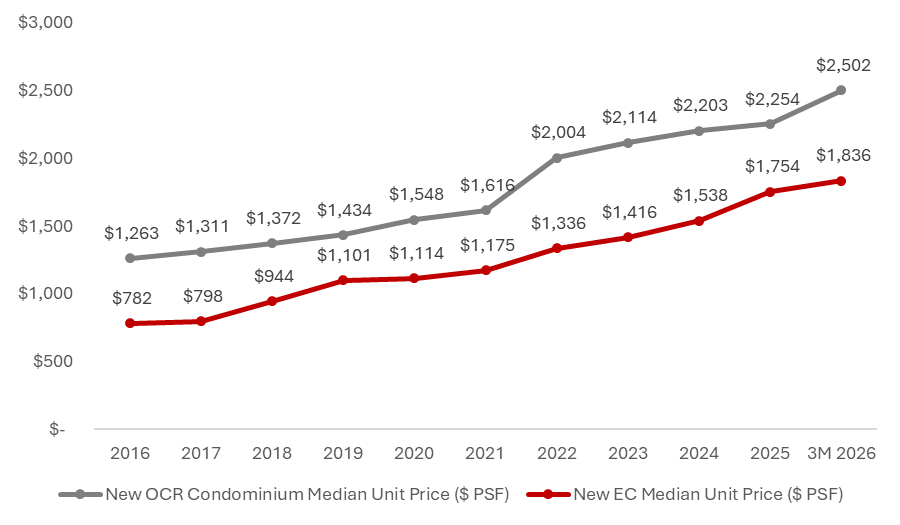

ECs are a popular choice amongst HDB upgraders

ECs have consistently been a popular choice among HDB upgraders. This is due to their more accessible pricing compared to private condos.

As of early 2026, there remains a sizeable gap in new home pricing between non-landed private homes and ECs within the OCR. This price differential highlights the value proposition of ECs, particularly for HDB upgraders whose household income do not exceed the income ceiling of $16,000.

Apart from commanding lower prices, ECs also offer an advantage when it comes to Additional Buyer’s Stamp Duty (ABSD). Unlike private condos, where HDB upgraders must first pay a 20% ABSD upfront before applying for remission, EC buyers (must be at least 1 SC) are exempted from this requirement. This reduces upfront cashflow, and improves the attractiveness of ECs for HDB upgraders.

Moreover, EC buyers may opt for the Deferred Payment Scheme (DPS), whereby they will only need to pay a deposit and defer their EC loan till after it has been completed. In this way, the buyers will not need to service two mortgages while waiting for their new home.

Potential Demand

Demand for this future EC development will come primarily from HDB upgraders in Yishun, although we could see interest from upgraders coming from nearby towns in the North, such as Sembawang and Woodlands. [EM1]

Between 2026-2029 itself, we may see over 2,500 (4-room and larger) flats fulfil their Minimum Occupation Period in Yishun, with a further almost 1,800 flats and 1,000 flats of such MOP flats in Woodlands and Sembawang respectively. This trend could create supply of potential HDB upgraders, which will strengthen prospect for future EC projects.

That said, Sembawang and Woodlands will see 2 EC launches this year at Woodlands Drive 17 and Sembawang Road. This influx of supply will significantly expand the pipeline of EC units coming up in the north region. As such, demand from prospective buyers could be diluted across the various projects.

As of 2025, there is currently no supply of EC within Yishun. The most recent launch was North Gaia in 2022, located just 10 minutes from this GLS site. It has been fully sold out since last year.

Across the broader market, available inventory remains tight as of end-April, with unsold stock remaining only at Coastal Cabana.

Table 3: New ECs available as of end-April 2026

| EC | Location | Market Segment | Launch Date | Take-Up Rate at Launch | Total Number of Units | Units Sold / % sold till date | Number of Units Available |

| Coastal Cabana | Pasir Ris | East | Jan 2026 | 66% | 748 | 605/80.9% | 143/19.1% |

Source: ERApro as 29 April 2026, ERA Research and Market Intelligence

Table 4: ECs launch-launch frequency in Yishun

Project Name

|

Location |

Year | Launch-to-launch intervals (years) |

| North Gaia | Yishun Avenue 9

| 2020 | - |

| Signature at Yishun | Yishun Street 51 (Parcel B)

| 2014 | 6 |

| The Criterion | Yishun Street 51 (Parcel A)

| 2014 | 0 |

| One Canberra | Yishun Avenue 7/Canberra Drive

| 2011 | 3 |

| The Canopy | Yishun Avenue 11

| 2010 | 1 |

| Lilydale | Yishun Avenue 6

| 2000 | 10 |

| Average: | 4 Years |

Source: URA, ERA Research and Market Intelligence

The last EC project to launch in Yishun was North Gaia, which was introduced to the market five years ago. This significant time gap highlights the tight EC supply within the area, while also signalling the likelihood of pent-up demand. This could compel developers to bid more competitively for the site to seize the opportunity to plug the gap in this market segment.

Developers must be cautious because of buyers’ affordability

Due to the income ceiling of $16,000, as well as the Mortgage Servicing Ratio (MSR) and Total Debt Servicing Ratio (TDSR), the maximum loan a buyer can borrow is approximately $1.01 million. Amid rising EC prices, and a cap in loan quantum, EC buyers will now have to satisfy a larger initial cash outlay.

This may potentially deter upgraders to enter the EC market, instead opting for full private condominiums. Although they come with a higher price tag, buyers may only need to put a lower downpayment. Moreover, they can take a larger loan as private properties are only subjected to only the TDSR, and not the MSR.

The tender for the Government Land Sale (GLS) site at Miltonia Close closed today, on 14 April 2026. It drew attention from three bidders, with the top bid of $340.9 million (or $732 psf ppr) submitted by Hoi Hup Realty Pte Ltd.

“Participation was relatively measured, with three bidders and a top bid of $732 psf ppr, suggesting a more selective approach by developers towards EC sites in Northern Singapore. This comes amid robust EC supply in the region, which likely shaped a more calibrated bidding strategy as developers balance land acquisition against future launch positioning,” said Eugene Lim, Key Executive Officer, ERA Singapore.

“Tenders for two EC sites at Canberra Drive and Sembawang Drive, with an estimated 185 and 450 units each, are slated to open in May and June this year under the 1H 2026 GLS programme.

This is on top of the strong EC project pipeline in the North, including developments at Woodlands Drive 17 and Sembawang, which are anticipated to launch by next year. Together, these additions represent a more competitive supply landscape for ECs in the region.

Conclusion

The tender for the Government Land Sale (GLS) site at Miltonia Close closed today, on 14 April 2026. It drew attention from three bidders, with the top bid of $340.9 million (or $732 psf ppr) submitted by Hoi Hup Realty Pte Ltd.

Participation was relatively measured, with three bidders and a top bid of $732 psf ppr, suggesting a more selective approach by developers towards EC sites in Northern Singapore. This comes amid robust EC supply in the region, which likely shaped a more calibrated bidding strategy as developers balance land acquisition against future launch positioning.

Tenders for two EC sites at Canberra Drive and Sembawang Drive, with an estimated 185 and 450 units each, are slated to open in May and June this year under the 1H 2026 GLS programme.

This is on top of the strong EC project pipeline in the North, including developments at Woodlands Drive 17 and Sembawang, which are anticipated to launch by next year. Together, these additions represent a more competitive supply landscape for ECs in the region.

Buyer Demand

Demand for the future EC development is expected to be anchored by HDB upgraders in Yishun, with additional spillover from nearby northern towns such as Sembawang and Woodlands. In Yishun alone, around 5,700 three-room and larger flats are set to exit their Minimum Occupation Period (MOP) between 2022 and 2027, forming a sizeable pool of HDB upgraders.

Limited fresh EC supply in Yishun and the wider northern region is expected to support demand for Miltonia Close’s future development. The last EC launch in Yishun, North Gaia, was fully sold in 2025, and buyers who missed out are likely to turn their attention to this upcoming development.

Across the broader EC market, available inventory remains relatively tight, with unsold stock currently concentrated in projects such as Coastal Cabana and Rivelle Tampines in the East. This supply tightness is expected to ease later this year, with upcoming EC launches at Woodlands Drive 17, Senja Close, and Sembawang Road set to replenish options for buyers.

Prospective buyers seeking a tranquil living environment might find the future EC project attractive as it is located near Lower Seletar Reservoir. It is also rare for ECs to offer waterfront views.

The lease for the adjacent Orchid Country Club is set to expire in 2030, and under the URA 2025 Master Plan, the site will be re-zoned for residential use, subject to detailed planning. This future transformation could introduce additional housing and amenities to better serve residents in the precinct.

Outlook

Despite the ongoing US-Iran conflict and its impact on the global economy, Singapore’s real estate market has remained resilient. GLS sites launched so far have generally been well received by developers, with steady participation and measured bids observed.

At the same time, buying activity at recent new launches has remained strong. Several projects have recorded high take-up rates, reflecting sustained demand, particularly for well-located developments.

This suggests that overall buying appetite continues to hold firm amid broader economic uncertainties, supported by underlying demand from owner-occupiers and upgraders.

We are seeing developers place greater emphasis on sites with strong locational attributes and clear demand fundamentals, rather than pursuing opportunities indiscriminately. This more selective and disciplined approach is likely to persist, particularly as the pipeline builds and competition across launches intensifies.

While external headwinds and broader cost pressures warrant close monitoring, Singapore’s residential market has consistently demonstrated resilience, even through periods of uncertainty. Such challenges are unlikely to erode underlying drivers of local housing demand, including Singapore’s fiscal stability, finite land supply, and steady population growth.

I confirm that I have read theprivacy policy and allow my information to be shared with this agent who may contact me later.