November 2025 Monthly Developer Sales Report: Moderated New Sale Performance Ahead of Year-end Festive Period

- Kwong Seong Ping

- 7 min read

- Research

- 15 Dec 2025

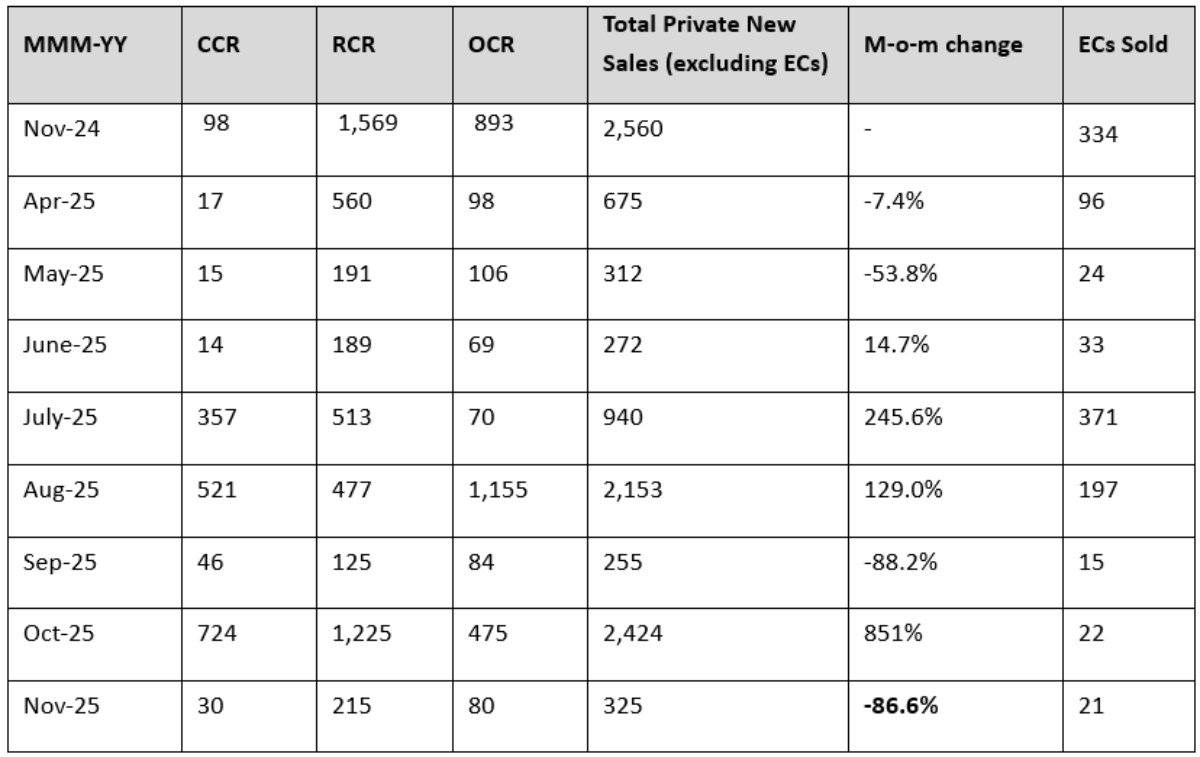

November 2025 saw developer sales coming in at 325 new private homes (excluding ECs), reflecting an 86.6% month-on-month (m-o-m) decrease in transaction volume. The fall in new home sales was primarily due to only one new launch this month, as compared to October, which saw 4 launches totaling 2,233 units.

The Sen, the only new project launched, saw 77 units sold. It represented nearly a quarter of all new private home sales. Meanwhile, the Executive Condominium (EC) market saw 21 units sold, which was one less than the 22 units transacted in the previous month. Otto Place sold 16 units, making up 76.2% of the total number of EC sold this month.

Table 1: New home sales over the last six months

The Rest of Central Region (RCR) accounted for the majority of new sales in November, with a total of 215 units sold, followed by the OCR with a total of 80 units sold. The stronger preference for RCR developments may be due to the right balance between price, location, and lifestyle offerings.

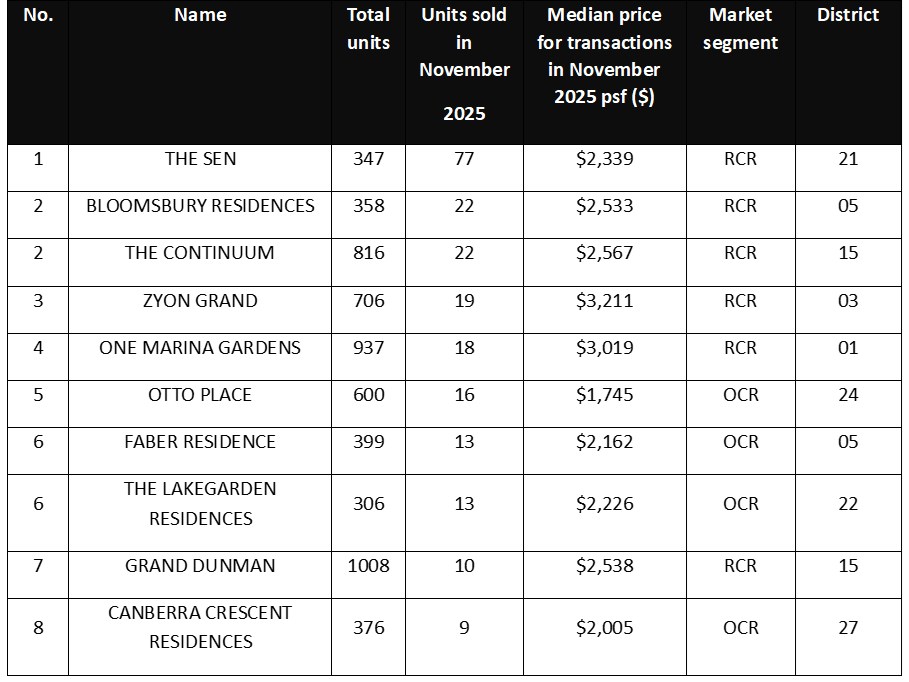

Best Performing New Launches

The Sen

The Sen is located in Upper Bukit Timah and is developed by Sustained Land Pte Ltd. The project saw 77 of its 347 units (22.2%) sold, at a median price of $2,339 psf. This project also marks Singapore’s final new private home launch for 2025.

Of the 77 units sold, two-bedroom and three-bedroom units accounted for approximately 80% of transactions. With a unit mix largely made up of 2-bedders and 3-bedders, coupled with its palatable median price, this development maintains a more accessible overall price quantum. 2 and 3-bedroom units also catered to smaller families, who could property right-sizers from the nearby landed homes, or their children buying their own place while living near their parents.

While the take-up rate may appear modest compared with some recent launches at first glance, The Sen is performing steadily, given the quieter year-end period. Most buyers are owner-occupiers who typically take more time to assess layouts, orientation, and long-term investment before making a new purchase, which explains the measured yet healthy sales pace.

RCR New Launches Also See Healthy Take-Up Amid Month Lull

The top five projects sold in the month are all in RCR, which continued to register healthy buyer interest despite the quieter year-end period. This steady uptake suggests that buyers remain confident in the RCR market segment, even as overall transaction volumes moderate.

Among the top performers were Bloomsbury Residence (99-LH) and The Continuum (FH), each selling 22 units in the month. Both their median prices of approximately $2,500 psf, similar to the median psf of $2,518 for RCR new homes in November. These previously launched projects offer stronger value propositions among buyers looking for a new home in RCR.

Zyon Grand and One Marina Gardens also sold 19 and 18 units in November, respectively, despite benchmark prices showed confidence among buyers looking at properties near the city centre. Both projects border the CCR, sharing similar locational attributes. With only 4 launches expected next year, the RCR market will likely see further activity as buyers look to secure these units ahead of potential price movements upwards.

OCR new homes continue to attract buyers

OCR new homes continue to attract strong buyer interest, reflecting sustained demand for affordable and well-located OCR new projects. The steady take-up may be largely due to buyers prioritising value, accessibility, and future growth potential in the OCR.

Faber Residence and The Lakegarden Residences each saw 13 units sold, with median prices of $2,162 psf and $2,226 psf respectively, signalling resilient demand for the OCR projects. These projects continue to appeal to families and HDB upgraders drawn to their improved lifestyles and proximity to established amenities.

Canberra Crescent Residences also recorded nine units sold at a median price of $2,005 psf, adding to the positive performance across OCR launches. This may be due to its lower median psf amongst OCR projects.

The number of units sold suggest that well-positioned OCR projects remain competitive and continue to attract HDB upgraders.

Table 2: Top ten performing new launch project (excluding ECs) in November

Executive Condominium (EC)

November clocked in 21 Executive Condo (EC) sales, a similar performance from the previous month, which saw 22 EC transactions. With no new EC launches, buyers have been snapping up the remaining stock on the market. Overall, ECs this month were transacted at a median price of $1,491 psf, with most transactions taking place at Otto Place, selling 16 out of 22 overall EC units in the month, with only 14 units still available at Otto Place.

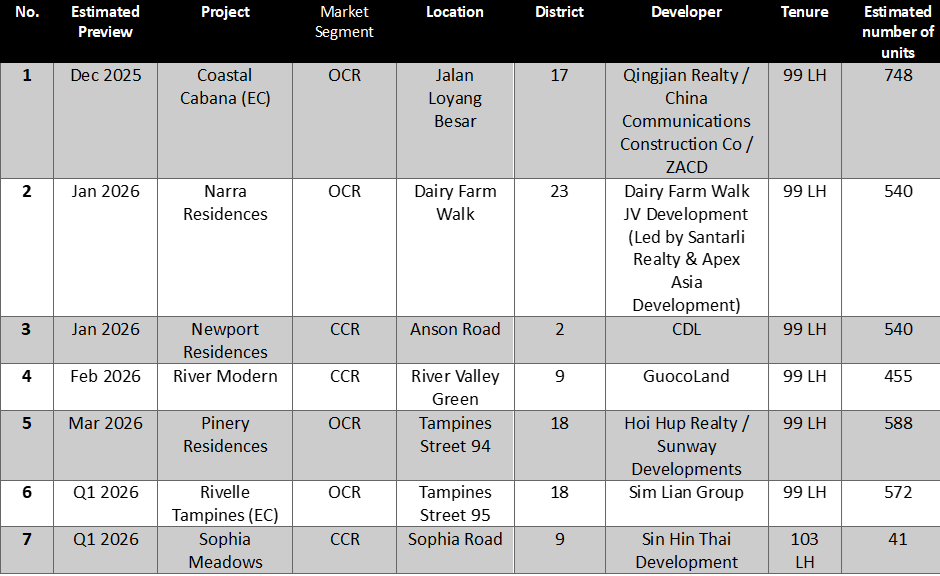

The next EC launch is the 748-unit project Coastal Cabana, located at Jalan Loyang Besar and Rivelle Tampines (560 units), located at Tampines Street 95. These projects are expected to perform well due to strong pent-up demand for ECs and their affordability relative to private homes.

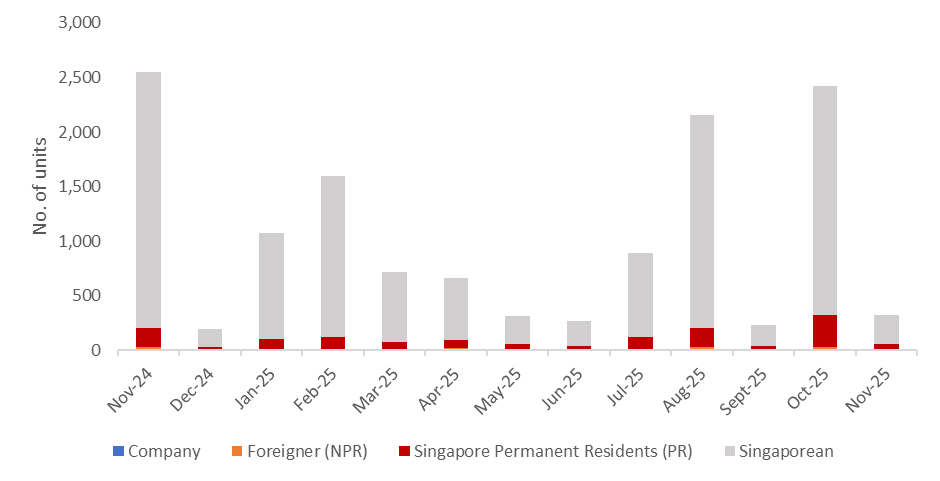

Buyer Profile

Chart 1: Buyer profile for all new non-landed homes (excluding EC)

With the steep Additional Buyer’s Stamp Duty still in place, demand from foreign buyers for new private homes remained subdued. November saw a total of 10 non-landed private home (excluding ECs) transactions made by foreign buyers, making up just 3.1% of the month’s total deals. Meanwhile, Singapore Permanent Resident buyers clocked 42 transactions in November, accounting for 13.1% of all new private home (excluding ECs) purchases in the month.

Lastly, Singaporeans continued to dominate the market in November, accounting for 83.8% of new private home sales (excluding ECs), or 269 units.

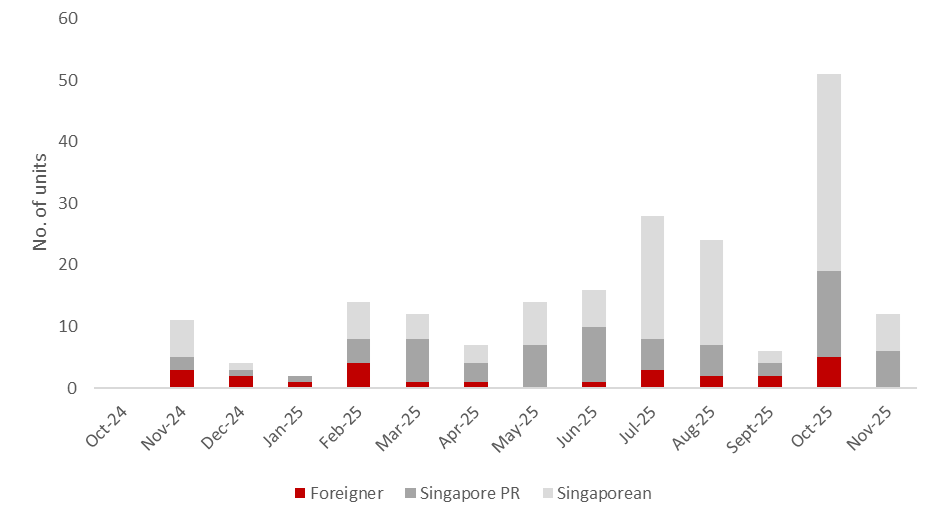

Luxury Homes

Chart 2: Buyer profile for homes transacted at $5mil and more

In November, the luxury home market saw a sharp decrease in activity. A total of 12 new private residential transactions were recorded for homes priced at $5 million and above. These were evenly distributed among Singapore Permanent Residents and locals, who accounted for 6 transactions each.

This month saw two transactions above $10 million at 32 Gilstead and W Residences Marina View. The four-bedroom unit at 32 Gilstead, with a size of 4,176 sq ft at 32 Gilstead, was sold for $15 million. This development is sold out, largely due to its expansive floor plates, freehold tenure and rare opportunity in prime district 11, which has a low supply of new home stock. While the unit at W Residences Marina View was sold for $10.9 million, a 2,809 sq ft five-bedroom unit.

Between the $5million to $10 million price range, 10 transactions were recorded. Notable developments include three units at Grand Dunman and one unit at One Marina Gardens, both situated in prime city-fringe locations. These projects combine central convenience with more spacious layouts, ranging from approximately 1,600 sq ft to 2,200 sq ft, making them well-suited for larger families seeking a prestigious address.

Closing Thoughts and Forecast

November’s sales in the new private home market remained modest, aligning with only one new launch during the month. Looking ahead to December, we expect sales activity to remain modest due to the upcoming festive season and school holidays.

Despite global uncertainties, healthy take-up rates reflect resilient buyer sentiment, supported by a potential Fed rate cut and renewed confidence from the Draft Master Plan 2025, which outlines new housing precincts and integrated hubs across Singapore. Together, these developments help promote buyer confidence by reinforcing the Government's long-term plans for urban renewal and liveability.

Collectively, the total number of new private homes (excluding ECs) sold in the first 11 months of 2025 is 10,754 units. Barring any unforeseen circumstances, ERA Singapore projects new home sales to be between 10,000 – 11,000 units for the whole of 2025

Table 2: Upcoming launches in 2025/1Q 2026

I confirm that I have read theprivacy policy and allow my information to be shared with this agent who may contact me later.