October 2025 Monthly Developer Sales Report: Primary Market Peaks in October with the Launch of Four Blockbuster Projects

- ERA Singapore

- 8 min read

- Research

- 17 Nov 2025

October 2025 saw a record 2,424 new homes sold, the highest thus far in 2025. This marked an 851% quarter-on-quarter (q-o-q) growth and can be attributed to the launch of four highly anticipated projects that were launched in the month.

These four projects were Skye at Holland, Zyon Grand, Penrith and Faber Residences, which made up 84.6% of all private (non-landed) new sale transactions in the month.

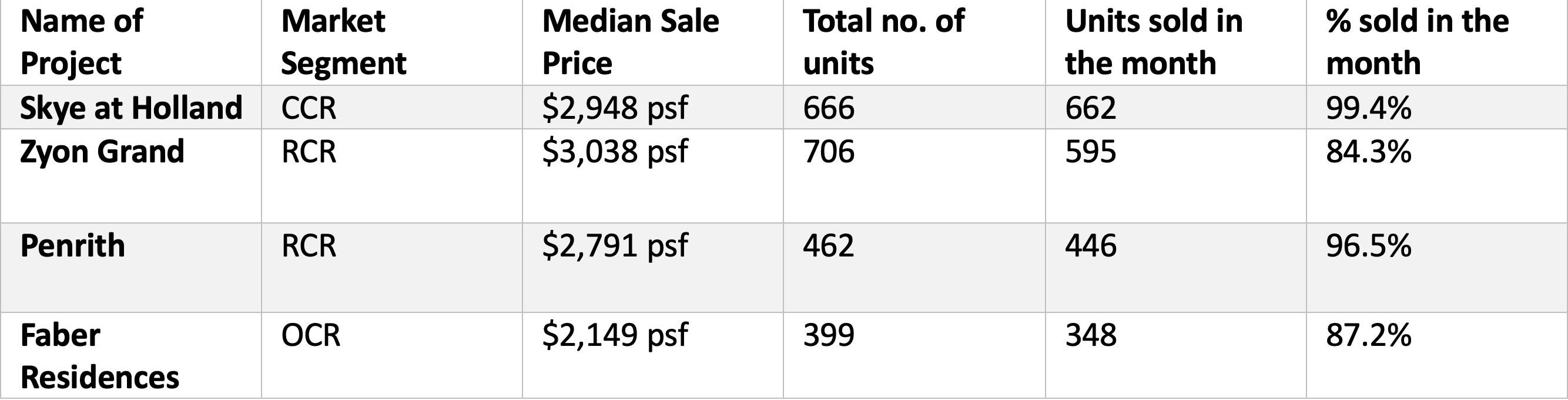

Table 1: New projects launched in October 2025

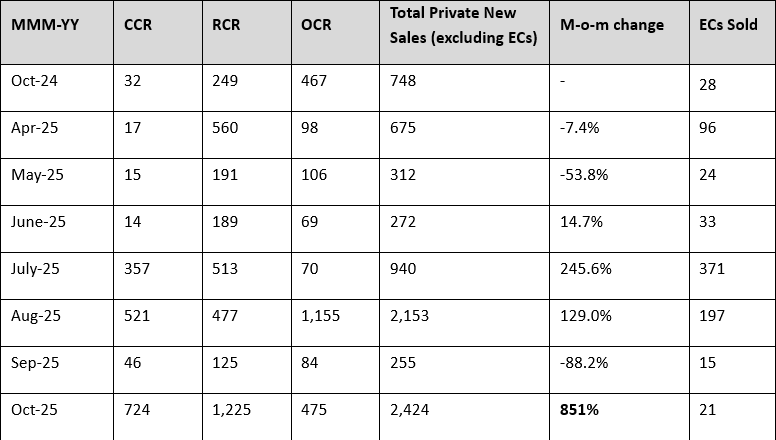

This juxtaposes the slump witnessed in September, where only 255 units were sold due to a seasonal lull because of the school holidays and the Hungry Ghost Month. In the 10 months of 2025, we have reached 10,348 total new sale transactions, over 1.5 times the total for the entire 2024.

Meanwhile, the Executive Condominium (EC) market saw 21 units sold, which was slightly more than the 15 units transacted in the previous month. All but one unit, which was sold at Novo Place took place at Otto Place.

Table 2: New home sales over the last six months

Best Performing New Launches

Skye at Holland

Skye at Holland saw an overwhelmingly positive reception. The project sold 99% of its units on its launch weekend, which was surprising for a CCR project. The project recorded the highest number of CCR units sold (662) in a single project during its launch month since Duo Residences.

While the CCR has seen launches in previous months, such as River Green, they are located within the same locale and pose competition to one another, as well as other nearby launches like Zyon Grand. Therefore, they are likely to share the same pool of nearby HDB upgraders and buyers.

Meanwhile, other previous leasehold CCR launches like UPPERHOUSE at Orchard Boulevard and Aurea position themselves as smaller, more exclusive, luxury developments with higher entry prices.

Skye at Holland both secures a strong CCR location near an MRT station and access to many amenities at a palatable price point, with median transaction prices at $2,949 psf recorded in the month. With a balance of attractive pricing, family friendly layouts and a strong location that also promises a steady exit strategy, Skye at Holland is not only the top performer for the month, but potentially for the entirety of 2025.

Penrith

The second-best performing launch was Penrith at Margaret Drive, which achieved a strong 97.0% (446 units) take-up. Its launch was highly anticipated due to its advantageous location in the mature estate of Queenstown.

Queenstown being a mature estate creates many attractive plus points, which include proximity to an MRT station, primary schools, and various amenities including healthcare and dining options.

The residential town is also home to many high-value HDB flats that fetch attractive prices in the resale market, which could have fed into the supply of buyers for these units sold at Penrith. Moreover, this could represent a strong future exit strategy for current investment buyers.

Zyon Grand

Zyon Grand is located in the River Valley/Zion Road cluster of GLS sites and has seen a strong take up rate of over 84% in October. The project, which sold at a median price of $3,038 psf was substantially lower than neighbouring River Green, which sold its units at $3,447 psf in the same month.

The project, developed by City Developments, one of Singapore’s most popular developers offers flexible and spacious layouts that appeal to upgraders from the nearby estates of Bukit Merah, Outram, and even Queenstown. Furthermore, the project has integrated features, as well as direct access to Havelock MRT station, which are attributes highly sought after.

In particular, over 80% of the three bedroom and larger units were sold on launch weekend, with prices starting at $3m and above. This shows that buyers have the budget and liquidity to invest in homes that have both good layouts and premium locations.

Faber Residences

Faber Residences, located in west coast is the sole OCR launch that took place in October. The project is a low-rise, low-density development that is ideal for families, especially those used to staying in the West region.

Moreover, the strong focus on liveability by providing functional spaces and efficient floor plates will be a draw for buyers accustomed to larger living spaces.

The project sold at a median price of $2,149 psf, which was at a much more palatable price range compared to the other projects that launched in the month. Furthermore, it was the only OCR condo launched in the West region since Elta earlier in the year, and the last OCR launch that we will see until 2026, which could have drawn in a crowd of more price-sensitive buyers.

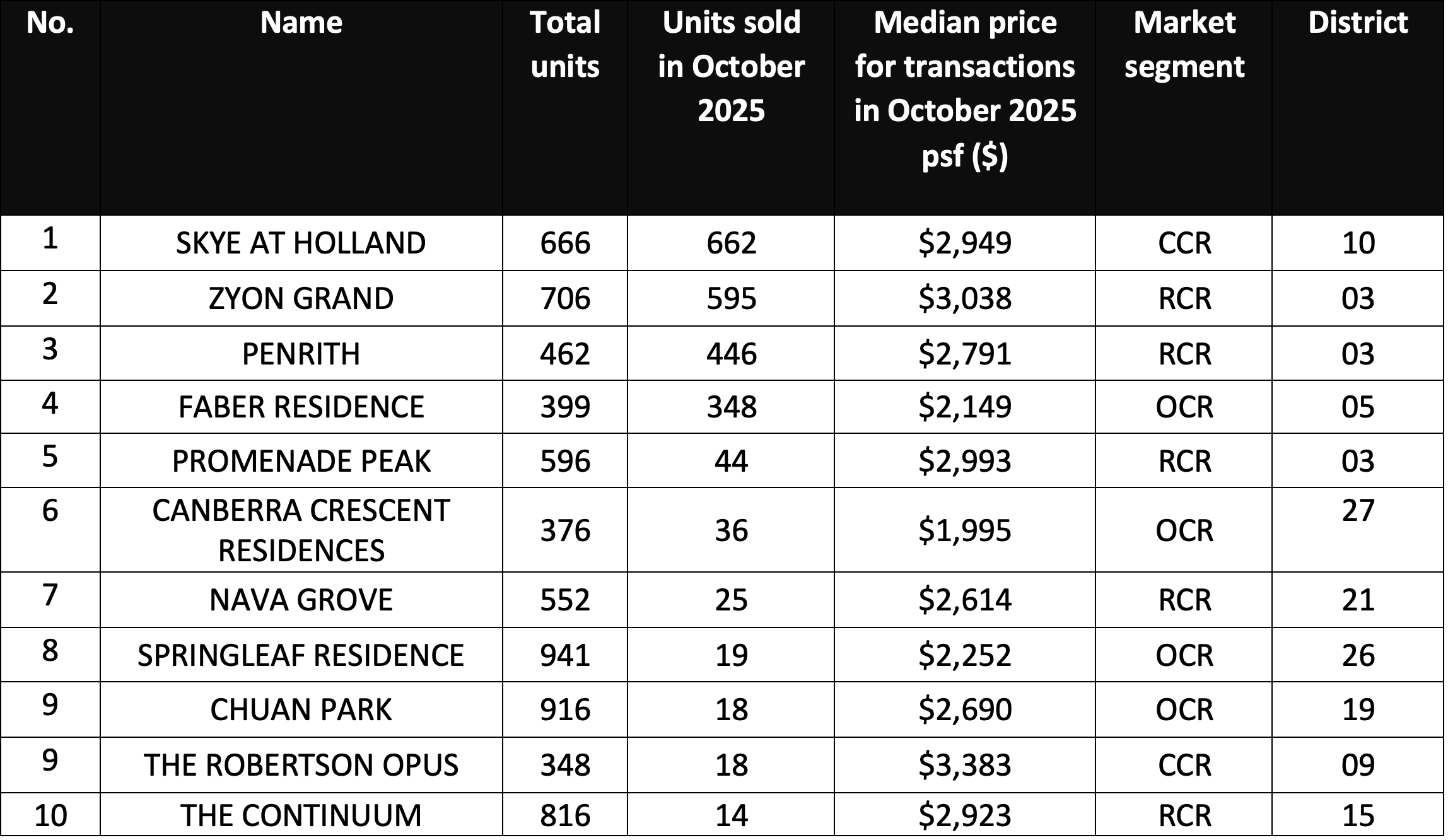

Table 2: Top ten performing new launch project (excluding ECs) in October

Executive Condominium (EC)

October clocked in 21 Executive Condo (EC) sales, a similar performance from the previous month, which saw 15 EC transactions. With no new EC launches, buyers have been buying up whatever remaining stock of ECs on the market. All but one unit, which was sold at Novo Place took place at Otto Place.

The next expected EC launch is the 748-unit project Coastal Cabana at Jalan Loyang Besar, acquired by Qingjian Realty in August 2024 at a land rate of $729 psf ppr, slated to launch next year.

Buyer Profile

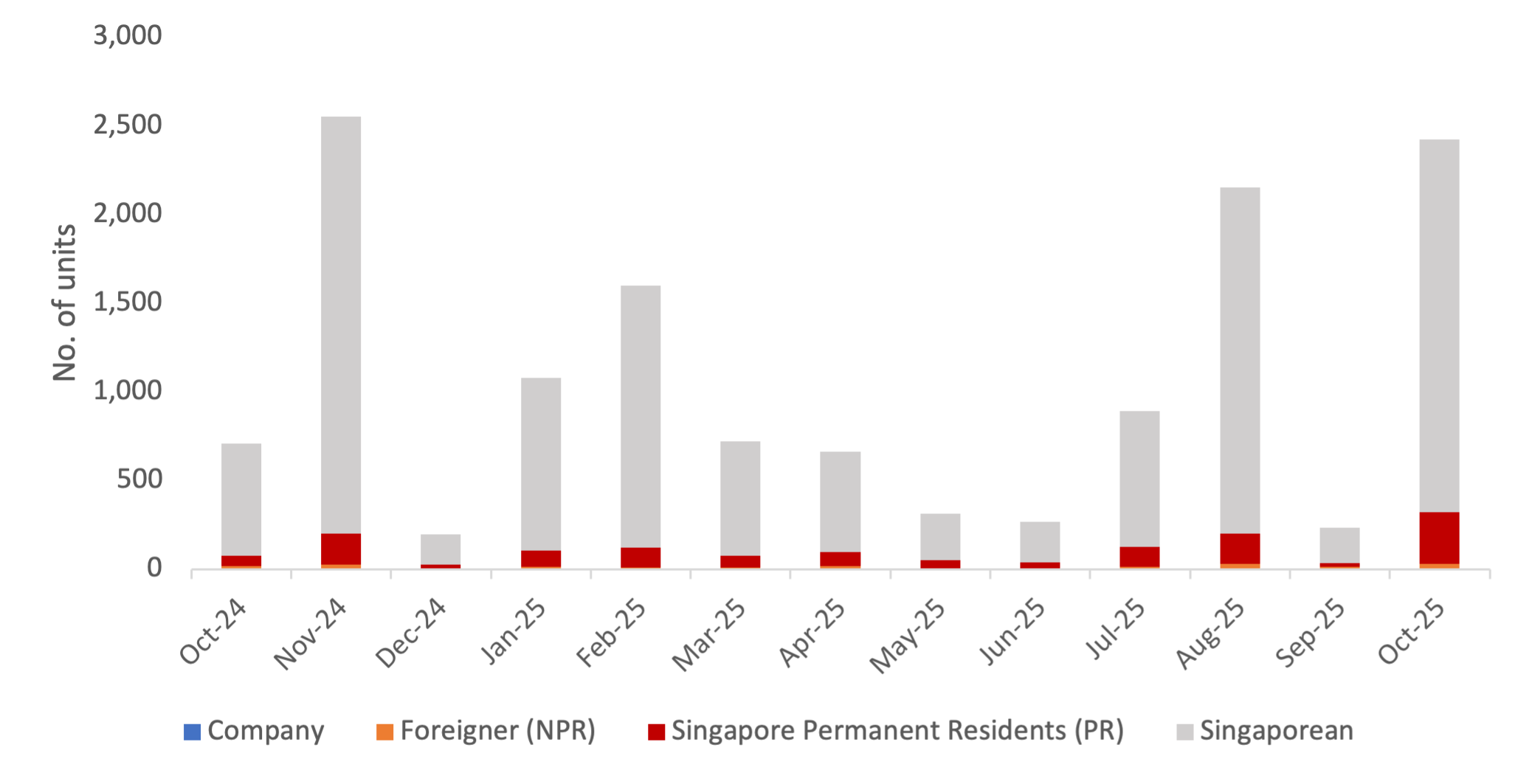

Chart 1: Buyer profile for all new non-landed homes (excluding EC)

With the steep Additional Buyer’s Stamp Duty still in place, demand from foreign buyers for new private homes remained subdued. October saw a total of 31 non-landed private home (excluding ECs) transactions made by foreign buyers, making up just 1.3% of the month’s total deals. Meanwhile, Singapore Permanent Resident buyers clocked 290 transactions in June, accounting for 12.0% of all new private home (excluding ECs) purchases in the month.

Lastly, Singaporeans continued to dominate the market in October, accounting for 86.7% of new private home sales (excluding ECs), or 2,101 units, following the successful quadruple of launches.

Luxury Homes

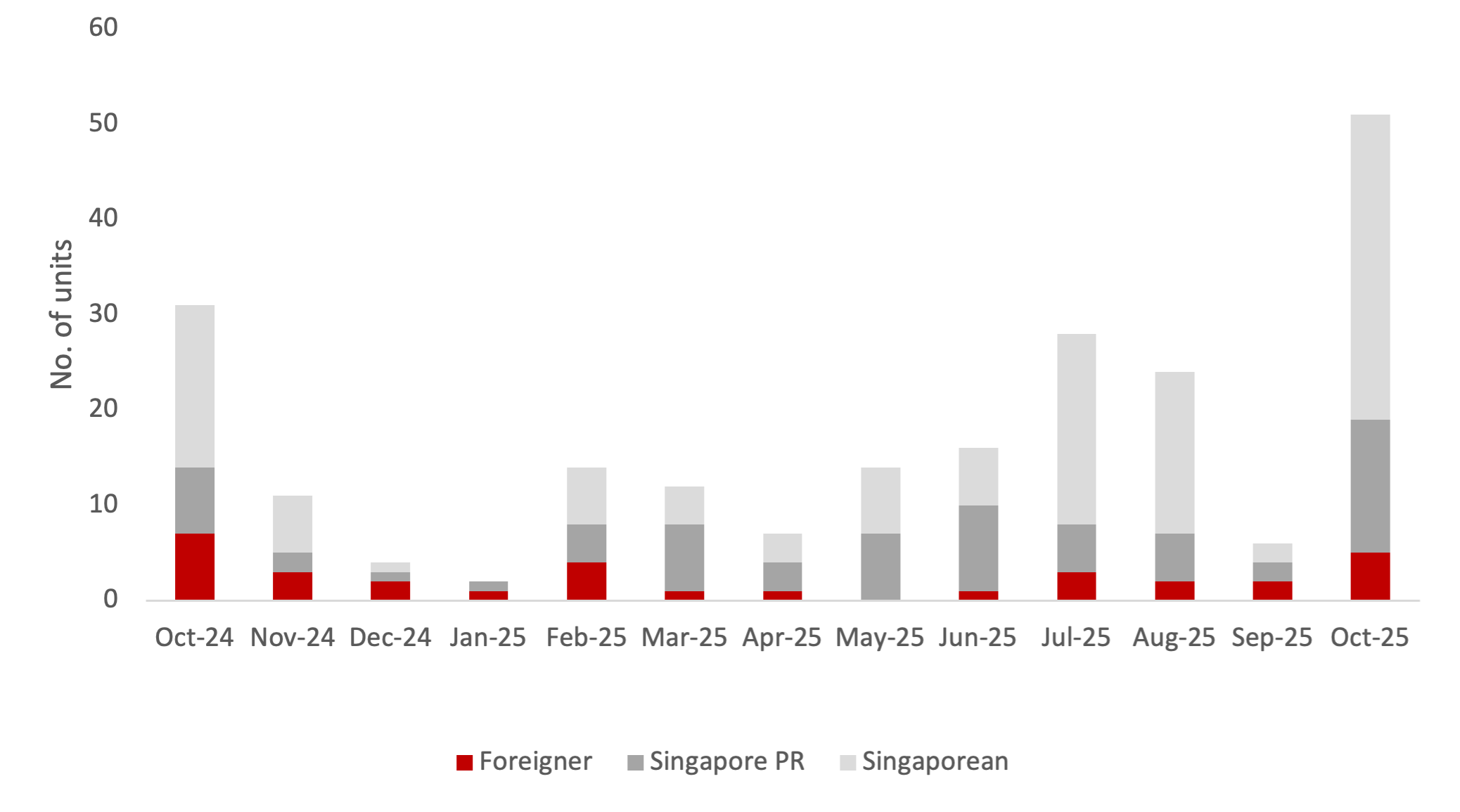

Chart 2: Buyer profile for homes transacted at $5mil and more

In October, the luxury home market saw a sharp increase in activity, with 51 transactions worth $5m and above. These were distributed among foreigners (5), Singapore Permanent Residents (14) and locals (32).

Particularly, we saw a large number of homes transacted in the $5m to $6m range, with 44 of 51 luxury home transactions falling within this price range. This was primarily fuelled by transactions for 4-bedroom units (1,765 sqft) at Skye at Holland, which made up 29, or 56.9% of all such transactions. Despite the smaller floor plan size compared to a traditional 4-bedroom layout, Skye at Holland managed to attractive many buyers for these units in its launch month due to the rare opportunity to purchase a CCR 4-bedroom product at the $5m mark.

The highest transaction was for a 4-bedroom unit priced at $22.7m at 21 Anderson. Purchased by a Singaporean buyer, this is one of the 14 available 4-bedroom units. The combination of the opulent and spacious layout, freehold tenure, and an exclusive location earned 21 Anderson the top spot this month.

There were two other transactions that exceeded the $10m mark, a 2,900 sqft unit at Park Nova and a 1,797 unit at Skywaters Residences, as well as a 2,659 sqft penthouse unit at Zyon Grand. These transactions suggest that buyers seeking high-end properties may be attracted to the expansive floor plates and coveted addresses offered by such ultra-luxury projects.

Closing Thoughts and Forecast

Thanks to the quadruple of highly anticipated projects all making their launches in October, the new sale market has been reinvigorated for possibly the final time before the year ends. With only one new project expected to launch before the year ends (the RCR project The Sen), we should see a more subdued final two months of the year, featuring the seasonal lull as Singaporeans go off on their annual vacations and school holidays.

Collectively, the total number of new private homes (excluding ECs) sold in the first ten months of 2025 is 10,346 units, almost 1.5-times the 6,626 units sold throughout the entire year of 2024. With the stellar performance of the new sale market in the month, new sale transactions have reached ERA Singapore forecasts of around 9,500 units for the whole of 2025.

Despite global uncertainties, healthy take-up rates reflect resilient buyer sentiment, supported by a potential Fed rate cut, upgraded GDP forecasts (1.5%–2.5%), and renewed confidence from the Draft Master Plan 2025, which outlines new housing precincts and integrated hubs across Singapore. Together, these developments help promote buyer confidence by reinforcing the Government's long-term plans for urban renewal and liveability.

Table 2: Upcoming launches in 2025/1Q 2026

I confirm that I have read theprivacy policy and allow my information to be shared with this agent who may contact me later.