September 2025 Monthly Developer Sales Report: Sep 2025 Records Lowest Monthly New Home Sales This Year Amid Hungry Ghost & School Holidays

- Kwong Seong Ping

- 8 min read

- Research

- 15 Oct 2025

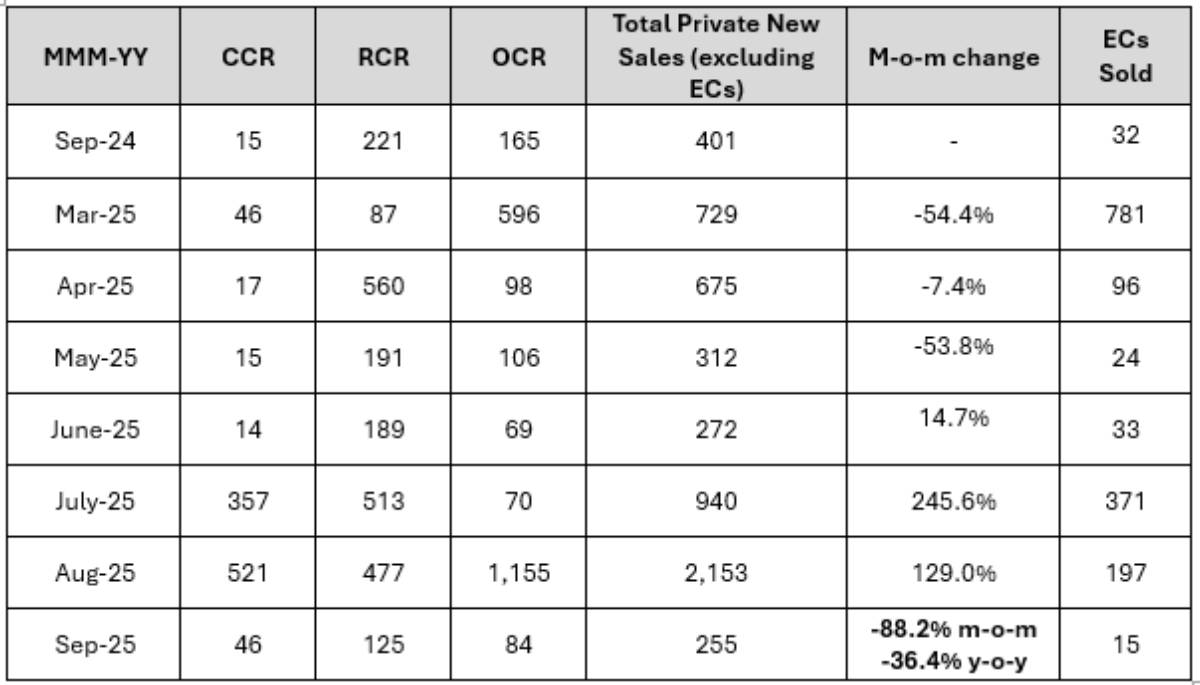

September 2025 saw developer sales coming in at 255 new private homes (excluding ECs), reflecting an 88.2% month-on-month (m-o-m) decrease in transaction volume. The fall in new homes sales may be attributed to the Hungry Ghost Month, a period when buyers traditionally delay property purchases, leading to a temporary lull. However, new sales activity is expected to rebound sharply, highlighted by the strong take-up rate at Skye at Holland, where 658 of 666 units (99%) were sold on the first day of launch.

Accounting for September’s developer sales, this puts the total number of new private homes (excluding ECs) sold in the past nine months of 2025 at 7,924units. This figure has surpassed the 6,626 new sale units transacted in the whole of 2024. This could be attributed to the robust pipeline of new launches in the previous months and moderating interest rate moving into year-end.

Meanwhile, the Executive Condominium (EC) market saw a -92.3% m-o-m decrease to 15 units. September EC new sales were primarily driven by Otto Place, which accounted for 8 units sold, representing 53.3% of total EC transactions. The remainder from Aurelle of Tampines (4 units), Lumina Grand (2 Units) and Copen Grand (1 units).

Table 1: New Home Sales Over the Last Six Months

September saw no new project launches, prompting buyers to focus on existing developments. This marks the lowest level of new launches in 2025 so far.

Rest of Central Region (RCR) projects made up the majority of the new sales in September, with a total of 122 units sold. Closely second is OCR with a total of 84 units sold. The strong RCR demand reflects buyers’ preference for city-fringe locations that balance convenience with relative affordability.

Best Performing New Launches

Canberra Crescent Residences continues to attract buyers a month after debut

Though modest, new sales at Canberra Crescent Residence secured the top-selling position for September. This may be large due to its attractive median pricing at $2,000 psf compared to recent new launches.

Designed with families and HDB upgraders in mind, with 75% of its units being three- and four-bedroom apartments that offer family-friendly layouts. This is reflected in sales, as two- and three-bedroom units accounted for 80% of transaction. The balanced distribution of layouts reflecting strong long-term own-stay demand over speculative investment.

Canberra Crescent Residences is strategically located between Canberra Plaza and the Bukit Canberra hub. It is also within walking distance of Canberra MRT Station. The development is aligned with the proposed future transformation outlined in the 2025 URA Draft Master Plan, which includes the redevelopment of Sembawang Shipyard into a vibrant new housing estate.

Grand Dunman Offers Premium RCR Value Propositions

Grand Dunman is a mega-luxury development located on the city fringe in prime District 15. This month the project sold an additional 24 units, bringing the total sold to 888 of 1,008 units (88.1%) of the development. Priced between $4 and $5 million accounted of 62.5% of the new sale, with a total 15 units sold.

The project is situated just a two-minute walk from Dakota MRT and one stop from Paya Lebar Interchange, with direct access to the Central Business District. It offers convenient access to key work nodes and major commercial hubs. Top school located within 1km are Kong Hwa School, Dunman High, and Chung Cheng High.

Additionally, the development is in close proximity to park connectors, East Coast Park, Marina Barrage, and Kallang Sports Hub, promoting an active and well-rounded lifestyle.

Future growth driven by the 2025 URA Draft Master Plan, including initiatives such as Kallang Alive and Long Island, further enhances the investment appeal of Grand Dunman. Coupled with its luxury facilities and family-oriented environment, the development offers a balanced lifestyle alongside strong long-term value.

CCR New Launches See Robust Take-Up Amid Month Lull

Continuing from last month, River Green and The Robertson Opus remain among the top-selling developments, with 16 and 10 units sold respectively. Demand in the CCR continues to show robust take-up and strong buyer interest.

The Core Central Region (CCR) remains highly attractive among local buyers due to its combination of prime location, strong connectivity, and relative value compared to other luxury areas. River Green, with majority of the new sale between S$1.5mil to S$3mil, 9 out of 15 units sold. This offers a comparatively accessible entry point for Singaporean and PR buyers while providing direct, sheltered access to Great World MRT.

Similarly, The Robertson Opus, with its 999-year leasehold tenure, appeals to a different buyer segment seeking long-term security and capital growth. The CCR centrality, prestige and proximity to key lifestyle hubs make it a preferred choice for CCR buyers seeking both convenience and long-term investment potential.

Table 2: Top ten performing new launch project (excluding ECs) in September

Executive Condominium (EC)

September clocked in 15 Executive Condo (EC) sales, a sharp decrease from the previous month, with no new EC launches. Overall, ECs this month were transacted at a median price of $1,758 psf, with almost 53.3% of transactions taking place at Otto place, the most recent EC launch.

The next expected EC launch is the 748-unit project at Jalan Loyang Besar, acquired by Qingjian Realty in August 2024 at $729 psf prr, slated to launch next year. These upcoming EC prices are expected to be higher, as Otto GLS site was previously awarded at a record low of $701 psf ppr.

Buyer Profile

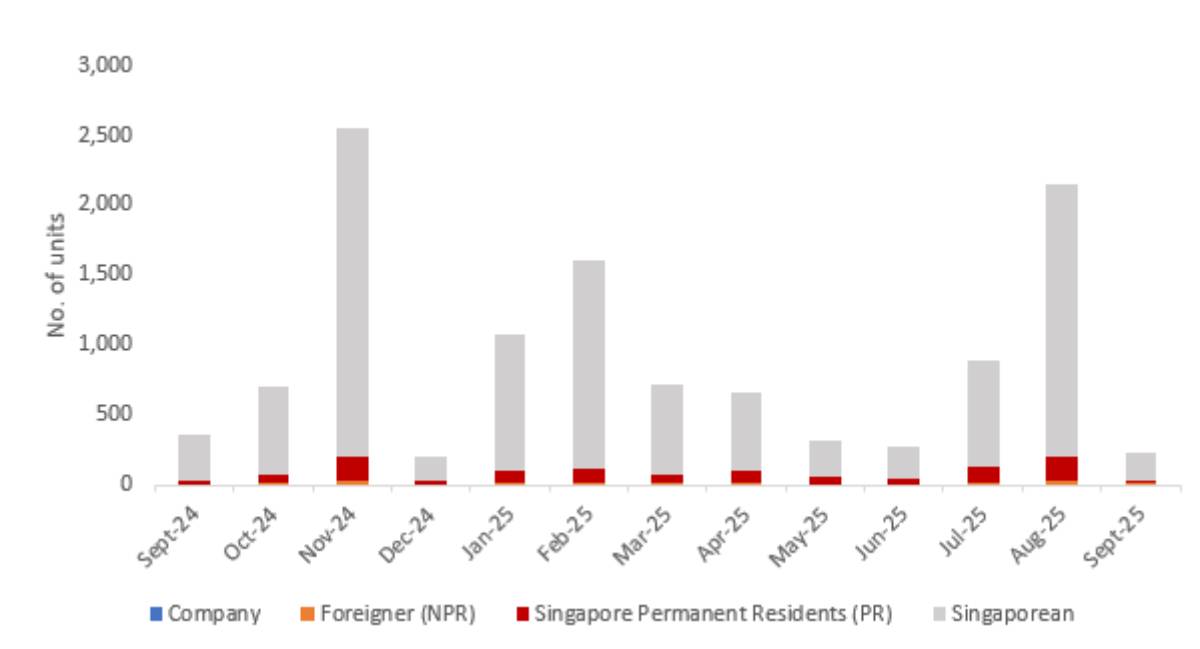

Chart 1: Buyer profile for all new non-landed homes (excluding EC)

With the steep Additional Buyer’s Stamp Duty still in place, demand from foreign buyers for new private homes remained subdued. September saw a total of non-landed private home (excluding ECs) transactions made by foreign buyers, making up just 6.0% of the month’s total deals. Meanwhile, Singapore Permanent Resident buyers clocked 21 transactions in June, accounting for 9.0% of all new private home (excluding ECs) purchases in the month.

Lastly, Singaporeans continued to dominate the market in September, with new private home sales (excluding ECs) sharp decrease by 89.9% quarter-on-quarter to 198 units, the lowest since December 2024. This moderation was largely due to the absence of new launches during the month.

Luxury Homes

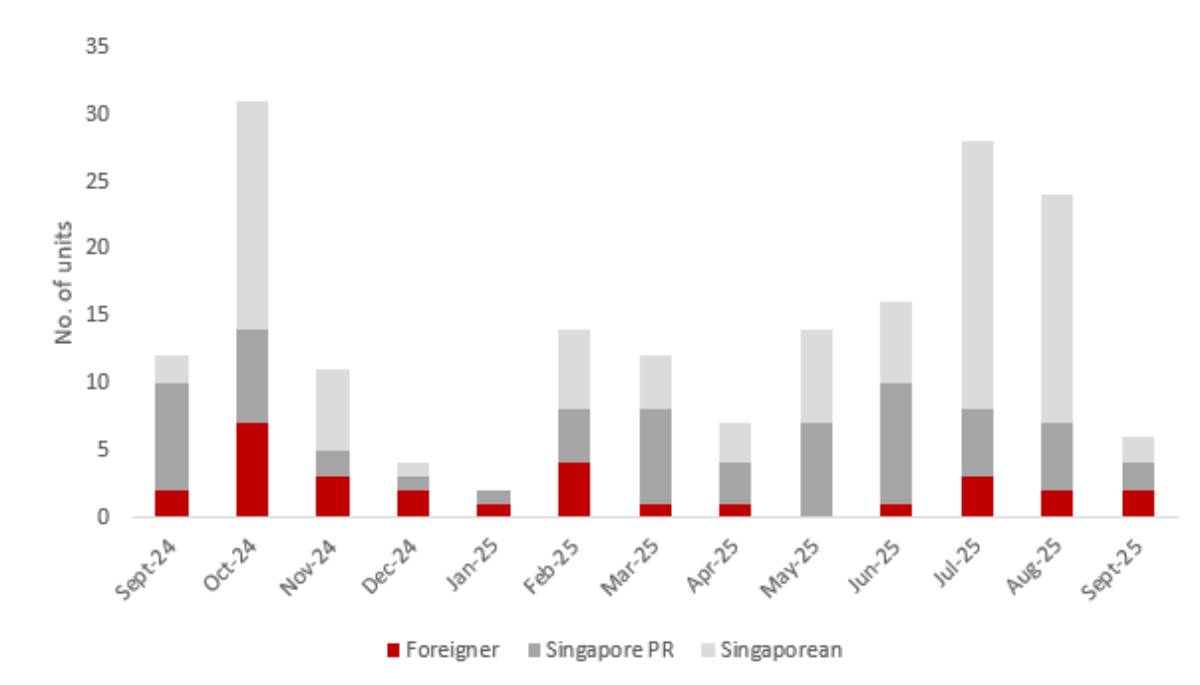

In September, the luxury home market saw a sharp decrease in activity, maintaining a stable trend and recording the second-highest take-up since November 2024. A total of 6 new private residential transactions were recorded for homes priced at S$5 million and above. These were evenly distributed among foreigners, Singapore Permanent Residents and locals, who accounted for 2 transactions each.

This month saw two transactions exceeding the S$20 million. Both were ultra-luxury freehold units within the same development at 21 Anderson. Both sales were 4,489 sq ft, four-bedroom unit that sold for about S$23.5milion to S$24million. These transactions suggest that buyers seeking high-end properties may be attracted to the expansive floor plates and coveted addresses offered by such ultra-luxury projects.

Within the S$5million to S$8 million price range, there were four transactions recorded. Canninghill Piers, an integrated development by City Developments Limited and CapitaLand Limited, a 2,788 sq ft five-bedroom unit was sold for approximately S$7.6 million. Promenade Peak saw two 1,884 sq ft four-bedroom units transacted at around S$6.4 million and S$6.7 million respectively. Lastly, Terra Hill recorded the sale of an 1,895 sq ft luxury penthouse for approximately S$5.3 million.

Closing Thoughts and Forecast

September sales in the new private home market remained subdued, aligning with the no new launches during the month. Looking ahead to October, we expect sales activity to rebound sharply, highlighted by the strong take-up rate at Skye at Holland, where 658 of 666 units (99%) were sold on the first day of launch, at an average price of $2,953 psf.

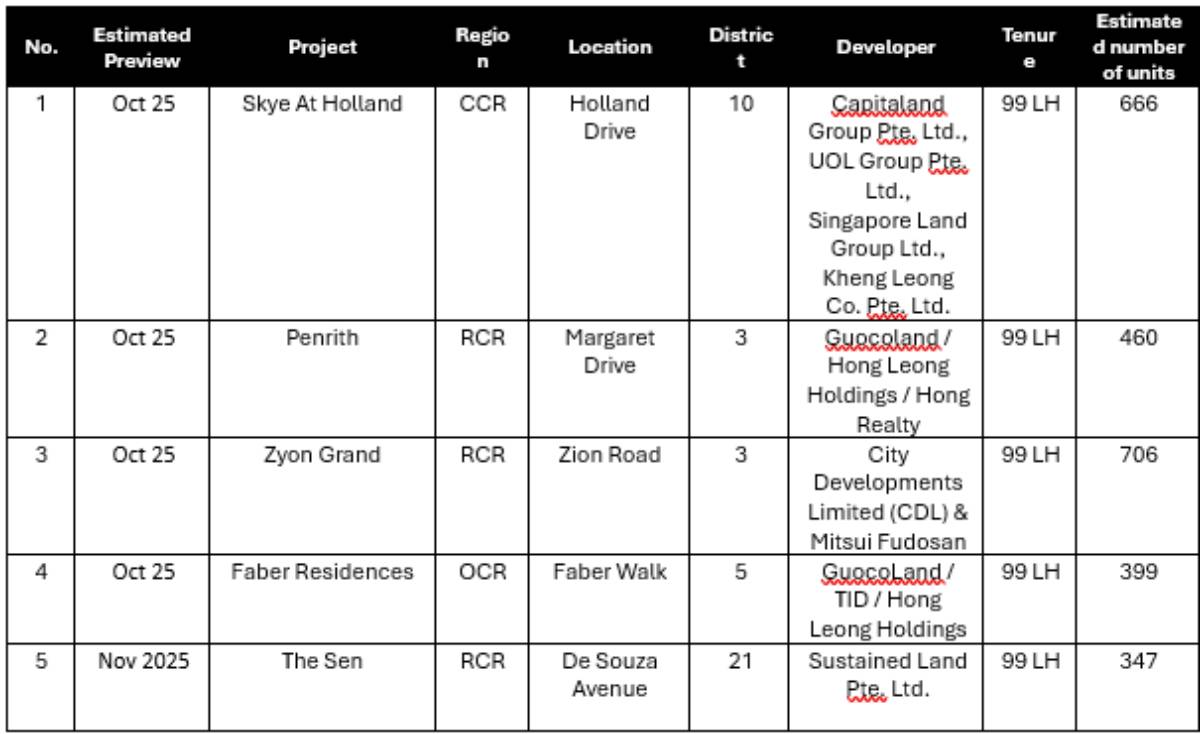

Five new launches are expected to launch in second half of 2025, with three new launches in the RCR namely Zyon Grand, Penrith, and The Sen, alongside Skye at Holland in the CCR and Faber Residences in the OCR. Demand is expected to remain resilient, with robust take-up rates expected across these projects, supported by strong buyer interest heading into year-end.

Collectively, the total number of new private homes (excluding ECs) sold in the first nine months of 2025 is 7,924 units, surpassing the 6,626 units sold throughout the entire year of 2024. Unless unforeseen circumstances arise, ERA Singapore forecasts new home sales to range between 8,500 and 9,500 units for the whole of 2025.

Despite global uncertainties, healthy take-up rates reflect resilient buyer sentiment, supported by a potential Fed rate cut, upgraded GDP forecasts (1.5%–2.5%), and renewed confidence from the Draft Master Plan 2025, which outlines new housing precincts and integrated hubs across Singapore. Together, these developments help promote buyer confidence by reinforcing the Government's long-term plans for urban renewal and liveability.

In the first seven months of 2025, there have been 5,527 new homes sold. Barring any unforeseen circumstances, ERA Singapore projects new home sales to be between 8,500 - 9,500 units for the whole of 2025.

Table 2: Upcoming launches in 2025

I confirm that I have read theprivacy policy and allow my information to be shared with this agent who may contact me later.