Singapore's HDB Market: Resale Prices Maintain Moderate Growth in 2025

- Ethan Hariyono and Stanley Lim

- 8 min read

- Research

- 10 Dec 2025

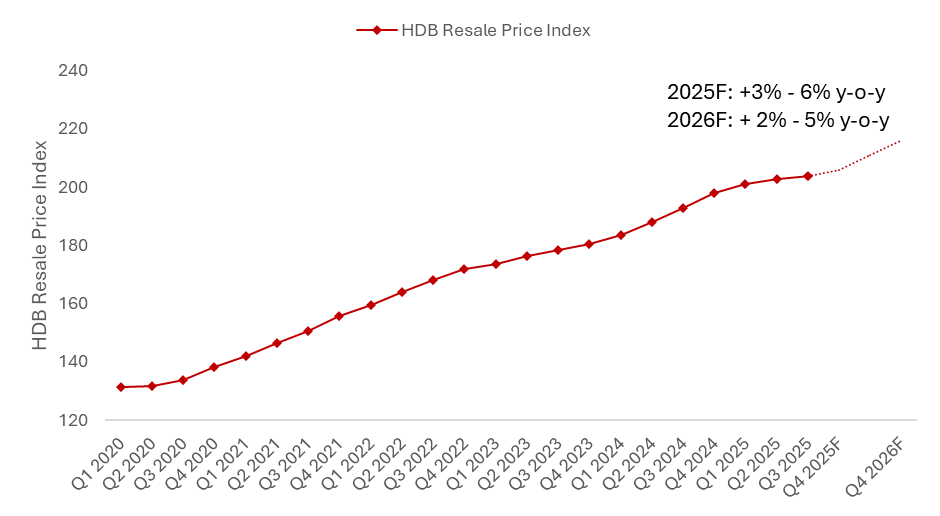

The Housing and Development Board (HDB) resale market saw continued price increases, reaching a new peak, supported by resilient homebuying activity. In the first three quarters of 2025, the HDB Resale Price Index (RPI) rose by 2.9% and is expected to keep rising, possibly leading to a full-year increase of between 3% and 6%.

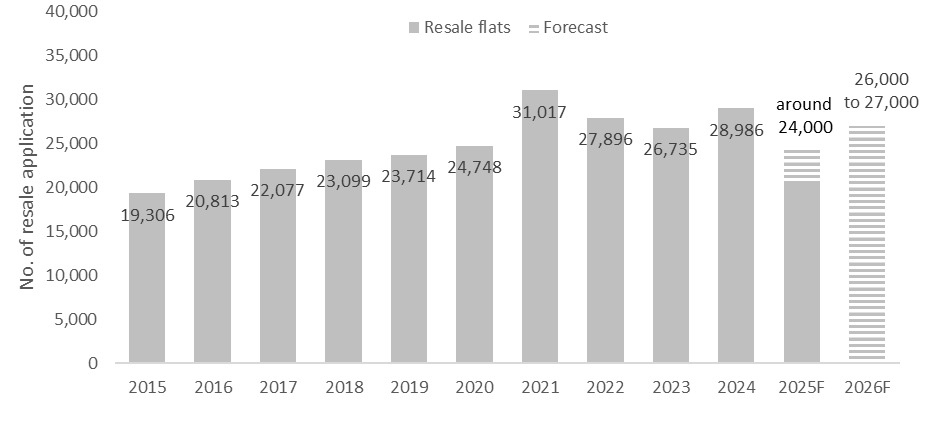

In the first 10 months of 2025, resale applications reached 21,412 and are projected to total 24,000-25,000 by year-end. This reflects a significant drop from full-year count of 28,986 units in 2024. The decline was mainly due to competing supply from more Sales of Balance (SBF) flats and fewer flats reaching their Minimum Occupation Period (MOP).

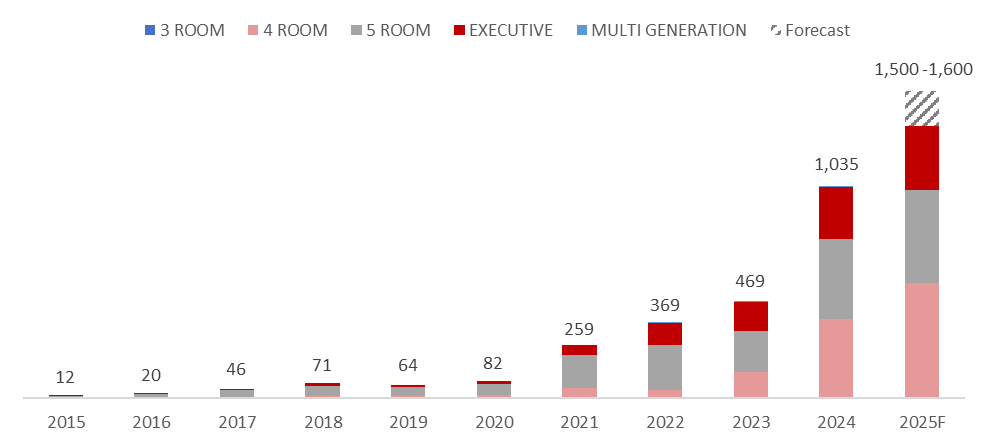

Conversely, we have observed a notable rise in million-dollar flats sold this year, with 1,330 of such sales recorded in the first 10 months of 2025. This figure is expected to reach around 1,500 units by year's end, which is approximately 44.9% higher than the previous peak of 1,035 million-dollar transactions in 2024.

In the Build-to-Order (BTO) segment, a total of 19,723 BTO flats were launched by HDB across 23 projects during the February, July, and October 2025 exercises. Additionally, 10,252 Sales of Balance (SBF) flats were launched concurrently during the February and October 2025 exercises. Notably, the February SBF exercise (5,590 units) was the largest SBF launch to date. Collectively, this brings the total number of new flats launched in 2025 to 29,975 units, representing a 41.2% increase from the 21,225 units released in 2024.

HDB Resale Prices to Continue Rising in 2026

Resale HDB prices continued to rise in 2025, though the pace of growth has slowed to a more stable and sustainable level. From the end of 2024 to the third quarter of 2025, the HDB RPI increased by 2.9% to 203.7, compared to the 6.9% increase seen over the same period last year. This aligns with ERA’s forecast, which predicts a 3–6% price increase by the end of 2025.

In 2026, the HDB RPI is expected to continue rising steadily between 2 and 5%, supported by the higher price base set in 2025. At the same time, the larger pool of 11,181 MOP-ready flats in 2026 should help maintain both resale price growth and transaction activity.

Chart 1: HDB Resale Price Index (RPI) Time Series

HDB homebuying activity sustained by better-than-expected economic performance

Despite various challenges, including trade tensions, HDB homebuying activity remained resilient in 2025, supported by better-than-expected economic growth and low unemployment. Similarly, a declining interest rate environment has helped boost resale HDB demand this year.

Although the Liberation Day announcement caused ripples in the market and prompted some knee-jerk reactions, the market quickly stabilised, aided by the temporary halt on trade tariffs. Singapore, being among the least affected by trade tariffs, also experienced a swift recovery, mainly driven by strong demand for chips and artificial intelligence (AI) technology.

Singapore’s economy gained momentum in Q3 2025, expanding by 2.9% year-on-year. This already exceeded earlier forecasts of 1.5% to 2% growth, which were affected by concerns over ongoing US tariffs. As a result, the Ministry of Trade and Industry (MTI) has upgraded the full-year forecast for 2025 to "around 4%."

Amid economic growth, the overall unemployment rate remained steady at 2% in September 2025. Both citizen and resident unemployment rates decreased, according to the Labour Market advance release [1]. However, future sentiments regarding hiring and wage growth could still be subdued by the less positive economic outlook, influenced by global uncertainties and trade tariffs. Even though retrenchment numbers in the first nine months of 2025 have increased by 13.8% to 10,630, up from 9,340 in the same period last year, the overall unemployment rate stays low at 2.0% in 3Q 2025.

Singapore continued to experience easing inflationary pressures. The Consumer Price Index in 3Q 2025 increased by 0.2% quarter-on-quarter. The inflation rate has also remained stable, with quarterly growth fluctuating between 0% and 1% since 3Q 2023.

Furthermore, the declining interest rate environment has provided additional relief to resale HDB homebuyers. The U.S. Federal Reserve (Fed) announced two rate cuts in September and October 2025, which helped ease pressure on flat owners with bank mortgages.

HDB resale transaction volume moderates in tandem with SBF launches

Resale HDB transaction volumes have slowed in the first ten months of 2025, with 21,412 applications recorded. This marks an 11.1% y-o-y decrease from the 23,791 applications during the same period in 2024. Based on this trend, full-year resale HDB transactions are likely to fall short of ERA’s initial projections of 26,000 to 27,000 units.

However, this easing in resale activity is largely expected due to increased competition from SBF exercises and a smaller pool of MOP flats in 2025. This year, two SBF exercises were launched – one in February and the other in July following its initial announcement during Budget 2025. February’s SBF exercise was also notably the largest to date, offering 5,590 flats. At the same time, MOP flat volume fell to 6,973 units this year. This supply of MOP flats is also the lowest in 11 years, since 2014, when only 5,301 units became available on the resale market.

For 2026, ERA forecasts HDB resale transactions to reach between 26,000 and 27,000 units. This outlook is mainly driven by two factors: a larger pipeline of 13,840 MOP flats entering the market, as well as steady price growth, which could encourage selling activity.

Chart 2: HDB Resale Applications

Million dollar flat transactions continue to rise in 2025

From January to October 2025, million-dollar HDB flat transactions reached 1,330 units. This marks a 55.9% year-on-year increase compared to the 853 transactions recorded in the same period in 2024. Driving this growth were 4-room flats, which experienced a 90.2% year-on-year surge in million-dollar transactions, rising from 295 deals in 2024 to 561 in 2025.

Chart 3: Million-Dollar Flat Transactions (by year)

Despite this increase, million-dollar flats still represented a small share of resale flat transactions. Out of the 20,694 resale applications recorded in 10M 2025, only 6.4% were million-dollar deals.

These transactions also remained largely concentrated in mature estates, which accounted for 91.4% of all million-dollar deals over the same period. Additionally, over half (52.3%) of million-dollar deals in 10M 2025 involved newer flats aged 15 years or less.

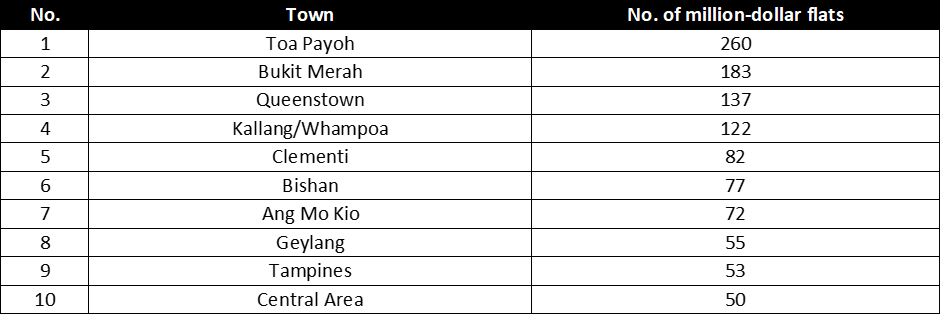

Table 1: HDB towns with the most million-dollar HDB transactions in 10M 2025

In line with the prevalence of million-dollar transactions in mature estates, Toa Payoh, Bukit Merah, and Queenstown recorded the highest number of such deals among HDB towns in 10M 2025. The priciest deal recorded during this period also took place in Queenstown, where a 5-room flat at Dawson Road sold for $1,658,888.

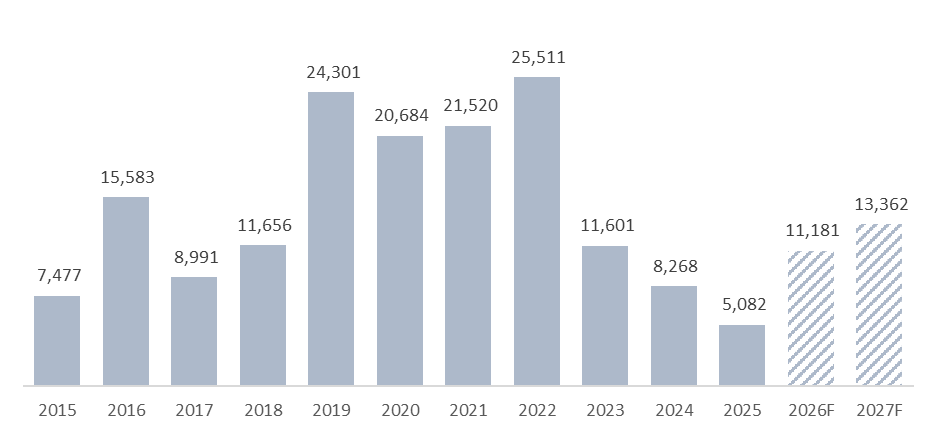

Supply of Minimum Occupation Period (MOP) Flats to increase next year

In 2025, a total of 5,082 flats sized 3-room and larger completed their 5-year MOP. This represents a 38.5% decrease from the 8,268 units recorded in 2024. However, this trend is expected to reverse next year, with the number of MOP flats(3-room and larger) projected to increase to 11,181 units in 2026.

Chart 3: HDB flats (3-room and larger) that reach the 5-year MOP by year

With a larger pool of flats reaching MOP, resale supply will rise accordingly. Precincts such as Northshore Drive (Punggol), Margaret Drive (Queenstown), as well as Bidadari Park Drive and Alkaff Crescent (both Toa Payoh), will see the highest number of MOP flats, and likely also stronger resale demand.

Robust BTO and SBF Market Helped Alleviate Pressure on Resale Market

Overall, we observed three BTO launches and two SBF launches during 2025. This increased the new flat supply to 19,723 BTO flats and 10,252 SBF flats.

The BTO market saw the launch of new housing precincts, such as Mount Pleasant in Toa Payoh, Berlayar Estate in Bukit Merah, and parts of the Greater Southern Waterfront. Additionally, there were further increases to the subsidy clawback rates for Prime flats, which reached its current peak of 14% as seen in Berlayar Residences that launched in October.

By providing more Prime flats within existing mature estates and through new housing precincts, HDB aims to curb the rising resale prices of newer flats in these areas.

Additionally, a significant influx of SBF supply occurred, with 10,252 SBF flats available for sale – nearly 6.5 times the SBF units offered in the previous year (1,588). SBF flats provide shorter waiting times compared to BTO flats, while also offering lower prices and longer leases than comparable resale flats. Moreover, SBF flats in mature estates or choice locations might not face the same strict resale restrictions imposed on the newer classification of Plus or Prime HDB flats.

Therefore, with such a large stock of BTO and SBF homes available this year, demand in the resale HDB market has eased slightly, resulting in fewer transactions and more moderate RPI growth over the year.

2026 will kick off with a joint BTO and SBF exercise in February, featuring around 4,600 BTO and 3,000 SBF flats.

What can we expect in 2026?

Table 2: ERA forecast of HDB Resale Market

In 2026, we expect the wider resale market to see around 26,000 to 27,000 transactions, with price growth ranging from 2% to 5%. This aligns with the Singapore government’s aim for a stable and sustainable property market.

[1] Ministry of Manpower, Third Quarter 2025 Labour Market Advance Release

I confirm that I have read theprivacy policy and allow my information to be shared with this agent who may contact me later.