Telok Blangah Road Government Land Sale Site Analysis

- Egan Mah

- 10 min read

- Research

- 5 Nov 2025

URA has launched the tender for the Government Land Sales (GLS) parcel at Telok Blangah Road for residential use on 24 June 2025. The tender subsequently closed on 4 November 2025. In total, the site drew interest from three bidders, with the top bid of $918.3 million (or $1,326 psf ppr) submitted by Kingsford Hurray Development Pte Ltd. At $918.3 million, its top bid far surpasses other sites such as Bayshore Road’s $658.9 million and Dunearn Road’s $491.5 million. The high price quantum did not deter Kingsford to purchase the site, a signal of their strong confidence in the location.

Table 1: Site details of GLS

| Tenderer | Tendered Sale Price | Tendered Sale Price In $PSM of GFA | Tendered Sale Price In $PSF of GFA | |

| 1 | Kingsford Huray Development Pte Ltd | $918,300,400.00 | $14,272.62 | $1,326 |

| 2 | Guocoland (Singapore) Pte. Ltd. And Intrepid Investments Pte. Ltd. | $880,000,000.00 | $13,677.34 | $1,271 |

| 3 | Frasers Property Phoenix Pte. Ltd. And Metro Soilbuild Development Pte. Ltd. | $863,255,555.00 | $13,417.09 | $1,246 |

Source: URA

1.0 Site Details

Table 2: Site details of GLS

| Location | Telok Blangah Road |

| Region | RCR |

| District | 4 |

| Site Area (sqm) | 13,600sqm |

| Proposed Gross Plot Ratio | 4.7 |

| Land Use Zoning | Residential (Non-Landed) |

| Maximum Gross Floor Area | 63,920 sqm |

| Estimated Housing Units | 745 |

Source: URA

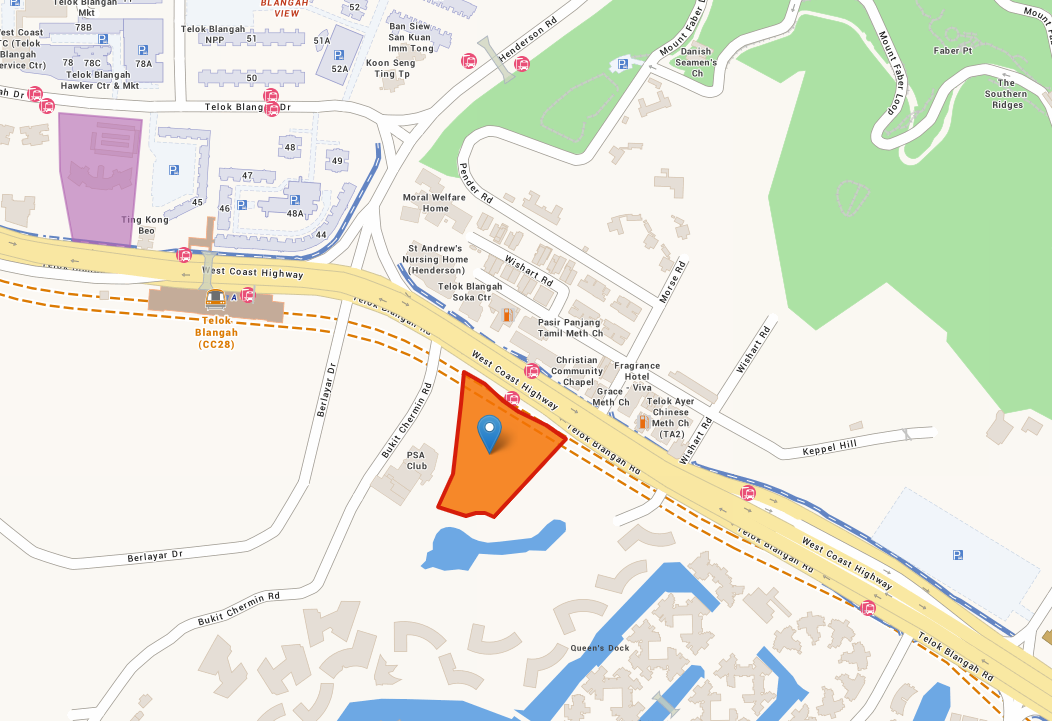

Map of Telok Blangah Road GLS site

2.0 Location Analysis

Connectivity

The site is located within a five-minute walk to Telok Blangah MRT Station on the Circle Line, therefore connecting residents to Harbourfront MRT station and the North East line one station away. This also enhances connectivity to key employment hubs such as one-north and Buona Vista. It is also expected that the Circle Line 6 (CCL 6) extension, which closes the loop for the Circle Line between Harbourfront and Marina Bay MRT stations, is slated to be operational in 1H 2026, therefore adding additional MRT stations on the CCL. Residents can also enjoy access to the Central Business District under ten minutes via the West Coast Highway.

Lifestyle and Recreation

The Telok Blangah site is near major retail nodes such as VivoCity and Harbourfront Centre, providing a wide range of shopping and dining options. The site also in close proximity to Mount Faber Park and families may appreciate the ease of access to Sentosa, as well as Labrador Park and the Southern Ridges. Due to its close proximity to an extensive network of nature and waterfront amenities, it is uniquely positioned to appeal to nature lovers and active families. The former Keppel Club site under GSW, will see about 20% of its area to be set aside for parks and open land, adding to the green amenities already present in Telok Blangah.

The Telok Blangah GLS site, with its close proximity to green amenities thus aligns well with the increasing trend of buyer preferences for green living and wellness.

Neighbourhood Amenities

Families with school-going children may appreciate the site’s close proximity to a variety of schools within a 2km radius. There are also two international schools present in the Telok Blangah area, namely Shelton College International and ISS International School Singapore.

Table 3: Schools possibly within 2km of the Telok Blangah Site

School | Possible Distance to site |

Blangah Rise Primary School | Within 1 km |

Gan Eng Seng Primary School | Within 2 km |

Radin Mas Primary School | Within 2 km |

CHIJ (Kellock) | Within 2 km |

Source: MOE Schoolfinder

3.0 First Mover Advantage

The Telok Blangah site is strategically positioned to benefit from first mover advantage due to the GSW Master Plan, where it will unlock over 2,000 hectares of land for future commercial, residential and recreational uses. Just beside the GLS site, the Keppel Club site will also be redeveloped, offering 6,000 HDB flats and 3,000 private homes. In light of the upcoming new township, the Telok Blangah Site will be the first new private development before this major supply injection, giving it a strategic pricing advantage and potentially allowing buyers to enjoy capital appreciation when the GSW is in full effect.

The case studies shown in Table 3 have showcased that first mover advantage in transformation zones can achieve substantial capital appreciation prior to the subsequent GLS sites.

Moreover, developing a new housing estate within a mature estate like Bukit Merah, the project is poised to revitalise the area. New and fresh amenities could draw both first-time homebuyers or HDB upgraders seeking to live in a familiar estate or stay near their families.

Table 4: Price performance of condominiums that leverage on first mover advantage

| Development | Launch Month

| No. of Units | Median New Sale Launch Price PSF | Median Resale/Sub-sale Value (1Q 2025) | Appreciation |

| Livia | Jul 2008 | 605 | $670 | $1,318 | +96.7% |

| A Treasure Trove | Sep 2022 | 882 | $914 | $1,591 | +74.1% |

| Waterview | Nov 2010 | 696 | $922 | $1,480 | +60.5% |

Source: URA REALIS

A New Township and what it brings for the future Telok Blangah Development

On 15 May 2025, HDB announced that there will be around 1000 BTO flats that will be built on the site of the former Keppel Club will be launched for sale in October 2025.

The upcoming BTO site presents opportunities to anchor a new township in the area through injecting new amenities and vibrancy. However, buyer sentiment for the future development at the Telok Blangah site might be influenced by the upcoming BTO launches in the area. While some buyers welcome the added community infrastructure, some buyers who are seeking exclusivity and privacy may be deterred by the influx of BTO flats.

Given the close proximity of the site with future HDB development within the area, it is likely that future development at the GLS site will be a mass market product, stemming from upgrader demand from the new BTO enclave, when the 5-year Minimum Occupancy Period (MOP) period is met. The development in Telok Blangah will be offering an opportunity for buyers to upgrade to private housing while maintaining the convenience of being close to existing communal amenities and shops, retaining a sense of familiarity within the area.

As such, despite the presence of new HDB launches within the area, the Telok Blangah site offers strong exit strategies for buyers who are looking to purchase BTO flats and having the option to upgrade to private property thereafter.

While this is the maiden site sold in a new housing estate, strong demand for homes in the Greater Southern Waterfront has already been evident. The first BTO project (Berlayer Creek) launched in October 2025, as part of Bukit Merah Town, saw strong application rates, underscoring the area’s appeal. The application rates for 4-room flats were 3.1 and 23.8 for first and second timer applicants respectively.

4.0 Potential Buyer profile

The Telok Blangah site is the first private residential parcel to be introduced as part of a larger vision to transform the former Keppel Golf Course into a new housing precinct. As such, its future development could see heightened interest from investors eager for first-mover potential, alongside HDB upgraders currently residing in neighbouring planning areas.

While nearby condominiums such as Reflections at Keppel Bay cater primarily to the high-end market, the upcoming Telok Blangah GLS site is expected to attract a different buyer profile, particularly upgraders from mature HDB estates in Bukit Merah and Queenstown.

HDB upgraders from nearby Queenstown and Bukit Merah could see this future development as an opportunity to upgrade. The benefits of having first mover advantage thus becomes more relevant for upgraders, where they will want to ride the waves of the GSW transformation.

Table 5: Average Transacted Price of HDBs in Bukit Merah and Queenstown (1Q 2025)

Area | 4-room | 5-room | Executive |

Bukit Merah | $884,337 | $1,040,197 | - |

Queenstown | $932,560 | $1,154,179 | $1,299,250 |

Source: data.gov.sg

5.0 Supply outlook

While the site holds strong locational fundamentals and appeal, developers are expected to approach this site tender with measured optimism due to emerging headwinds that may moderate bid aggressiveness. One key consideration will be a growing supply pipeline of private housing and existing housing stock.

Table 6: Expected supply pipeline of private housing for 2025 and 2026

Category of Stock as of 15 May 2025 | Quantity of housing units |

Unsold Stock as of 1Q 2025 | 18,270 |

2H 2024 and 1H 2025 GLS | 8,415 |

Upcoming new launches in 2025 through 2026 | 6,338 |

Source: ERA Research & Market Intelligence, URA

Given that the above table have not yet included 2H 2025 GLS confirmed list, the estimated supply of private housing is likely to exceed 33,000 units. In addition, the former Keppel Club area will have around 3,000 private homes. The Telok Blangah site while enjoying the value of scarcity and appeal, will be facing stiff competition, many of which will be competing for the same buyer pool.

Further headwinds to be expected

Owing to prevailing economic conditions, developers are facing increased headwinds in the form of higher construction costs, which have dampened bidding appetite. This is apparent through the subdued interest shown for the two site tenders that recently closed in April 2025: While Lentor Gardens drew two bids, Media Circle (Parcel B) saw zero bidders.

In contrast, prior to the closing of the abovementioned tenders, a parcel at Bayshore Road attracted eight bidders in March 2025, with a significant 38.5% gap between the top and eighth bids. This popularity was likely due to the Bayshore Road parcel being the first residential site to be launched in the future Bayshore housing estate. The site’s close proximity to Bayshore MRT may have also been an additional draw for developers.

Table 7: GLS site tenders closed in Jan-Nov 2025

Tender close date | Site | No. of units | Region | No. of bidders | Highest bid price ($) | Land rate psf ppr ($) |

Jan-25 | Dairy Farm Walk | 540 | OCR | 2 | $505 M | $1,020 |

Jan-25 | Tengah Garden Avenue | 860 | OCR | 3 | $675 M | $821 |

Feb-25 | River Valley Green (Parcel B) | 580 | CCR | 5 | $628 M | $1,420 |

Mar-25 | Media Circle (Parcel A) | 345 | RCR | 3 | $315 M | $1,037 |

Mar-25 | Bayshore Road | 515 | OCR | 8 | $659 M | $1,388 |

Apr-25 | Lentor Gardens | 500 | OCR | 2 | $429 M | $920 |

Apr-25 | Media Circle (Parcel B) | 500 | RCR | 0 | - | - |

Jun-25 | Lakeside Drive | 575 | OCR | 6 | $608 M | $1,132 |

Jun-25 | Dunearn Road | 380 | CCR | 9 | $492 M | $1,410 |

Jul-25 | Chuan Grove (2H 2024) | 550 | OCR | 7 | $704 M | $1,376 |

Jul-25 | Holland Link | 240 | CCR | 5 | $368 M | $1,432 |

Aug-25 | Senja Close (EC) | 295 | OCR | 5 | $253 M | $771 |

Aug-25 | Woodlands Drive 17 (EC) | 420 | OCR | 5 | $361 M | $782 |

Sept-25 | Chuan Grove (2H 2024) | 505 | OCR | 5 | $624 M | $1,331 |

Sept-25 | Sembawang Road (EC) | 345 | OCR | 4 | $198 M | $692 |

Sept-25 | Chencharu Close | 875 | OCR | 3 | $1,013 M | $980 |

Oct-25 | Dorset Road | 425 | RCR | 9 | $524 M | $1,338 |

Oct-25 | Upper Thomson Road (Parcel A) | 595 | OCR | 5 | $614 M | $1,062 |

Nov-25 | Telok Blangah Road | 745 | RCR | 4 | $918 M | $1,326 |

Source: URA, HDB, ERA Research and Market Intelligence

With this slew of GLS site awarded since 2H 2024, there is a distinct likelihood that some 4,560 units are set to launch between 2025 to 2026. Furthermore, with another five sites currently open for tender, and another three sites set to launch in June 2025, this could result in another 4,010 units being added to the pipeline.

Developers are expected to remain upbeat on the residential market, as Singapore is undergoing several shifts that will contribute to the sustained demand for new homes.

Firstly, Singapore’s predominantly leasehold residential market drives demand for newer properties with longer remaining tenures, with many locals believing in trading up to newer developments with longer remaining leases to preserve asset value. This activity, in turn, supports the growth of property values over time.

Secondly, many GLS sites are located in future growth areas that are earmarked for development under URA’s Master Plans, this fosters buyer confidence in the future appreciation prospects of new homes in said locations.

Thirdly, the progressive payment schemes offered by new homes benefits first-time homebuyers by pacing payments with construction progress. This payment structure allows those in the early stages of their careers to accumulate more savings and grow their earnings, thus making it easier to meet full mortgage obligations later on.

Conclusion and Tender Closing Comments

Given developers’ strong appetite for land in recent tenders, the subdued showing of three bidders is a clear outlier. This also contrasts sharply with the fierce competition for past sites in emerging precincts.

Despite being in an untested market, buyers have been keen on sites that are presently less developed, buying into the transformation of the estate. In particular, sites that are or will be close to amenities and transport nodes are expected to see high demand.

There is growing optimism within Singapore’s residential market, underpinned by the strong sales performance seen across the 2025 launches to date. We expect to see some developers looking to replenish their land bank in anticipation of sustained demand.

Currently (as of 4 Nov 2025), excluding Executive Condominiums, three GLS sites remain open for tender, with another six sites on the 2H 2025 Confirmed List to be launched.

Developers who are unsuccessful in their current bids may turn their attention to upcoming RCR plots slated to be launched for tender in the coming months, including Dover Road, Tanjong Rhu Road and Kallang Avenue.

I confirm that I have read theprivacy policy and allow my information to be shared with this agent who may contact me later.