Upper Thomson Road (Parcel A) – Government Land Sale Site Analysis

- Stanley Lim

- 8 min read

- Research

- 31 Oct 2025

URA launched the tender for the Government Land Sale (GLS) parcel at Upper Thomson Road (Parcel A) for a residential with commercial at 1st storey development on 24 June 2025. The tender subsequently closed on 23 October 2025.

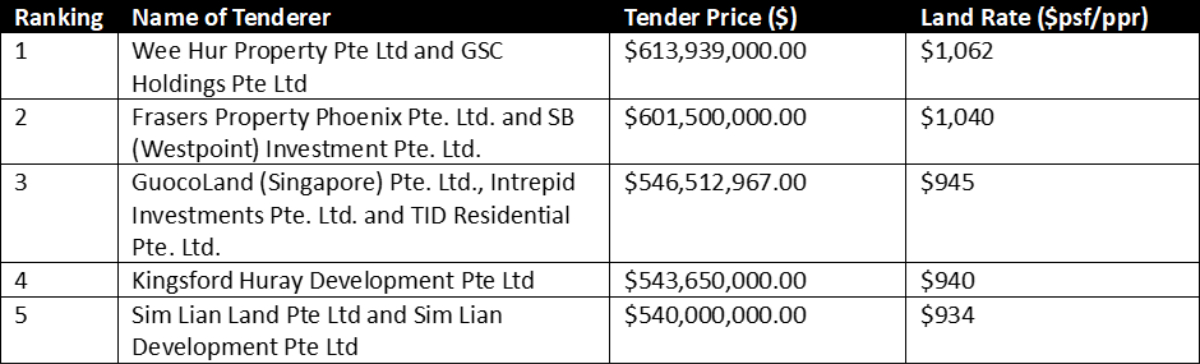

In total, the site drew interest from five bidders, with the top bid of $613.9 million (or $1,062 psf ppr) submitted by Wee Hur Property Pte Ltd and GSC Holdings Pte Ltd.

Table 1: Bidders for Upper Thomson Road (Parcel A) site

Upper Thomson Road (Parcel A) was previously launched for sale in December 2023 with a long-stay serviced apartment (SA2) requirement. The clause, however, dampened developer interest, resulting in no bids at the time when the initial tender closed in June 2024.

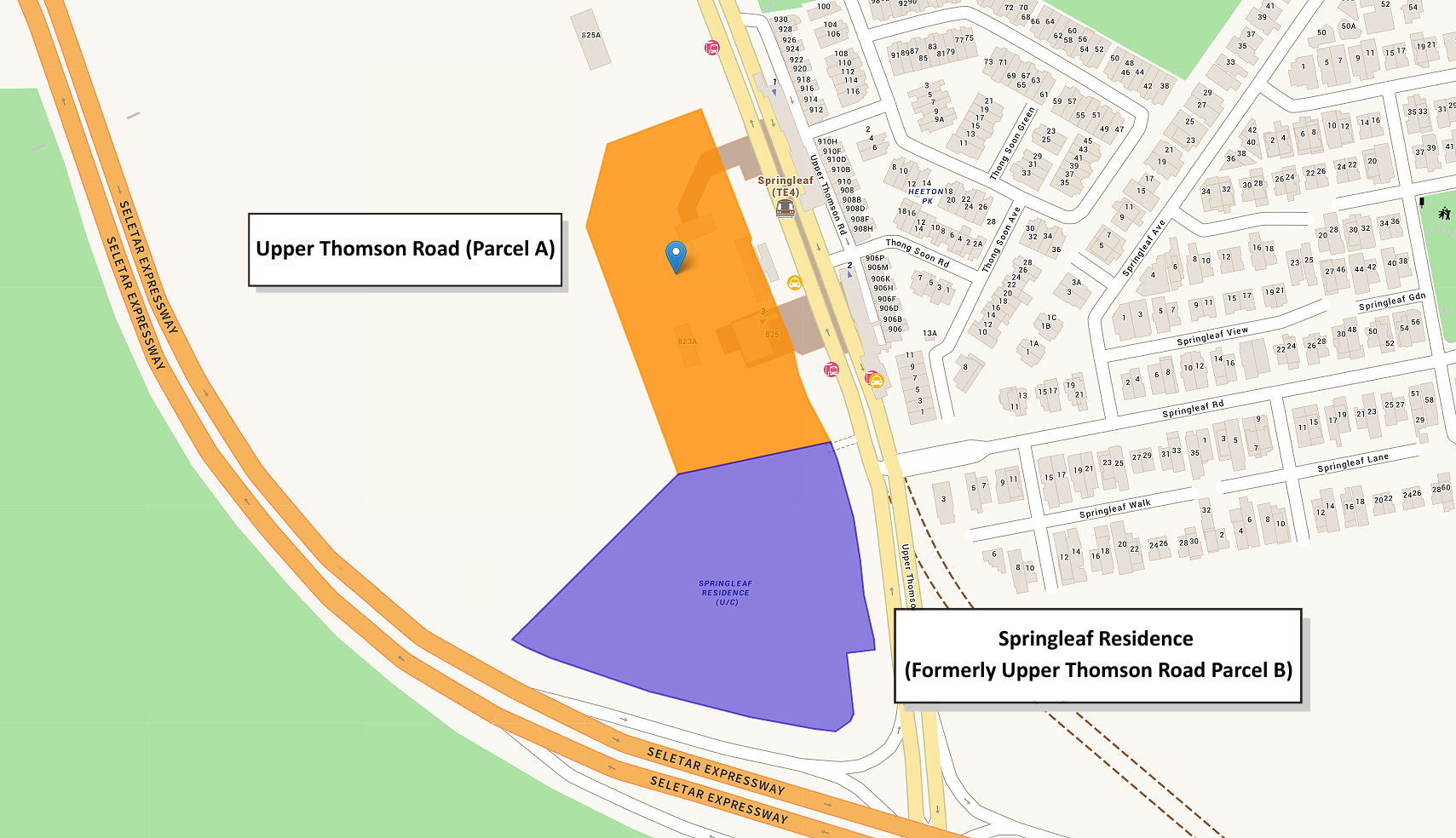

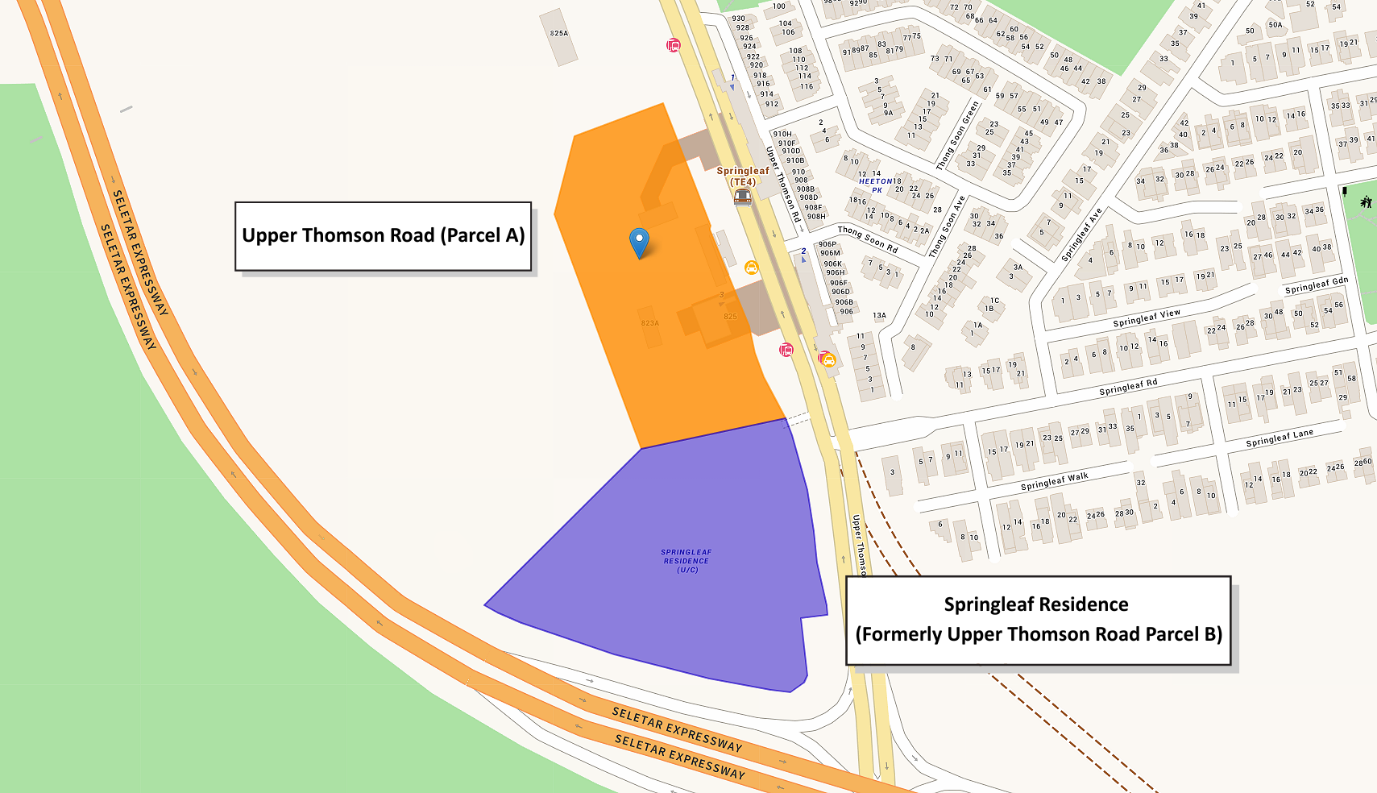

Following its subsequent tender after the rollback of the SA2 typology, Parcel A emerged as one of two pioneering high-rise residential plots in the Springleaf precinct, located next to its sister site, Upper Thomson Road (Parcel B).

Table 2: Bidders for Upper Thomson Road (Parcel B) site

Parcel B was developed and launched as Springleaf Residence by its sole bidder – a joint venture between GuocoLand (Singapore) Pte. Ltd. and Intrepid Investments Pte. Ltd. The development achieved a strong take-up rate of 92% during its launch weekend in August; this success likely strengthened bidder confidence in Parcel A’s potential and the Springleaf precinct, which was previously an untested market for non-landed developments.

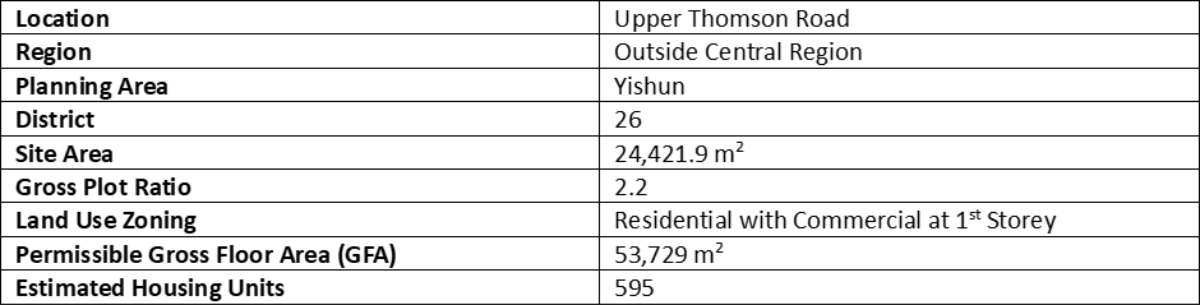

Site Details

Table 3: GLS site details

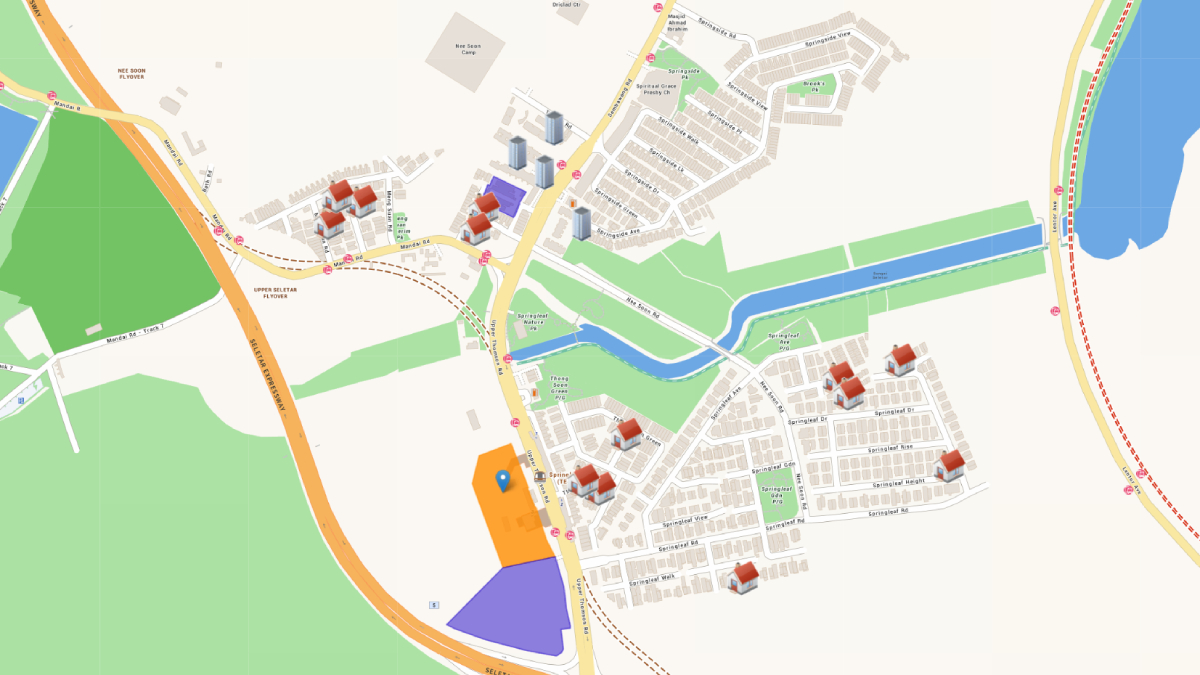

Figure 1: Location of Upper Thomson Road (Parcel A and Parcel B)

Springleaf shares several key characteristics with the Lentor Hills estate to the south, these include proximity to established landed housing enclaves, as well as access to nearby stations on the Thomson-East Coast Line (TEL). However, the biggest differentiator is Springleaf’s proximity to various green spaces.

These include the Central Catchment Nature Reserve (CCNR) and Upper Seletar Reservoir to the west, as well as Springleaf Nature Park and Lower Seletar Reservoir to the east.

While these natural spaces do enhance the site’s appeal, their proximity to Parcel A also means Biodiversity Sensitive Urban Design (BSUD) strategies must be adopted during planning and building stages. As a result, developers may face higher consultancy and construction costs.

Locational Attributes

Neighbourhood amenities

As a predominantly low-rise and tranquil neighbourhood, Springleaf’s present amenities are currently limited to a cluster of convenience stores and noteworthy eateries (e.g., Springleaf Prata, Bernie’s Restaurant). These are housed in a row of shophouses situated directly opposite Parcels A and B, on the other side of Upper Thomson Road.

This current gap in amenities could be addressed in time, as Upper Thomson Road (Parcel A) consists of a minimum of 1,000 sqm of Gross Floor Area (GFA) for a childcare centre, along with 1,500 sqm of commercial space allocated for either supermarket, retail or restaurant use.

There is also a notable absence of primary schools within the immediate vicinity of Parcel A, as none fall within the 1km radius required for priority admission. This is likely to have a bearing on the homebuying decisions of families with young children and/or couples with plans to start a family.

Transport and connectivity

Parcel A’s main advantage lies in its immediate proximity to Springleaf MRT station, which is located on the Thomson-East Coast Line (TEL). The site’s future development will also eventually integrate the station’s existing entrance/exit structure, providing residents with an even greater degree of convenience.

Via the TEL, residents will have a direct transit route to key destinations in central Singapore, including Orchard Road and Marina Bay. The TEL also offers excellent connectivity to the north, with Woodlands Regional Centre being two MRT stops away. By late-2026, the Johor-Bahru-Singapore Rapid Transit System (RTS) at Woodlands North will be easily reachable as well, just three stops up from Springleaf MRT station.

For those driving, a 15-minute commute along Upper Thomson Road provides access to more shopping centres like Thomson Plaza and Junction 8. This connectivity extends to Bishan Town Centre, identified as a future sub-regional centre under URA’s Master Plan 2025.

Price and Market Trends

In recent years, non-landed residential homes in District 26 have seen robust market uptake, evident by the string of successful new launches at the Lentor Hills estate. As a result, these favourable outcomes have strengthened developer optimism toward future land opportunities across the wider district, including the Springleaf precinct.

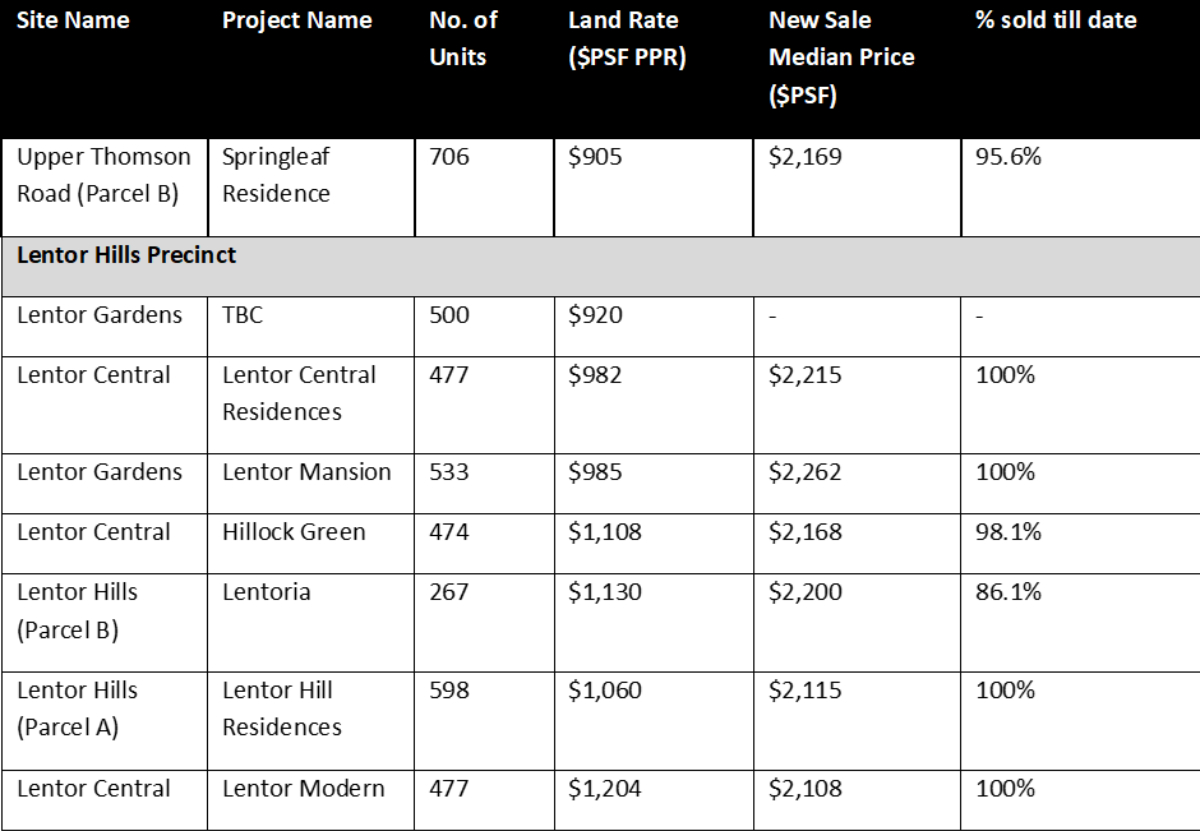

Table 4: Comparable recent sites and projects in D26

Since 2022, Lentor has seen six new launches totalling approximately 2,900 units. As of 29 October 2025, most of these developments are also now either fully sold out or nearing sold out, with fewer than 50 units remaining on the market. Furthermore, aside from the Lentor Gardens site acquired by the Kingsford Group in April with an estimated 530 units, there is no other foreseeable new supply within D26 in the immediate future.

These market factors, combined with the successful launch of Springleaf Residence, likely contributed to developer interest during Parcel A’s tender. Similarly, with new home supply remaining limited in both Springleaf and Lentor, the future development on Parcel A is well positioned to draw buyer interest.

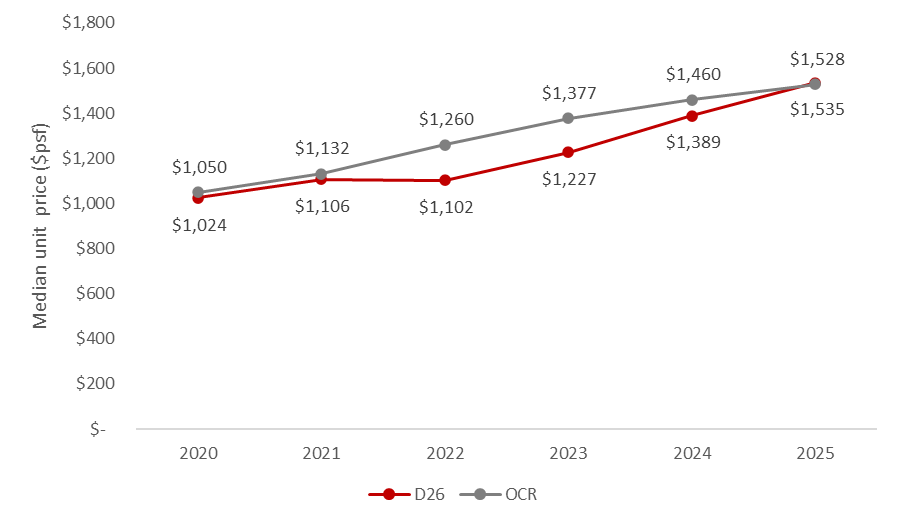

Steady Price Appreciation in District 26

Chart 1: Price performance of resale non-landed private homes in D26 vs Outside Central Region (OCR)

Beyond favourable sales conditions, D26 has also maintained a track record of steady price growth in the non-landed private housing segment. Between 2021 to 2025, median unit prices of resale non-landed homes in D26 rose by 49.9%, from $1,106 psf to $1,535 psf. This growth rate is in line with, and even slightly outpaces, the 45.5% increase recorded for the entire OCR, hence demonstrating the potential of D26 properties.

That said, D26’s annual price trajectory has not been entirely linear. In 2022, prices dipped marginally by 0.4% year-on-year before rebounding in subsequent years, supported by Lentor’s launches that helped spur interest in D26’s broader private home market.

Potential Demand/Buyer Profile

Table 5: 3Q 2025 median quantum prices for resale landed and new non-landed private homes in D26

Given the prevalence of landed properties in Springleaf, future demand for Parcel A’s development will likely arise from right-sizers from nearby enclaves along Upper Thomson Road, Mandai Road or Sembawang Road. Based on median landed home prices in District 26, they are likely able to transition comfortably into a new condominium. This affordability should likewise extend to owners of older non-landed properties, given the potential sales proceeds from their current homes.

Similarly, adult children of D26 landed homeowners may represent prospective buyers, especially if they wish to continue living in the same neighbourhood.

Table 6: Private residential stock breakdown by planning areas in D26 in 3Q 2025

In the same vein, developers are likely to view D26 as a ready pool of potential demand. This is given its healthy stock of 3,571 non-landed and 2,769 landed homes that could translate into future right-sizing activity.

Figure 2: Landed home estates near Upper Thomson Road (Parcel A)

Upgrader demand for Parcel A’s future development may arise from owners of larger HDB flats, specifically 5-room and Executive units, in towns such as Ang Mo Kio, Bishan, Woodlands, and Yishun. Within these locations, median resale prices for the aforementioned flat types range from approximately $677,000 to $1.2 million as of 3Q 2025. Hence, their owners might have sufficient capital to afford a new non-landed private home at Springleaf.

Table 7: Median resale HDB prices in Ang Mo Kio, Bishan, and Yishun in 3Q 2025

Furthermore, between 2026 and 2029, Ang Mo Kio, Bishan, Woodlands, and Yishun are expected to see a combined total of over 9,000 units completing their Minimum Occupation Period (MOP). This will likely bolster the pool of potential HDB upgraders in the coming years.

Conclusion

The participation of five bidders for Upper Thomson Road (Parcel A) signals strong developer confidence, buoyed by the robust sales performance of recent new launches and a lower interest rate environment.

This solid turnout also marks a clear turnaround in developers’ sentiment from the cautious tone seen last year, when the nearby Upper Thomson Road (Parcel B) site drew only one bid from a GuocoLand–Hong Leong Holdings joint venture in April 2024. As such, renewed developer confidence is evident on the back of improving market momentum.

At $613.9 million ($1,062 psf ppr), the top bid put in by Wee Hur Property and GSC Holdings is just 2% more than the second-highest by Frasers Property and SB (Westpoint) Investment at $601.5 million ($1,040 psf ppr). This tight margin signals strong confidence in the site’s potential as a pioneering high-rise development at Upper Thomson.

Hence, based on the land cost, the site could be launched at an average price of at least $2,300 psf.

Once successfully awarded, the site could enter the market around 2027 as fresh supply in both the OCR and Upper Thomson Road area. With Springleaf Residence likely to be fully sold by that time, the new site is well-positioned to capture unmet demand from interested buyers who were unable to secure a unit.

I confirm that I have read theprivacy policy and allow my information to be shared with this agent who may contact me later.