Economic Overview

Singapore’s economy further expanded by 3.8% year-on-year (y-o-y) in 1Q 2025, an increase from the 4.4% growth in 2024. However, on a quarter-on-quarter (q-o-q) basis, Singapore’s Gross Domestic Product (GDP) contracted by 0.8%. Among the sectors, the ‘Information & Communications, Finance & Insurance and Professional Services’ and the ‘Manufacturing’ Sector posted the sharpest GDP declines, contracting by 5.0% and 4.9% q-o-q respectively in 1Q 2025.

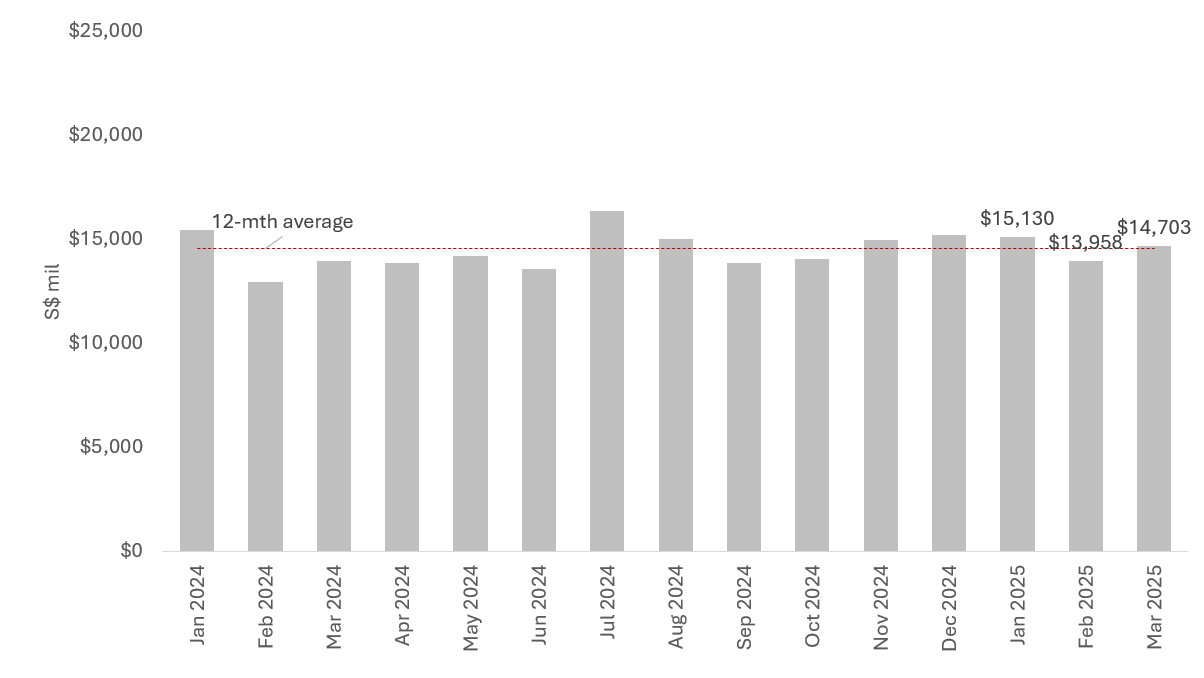

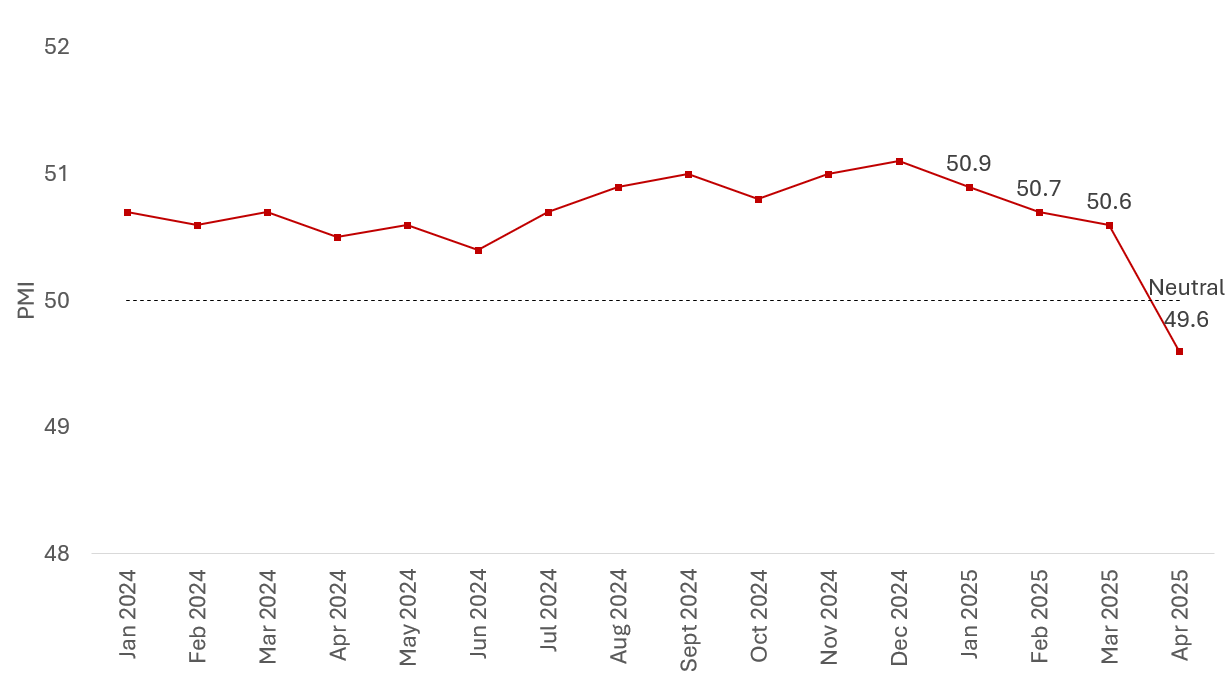

On a more positive note, Non-Oil Domestic Exports (NODX) remained above the previous 12-month average in January and March 2025, with only February registering a dip below the average. In the same vein, the Purchasing Manager Index (PMI) continued to indicate expansion, although it showed signs of gradual moderation over the first three months of 2025, with April’s PMI index dropping to under 50, ending a 19-month streak of expansion.

Chart 1: Non-Oil Domestic Exports and Manufacturing Exports

Source: Singstat, ERA Research and Market Intelligence

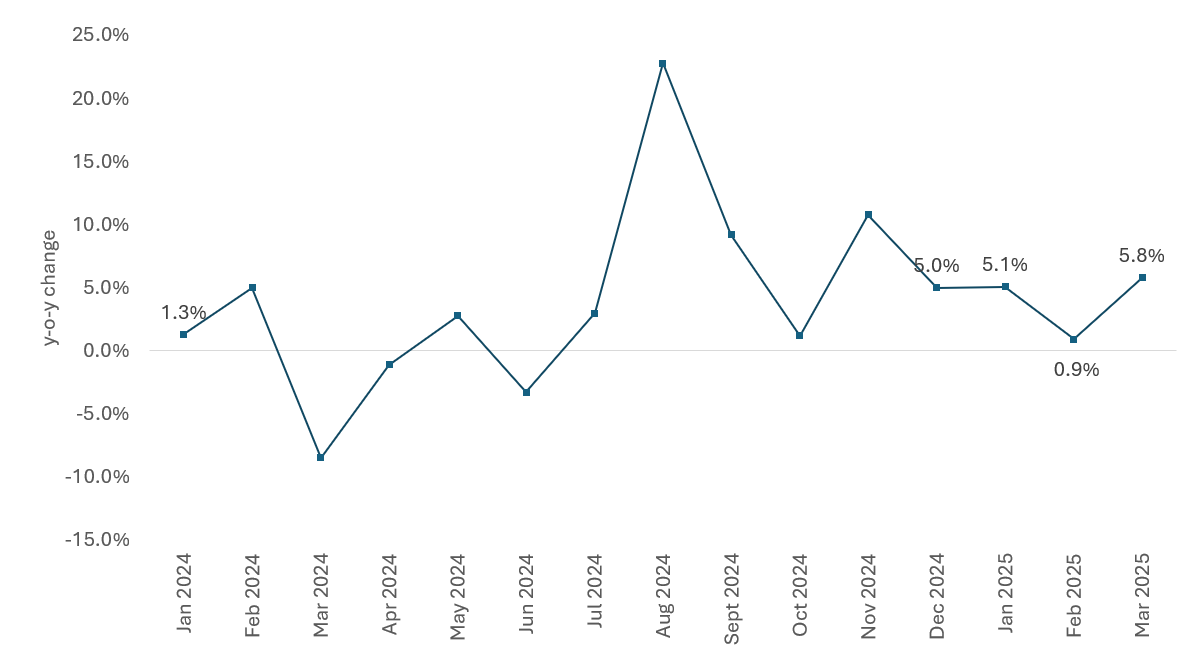

Chart 2: Manufacturing Output y-o-y Change

Source: Singstat, ERA Research and Market Intelligence

Chart 3: Purchasing Manager Index

Source: SIPMM, ERA Research and Market Intelligence

*The PMI reading with a score above 50 indicates that the manufacturing economy is generally expanding and that the economy is generally declining when the reading falls below 50, and a score of 50 indicates no change from the previous month.

Trump’s Tariffs Raises Uncertainty

US President Donald Trump’s unpredictable trade policy has instilled fear and uncertainty in financial markets. Singapore was viewed as an early “beneficiary,” as it faced the baseline 10% tariffs, the lowest among Asian countries. Firms seeking to mitigate risks in their supply chains from countries with higher rates may consider relocating or expanding production in Singapore.

However, Trump has since paused the tariffs for 90 days (from April 9, 2025) and capped all countries’ rates at the baseline 10%, except for China, Mexico, and Canada.

These fluid and ever-changing circumstances will keep firms on the sidelines. What happens after the 90 days remains to be seen. Trade partners could introduce retaliatory actions that may potentially intensify trade tensions. This could impact not just manufacturing, but also the demand for logistics and industrial services, as well as space and labour.

In light of the ongoing headwinds, the Monetary Authority of Singapore (MAS) has lowered Singapore’s 2025 GDP growth forecast to a range of 0.0–2.0% due to heightened geopolitical challenges. As a result, business confidence regarding future expansion is expected to be more measured, with firms likely adopting a cautiously optimistic stance.

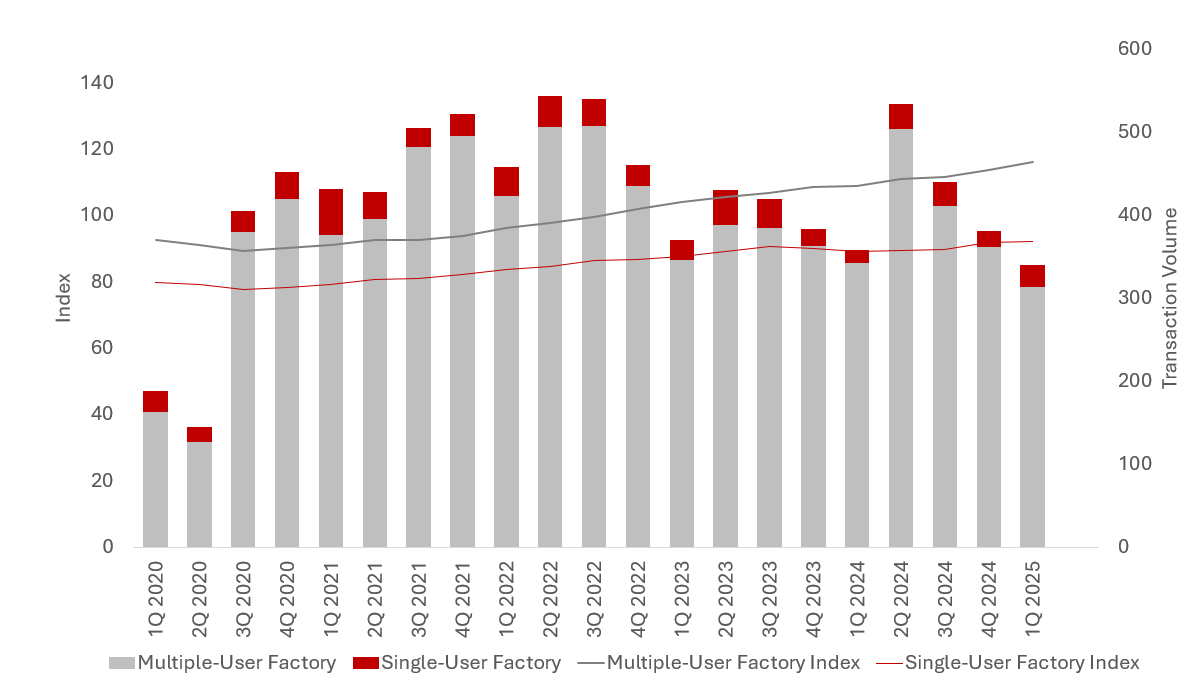

Price and Sales Transaction Volume

Prices for Multiple and Single-user Factory increased by 1.9% and 0.4% quarter-on-quarter (q-o-q) in 1Q 2025.

In contrast, Multiple-user Factory transaction volume fell by 13.3% q-o-q, marking a third consecutive quarter of decline. Single-user Factory, however, reversed the 34.5% q-o-q decline in 4Q 2024, achieving a rise of 36.8% in 1Q 2025.

CT Pemimpin, a new freehold B1 industrial building, was launched in February 2025. With its practical design, featuring a high floor-to-ceiling height, direct vehicular access, a large circulation area, and units with efficient and open layouts, it ticked most boxes and attracted buyers. Located between Marymount and Bishan MRT Stations, its central location was a big draw. Finding a suitable industrial space with specifications that meet their business needs is not an easy feat for many end users. It managed to sell 89% on launch day and is now fully sold, although no caveats have been lodged as of 24 April 2025.

Chart 4: Price Index and Transaction Volume

Source: URA, ERA Research and Market Intelligence

The most notable transaction in 1Q 2025 occurred on 13 March 2025, when JTC awarded the tender for the industrial site at 23 Lok Yang Way to Soilbuild Group Holdings Ltd for nearly $70.1 million. Additionally, a freehold Multiple-user Factory at 21 New Industrial Road was sold on 5 February 2025 for $62.0 million.

Table 1: Top Five Sales Transactions in 1Q 2025, based on caveats lodged

Source: URA, ERA Research and Market Intelligence; *Rounded up to the nearest year

Leasing and Leasing Volume

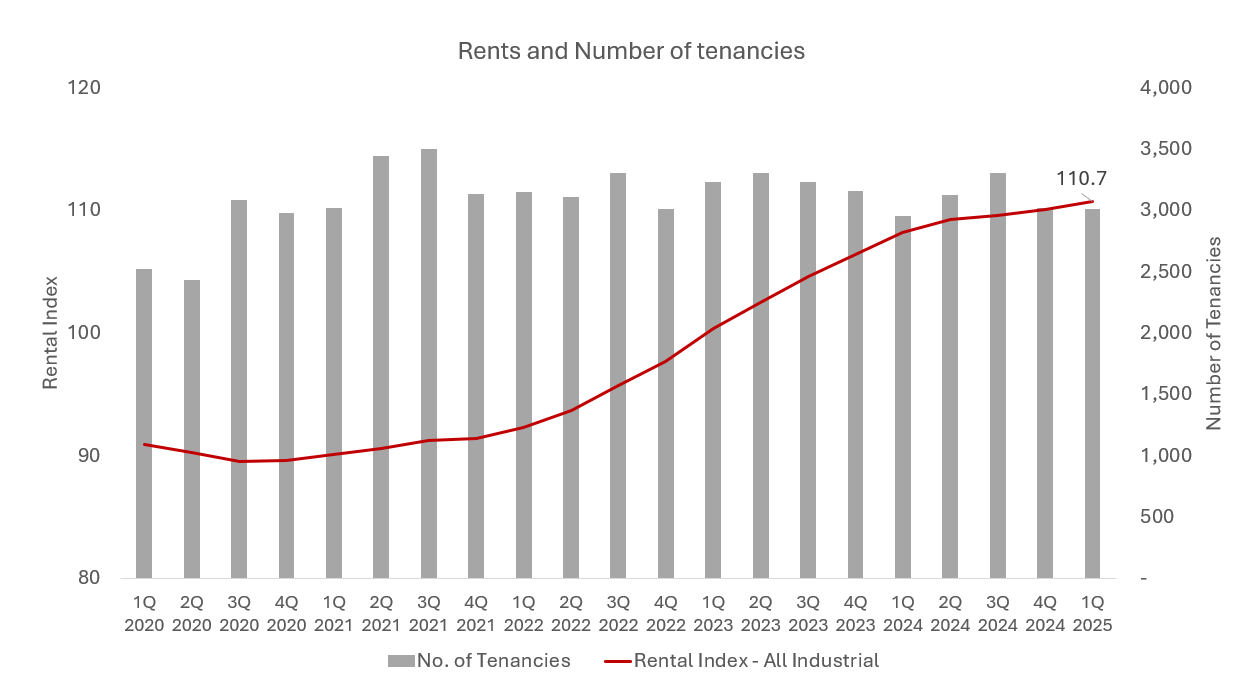

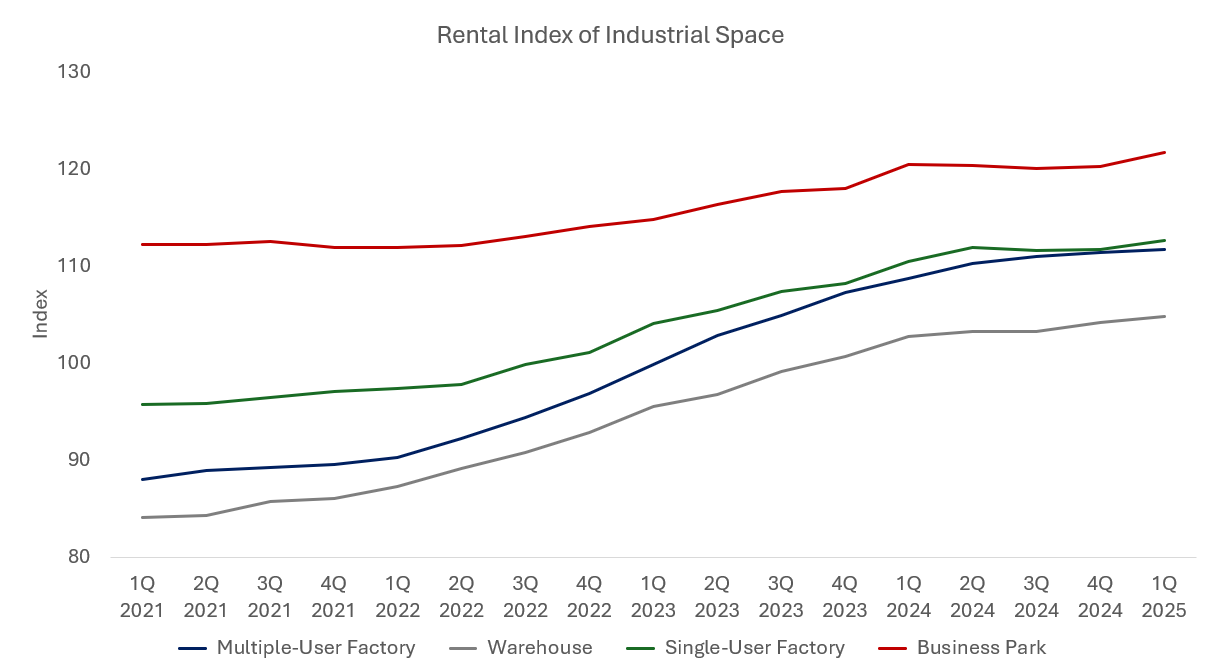

The JTC All Industrial Rental Index continued its upward trend, rising for the eighteenth consecutive quarter in 1Q 2025. Similar to 4Q 2024, rents also grew by 0.5% this quarter. However, despite the marginal increase, rents are likely to plateau and grow at a slower rate. Among all property types, Business Parks rents grew the most this quarter, rising 1.2% q-o-q.

While the rental index has climbed marginally q-o-q, leasing volume has decreased by a slight 0.4% q-o-q to 3,008 tenancies signed in 1Q 2025. This follows a decline in leasing transactions of 8.6% in 4Q 2024.

Chart 5: Rental Index and Number of Tenancies for Industrial Properties

Source: JTC JSpace, ERA Research and Market Intelligence

Chart 6: Rental Index and Number of Tenancies for Industrial Properties

Source: JTC JSpace, ERA Research and Market Intelligence

Upcoming Supply

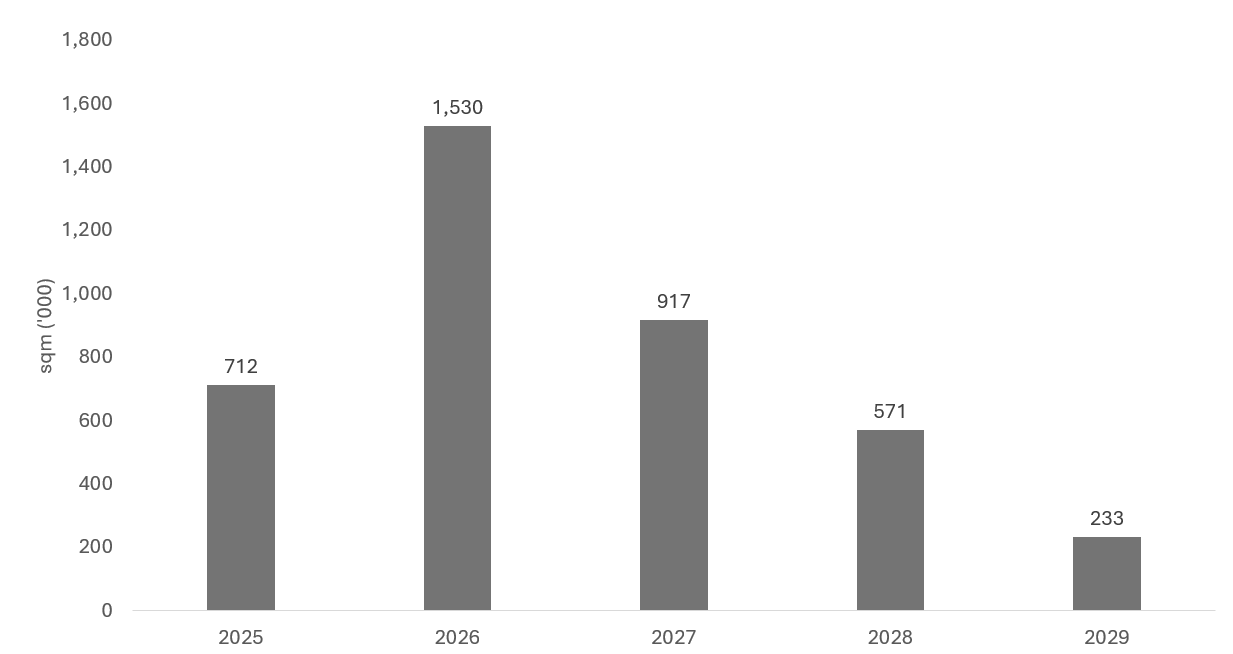

By the end of 2025, JTC forecasts that another 24 new industrial developments will attain their Temporary Occupation Permit (TOP). This will inject an additional 597,000 sqm of industrial space into the market. Some notable developments include a warehouse at DSV Pearl by Logos Pacv SG Propco Pte Ltd in Tukang Innovation Drive (67.700 sqm), a Business Park development in Punggol Digital District by JTC Corporation (72,960 sqm), and JTC Space @ Ang Mo Kio (117,230 sqm). In total, only 264,970 sqm (44.4% of total uncompleted GFA) is developed by JTC.

This slew of completions could cater to the demand for industrial spaces. However, since some of these leases have already been pre-committed, the occupancy rate is likely to remain stable.

New industrial spaces (Multiple-user Factory) developed by the private sector are likely to attract significant attention from business owners looking to purchase their own industrial space.

Following CT Pemimpin’s stellar performance, CT Foodnex and Ecofood@Mandai, both freehold strata food factories, could see renewed interest as well. Despite being located in the north-west of Singapore, they still present opportunities for businesses in the food and beverage (F&B) sector. With many restaurants and eateries across shopping malls and neighbourhood estates, these central kitchens could pique the interest of F&B owners or food caterers.

Chart 7: Supply of Industrial Spaces’ Expected Completion Year

Source: JTC JSpace, ERA Research and Market Intelligence

In conclusion

Protectionist measures between major trade partners such as the US, Canada, and China could cause ripple effects in small and open economies like Singapore. With cautiously optimistic sentiment, we are likely to see more muted growth in industrial rents and prices. However, the extent of growth would be moderated as firms remain cautious about the global geopolitical outlook amid a higher supply of industrial stock with more completions in 2025. Expansion plans could be put on the back burner as businesses navigate the prevailing headwinds.

Furthermore, the slowdown in Fed rate cuts due to persistent inflation rates may lead investors to remain on the sidelines. Transaction numbers might decrease, though not significantly. Due to tighter supply, prices and rents continue to grow at a sustainable pace.

In line with Singapore’s forecasted economic growth projections, prices and rents of industrial properties could see more measured growth, rising by up to 2% y-o-y in 2025.

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from relevant sources and/or seek appropriate advice from professionals such as valuers, financial advisers, bankers, and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accept no responsibility for the accuracy, reliability, and/or completeness of the information provided. Copyright in this publication is owned by ERA, and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.

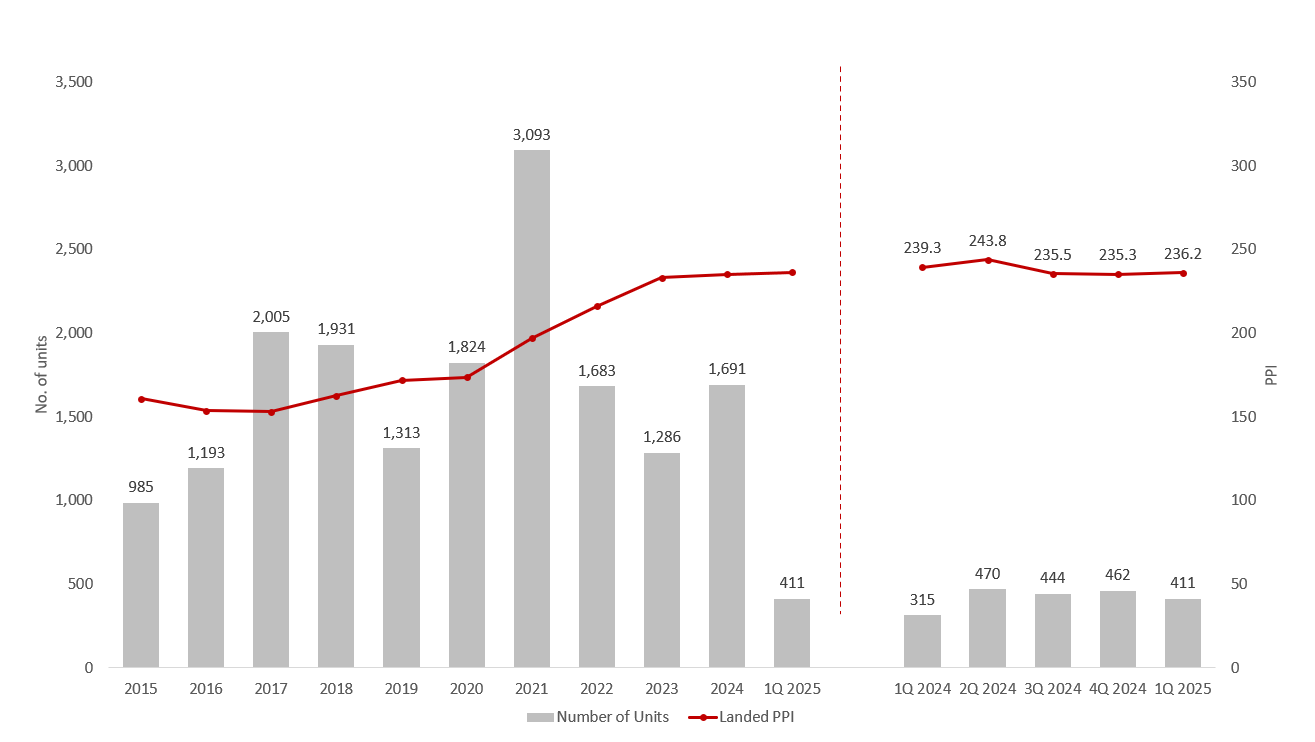

The Landed Price Index rose 0.4% quarter-on-quarter (q-o-q) in 1Q 2025, reversing the 0.1% decrease seen in 4Q 2024. This occurred despite fewer landed homes being transacted in 1Q 2025.

Landed Property Price Index and Transactions

The Landed Property Price Index remained largely stable in 1Q 2025, reporting a growth of 0.4% q-o-q. However, this was still a 1.3% decline year-on-year (y-o-y).

Meanwhile, landed property transactions declined by 11.0% quarter-on-quarter but increased by 9.6% compared to last year.

The increase in landed transactions compared to a year ago could be largely due to the moderating interest rate environment and rising non-landed home prices, which have paved the way for Singaporeans to upgrade to landed homes.

Chart 1: Landed Property Price Index and Transactions

Source: URA as of 26 Apr 2025, ERA Research and Market Intelligence

Price Quantum

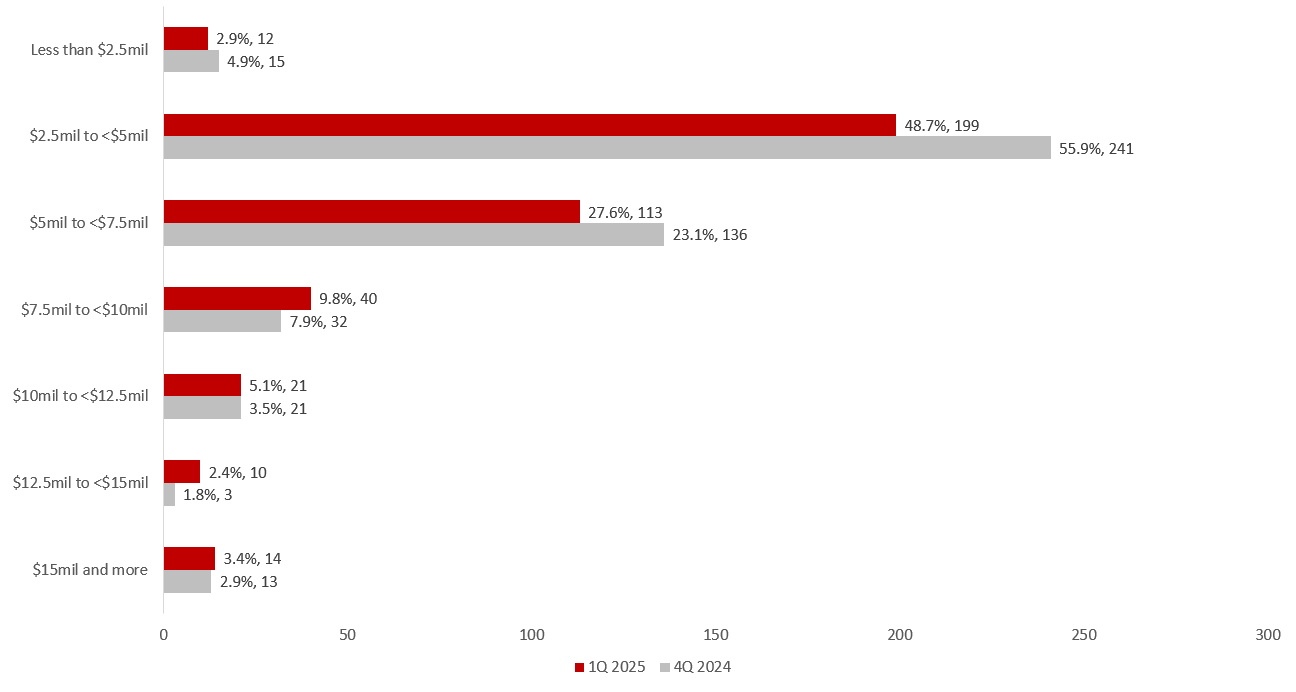

Under half of the landed homes sold in 1Q 2025 were priced below $5 million. Meanwhile, the $5 million to $10 million segment experienced a 0.8% contraction in sales volume, while the sub-$5 million segment saw a more significant 17.6% quarter-on-quarter decrease in transactions.

In contrast, demand for high-end landed homes grew in 1Q 2025, with URA caveats indicating a 21.6% quarter-on-quarter increase in transactions for landed properties valued at $10 million and above.

The highest-priced deal in 1Q 2025 was a Good Class Bungalow (GCB) located at 21 Gallop Park. This 16,307-square-foot freehold home was reportedly sold by Chua Soon Hock, the founder of Singapore hedge fund Asia Genesis Asset Management, for $58 million. Another GCB at 16A Leedon Park was sold for $45.8 million.

Due to Singapore’s political and economic stability, particularly during this period of uncertainty, GCBs, characterised by their consistently strong demand and limited supply, are viewed as safe haven assets that offer a hedge for long-term wealth preservation and will continue to attract newly minted Ultra-High Net Worth citizens.

Chart 2: Price Quantum 4Q 2024 versus 1Q 2025

Source: URA, ERA Research and Market Intelligence

Type of properties

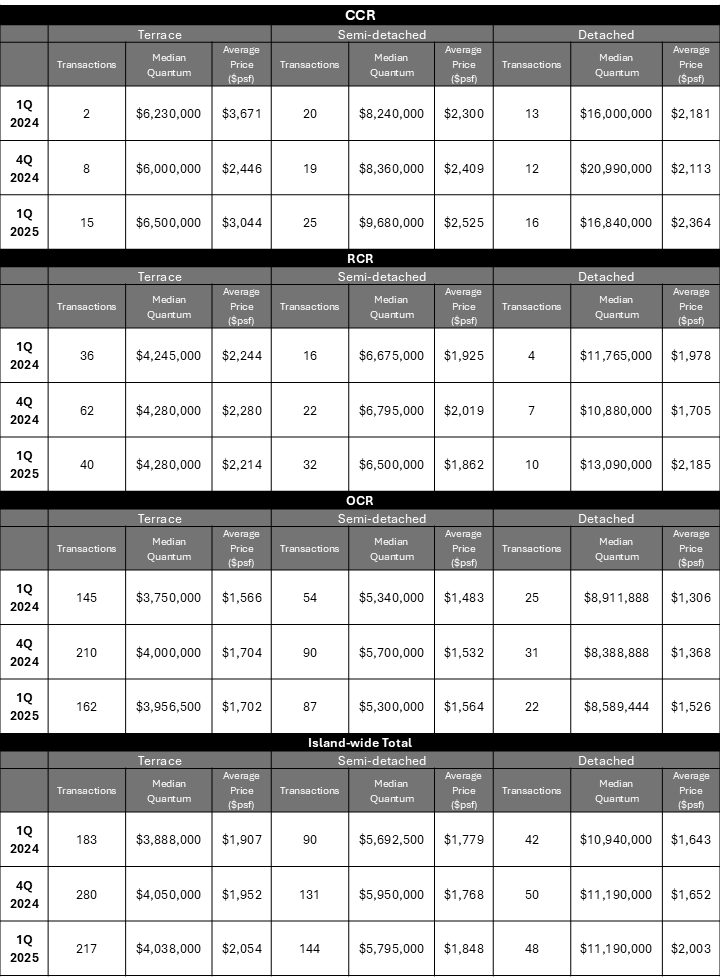

Overall, the number of semi-detached and detached homes sold remained similar to 4Q 2024. However, fewer terrace homes were sold in 1Q 2025 (217 units) compared to the 280 units in 4Q 2024.

Outside the Core Central Region (CCR), terrace houses experienced a sharp decline in transaction volume, mainly due to high prices. Nonetheless, demand for larger homes remained strong, with semi-detached homes recording a 31.6% quarter-on-quarter increase and detached homes seeing a 33.3% quarter-on-quarter increase, respectively.

Table 1: Transaction Volume and Average Price by Landed Property Type/Market Segment

Source: URA as of 17 Apr 2025, ERA Research and Market Intelligence

Purchasers address indicator

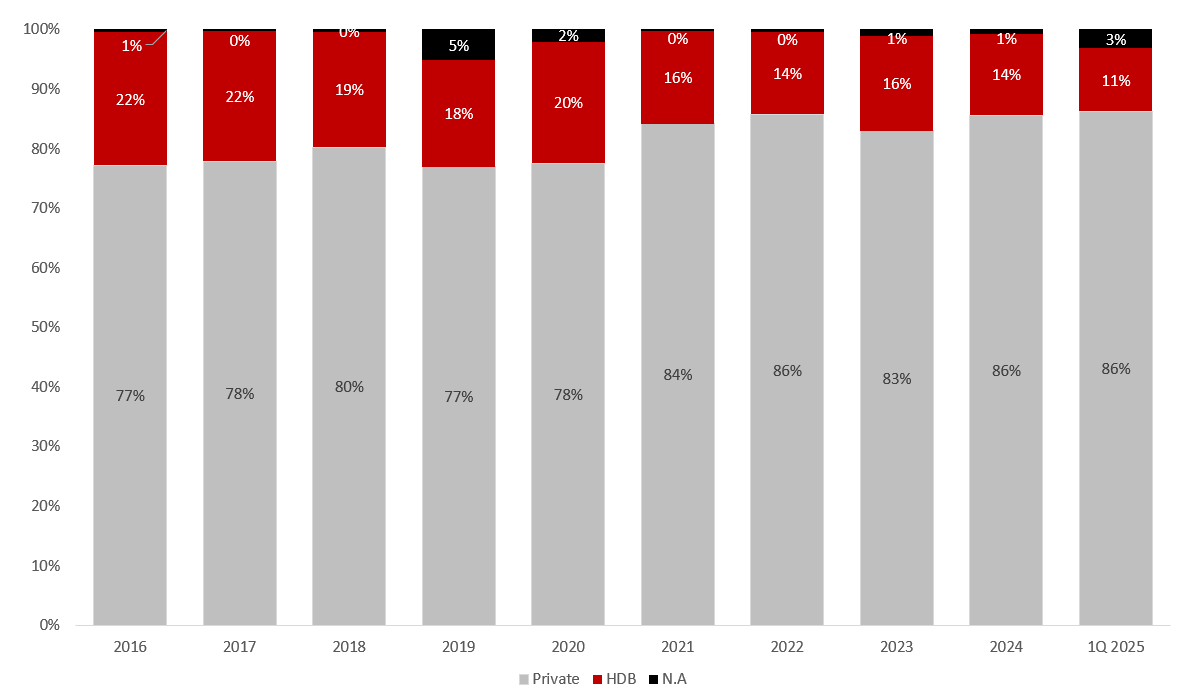

Amid rising landed housing prices, the proportion of HDB owners upgrading to landed properties continues to shrink further in 1Q 2025. While landed upgraders with HDB addresses represented 14% of the total upgrader population in 2024, that percentage decreased to 11% in 1Q 2025. Although HDB resale prices have risen for the 23rd consecutive quarter, upgrading to landed homes remains more challenging due to their significantly higher starting prices.

This finding also aligns with a trend that began in 2017, specifically a steadily shrinking share of HDB-to-landed upgraders from the last high of 22% in that year.

Chart 3: Landed home buyer profile

Source: URA, ERA Research and Market Intelligence

In conclusion

With potentially strong economic headwinds and geopolitical uncertainties, upgraders may not be willing to pursue landed homes in the short term. Moreover, rising prices and elevated-for-longer interest rates could price some buyers out of the landed home market.

On the other hand, larger landed homes with a higher price quantum could still experience strong demand. Wealthier buyers with greater purchasing power may view this as an opportune time to enter the market, especially given the limited supply of such homes.

With landed homes experiencing a slight decrease in transactions in 1Q 2025 and facing ongoing economic headwinds, ERA has revised its earlier forecast to a year-on-year price growth of 3-5%. Taking into account only non-strata landed homes. we estimate between1,500 to 1,800 landed transactions for 2025.

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.

下文由ERA公关经理岳开新翻译

数据来源为建屋发展局(HDB)与市区重建局(URA)于2025年4月1日发布的季度预估统计。

根据建屋发展局的预估数据显示,今年第一季组屋转售价格指数(RPI)上升至200.9,环比增长1.5%。

这标志着该指数已连续第20个季度增长,涨势有望与ERA此前预测的全年3%至6%增幅相符。

图一:组屋转售价格指数与交易量走势对比

资料来源:建屋局、ERA研究和市场情报(数据截至今年3月27日)

受季节性因素影响 组屋转售交易量下滑

2025年第一季共有6392个组屋单位转售,同比下降7.7%。

交易量减少的主要原因包括季节性淡季影响,以及今年2月推出超过一万个预购组屋(BTO)和剩余组屋(SBF)单位的大型配售活动。在大量新组屋供应下,部分买家可能将注意力从转售市场转向这些新推出的项目。

与2024年第四季相比,2025年首季三房式和四房式组屋交易量有所上升加,而公寓式组屋单位(Executive flat)的交易量则继续下滑。

今年2月,年度首轮预购组屋项目中,亮点包括女皇镇的两个优选地段组屋(Plus Flats)项目,以及位于兀兰和义顺真查鲁(Chencharu)的实惠组屋项目,其中后者是一个综合发展项目,设有巴士转换站和商业设施,进一步提升居住便利性。

相比预购组屋,剩余组屋的等候时间短。其中有四成的剩余组屋单位已完工,买家可在短时间内入住。

其余尚未竣工的SBF单位,也普遍拥有缩短的等待期。对于对入住时间要求不高的买家而言,这类组屋成为转售市场之外的实惠替代选项。

本次推出的剩余组屋还包括位于成熟市镇和市中心的单位,且不受新组屋政策黄金地段组屋模式(Prime Location Public Housing,简称PLH)的限制。结合更短的等待时间,这些单位吸引了大量申请,进一步分流了原本可能进入转售市场的购屋需求。

目前,申请者正等待选房结果。对于未能购得单位的买家,预计他们会在第二季回流转售市场。

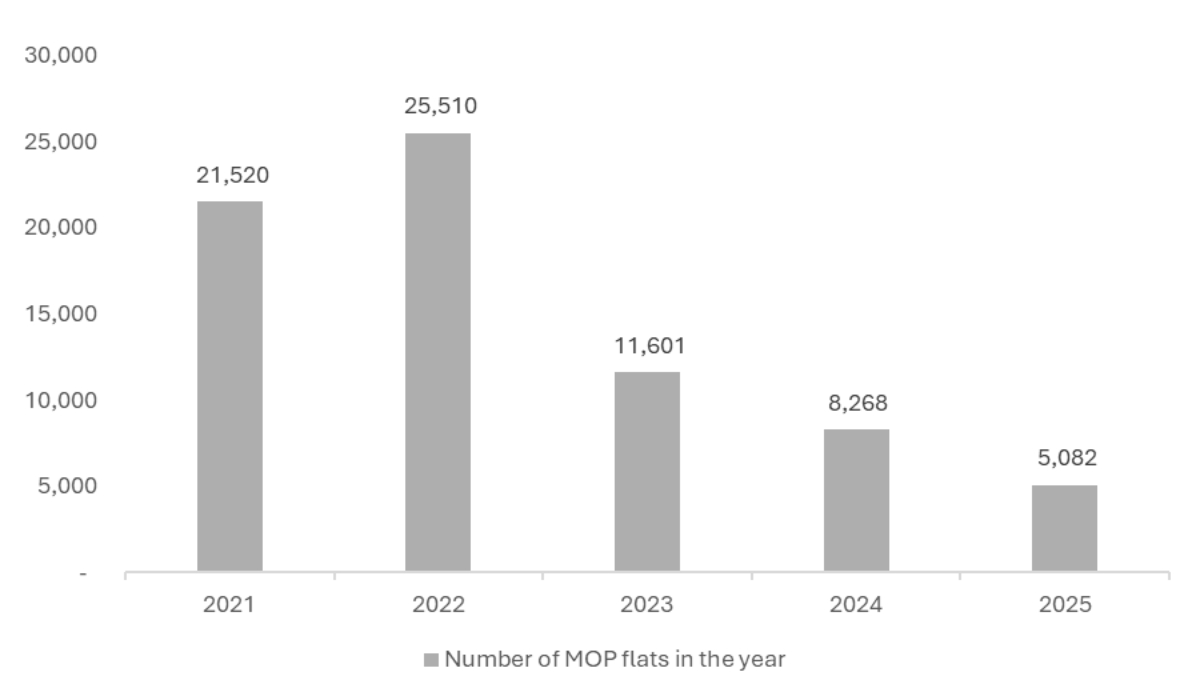

2025年满五年居住年限(MOP)的组屋数量减少

今年将有5082个组屋单位达到MOP,比去年减少38.5%,这将使转售市场的价格承压。

在市中心和成熟市镇,这一影响尤为明显。这些地区的新推出的预购组屋受新组屋政策限制,部分买家为此已转向转售市场。

图二:近五年MOP组屋数量

资料来源:建屋局、ERA研究和市场情报(数据截至今年3月27日)

这些买家不愿接受新政策中的转售限制,例如10年MOP、MOP后出租限制、转售时的津贴回扣以及转售组屋购买家庭收入上限等。

由于不受新政策影响的组屋供应减少,使其价格稳步上升,这可能会让预算较紧的买家望而却步。

同时,拥有这些组屋的屋主的持守能力较强,除非有优渥的报价,否则不太可能出售单位。

百万组屋交易量持续增长

首季,百万组屋交易数量从上一季度的285宗上升至295宗,环比增长3.5%;同比增长高达61.2%,当时则成交183宗。

在295宗交易中,约有271宗(占比78%)为四房式和五房式单位。与过去四个季度的平均水平相比增长了5%,显示这两类较大户型单位正在成为百万组屋市场的主要推动力。

图三:各类百万组屋单位的交易量

资料来源:建屋局、ERA研究和市场情报(数据截至今年3月27日)

2025年第一季度,百万组屋交易占所有交易的8.9%,几乎是2024年第四季的两倍,当时为4.6%。

这些组屋交易仍主要集中在成熟市镇,反映出买家对优质地段的持续强劲需求。

除了从私宅市场回流的买家外,越来越多现有组屋住户也愿意支付溢价,购买地段优越、设施完善的较新组屋,尤其是刚满五年MOP、位于中心区域的单位。这类单位不仅地理位置优越且交通便利,还邻近各类生活设施与热门学校,成为购屋者的理想选择。

随着今年MOP组屋数量的减少,市场对这类单位的需求将继续支撑其价格上扬。

资料来源:建屋局、ERA研究和市场情报(数据截至今年3月27日)

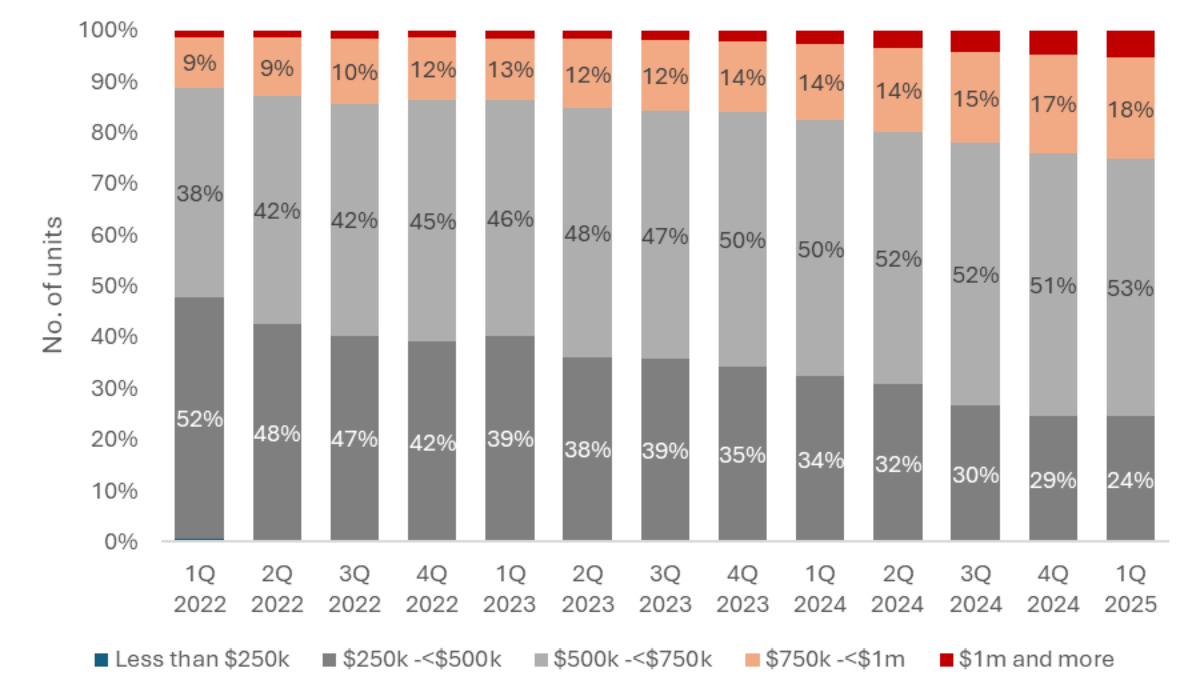

尽管高价交易有所增长,大多数转售组屋的价格仍维持在大众可负担的价格区间内。今年第一季,约有53%的转售交易价格介于50万至75万元之间,为大部分购屋者所能接受;另有24%的交易价格介于25万至50万元之间。

这意味着大约四分之三仍在合理、可负担的范围内,为首次购屋者与预算有限的家庭提供选择。

全年展望与预测

随着第一季预购组屋和剩余组屋单位配售结果公布,未成功购得单位的申请者预料将转向转售市场,推动2025年第二季度的交易活动回升。

不过,MOP组屋供应量的下降将减少转售市场的“优质货源”,也意味着全年交易量可能会趋缓,价格则维持温和增长。

预计今年全年组屋转售价格将增长3%至6%,交易量介于2万6000个至2万7000个单位。

本文中的信息仅供参考,不构成对信息的准确性、完整性或可靠性的保证。使用者应自行核实相关信息,并根据具体情况向独立的专业人士(如估价师、财务顾问、银行从业人员及律师)寻求专业意见。ERA及其销售人员对于因使用本信息而导致的任何直接或间接损失概不负责。此外,本文件受著作权法保护,ERA拥有其著作权。未经事先书面许可,任何个人或机构不得以任何形式或手段对本文件进行复制、传播或用于商业用途。

下文由ERA公关经理岳开新翻译

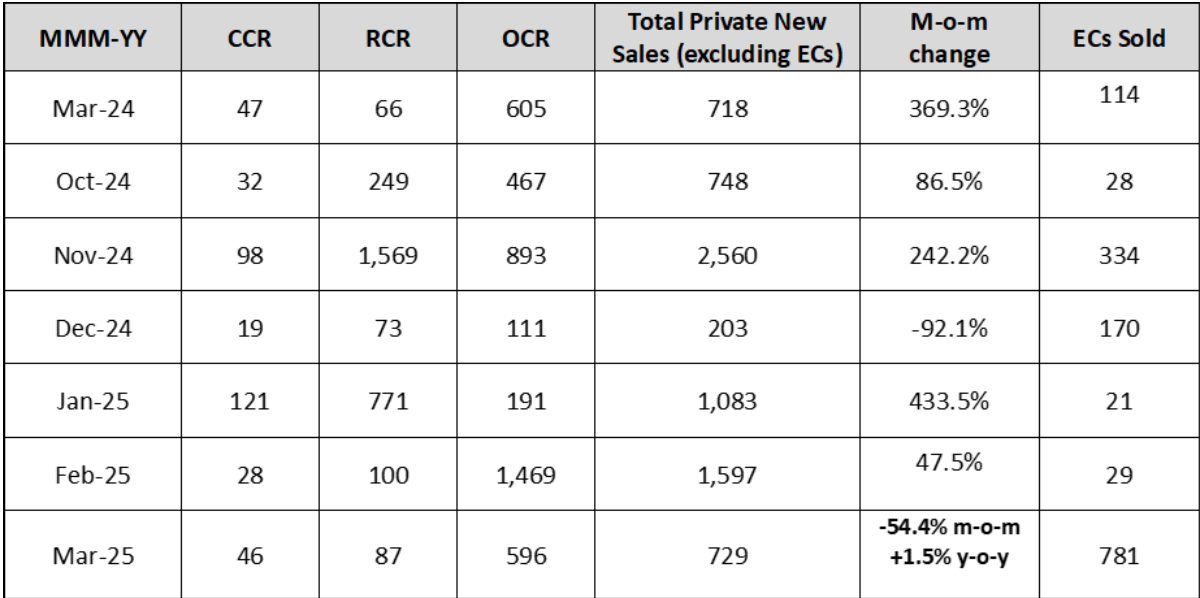

今年3月发展商共售出729个新私宅单位(不包括执行共管公寓,简称ECs ),环比下降54.4%,这主要因2月超高的新私宅销售基数。同时,小型项目的推迟也对3月销量下降产生影响。尽管如此,新私宅整体销量仍保持稳定。

本月共推出555个新私宅单位(不包括ECs),主要为一些中小型项目,如Lentor Central Residences(477个单位)和Aurea的首期(78个单位)。相比之下,2月则推出了近1700个单位,包括混合用途霸级项目PARKTOWN Residence(1193个单位)和逸泰·雅居(ELTA)(501个单位)。

2025年首度,新私宅销量达3409个单位(不包括ECs),发展商仅在前三个月就已超过去年总销量的一半,去年销量为6626个单位。

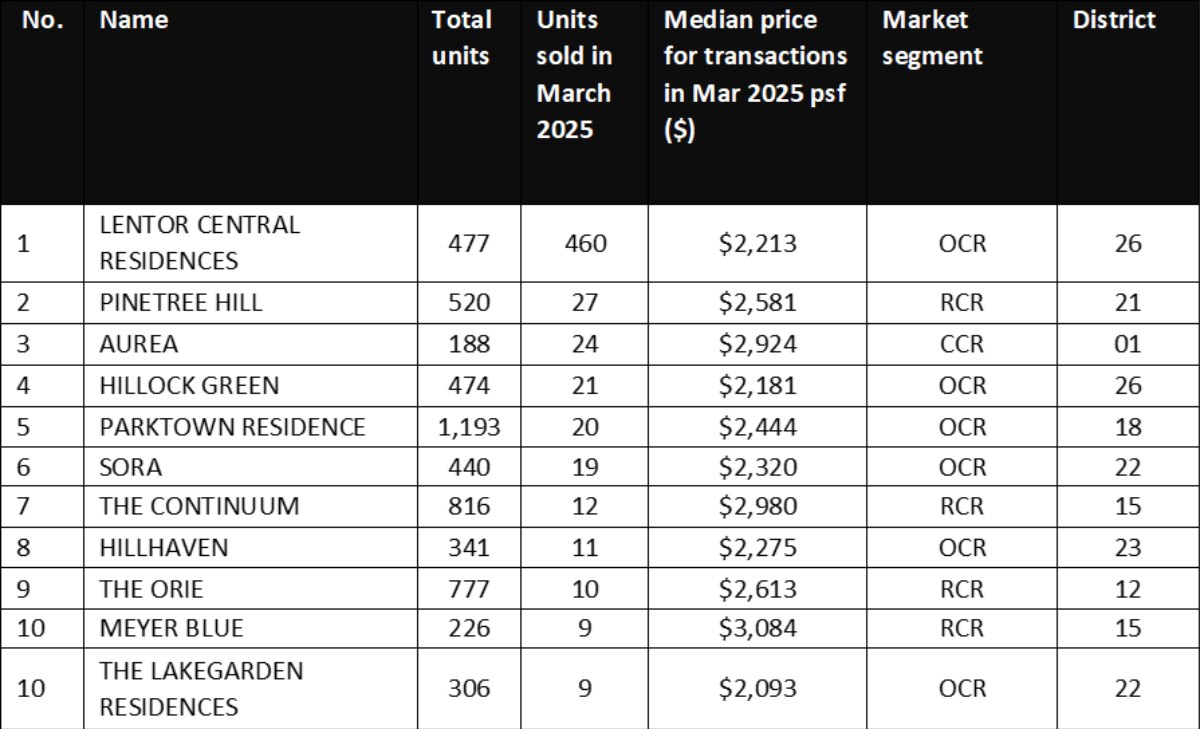

Lentor Central Residences(477个单位)是伦多山(Lentor Hills)私宅区的第六个项目,Aurea(188个单位)则是位于黄金坊(Golden Mile Complex)旧址的CCR项目,3月新私宅销售主要来自于这两个项目。其中,前者在3月售出其总单位数的96.4%或460个单位,后者则售出了已推出78个单位中的30.8%或24个单位。

表现最佳的新项目

.jpg)

尽管是伦多私宅区的第六个项目,Lentor Central Residences几乎售罄

尽管Lentor Central Residences是这个区的第六个私宅项目,但推出的首个周末就卖出96.2%的单位。项目强劲需求主要由于具有竞争力的定价及优越的地理位置。

此外,与近期其他位于OCR的新盘相比,Lentor Central Residences有性价比优势。2025年首度OCR新项目的中位尺价为2288元,而Lentor Central Residences 的中位数尺价则为2213元。

同时,项目的一卧房和三卧房单位已全部售罄,中位数价格分别为109万元和221万元,这在组屋升级者和“以小换大”购房者的预算区间。

伦多山私宅区的发展仍将继续,近期招标的伦多花园(Lentor Gardens)地段预计将是下一个受瞩目的项目。本月初,中国开发商鑫丰地产旗下的Kingsford Huray以最高标价标得,预计将于2026年中左右推出市场。

第七邮区唯一新盘Aurea表现不俗

位于黄金坊旧址的Aurea,在推出第一个周末售出30.8%的单位。发展商共推出78个单位,售出其中的24个,这得益于项目宽敞的户型设计及可俯瞰加冷盆地(Kallang Basin)与滨海湾的迷人景观。

考虑到Aurea的高端定位,3月的销售表现可圈可点。项目预计吸引投资者和年轻夫妇的兴趣,首周所售单位中,近一半(45.8%)为两房单位,共售出11个,两房单位中位数价格为190万元。

受首次购屋者(first-timer)青睐,晶莹轩(Aurelle of Tampines)推出即卖出89.7%的单位

在晶莹轩的带动下,3月EC销量环比大幅增长至781个单位。其中,晶莹轩推出的760个单位中,售出92.8%;项目所有四卧房和五卧房单位已售罄。多数买家为首次购屋者。

由于EC项目的价格比私宅低,依旧具有市场吸引力和性价比。此外,晶莹轩邻近淡滨尼北综合交通枢纽(Tampines North Integrated Transport Hub ),更吸引注重交通便利的买家,因此其强劲表现在预期之中。

接下来的EC项目包括年中推出位于登加区田园弄(Plantation Close)的Otto Place以及位于惹兰罗央勿刹(Jalan Loyang Besar)的项目。

买家背景

的买家概况.jpg)

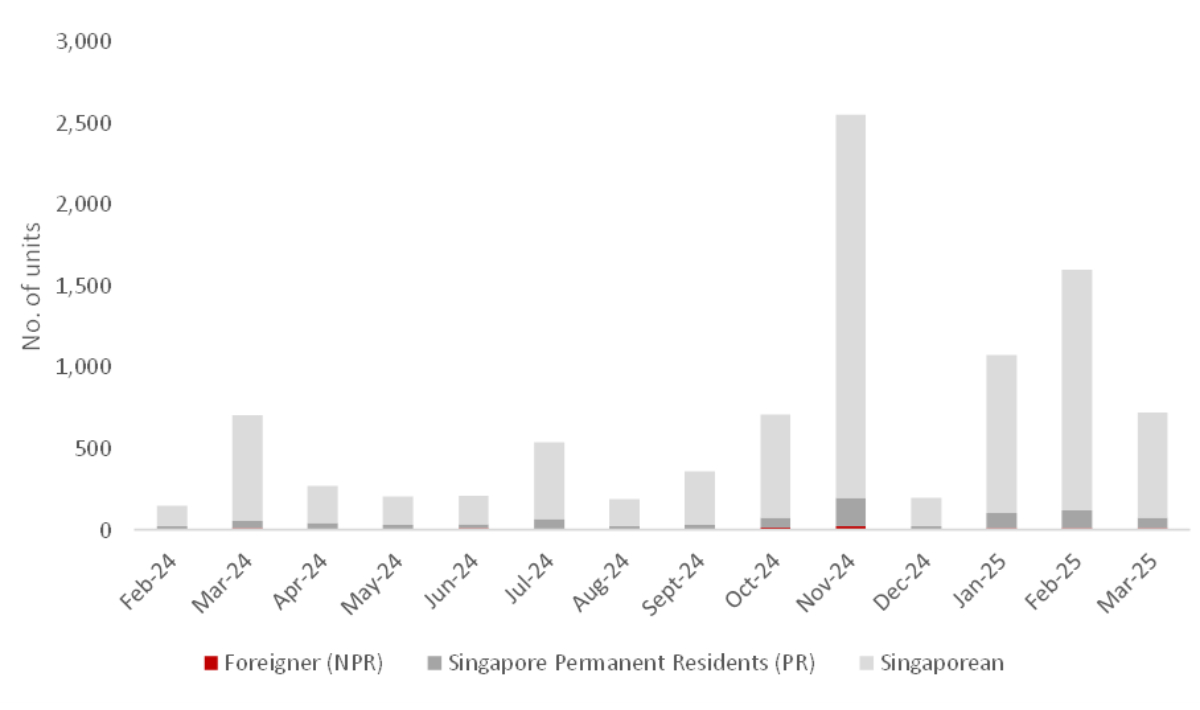

受额外买家印花税(ABSD)影响,外国买家的需求继续平平。3月,外国买家共完成了10笔交易,仅占本月总交易的1.4%。永久居民买家在当月完成了66笔交易(不包括EC),占9.2%。

新加坡人在仍是购买主力,共有645笔交易,占本月新私宅销售的89.5%(不包括EC)。

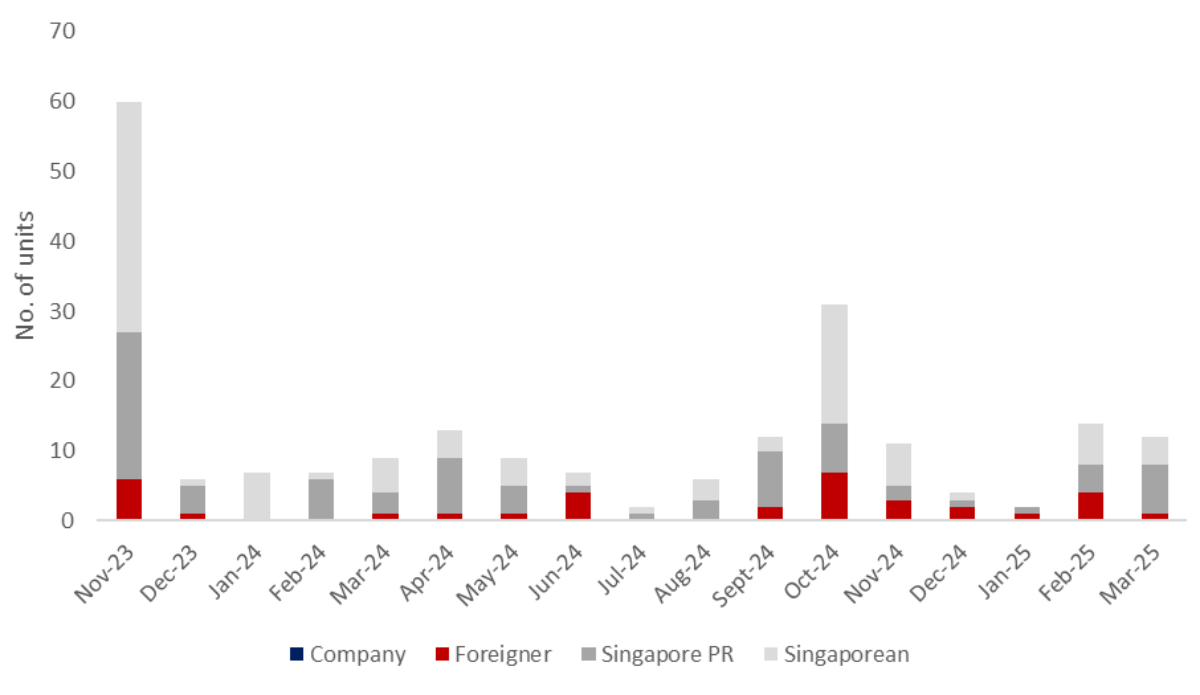

豪宅交易量下滑

豪华私宅交易下滑,共有12宗成交价在500万元及以上的交易。其中7宗交易来自新加坡永久居民,新加坡公民和外国买家分别占四宗和一宗。

成交价前三位的均由永久居民完成,分别为位于纽顿区32 Gilstead的永久地契单位(1300万元)、The Avenir(900万元)以及华登嘉苑(Watten House)(620万元)。这些大单位的面积至少1800平方英尺。

由于永久居民在新加坡购买有地住宅需要特别批准,这可能让他们转而选择类似的公寓单位。尽管需支付额外买方印花税(ABSD),但对于长期持有而言,大型永久地契住宅依然被视为保值良选,特别是为传承而购买。

最受欢迎的新豪宅项目是Aurea,项目共售出四个单位价格介于580万至610万元。它们都位于20层以上的四卧房单位,可欣赏加冷河与滨海湾的美景。对空间和景观有要求的买家,愿意为其支付溢价。

总结与展望

自4月初起,特朗普新一轮关税政策扰乱全球市场,导致市场情绪情绪,这可能让本地房地产市场承压。一些买家可能选择观望并延后购房计划。不过,估计这只是短期的情绪反应。

受益于本地买家的中长期房地产投资规划,购房更倾向于自住需求,而非投机。

展望下个月,随着位于RCR的滨海花园一号(One Marina Gardens)、Bloomsbury Residences和Arina East Residences等新项目陆续推出, 预计新私宅销售动能有望持续。

EC市场方面,由于4月没有新项目推出,而现有库存继续减少。晶莹轩开放后,会吸引大量第二次买家(second-timer)入场。

ERA预计今年全年新私宅销量将达到8500至9500个单位。

本文中的信息仅供参考,不构成对信息的准确性、完整性或可靠性的保证。使用者应自行核实相关信息,并根据具体情况向独立的专业人士(如估价师、财务顾问、银行从业人员及律师)寻求专业意见。ERA及其销售人员对于因使用本信息而导致的任何直接或间接损失概不负责。此外,本文件受著作权法保护,ERA拥有其著作权。未经事先书面许可,任何个人或机构不得以任何形式或手段对本文件进行复制、传播或用于商业用途。

In total, developer sales accounted for 729 new private homes (excluding ECs) sold in March. While this figure reflects a 54.4% month-on-month (m-o-m) decrease, this is mostly attributable to February’s exceptionally large base. Likewise, smaller development sizes also contributed to March’s lower, but healthy new home sales volume.

A total of 555 new private homes (excluding ECs) were launched, with smaller developments like Lentor Central Residences (477 units) and Aurea (78 units) making their debut. This is in contrast to February, which saw the launch of nearly 1,700 new homes launched at Parktown Residence (1,193 units) and Elta (501 units).

With 3,409 new private homes (excluding ECs) sold in 1Q 2025, developers have already achieved roughly half (nearly 51.4%) of their total sales volume for the entire preceding year (6,626 units in 2024) in just the first three months of 2025.

Table 1: New Home Sales Over the Last Six Months

Source: URA as of 15 April 2025, ERA Research and Market Intelligence

Lentor Central Residences (477 units), the sixth launch of Lentor Hills estate, and Aurea (188 units), a key Downtown Core project on the former Golden Mile Complex site, were the main contributors to March’s strong developer sales.

Respectively, Lentor Central Residences and Aurea sold 96.4% (460 units) and 30.8% (24 units of the 78 units launched) of their total units in March.

Best Performing New Launches

Table 2: Top ten performing new launch project (excluding ECs) in March

Source: URA as of 15 April 2025, ERA Research and Market Intelligence

Lentor Central Residences nearly sold out despite being Lentor Hills estate’s sixth new launch

Though Lentor Central Residences was the sixth new private development to debut in the area, it saw a 96.2% take-up rate on its launch weekend. Strong demand for the project largely stemmed from a combination of competitive pricing and appealing location attributes.

Additionally, Lentor Central Residences presented a competitive value proposition versus other recent OCR new launches. The median price of OCR new sales in 1Q 2025 was $2,288, while the median new sale price of Lentor Central Residences in March was $2,213 psf.

Moreover, Lentor Central Residences’ 1-bedroom and 3-bedroom units were sold out at a median quantum of $1.09M and $2.21M respectively. This positions them well within the sweet spot range for HDB upgraders and right-sizers.

The development of Lentor Hills estate is set to continue, with the recently tendered Lentor Gardens site set to be the next anticipated launch. On 3 April 2025, Chinese developer Kingsford Group put in the top bid for the site, with a potential launch around mid-2026.

Respectable showing by Aurea, first-and-only new launch in D7 for 2025

Aurea, located at the former Golden Mile Complex, achieved a respectable 30.8% take-up rate on its launch weekend. A total of 78 units were launched by developers, with 24 units sold, owning to their sizeable floor plates and captivating views of the Kallang Basin and Marina Bay.

Considering Aurea’s premium positioning, sales for March can be viewed as robust. Furthermore, the project is expected to resonate with investors and young couples; nearly half (45.8%) of Aurea’s launch weekend sales were two bedders, with 11 of such units sold at a median quantum of $1.9M.

Aurelle of Tampines Sold 89.7% at its initial booking, driven by first-timer buyers

March clocked a total of 781 new Executive Condo (EC) sales, a sharp increase from the previous month due to the launch of Aurelle of Tampines. Aurelle of Tampines sold 705 out of 760 units, this translates into a 92.8% take-up rate that also saw all of its four and five-bedroom units being sold out. The majority of the units were snapped up by first-timer buyers.

ECs continue to allure buyers with their lower price compared to new private homes by presenting a strong value proposition. Furthermore, Aurelle of Tampines’s location beside Tampines North Integrated Transport Hub appeals to buyers who prioritise connectivity and convenience. Thus, the strong launch weekend performance was expected. As of 8 April 2025, only 55 units remain unsold in this EC development.

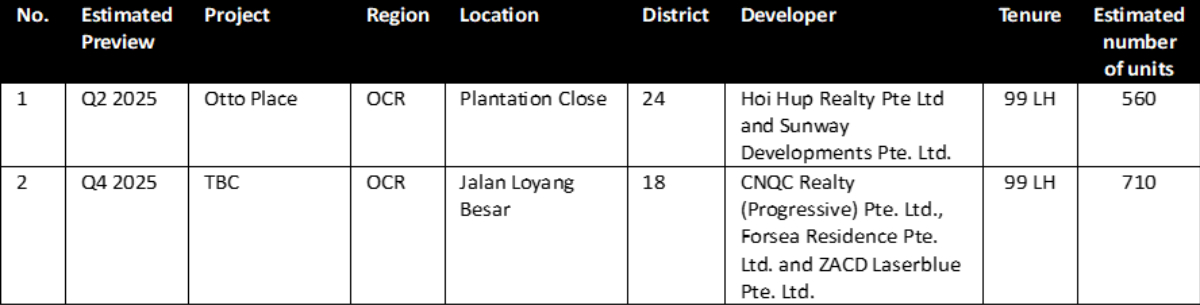

With Aurelle of Tampines’s quota for 2nd timers being lifted next month, we expect sales momentum to remain strong. However, with a lack of new EC launches, this momentum may be short lived. Upcoming EC launches include Otto Place (mid-2025) in Plantation Close and the Jalan Loyang Besar EC.

Buyer Profile

Chart 1: Buyer profile for all new non-landed homes excluding ECs

Source: URA as of 8 April 2025, ERA Research and Market Intelligence

With the punitive Additional Buyer’s Stamp Duty still in effect, foreigner demand for new private homes continued to stay flat. March 2025 saw a total of 10 transactions made by foreign buyers, making up just 1.4% of the month’s total deals. Meanwhile, Singapore Permanent Resident (SPR) buyers clocked 66 transactions in March, accounting for 9.2% of all new private home (excluding ECs) purchases in the month.

Lastly, Singaporeans continued to dominate the market in March, accounting for 645 transactions or 89.5% of total new private home sales (excluding ECs) for the month.

Luxury Homes Take a Dip in Transactions

Chart 2: Buyer profile for homes transacted at $5mil and more

Source: URA as of 8 April 2025, ERA Research and Market Intelligence

The luxury home market saw a drop-in transaction activity, with 12 new home transactions priced at $5 million and above. The majority of these transactions were made by SPRs, while four transactions were by Singaporeans, and one was by a foreigner.

The top three transactions by price were all made by Singapore Permanent Residents (SPRs), involving freehold units at 32 Gilstead ($13.0M), The Avenir ($9.0M), and Watten House ($6.2M). These units offer spacious layouts of at least 1,800 sqft.

Given that approval is required before they can purchase landed homes, SPRs are likely to gravitate towards condominium units with larger floor plates instead. Furthermore, while SPRs are subject to ABSD, a spacious freehold property is still considered a solid long-term asset, especially for those purchasing with legacy planning in mind.

The most popular new luxury development for March was Aurea, which moved four units priced between $5.8 million and $6.1 million. They were all high-floor 4-bedroom units (above 20 storeys) that had waterfront views towards Kallang River and Marina Bay. Buyers seeking larger units with scenic views are also willing to pay a premium for a home that appeals to their liking.

Closing Thoughts and Forecast

Since early April, Trump’s new tariffs have roiled global markets and triggered volatility, resulting in dampened sentiments that could weigh on local real estate. As a result, some property buyers may opt to wait out any potential turbulence and delay their purchases. However, this is expected to be a knee-jerk effect.

Singapore’s property sector benefits from domestic buyers’ mid- to long-term outlook. This ensures that local real estate activity remains rooted in genuine buyer needs, rather than speculative activity.

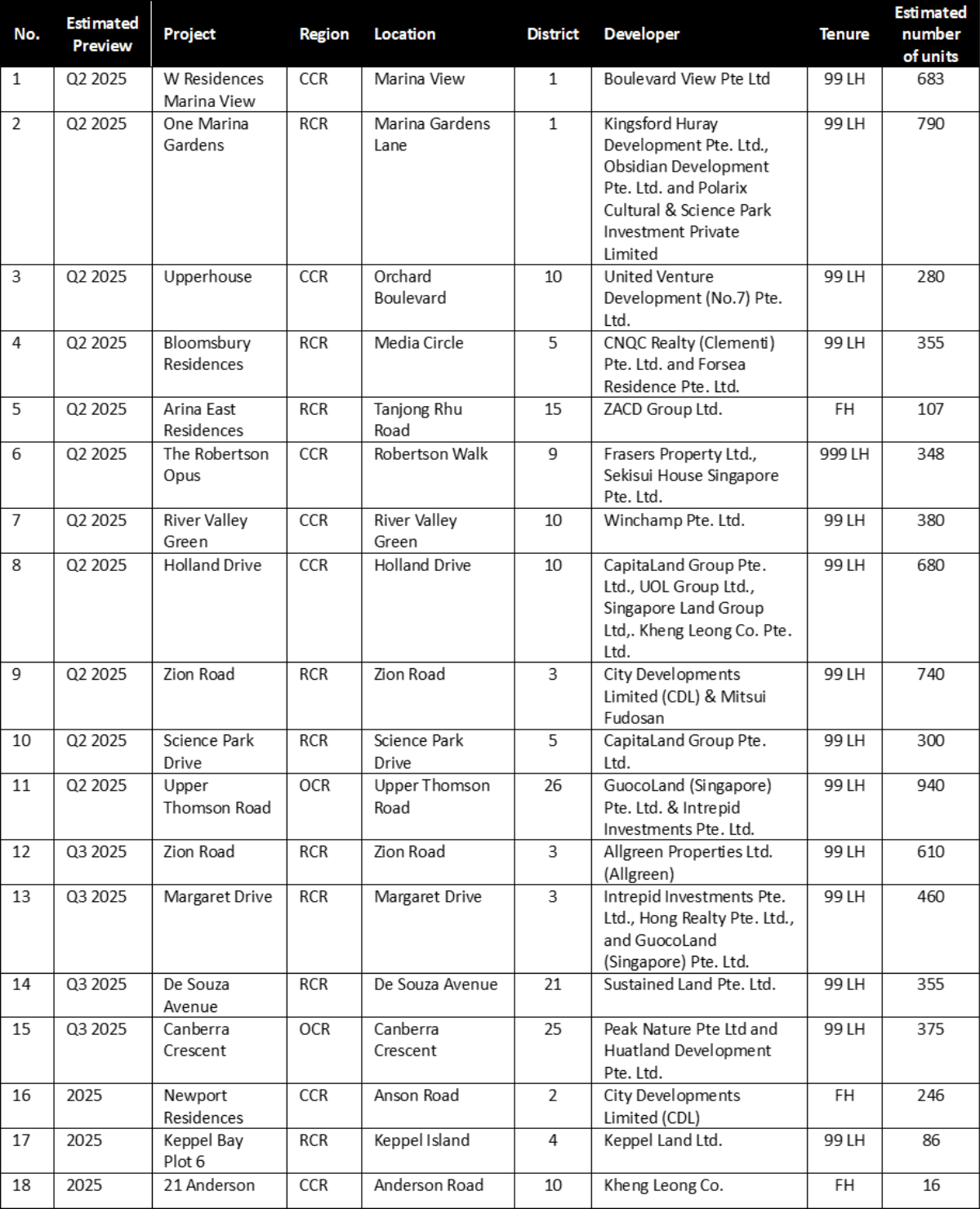

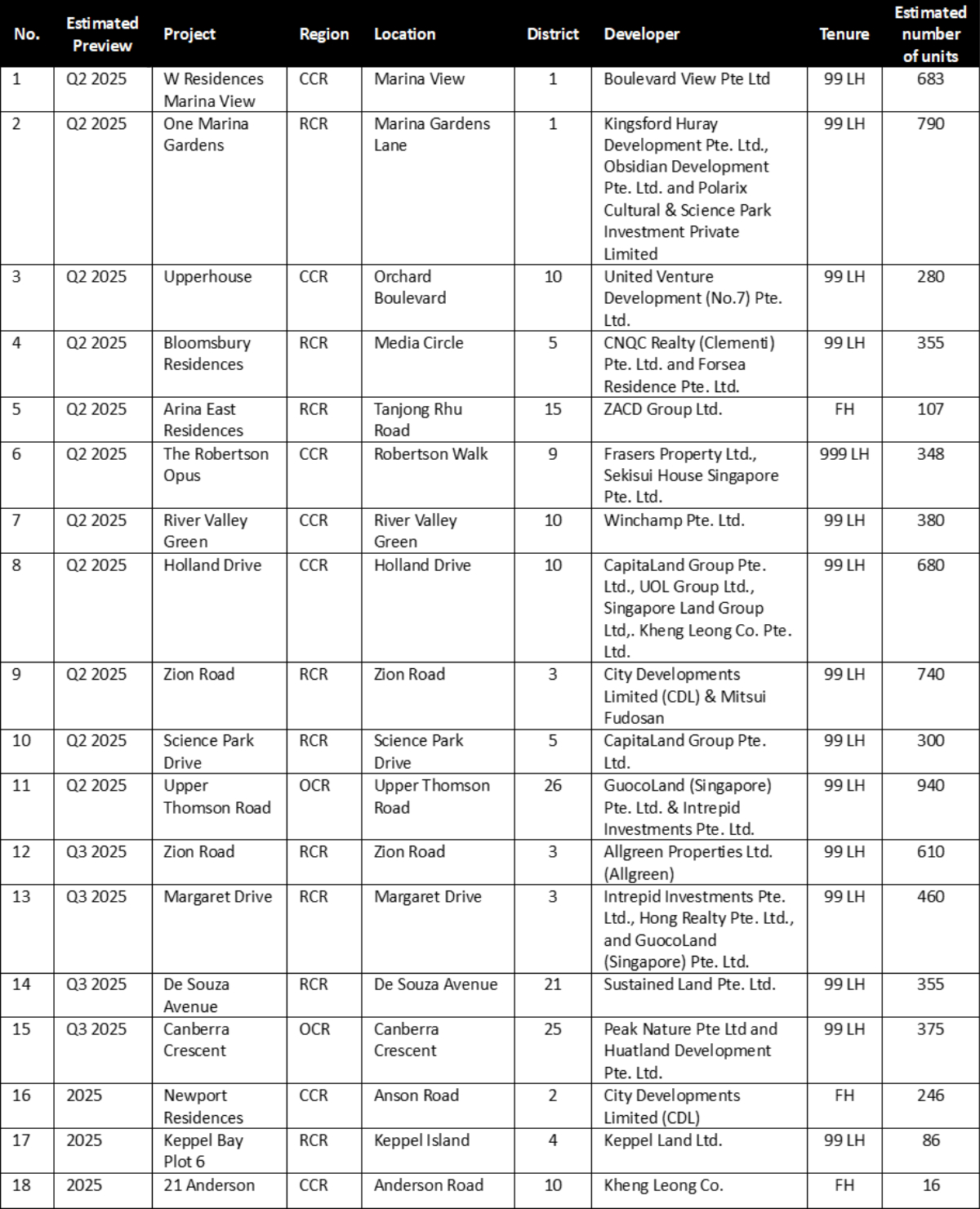

Come next month, we can expect to see continued sales momentum in the new home market, with the launches of One Marina Gardens (CCR), as well as Bloomsbury Residences and Arina East Residences (both RCR).

ECs, on the other hand, will see new home stocks continuing to deplete with a lack of new launches in April. Second-timers are also expected to snap up remaining units at Aurelle of Tampines once booking commences. Building on the ongoing momentum in new home sales, ERA Singapore projects 8,500 to 9,500 new homes to be sold for the entirety of 2025.

Table 3: Upcoming launches in 2025

Executive Condominium

Source: ERA Project Marketing

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.

This article was written in conjunction with Eugene Lim, Key Executive Officer and Wong Shanting, Head of Research and Market Intelligence of ERA Singapore

The article first appeared in The Business Times BT Property Week section on 9 April 2025.

In recent years, the practice of clustering new home launches within the same neighbourhoods has been growing in prominence. For instance, Tengah and Lentor Hills Estate have seen a staggered rollout of fresh private housing projects, in line with URA’s broader master plan for precinct renewal or development.

Similarly, in the months ahead, we can expect to see similar residential clusters taking shape at Zion Road, River Valley and one north.

Though no formally-adopted term for this trend exists, parallels can be drawn with the concept of “agglomeration” in which businesses cluster to yield synergistic benefits.

From an urban planning perspective, concentrating new home launches in the same neighbourhoods could enhance planning efficiency, resulting in more effective resource allocation when developing new precincts.

This benefit is crucial, as investing in infrastructure for new precincts is a significant undertaking that should not be taken lightly. By strategically clustering new homes in the same area, the Government can ensure that any infrastructure investments are focused on meeting the needs of a larger community.

The clustering of new home launches is nothing new

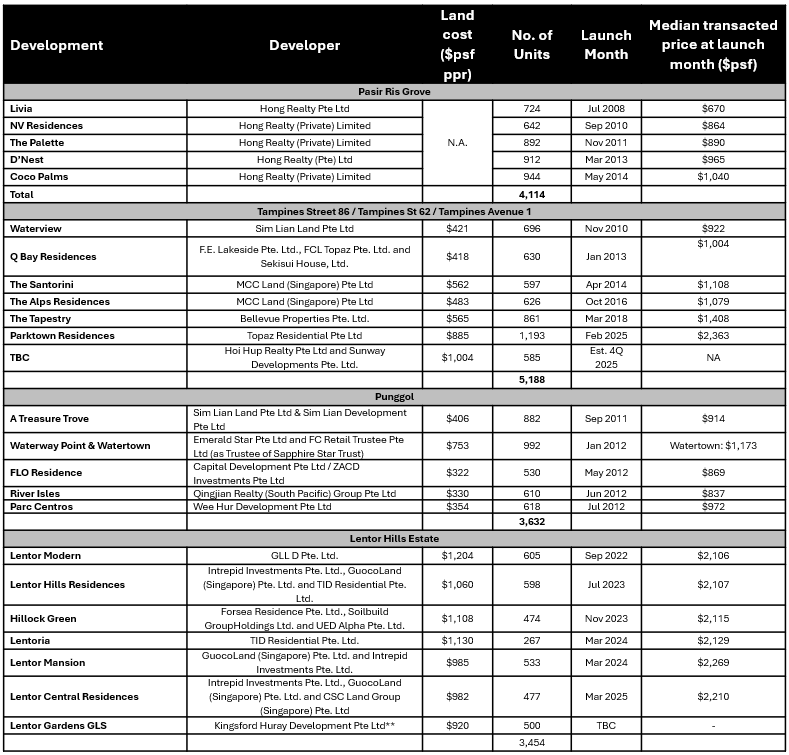

The concept of clustering new home launches is not a new one, having been previously observed in areas such as Pasir Ris, Punggol, Sengkang, and Tampines. In a way, this could be the fastest and most efficient way to developing a new township, whether as an independent entity or as an extension to an existing town.

Between 2008 and 2014, Pasir Ris Grove saw five new homes launches bringing over 4,100 new homes in the vicinity. All five projects were also collectively developed by Hong Realty Pte Ltd. Likewise, between 2010 and 2017, five residential sites along Tampines Street 86 / Tampines Avenue 1 were awarded under the Government Land Sales (GLS) Programme to different developers. Altogether, these five sites yielded some 3,400 units. More recently, five sites, yielding approximately 3,600 units, were sold to drive the development of the Punggol New Town.

This is particularly pronounced in the Lentor Hills Estate cluster, which has seen six launches to date, with another site expected to launch in 2026. Despite initial concerns about a potential supply glut with each successive launch, such fears were allayed as demand for new homes remained robust, evident by healthy take-up rates and rising home prices. GuocoLand, in particular, is the developer behind four of the Lentor Hills Estate developments, allowing them to be bold and experiment with various concepts tailored to meet the diverse needs of homebuyers.

Table 1: Launches in new housing clusters

Source: URA, ERApro, ERA Research and Market Intelligence

*Based on caveats

**Subject to site being awarded

While the clustering of homes is often seen as a strategic move for developers and the government, it also brings about tangible benefits for buyers. Let us explain further below.

1. Buyers get to explore all various projects and make well-informed decisions

One significant benefit is that buyers can ‘shop’ at all the projects almost simultaneously.

This allows them to make an informed decision before committing to their home purchase. By being able to view multiple projects simultaneously, buyers can compare features, layouts and prices more effectively. This transparency and ease of comparison can lead to better decision-making.

Additionally, it reduces the pressure of having to make quick decisions based on limited information, as buyers have a comprehensive view of the new homes launched in the vicinity.

2. New amenities and rejuvenation to support the growing community

The clustering of new homes often acts as a catalyst for urban rejuvenation, prompting the government to introduce new amenities and infrastructure to meet the needs of incoming residents.

For example, the Our Tampines Hub was opened in 2017 to serve the residents of Tampines. In a more recent example, Our Residents’ Hub @ Lentor Estate was opened in end-2024, ahead of the influx of future dwellers.

Another notable example is Pasir Ris, where a new sports and hawker centre was added in the 2010s, alongside the announcement of the new Cross-Island Line with an interchange at Pasir Ris.

Looking ahead, upcoming precincts like Tengah are also expected to benefit from new initiatives and infrastructure developments.

3. Sustained price growth through the clustering of new home launches

In most cases, the clustering of new home launches results in new home prices trending higher with each subsequent launch. This pattern is reinforced by developers pricing latter launches higher due to rising land and construction costs.

Moreover, as the estate matures with the addition of more amenities and robust transportation networks, this leads to prices being pushed further upwards. This dynamic demonstrates the first-mover advantage, whereby early buyers secure lower prices than those who purchase later.

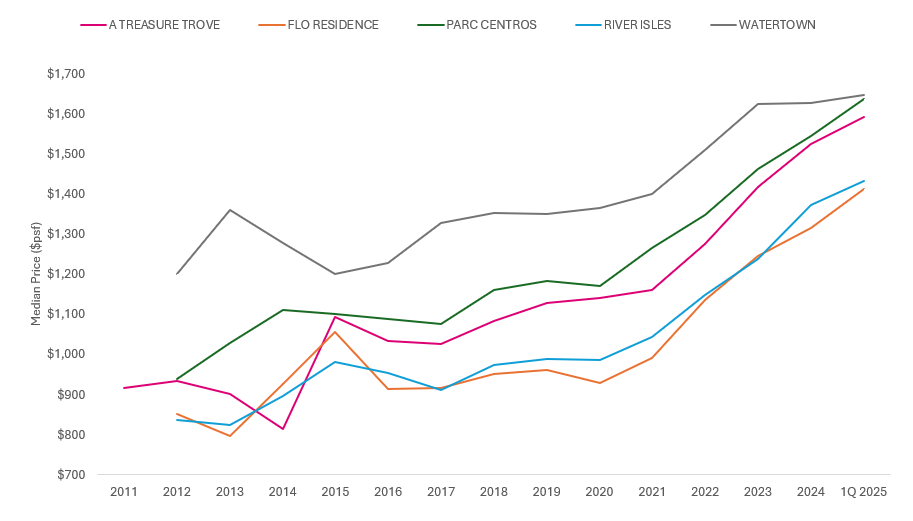

Chart 1: Median Price psf condos at Punggol

Source: URA, ERA Research and Market Intelligence

*For periods without transactions, we estimated prices using the average of the preceding and following transaction prices.

Since their respective debuts, condominiums in the Punggol have delivered a compound annualised returns of between 2.5% and 4.4%, based on median transacted price per square foot ($psf). Even though there are some price differences across the projects, their price trends have generally moved in parallel, reflecting a broadly similar pace of appreciation over time. This observation brings us to our next point.

4. A similar price entry point minimises the risk of losses and supports price growth

With new homes launched at comparable price points, it reduces the likelihood of any owner selling at a loss. This pricing alignment can help maintain market confidence and support steady price appreciation across the precinct.

5. Competition could drive developers to enhance their product offerings

Having successive launches also means more and better options for buyers. With similar locational attributes, developers will compete to offer compelling and unique projects that stand out in the market.

These projects are also often better positioned with higher-quality finishes, a more diverse mix of unit sizes and layouts, and innovative designs aimed at different homebuyer segments.

In an environment where intense competition for the same pool of buyers and price sensitivity both exist, developers will strive to outdo each other. Hence, regardless of whether there are multiple developers or just one developing a few sites within a precinct, homebuyers will be the ultimate beneficiaries of this heightened competition.

This is evident in Lentor Hills Estate, which saw six launches over a 30-month period. In particular, Guocoland has developed four of the six sites awarded in the Lentor Hills Estate. With each launch, Guocoland was able to better anticipate the needs of its buyers. From unit layouts to unit sizes, each development was thoughtfully tailored to suit the needs of different buyers.

Over the past 30 months, we have seen diverse unit configurations. Lentor Modern, launched in September 2022, offers flexible spaces with adaptable layouts designed to meet the post-pandemic needs of families for larger living spaces or dedicated workspaces. Lentor Hills Residences featured dual-key units for investors seeking rental income. Hillock Green and Lentoria focused on larger, more efficient floor plans with squarish layouts and combined living and dining areas ideal for hosting.

6. A large precinct can support an easy exit strategy

With a sizable number of homes in the precinct, homeowners can expect consistent market activity, making it easier to sell their homes when the time comes. This reduces the risk of not being able to find a buyer in the future and helps sustain property values in the long term. Furthermore, a well-planned precinct with amenities and strong transport connectivity tends to attract a continuous influx of potential buyers, which is advantageous for the resale process.

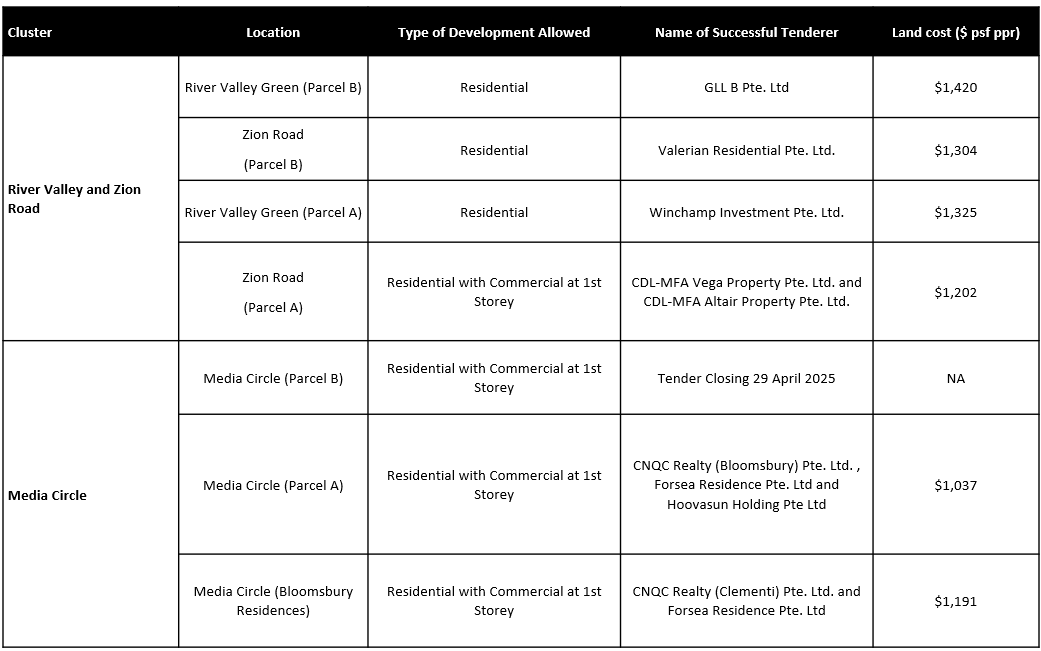

Looking ahead, the next “agglomeration” of new home clusters is expected to take place in the River Valley, Zion Road, and Media Circle precincts. These includes four sites at River Valley and Zion Road cluster as well as three sites at Media Circle.

Table 2: List of Upcoming Clusters

Source: URA, ERA Research and Market Intelligence

Conclusion

In closing, while some buyers may be hesitant about locales with multiple new launches, clear advantages do exist. The ability to view and compare several home launches simultaneously empowers buyers to make well-informed decisions.

Separately, one can also expect new amenities alongside enhanced connectivity that could contribute to long-term price growth. As these precincts mature, the steady influx of homebuyers provides a viable exit strategy, should owners need to sell their homes for any reason.

Looking ahead, the next “agglomeration” of new home clusters is expected to take place in the River Valley, Zion Road, and Media Circle precincts. Could one of new projects be where you call home next?

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.

下文由ERA公关经理岳开新翻译

数据基于市区重建局(URA)于2025年4月1日发布的季度预估统计。

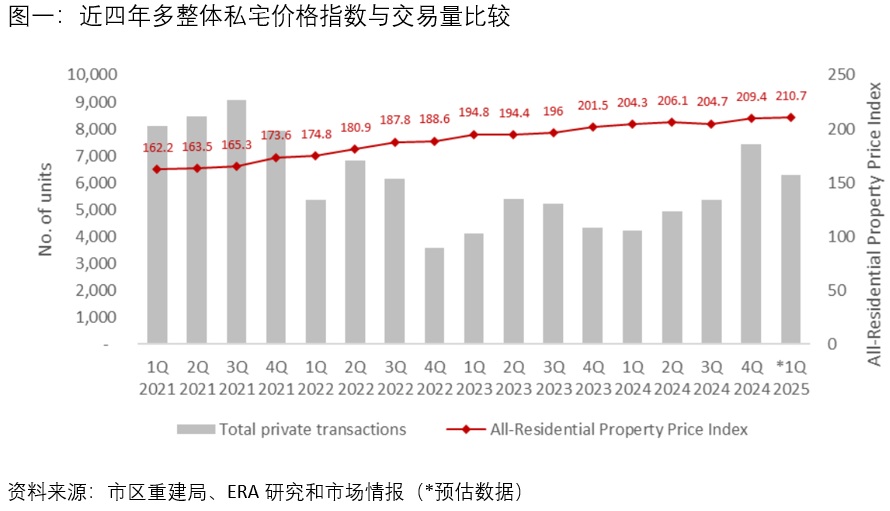

2025年第一季整体私宅价格指数环比上涨0.6%,涨幅温和;而私宅交易量则环比下滑了15.3%。

经济利好推动购房回暖

受益于多项经济利好指标及利率走势稳定,买家重返新私宅市场,带动整体市场活跃度上升。

整体来看,新加坡去年的经济表现优于预期。根据贸工部数据,2024年新加坡经济增长达4.4%,远高于2023年1.8%的增幅。不过,持续加剧的贸易紧张局势,让市场仍持审慎乐观态度。

新加坡房地产市场仍主要由本地需求支撑。稳定的就业环境、收入增长以及低失业率,使得更多国人有能力负担私宅。此外,政府组屋转售价格的上涨,也持续推动国人产业升级。

此外,继美国联邦储备局(FED)于去年9月、11月及12月连续三次降息后,利率在去年下半年开始趋缓。美联储的目标利率区间因此下调至4.25%至4.50%,借贷成本降低也提升了消费者信心。

本地方面,核心通胀率也有所缓解,去年平均为2.7%,大幅低于前年的4.2%。

尽管当前经济环境让市场回暖,但在地缘政治不确定因素影响下,部分买家仍可能保持审慎乐观态度。新加坡作为亚太地区的重要枢纽,即便全球贸易紧张局势升级,或面临经济放缓的风险,其战略地理位置和中立立场有望继续吸引海外投资者关注。

整体私宅价格与交易情况

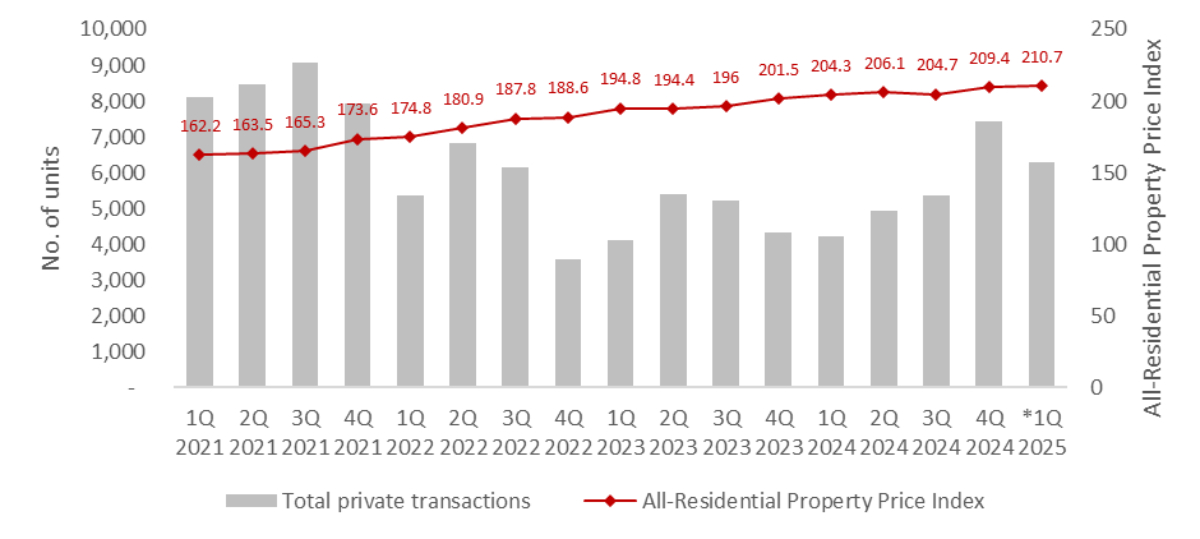

根据市建局发布的第一季最新预估数据,整体私宅价格在本季度呈温和上升趋势,这主要因年初新私宅销售强劲。整体私宅价格指数环比上涨0.6%,延续了去年第四季环比涨幅2.3%的上行势头。

不过,受转售市场交易量减少的影响,整体宅交易量有所下滑。截至3月中旬,今年第一季私宅总交易量为6299个单位,较去年第四季的7433个单位减少了15.3%。

各地区中,根据数据显示,其他中央区(RCR)的非有地私宅价格指数涨幅最为显著,环比增长1.0%。核心中央区(CCR)和中央区以外(OCR)的非有地私宅价格指数则分别环比上扬0.6%和0.3%。价格上涨主要由近期各地区更高的新私宅价格带动。

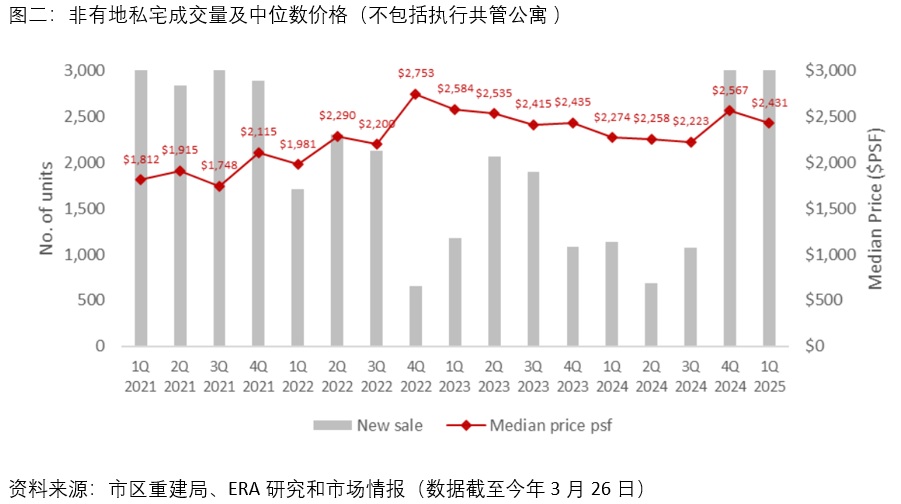

非有地新私宅销售(不包括执行共管公寓)情况

今年第一季,私宅市场延续了前一季度的良好势头,销售依旧强劲。根据截至3月26日的买卖禁令(caveats),本季度新私宅成交量为3268个单位,环比小幅下滑3.1%,这主要是由于去年第四季基数较高。

尽管略有回落,但第一季的新私宅销量依然高于2021年第四季至2024年第三季的新私宅季度销量。这主要得益于若干“明星项目” 推出,这些项目位于长期缺乏非有地新私宅供应的区域,或是位于设施完善、交通便利的成熟市镇。

其中,今年1月推出的艺景峰(The Orie),是大巴窑自2015年以来的首个新盘。开盘首个周末便售出668个单位(占总单数的75%)的亮眼销售成绩。项目的成交中位数尺价达到每平方英尺2704元,创下RCR的价格新基准。

2月在淡滨尼推出了综合型霸级项目Parktown Residences,共计1193个单位,开盘第一个周末热卖1041个单位(占总单数的87%)。同时开盘的位于金文泰1道(Clementi Ave 1)的新项目逸泰·雅居(ELTA),也在首个周末售出501个单位中的326个(占总单数的65%)。

上月开盘的99年地契伦多新私宅Lentor Central Residences亦表现不俗。尽管是这个区域的第六个新项目,但购买热情依然高涨,开盘即售出445个单位(占总单数的93%)。

近期新私宅的热销也带动了之前已开盘的新项目。未能购得心仪单位的买家开始转向价格相近的项目,其中,松岩轩(Pinetree Hill)、Hillock Green及水岸华庭(SORA)的销量均有所增加。此外,位于市中心为数不多的现有新盘之一的 柏南华庭(One Bernam),也在本季度全部售罄。

执行共管公寓(EC)

今年首季仅有一个EC项目晶莹轩(Aurelle of Tampines)在3月推出,开盘当天即售出760个单位中的九成,平均成交价格为每平方英尺1766元。根据买卖禁令,发展商在今年首季共售出817个EC单位,环比增长54.7%。值得注意的是,晶莹轩距离综合型开发项目Parktown Residences仅约200米,为买家提供了另一种选择。

目前,市场新EC库存有限。截至3月26日,全岛范围内仅剩不到130个可售单位,分布在五个项目之中。虽然今年仍有两个EC项目计划推出,分别是位于登加区田园弄(Plantation Close)项目Otto Place以及位于惹兰罗央勿刹(Jalan Loyang Besar)的项目,但这些供应或许仍难以满足市场需求。

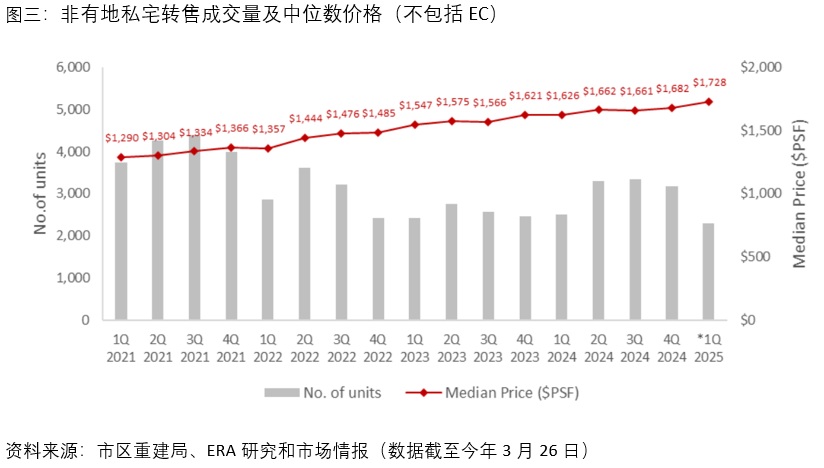

非有地私宅转售与楼花转售(Subsale)(不包括 EC)

根据截至3月26日的市建局买卖禁令,今年第一季度,转售交易占所有非有地私宅销量(不包括EC)的39.8%,首季共成交2294个单位。相比去年第四季3173个单位的成交量,本季度环比下降了27.7%。而上一季度转售交易较去年第三季也环比下降了4.9%。

连续两季交易量下滑,可能因新私宅的热卖,以及私宅竣工数量的减少。根据市建局全年预估数据,2025年私宅(不包括EC)的竣工数为5846个单位,显著低于2024年的8460个单位。

从另一方面看,新竣工私宅供应的相对稀缺可能会推高转售私宅的价格。因此,转售价格出现上升,这与今年首季度中位数单位价格环比上涨2.7%相吻合。

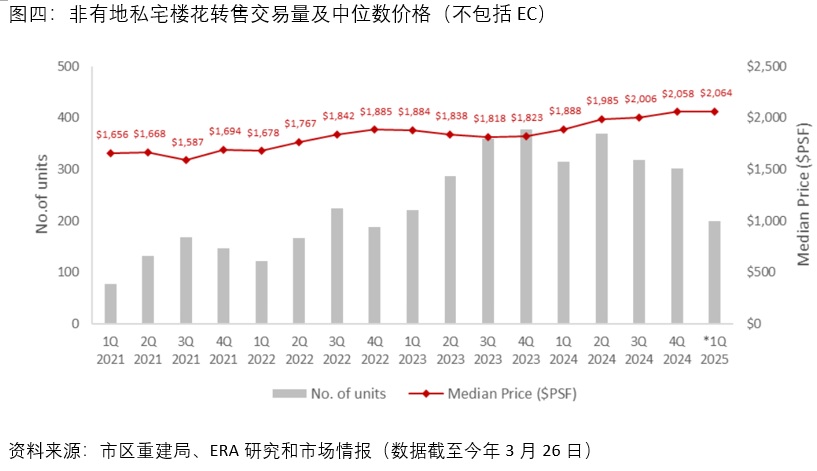

楼花转售交易本季度占所有非有地私宅销售(不包括 EC)的3.5%,根据买卖禁令数据,共有199个交易。较去年第四季的302个环比下降34.1%。

楼花转售的中位数尺价则小幅上涨0.4%,达每平方英尺2064元。

上述原因可能也因受新私宅热销以及转售供应减少的影响。

市场展望

接下来,预计将有多个位于CCR及RCR的项目推出,包括滨海花园一号(One Marina Gardens)、Bloomsbury Residences以及位于乌节林荫道(Orchard Boulevard)的Upperhouse。滨海花园一号和Bloomsbury Residences 将吸引那些具备长远眼光并看好市区规划潜力的买家或投资者。而Upperhouse 则因地理优势和临近乌节林荫地铁站,主打高净值买家。

这些买家通常在评估投资机会时更为谨慎,购买过程需时间考虑。因此这些项目的销售可能会较平缓。

由于近期新私宅热卖,ERA 已将全年新私宅销量由之前的7000至8000个单位,上调至8500至9500个单位。同时,预计到2025年底,楼花及转售交易量将分别达到1100至1300个单位以及1万4000至1万5000个单位。

本文中的信息仅供参考,不构成对信息的准确性、完整性或可靠性的保证。使用者应自行核实相关信息,并根据具体情况向独立的专业人士(如估价师、财务顾问、银行从业人员及律师)寻求专业意见。ERA及其销售人员对于因使用本信息而导致的任何直接或间接损失概不负责。此外,本文件受著作权法保护,ERA拥有其著作权。未经事先书面许可,任何个人或机构不得以任何形式或手段对本文件进行复制、传播或用于商业用途。

Figures are based off the official flash estimates for URA quarterly statistics, released on 1 April 2025.

SINGAPORE, 01 April 2025 – As reflected in the latest flash estimates released by URA, the All-Residential Property Price Index exhibited a modest increase of 0.6% quarter-on-quarter (q-o-q) in 1Q 2025, while the total transaction volume of private homes inched down 15.3% over the same timeframe.

Favourable Economic Conditions Fuel Homebuying Activity

Recent months have seen the return of homebuyers to the new launch market, supported by favourable economic conditions, as reflected across various indicators and moderated interest rates.

On the whole, Singapore put up a better-than-expected financial showing last year. According to the Ministry of Trade and Industry, the national economy expanded by 4.4% in 2024, more than double of the 1.8% growth recorded for 2023. That said, while the market remains cautiously optimistic on growth prospects amid the escalating trade tension.

Singapore’s property market remains propped up by domestic demand. Good jobs, rising income and low unemployment rates have made private homes more accessible for Singaporeans. Moreover, the rising HDB resale prices will continue to help pave the way for Singaporeans to upgrade to private homes.

Moreover, interest rates had also begun tapering in the latter half of 2024, following a trio of rate cuts by the U.S. Federal Reserve (Fed) during September, November and December. This brought the Fed’s target interest rate range down to 4.25% to 4.50%, lowering borrowing costs and raising consumer optimism. Locally, core inflation rates also eased to an average of 2.7% last year, down from 4.2% in 2023.

While market conditions are encouraging and favourable for home buyers, some buyers may remain cautiously optimistic amid geopolitical headwinds. Singapore’s position as a key Asia-Pacific hub could prove advantageous, as its neutrality and strategic location may continue to attract interest even amid escalating trade tensions and the risk of a global economic slowdown.

All-Residential Private Home Prices and Transactions

As reflected in the latest flash estimate figures released by URA for 1Q 2025, overall private home prices rose moderately on the quarter, pushed further upwards by the solid performances of new launches debuting in the opening months of the year. In relation, the All-Residential Property Price Index was observed to have risen moderately by 0.6% quarter-on-quarter (q-o-q), carrying forward the upwards momentum demonstrated in 4Q 2024 when it rose 2.3% q-o-q.

However, despite the strong start to the year observed in the new sale market, overall transaction numbers of private homes exhibited a decline, dragged down by a downtick in the number of secondary market transactions. In 1Q 2025, the total transaction volume of private homes (up to mid-March) was 6,299 units, which is 15.3% less than the 7,433 units sold in 4Q 2024.

Chart 1: All-Residential Property Price Index and Total Private Transaction Volume

Source: URA, ERA Research and Market Intelligence (*Based on flash estimates.)

Also, according to flash estimates released by the Urban Redevelopment Authority (URA), the non-landed RCR property index showed the most pronounced growth among regional sub-markets, with a moderate yet notable 1.0% q-o-q increase.

Similarly, the non-landed CCR and OCR property price index saw 0.6% and 0.3% q-o-q growth. These increases were largely driven by higher price benchmarks achieved at recent new home launches across all market segments.

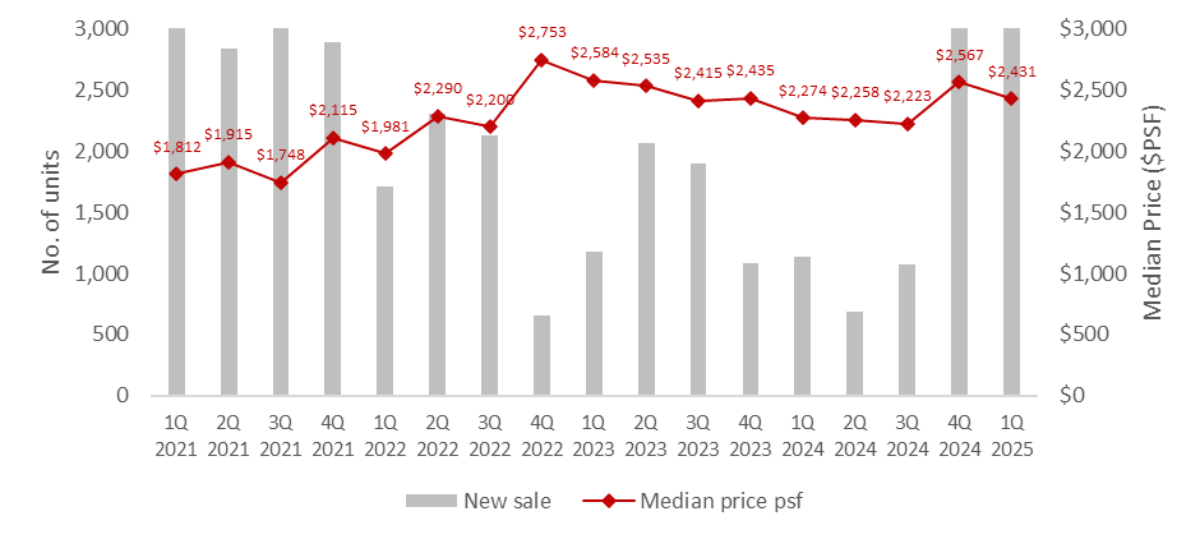

New Sale (Non-Landed Homes, Excluding ECs)

The private residential market maintained its upward momentum in 1Q 2025, with primary sales continuing their strong performance from the previous quarter. According to caveats as of 26 March 2025, new sale transactions in 1Q 2025 dipped 3.1% quarter-on-quarter (q-o-q) to 3,268 units per URA caveats (reflecting a higher base in 4Q 2024). 1Q 2025’s sales volume remained above all quarterly new home sales recorded between 4Q 2021 and 3Q 2024. This resilience was driven by several blockbuster launches taking place in either underserved locations lacking in new non-landed private residential supply or in established towns with strong amenities and transport links.

In January 2025, The Orie, the first launch in Toa Payoh since 2015, was launched and achieved outstanding performance. During its launch weekend, it moved 668 units (75%) at a median price of $2,704 psf, setting a new benchmark for the RCR.

February saw the launch of Parktown Residences, an integrated mega-development of over 1,193 units at Tampines, and ELTA, a 501-unit project at Clementi Ave 1. They sold 1,041 (87%) and 326 units (65%) during their launch weekend respectively.

Lentor Central Residences, in the new Lentor Hills cluster, is another popular up-and-coming housing estate. Despite being the sixth launch, its performance was still stellar. 445 units (93%) was snapped up at launch.

Stellar sales performance and buzz from the newly launched projects have also created interest in existing projects. Buyers who were unsuccessful in getting their desired unit may look towards other similar-priced projects. Thus, Pinetree Hill, Hillock Green and SORA also saw an uplift in units sold. One Bernam, one of the few existing launches located in the Downtown Core, was fully sold this quarter.

Chart 2: New Sale Transactions and Median Price for Non-Landed Homes (excluding ECs)

Source: URA as of 26 Mar 2025, ERA Research and Market Intelligence

Table 1: Top 10 Best-Selling Projects in 1Q 2025

Source: URA, ERAPro as of 26 Mar 2025, ERA Research and Market Intelligence

Executive Condominium

1Q 2025 saw a single EC launch with Aurelle of Tampines’s debut in March 2025 – the project saw 90% of its 760 units sold at an average price of $1,766 psf on launch day. According to caveat data, this resulted in a 54.7% q-o-q increase in EC sales by developers who sold 817 units in total over 1Q 2025. Notably, Aurelle of Tampines is also just 200m away from Parktown Residences, offering buyers an alternative option.

Following Aurelle of Tampines’s strong performance, the current supply of new EC homes is fairly limited. As of 26 March 2025, there are fewer than 130 units available across five projects island wide. Though there are another two projects at Plantation Close (Otto Place) and Jalan Loyang Besar slated to be launched this year, this incoming supply might still fall short of demand.

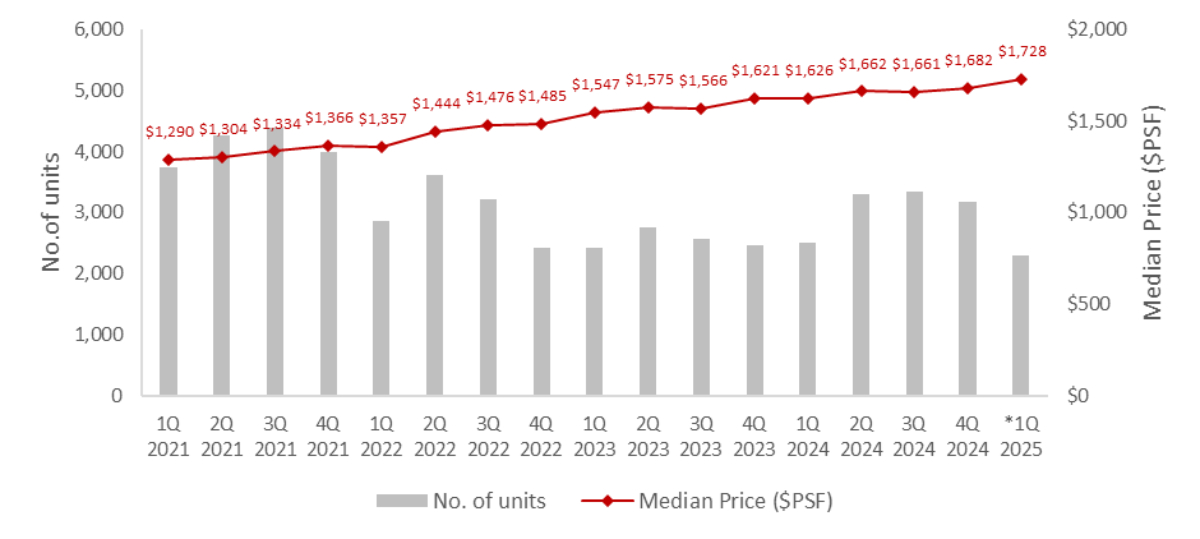

Resale and Sub-Sale (Non-Landed Homes, Excluding EC)

Based on URA caveat as of 26 March 2025, resale transactions accounted for 39.8% of all non-landed private home sales (excluding ECs) in 1Q 2025, corresponding to a total of 2,294 resale units changing hands over the quarter. Compared to the last period, which saw 3,173 resale transactions in 4Q 2024, this represents a 27.7% q-o-q decline in the number of resale units sold.

Chart 3: Resale Transactions and Median Price for Non-Landed Homes (excluding ECs)

Source: URA as of 26 Mar 2025, ERA Research and Market Intelligence

This finding also marks a continuation of 4Q 2024’s decline in resale transactions for non-landed private homes (excluding ECs), whereby a 4.9% q-o-q downtick was observed last quarter.

These successive downticks in resale volume could plausibly be due to competition posed by the new sale market, as well as the tapering number of private home completions. At present, URA’s full-year estimates for completions of private homes (excluding ECs) stand at 5,846 units for 2025, which is notably lower than the equivalent of 8,460 units for 2024.

Conversely, this relative scarcity of new completions could have fuelled price growth in the resale market, as available inventory diminishes. This resulting upwards price pressure dovetails with the slight 2.7% q-o-q uptick in median unit prices observed for 1Q 2025.

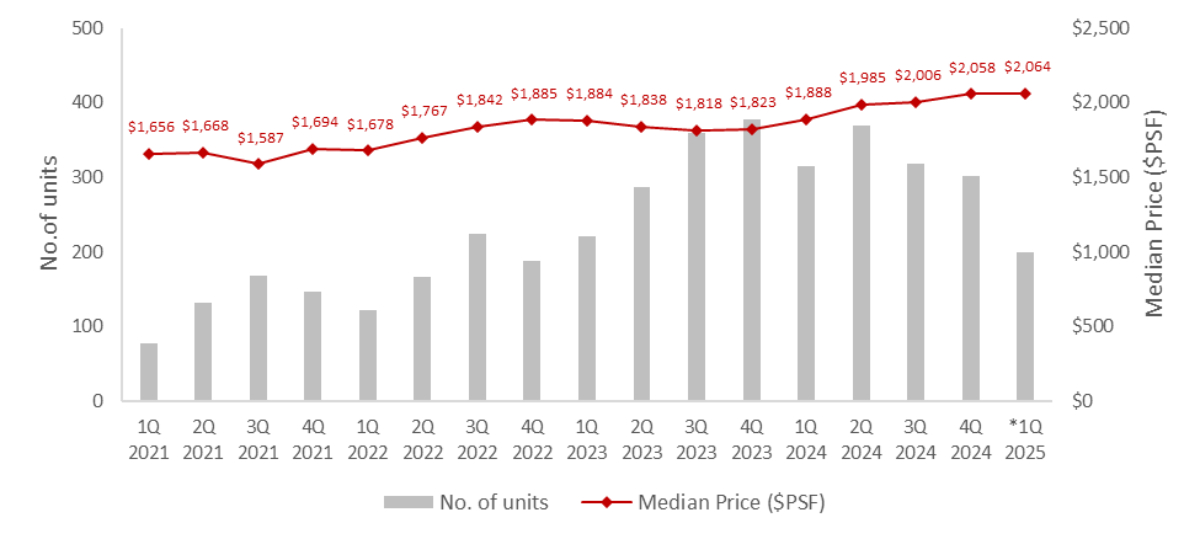

Chart 4: Sub-Sale Transactions and Median Price for Non-Landed Homes (excluding ECs)

Source: URA as of 26 March 2025, ERA Research and Market Intelligence

Sub-sales, on the other hand, made up 3.5% of all non-landed private home sales (excluding ECs) in the quarter, clocking a total of 199 transactions based on available caveat data. On the quarter, this represents a 34.1% q-o-q decline from the 302 transactions recorded for 4Q 2024. Median unit prices in the sub-sale market also edged up by 0.4% q-o-q, reaching $2,064 psf.

These movements in the sub-sale market were likely shaped by the same factors influencing resale trends, namely the robust uptake of new launches and declining secondary stock.

Market Outlook

The coming months will likely see launches in the CCR and RCR, such as One Marina Gardens, Bloomsbury Residences (in Media Circle) and Upperhouse in Orchard Boulevard. One Marina Gardens and Bloomsbury Residences will appeal to astute buyers or investors who take a long-term view on the market as these locations undergo masterplan transformation. Separately, Upperhouse at Orchard Boulevard aims to attract well-heeled, lifestyle-driven buyers, with its location beside the Orchard Boulevard MRT station serving as an added advantage.

These buyers tend to take a more deliberate approach when evaluating investment opportunities, so sales for these projects may progress at a more measured pace, reflective of the discerning nature of these buyers.

Building on the recent momentum in new home sales, ERA has revised our earlier projection of 7,000 and 8,000 new home sales to 8,500–9,500 units for the whole of 2025.. In conjunction, sub-sale and resale transactions are also expected to reach between 1,100 to 1,300 units and 14,000 to 15,000 units respectively by the close of 2025.

Table 2: Upcoming launches in 2025

Source: ERA Project Marketing

Executive Condominium

Source: ERA Project Marketing

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.

Figures are based off the official flash estimates for HDB/URA quarterly statistics, released on 25 April 2025.

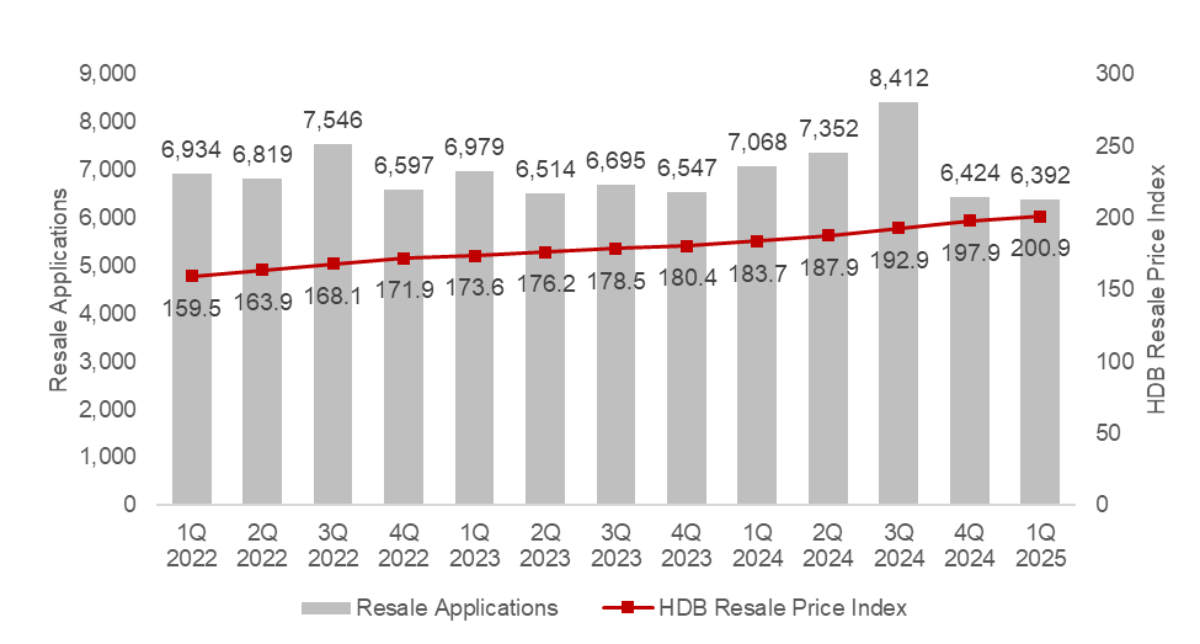

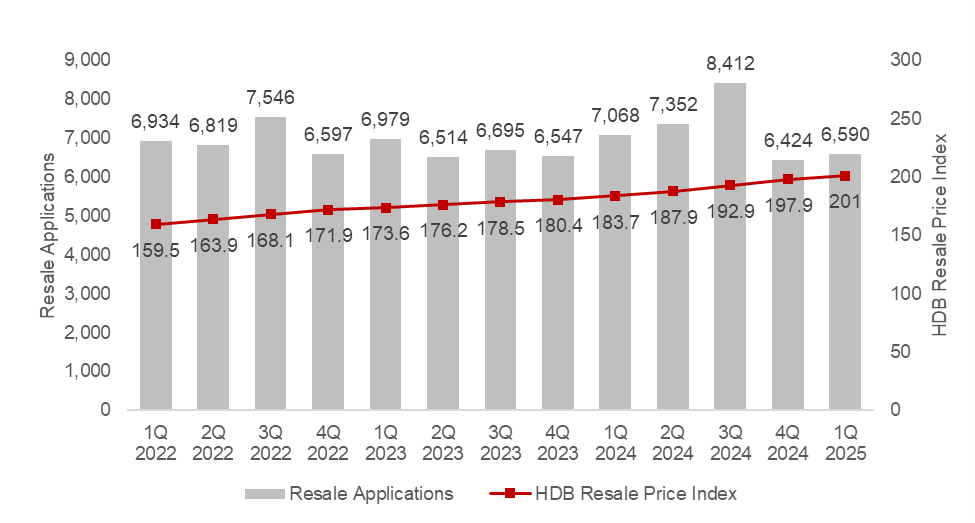

According to the Housing and Development Board (HDB)’s quarterly report, the HDB RPI rose to 201.0, a 1.6% increase quarter-on-quarter (q-o-q) in 1Q 2025.

This is the 23rd consecutive quarter of growth of the RPI, and is lower than the average quarterly growth of 2.3% in 2024.

Chart 1: HDB RPI vs Number of Transactions

Source: HDB, ERA Research and Market Intelligence as at 25 April 2025

Transaction Volume Down Amidst Seasonal Lull

There were a reported 6,590 HDB resale transactions recorded in 1Q 2025. This was a 6.8% decline y-o-y.

The lower transaction volume witnessed in the quarter can be attributed to the seasonal lull and the bumper crop of over 10,000 Build-to-Order (BTO) and Sale of Balance Flats (SBF) offered through an exercise in February. With these many BTO and SBF flats on offer, buyer’s eyes may have been pried away from the HDB resale market.

Compared to 4Q 2025, there were more 3-room and 4-room flats transacted in 1Q 2025, while the number of executive flats sold continues to decline.

February saw the first BTO launch of the year, which offered highlights such as a pair of Plus flat projects in Queenstown, as well as affordable projects in Woodlands and Yishun (Chencharu) – with one of the latter mentioned projects being an integrated housing development, with a bus interchange and commercial segment.

These SBF flats feature shorter waiting times compared to BTO flats. With 4 out of 10 SBF flats are already completed, this allows buyers to move in at a short notice.

The remainder of the SBF projects mostly had drastically reduced wait times and might be appealing to homebuyers who might have less urgent housing needs, offering a more affordable alternative to the resale market.

The SBF exercise offered flats in mature estates and centrally located (prime) locations, but without the new resale restrictions imposed on newer Prime Location Housing (PLH) flats. Combined with a shorter completion runway, these flats drew high application rates and could have stolen some of the thunder away from the resale market.

Applicants of these flats are waiting the results – should they not be able to secure a unit, we could very well see them return to the resale market in 2Q 2025.

Fewer MOP flats compared to 2024

In 2025, we will see 5,082 HDB flats fulfil their Minimum Occupation Period (MOP). This figure is 38.5% less than what we witnessed in 2024, which already saw stress being placed on resale prices.

This is apparent for resale flats in central locations and mature estates. BTO flats in these locations fall under the new classification of Plus and Prime classification BTO flats may have driven more homebuyers to seek out HDB resale homes instead.

Chart 2: Number of MOP Flats by year

Source: HDB as at 27 March 2025, ERA Research and Market Intelligence

These buyers are unwilling to accept the resale restrictions such as a 10-year Minimum Occupation Period, rental restrictions after MOP, subsidy clawback upon resale and resale income cap that the new classification of flats place on future buyers.

With fewer of these flats being made available, prices for them are steadily increasing, which could discourage buyers with more modest budgets from making their upgrades or purchases.

Likewise, knowing the lack of supply in the market now, homeowners of these flats could have greater holding power and are less likely to sell their units unless a good deal falls into their hands.

Million-Dollar Flat Transactions on the rise

In 1Q 2025, there was an increase in the number of million-dollar flat transactions from 285 in 4Q 2024, to 348 in 1Q 2025. This is a 22.1% q-o-q increase and a 90.2% y-o-y increase from 183-million-dollar transactions in 1Q 2024.

We noted that 271 (or around 78%) of these million-dollar flat transactions consisted of 4-room and 5-room flat transactions. A 5% increase from the previous four quarter average, this shows a trend of 4-room and 5-room flats increasing in price, driving the million-dollar flat market.

Chart 3: HDB Flat Transactions over $1m

Source: HDB as of 27 Mar 2025, ERA Research and Market Intelligence

The percentage of million-dollar flat transactions in 1Q 2025 accounted for 5.3% of all transactions this quarter.

Flats in mature estates continue to make up the bulk of the million-dollar flat transaction, highlighting the demand for homes in choice locations.

Apart from private home downgraders, there are increasingly more HDB dwellers willing to shell out a premium for a newly and centrally located flats. They may choose to upgrade within the HDB market itself, opting to purchase larger homes in central locations with longer leases, such as newly-MOP flats. These homes offer outstanding location attributes, with good transport connectivity, amenities and proximity to good schools, making them a great choice.

With the decline in the number of MOP flats in 2025, we expect to see prices of these flats continue to rise amid firm demand.

Chart 4: HDB Transactions by Price Ranges

Source: data.gov.sg as of 27 March 2027, ERA Research and Market Intelligence

Despite this, the majority of HDB resale flats remain affordable. Some 53% of the HDB resale transactions in 1Q 2025 fell between $500k and $750k, a comfortable price range for most Singapore homebuyers. Another 24% fell between $250k and $500k. This makes up about three-quarters of HDB resale transactions that still remain affordable and accessible to homebuyers.

ERA’s Outlook and Forecast for the rest of the year

We should see a recovery in transaction volume in the following quarters as applicants of the BTO and SBF exercises that took place in the quarter are likely to look towards the resale market in the following months if they are unable to secure their units. This should, in turn bolster transaction volume in 2Q 2025.

With a reduced supply of MOP flats in 2025, which have been a key driver of price growth in recent years, we should see a moderate price growth, and fewer transactions to close out the year. We anticipate an overall 3% – 6% price growth, with 26,000 – 27,000 resale HDB flat transactions by end-2025.

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.

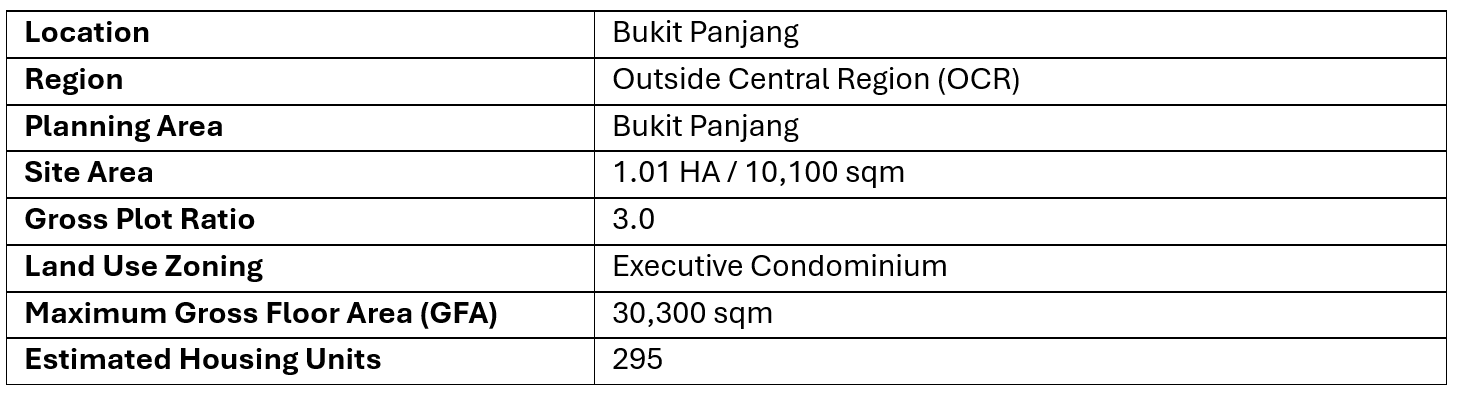

HDB has launched the tender for the Government Land Sale (GLS) parcel at Senja Close, for an executive condominium (EC). The tender for sale will close at 12 noon on 5 August 2025.

Site Details

Table 1: Details of Senja Close EC GLS Site

Source: URA

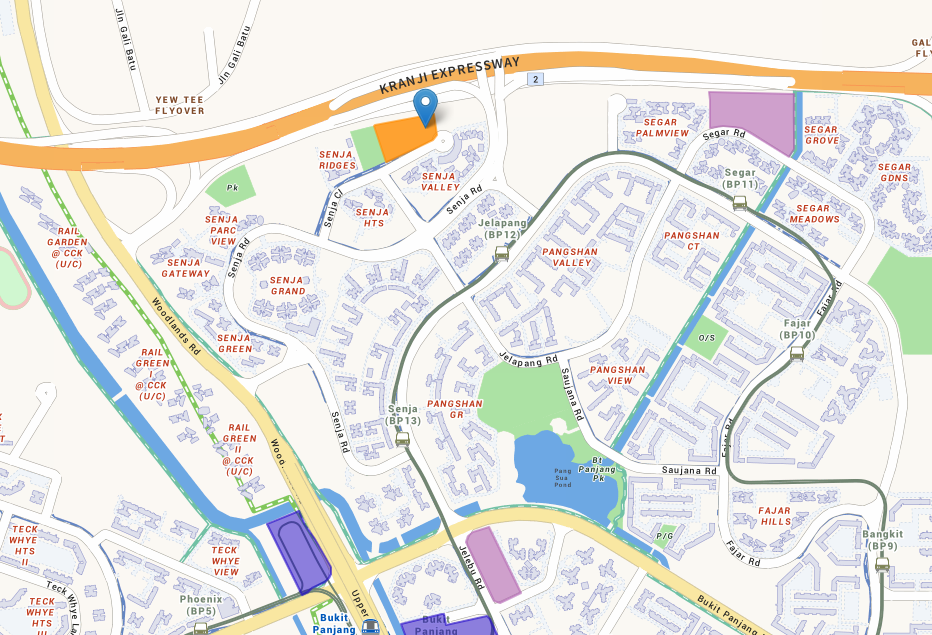

Map of the Senja Close EC site

Source: URA

Locational Attributes

The Senja Close site is within a 10-minute walk to Jelapang LRT station, which is two LRT stops away from Bukit Panjang Station on the Downtown Line (DTL). The DTL connects to Singapore’s downtown and eastern regions. Located a few stops away from Jelapang LRT Station is also Choa Chu Kang MRT and Bus Interchange on the North South Line (NSL).

Major roads and expressways serving the site include the Kranji Expressway (KJE), Woodlands Road, and the Bukit Timah Expressway (BKE). Additionally, Woodlands Regional Centre and the Jurong Lake District are 20 minutes away from the site.

Despite being located within a residential enclave, Senja Close is surrounded by three primary schools, all within a 1km radius. Residents can also experience the convenience of living near a suite of amenities. These include Senja Hawker Centre, Senja Woods (neighbourhood park) and Greenridge shopping centre (neighbourhood mall).

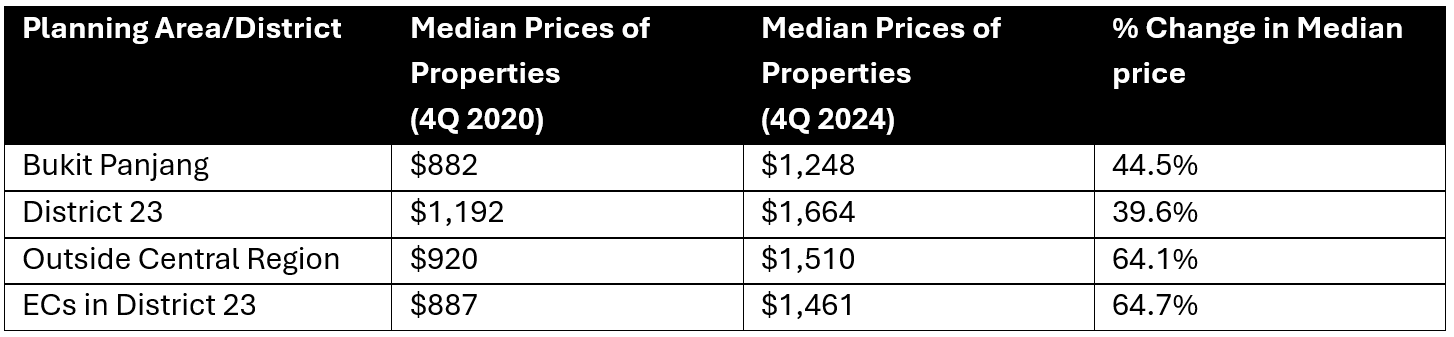

Price and Market Trends

Between 4Q 2020 and 4Q 2024, the median price psf of ECs in Bukit Panjang, District 23, and OCR have increased across the board. Over this period, median prices in Bukit Panjang and District 23 saw a big increase of 44.5% and 64.7% respectively. Additionally, OCR ECs recorded a significant 64.1% jump. For ECs in District 23, median prices have also risen 64.7% from $887 psf in 4Q 2020 to $1,461 psf in 4Q 2024.

Table 2: Prices of All Non-Landed Private Homes in the Vicinity

Source: URA as of 24 February 2024, ERA Research and Market Intelligence

ECs are a popular choice amongst HDB upgraders

ECs have consistently been a popular choice among HDB upgraders. This is due to their more accessible pricing compared to private condos. Last year, new homes sized between 900 to 1,000 sqft in the OCR saw a 42% difference in median prices between ECs ($1.48M) and private condos ($2.10M). This gap highlights the value proposition of ECs, particularly for HDB upgraders who meet the income ceiling of $16K. Hence, buyers, particularly HDB upgraders, see value in ECs.

Apart from commanding lower prices than new private condos in the OCR, homebuyers have the additional flexibility of not needing to dispose of their existing home, prior to purchasing an EC. This is on top of the added benefit of ABSD remission for Singaporean purchasers.

Moreover, EC buyers may opt for the Deferred Payment Scheme (DPS), whereby they will only need to pay a deposit and defer their EC loan till after it has been completed. In this way, the buyers will not need to service two mortgages while waiting for their new home.

With no ABSD payable and the availability of the DPS, HDB owners will find it easier to upgrade to new ECs.

This widespread appeal is reflected by the over-50% take up rates observed at the last four EC launches, including the latest Aurelle of Tampines. These figures could be even higher if not for the second-timer quota of 30% at launch.

Potential Demand

Demand for this site will come from primarily from HDB upgraders living in the western and northern regions of Singapore. Between 2024 and 2027, an estimated number 2,344 flats (4-room and larger) in Bukit Panjang, Choa Chu Kang and Bukit Batok will fulfil their Minimum Occupation Period (MOP).

Given the scarcity of fresh EC supply in the immediate vicinity, we may see competitive bidding activity for this site. Likewise, the presence of an LRT station nearby and amenities like Senja Hawker Centre and Greenridge Shopping Centre could further boost the site’s attractiveness to developers and potential buyers alike.

Currently, the median transaction price of 5-room flats in 2024 at Bukit Panjang, Choa Chu Kang and Bukit Batok are $658,000, $618,000 and $758,500 respectively.

Additionally, this is the third Executive Condominium development in Bukit Panjang, which will further increase demand due to the limited supply of ECs in the Bukit Panjang planning area. This could also fuel buyers’ available cash on-hand, further boosting demand from HDB upgraders.

Table 3: HDB flats reaching MOP between 2024 to 2027

Source: Singstat, ERA Research and Market Intelligence

The last Bukit Panjang EC site tender (now Blossom Residences) dates back to December 2010, resulting in five bidders and a land cost of $271 psf ppr. Furthermore, with Blossom Residences being the last EC launch in Bukit Panjang since 2011, the Senja Close site could see some pent-up demand from HDB upgraders in the vicinity.

Shortage of New ECs

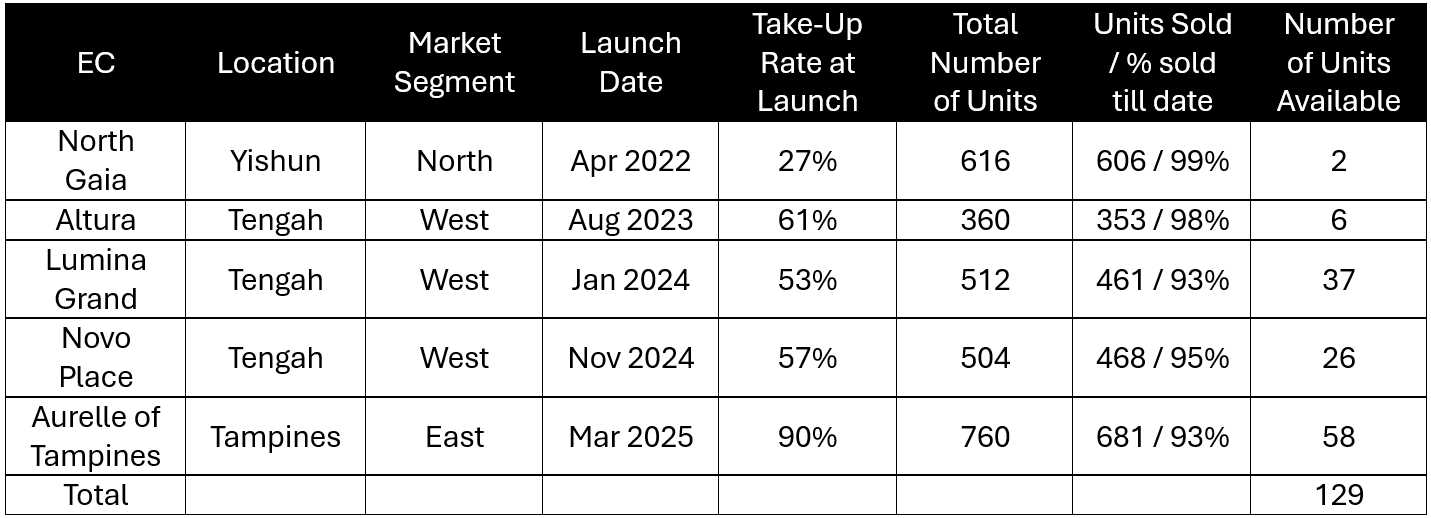

As of 27 March 2025, the current supply of new EC homes is fairly limited, with fewer than 130 units available across five projects island wide. Though there are another two projects at Plantation Close and Jalan Loyang Besar slated to be launched this year, this incoming supply might still fall short of demand.

Table 4: New ECs available

Source: ERApro as of 27 Mar 2025, ERA Research and Market Intelligence

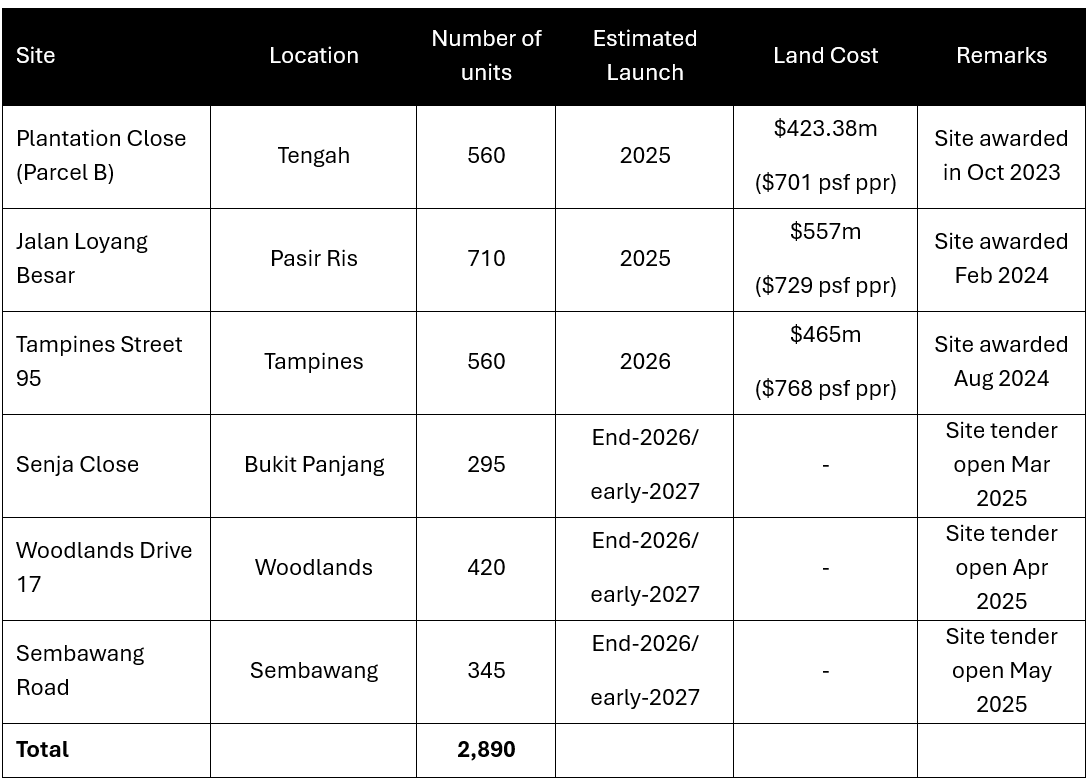

There is also a low EC supply in the pipeline. In the West, all existing new ECs are located in Tengah, which is a new estate. For those looking to stay in an estate with amenities and a transport network that is already established, they will look to this site. Moreover, the only other future launch in the West is the 560-unit Plantation Close (Parcel B) development is available.

Table 5: EC units in the pipeline

Source: URA, ERA Research and Market Intelligence

Developers have to be cautious because of buyers’ affordability

Due to the income ceiling of $16,000, as well as the Mortgage Servicing Ratio (MSR) and Total Debt Servicing Ratio (TDSR), the maximum loan a buyer can borrow is approximately $1.01 million. Amid rising EC prices, and a cap in loan quantum, EC buyers will now have to satisfy a larger initial cash outlay.

This may potentially deter upgraders to enter the EC market, instead opting for full private condominiums. Although they come with a higher price tag, buyers may only need to put a lower down payment. Moreover, they can take a larger loan as private properties are only subjected to only the TDSR, and not the MSR.

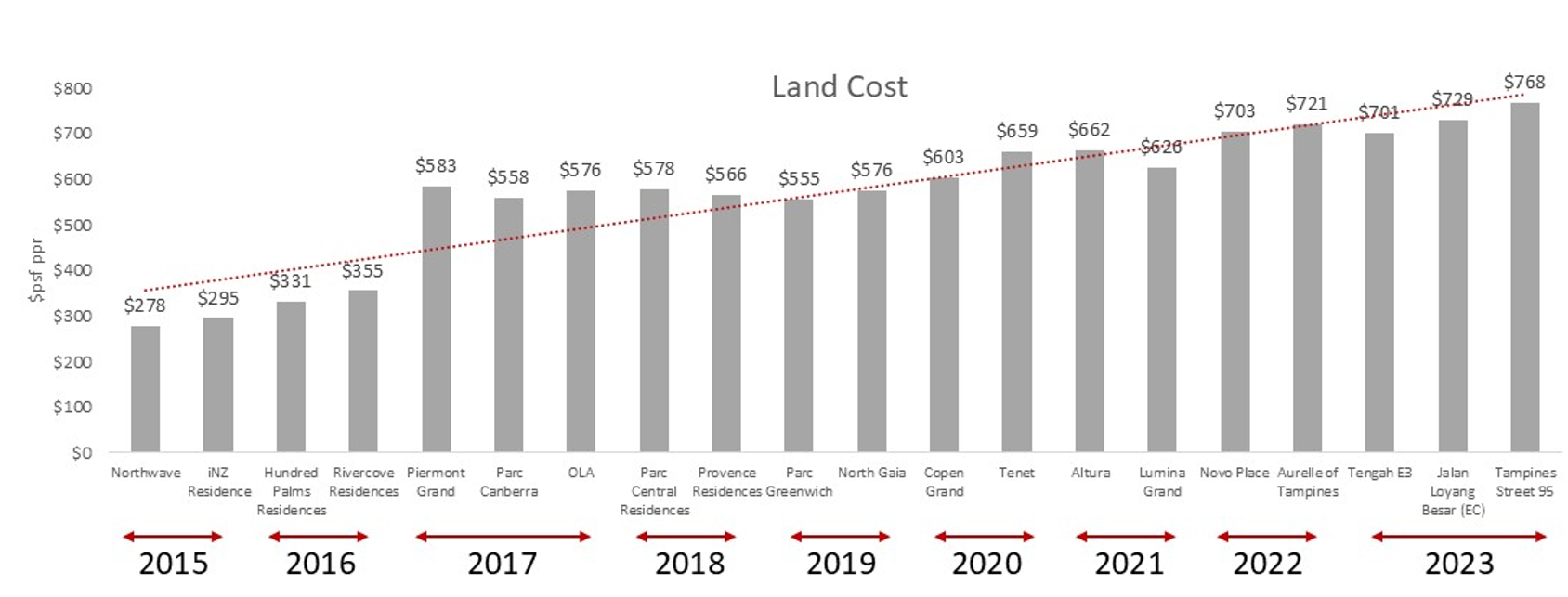

Rising EC Land Cost

The continued strong demand for new ECs has resulted in developers increasingly aggressive bidding strategy. Between 2015 and 2024, the average EC land costs have risen 164%, from $287 psf ppr to $733 psf ppr. To illustrate a more recent example, the Tengah Garden Walk EC site, subsequently launched as Copen Grand, was awarded to a joint venture between City Development Group and MCL Land, at $603 per square foot per plot ratio (psr ppr) in 2021.

As such, we could see new benchmark prices for ECs. Prices will be a far cry from the last EC sold in Bukit Panjang at Segar Road. In 2010, the site was awarded for just $271 psf ppr.

Chart 1: Land cost of ECs since 2015

Source: URA, HDB, ERA Research and Market Intelligence

Conclusion

Developers could show moderate interest in this Senja Close EC site, given limited competition due to the scarcity of fresh EC supply in the immediate vicinity. ECs also present less risk than other private sites, with a lower upfront cost and strong buyers’ demand. Developers could also take cues from the overwhelming demand at Aurelle of Tampines’s launch weekend and submit bid prices accordingly.

In view of the healthy EC demand, the government has committed to releasing three EC sites for sale in 1H 2025, and the Senja Close site is the smallest among them. Considering the size of the site, coupled with healthy EC demand, we could see more intense bidding competition. Since 2021, nine EC sites launched, averaging 6.7 bids from developers.

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.