4Q 2024 URA Private Residential Report – Singapore’s Private Home Prices Climb 3.9% for Full-Year 2024, Slowest Growth Since 2020

- ERA Singapore

- 11 min read

- Research

- 24 Jan 2025

SINGAPORE, 24 January 2025 – According to the Urban Redevelopment Authority (URA)’s report for 4Q 2024, private home prices had risen 2.3% quarter-on-quarter (q-o-q), marking a reversal of the 0.7% q-o-q decline observed in 3Q 2024.

In tandem, total transaction volume of private homes also rose to 7,433 units in 4Q 2024, marking a significant increase of 38.4% from the 5,372 units recorded for 3Q 2024.

4Q 2024’s price uptick also brings full-year growth to 3.9% for private homes, reflecting a slower pace of increase compared to the 6.8% growth achieved in 2023. This is also the slowest rate of growth since 2020, when the all-private residential price index rose 2.2% y-o-y.

Comments by ERA

“The overall private residential price index experienced its slowest growth since 2020, growing at a more moderate pace in 4Q 2024. The growth was supported by new home launches such as The Collective at One Sophia, Emerald of Katong, Chuan Park and Nava Grove that have helped supported home price growth in all regions.” Said Marcus Chu, CEO, ERA Singapore.

“Since the series of Fed interest rate cuts from September 2024, we have seen a surge in buyer confidence across the board driving an uptick of market activity in 4Q 2024. 4Q 2024 new home sales accounted for just above half of the new home sold in 2024 and is the highest since 3Q 2021. Likewise, Resale and Sub-sale transactions rose 22.6% y-o-y in 2024.”

“Today’s market is reflective of genuine upgraders’ demand and the buyers welcomed the interest rate cuts as a much-needed reprieve from the higher interest rate environment since 2022. Although we are seeing higher home prices, majority of the buyers’ affordability remains constrained by the price quantum.”

“With landed homes price growing at a more moderate pace of 0.9% y-o-y in 2024, we have seen transaction volume rise by 29.9% y-o-y, from 1,286 units in 2023 to 1,671 units. The rising non-landed home prices have also helped supported more Singaporeans to move into the landed property segment.”

“Going forward, with fewer completions expected in 2025, we may see a supply crunch in the secondary market, prompting buyers to pivot toward the new home market instead. While unsold stock has gradually tapered to 19,606 in 4Q 2024, the upcoming 24 new home launches in 2025 will inject fresh supply of new homes.”

Nonetheless, ERA remains cautiously optimistic about Singapore’s residential market in 2025. Supported by strong macroeconomic fundamentals, Singapore is likely to strengthen its position as a ‘safe harbour’ amid looming economic uncertainties.

Assuming stable macroeconomic conditions and the absence of unforeseen negative factors, new home prices are expected to continue their upward trajectory, potentially achieving 3-5% y-o-y growth in 2025. The ample new home launches will support new home transaction volume which is projected to reach between 7,000 to 8,000 units in 2025, dependent on a favourable economic outlook.

ERA estimates that sub-sale transactions will range between 1,100 to 1,300 units, with median prices possibly growing by 7% to 9%. Resale transactions are also expected to reach between 14,000 to 15,000 units, accompanied by a median price growth of 6% to 8% by the close of 2025.

Rents have eased in 2024, on the back of higher completion since 2023 that led to strong competition for tenants. Looking ahead, with the supply of completed units tightening in both the private home and HDB markets, prices in the residential leasing market are primed for growth in 2025. Moreover, assuming no significant changes in economic conditions and foreign worker numbers, rental demand is also likely to stay consistent next year without any significant spikes or declines.

However, rental price growth is likely to diverge across the market, with newly completed homes expected to sustain stronger rent appreciation, while older properties may experience slower or flattish growth. Similarly, properties in Singapore’s outlying regions could see sharper increases in rents and stronger demand as tenants become more cost-conscious.

Come next year, ERA forecasts tempered rental price growth for private homes within a projected range of 0 to 3% y-o-y in the face of fewer completions and a more cautious economic outlook. We also anticipate the number of private home rental contracts to remain consistent, with numbers expected to reach between 80,000 and 90,000 in 2025.

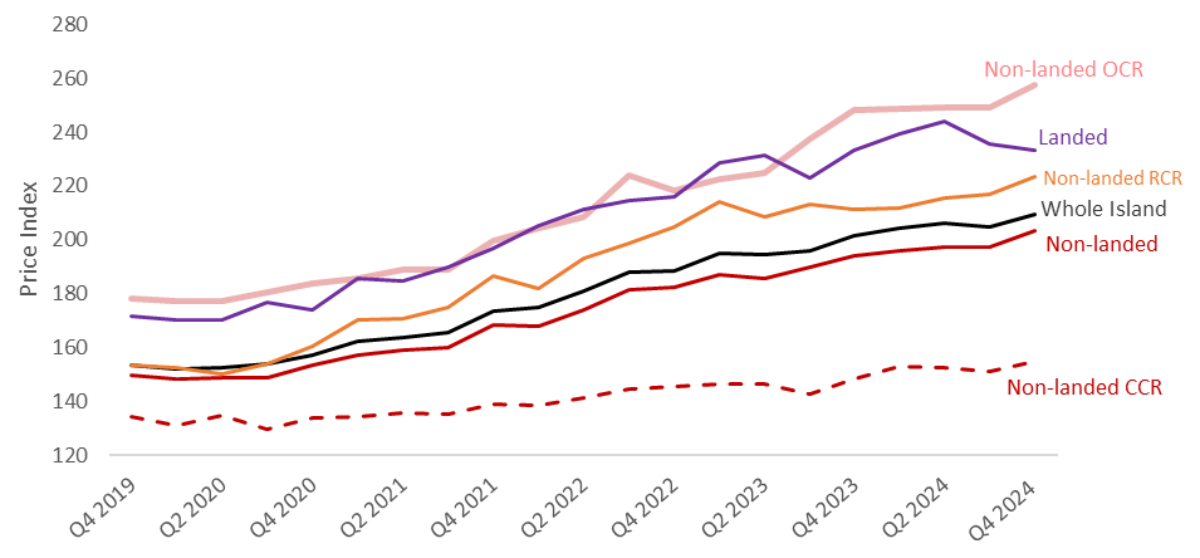

URA Private Property Index

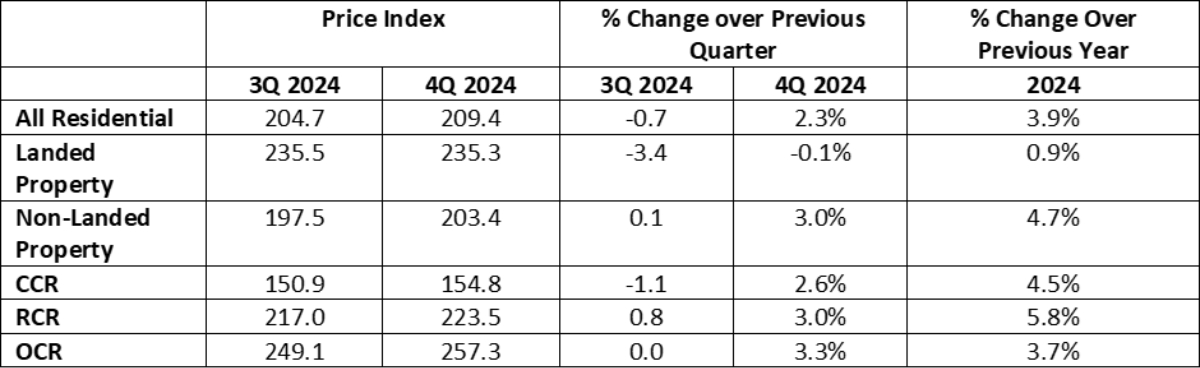

In 4Q 2024, the All-Residential Property Price Index (PPI) rose by 2.3% quarter-on-quarter (q-o-q). This is a reversal of 3Q 2024’s performance which saw prices dipping by 0.7% q-o-q. The final print figure also aligns with the 2.3% q-o-q increase per URA flash estimates released earlier on 2 Jan 2025.

In the non-landed private home segment, prices rose 3.0% q-o-q in 4Q 2024. Notably, this is a more pronounced increase compared to the 0.1% q-o-q gain in non-landed private home prices in 3Q 2024.

Leading these price shifts was the Outside Central Region (OCR), which saw a 3.3% q-o-q uptick for non-landed private homes. Likewise, the Core Central Region (CCR) and Rest of Central Region (RCR) both saw prices lift by 2.6% q-o-q and 3.0% q-o-q respectively.

In the landed property sub-market, prices shrank by 0.1% q-o-q in 4Q 2024. This decline is notably smaller than the 3.4% q-o-q downtick registered in the previous quarter.

Chart 1: URA Private Property Price Indexes

Table 1: Change in URA Private Property Price Indexes for 3Q 2024 and 4Q 2024

Transaction Volume

Transaction numbers for all private properties rose substantially in 4Q 2024. Based on latest figures released by URA, a total of 7,433 private homes were moved on the primary and secondary market. This surge represents a sharp increase of 38.4% q-o-q from the 5,372 units sold in 3Q 2024.

In terms of overall annual transactions for all private homes, 2024 saw full-year sales reaching 21,950 units, up 15.3% from the 19,044 units sold in 2023. This 52.9% downtick from the last high in 2021, which saw 33,557 units sold.

Notably, buyers of private homes were also largely driven to the secondary market in 2024, with the full-year figure for resale transactions rising to 14,053 units from 11,329 units in 2023.

Possible factors for this uptick in resale transactions include lower borrowing costs following the Fed’s interest rate cuts, as well as the widening price gap between new and resale non-landed private homes (excluding ECs).

Based on caveat data, the gap in median prices between the new and resale non-landed private homes (excluding ECs) widened significantly from 34.0% in 3Q 2024 to 52.5% in 4Q 2024.

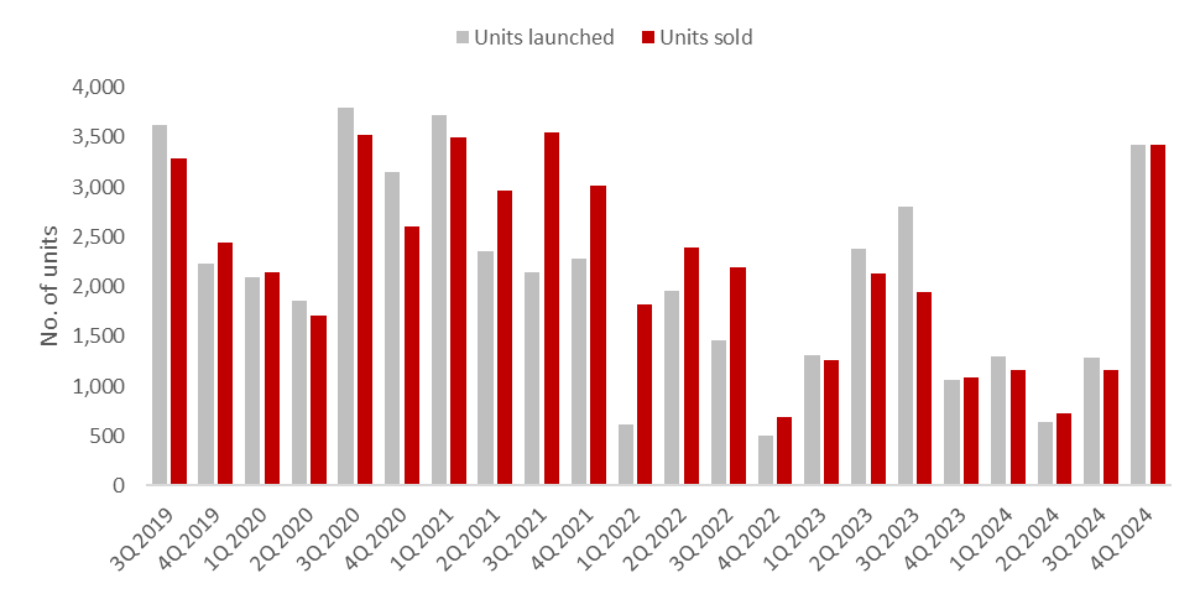

New Private Home Sales (Excluding ECs)

4Q 2024 saw a resurgence in sales of new private homes (excluding ECs), with corresponding transaction volume reaching 3,420 units over the course of the quarter. On the quarter, this represents a 194.8% q-o-q increase over the 1,160 units sold by developers in 3Q 2024.

This upturn in sales coincides with an increase in the number of private homes (excluding ECs) launched by developers. In 4Q 2024, a total of 3,425 units made their debut across several highly anticipated projects, including but not limited to Chuan Park, Union Square Residences, The Collective at One Sophia, Emerald of Katong, and Nava Grove.

The number of private residential units launched in 4Q 2024 also represents a 166.7% q-o-q increase over the 1,284 units brought to market by developers in 3Q 2024.

Correspondingly, the unsold stock of private homes (excluding ECs) contracted 2.7% q-o-q to 19,405 units in 4Q 2024, down from the 19,940 units recorded in 3Q 2024. As a result, this could lead to upward pressure on new home prices as buyers face a more competitive market.

Chart 2: New Homes Launched and Sold (Excluding ECs)

Executive Condominium

Following the debut of Novo Place in November, the number of Executive Condominium (EC) units sold by developers rose sharply to 528 units in 4Q 2024, representing a 407.7% q-o-q increase over the 104 units sold in 3Q 2024.

Additionally, a total of 504 EC units were launched by developers in 4Q 2024, contrasting the lack of fresh supply in the absence of new EC projects during 2Q and 3Q 2024.

Resale and Sub-Sale (Excluding ECs)

Chart 3: Resale and Sub-sale Transaction Volume

In 4Q 2024, sales of private homes (excluding ECs) were driven equally by both resale and new sale transactions. Based on URA Realis data, new sale transactions constituted 46.0% of the quarter’s private home sales (excluding ECs), while resale transactions accounted for 49.8%.

On the quarter, sales of private homes (excluding ECs) on the resale market fell by 4.1% q-o-q, from 3,860 units in 3Q 2024 to 3,702 units in 4Q 2024.

Sub-sales of private homes (excluding ECs) also fell over the quarter. Based on latest data from URA, a total of 311 sub-sale transactions were recorded for 4Q 2024, reflecting 11.6% q-o-q decline from the 352 transactions in 3Q 2024.

Landed Homes

Chart 3: Landed homes sold in each quarter

Prices of landed homes rose 0.1% in 4Q 2024, reversing the 3.4% decrease in the previous quarter. For the whole of 2024, prices of landed homes grew at a more moderate pace of 0.9% y-o-y.

According to caveats, 441 landed homes were sold in 4Q 2024, similar to 3Q 2024. For the whole of 2024, landed property transaction volume rose by 29.9% y-o-y, from 1,286 units in 2023 to 1,671 units.

According to caveat data, the majority of landed home transactions (67.8%) in 4Q 2024 were priced between $3.5M and $7M.

Moreover, a possible factor for price increases during the quarter was the notable surge in landed home sales within the $6M to $7M range, rising from 14 units in 3Q 2024 to 45 units in 4Q 2024. In turn, this heightened demand for higher-priced homes can be traced back to the Federal Reserve’s interest rate cuts, which boosted buyer receptiveness.

Leasing

Rents for private residential properties remained unchanged in 4Q 2024, with the all-residential rental index remaining at 157.9, similar to 3Q 2024. Rents for non-landed properties also rose further by 0.2% q-o-q in 4Q 2024, continuing the positive trend observed in 3Q 2024. Rents of landed properties meanwhile fell by 1.8% q-o-q.

By region, rents for non-landed private properties rose 0.9% q-o-q in the CCR. Likewise, rents for the RCR rose by 0.3% while rents in the OCR fell by 0.8% in 4Q 2024.

According to URA Realis data, a total of 18,340 non-landed residential rental contracts were also inked in 4Q 2024, marking a 24.8% q-o-q downtick over the previous quarter.

For the whole of 2024, rentals of non-landed properties in the CCR, RCR, and OCR decreased by 2.4%, 1.3% and 1.3% respectively, a contrast from the respective increases of 5.0%, 9.0% and 7.5% in 2023

Looking ahead, rents for non-landed properties are expected to grow further in 2025. This is due to a noticeable decline in completions, which is likely to apply upward pressure on rental prices.

While completions of non-landed homes (excluding ECs) totalled 3,253 units in 3Q 2024, this dipped slightly with 3,084 private homes in 4Q 2024. Furthermore, projected full-year completions for non-landed homes (excluding ECs) currently stands at 5,846 units for 2025, which is markedly lower than the 8,460 units completed in 2024.

What Lies Ahead for the Private Home Market in the Coming Months?

Though recent interest rate cuts and a more positive economic outlook have breathed new life into the new launch market, challenges remain with the possibility of higher-for-longer interest rates, an impending Trump presidency, as well as ongoing trade tensions that could impede Singapore’s economic growth.

Nonetheless, ERA remains cautiously optimistic about Singapore’s residential market in 2025. Supported by strong macroeconomic fundamentals, Singapore is likely to strengthen its position as a ‘safe harbour’ amid potentially stormy conditions. This could, in turn, boost buyer confidence and bolster demand for new private homes even in the face of a challenging global economy.

Assuming stable macroeconomic conditions and the absence of unforeseen negative factors, new home prices are expected to continue their upward trajectory, potentially achieving 3-5% y-o-y growth in 2025. The ample new home launches will support new home transaction volume which is projected to reach between 7,000 to 8,000 units in 2025, dependent on a favourable economic outlook.

ERA estimates that sub-sale transactions will range between 1,100 to 1,300 units, with median prices possibly growing by 7% to 9%. Resale transactions are also expected to reach between 14,000 to 15,000 units, accompanied by a median price growth of 6% to 8% by the close of 2025.

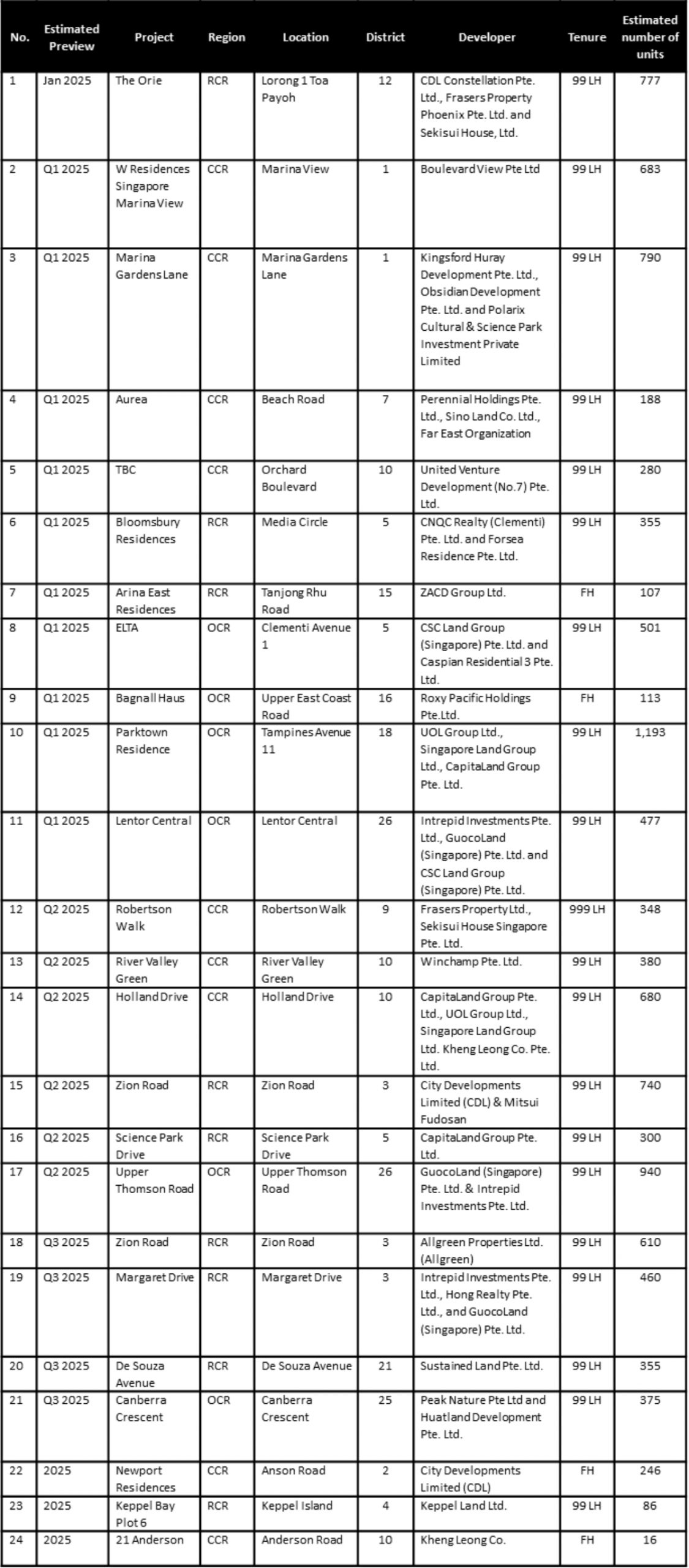

Table 2: Upcoming launches in 2025

Executive Condominium

I confirm that I have read theprivacy policy and allow my information to be shared with this agent who may contact me later.