Holland Village has been the talk of the town of late, but not for the same reasons as before.

In its heyday, this centrally-located town was widely recognised as one of Singapore’s most iconic cultural hotspots, especially with its varied nightlife venues and dining options that drew in crowds. More recently, however, it has made headlines for much a different reason: Holland Village has taken on a new identity, though not by choice.

Once a neighbourhood steeped in artistic charm, Holland Village has lost much of its former character amid a leaner commercial landscape. The departure of many familiar names (think Bynd Artisan, Thambi Magazine Store, and Crystal Jade La Mian Xiao Long Bao) has not only dimmed Holland Village’s once-vibrant identity, but has also left long-time visitors with a deep yearning for the past.

Yet, new additions in recent years, like One Holland Village and its accompanying residences, have breathed fresh life into the area. This raises the question: Where will this distinctive neighbourhood go from here?

Holland Village is no stranger to change

Source: Google Maps, ERA Research and Market Intelligence

Bounded by Holland Road and Holland Avenue, Holland Village mostly comprises of shophouse rows and low-rise malls featuring an eclectic mix of businesses, anchored by Holland Village Market & Food Centre at its heart.

While this is the Holland Village that so many have grown to know (and love), this current identity is just but the latest chapter in its ongoing evolution.

Long before becoming a beloved enclave, Holland Village started life as a recreational neighbourhood for British soldiers in the 1930s. Also, during this time, the areas surrounding Holland Village were primarily occupied by crop plantations and a Chinese cemetery; both remained until their respective plots were acquired for redevelopment in the 1960s.

Subsequently, with more military housing built in the 1960s, Holland Village’s community continued to flourish. Alongside it came pubs, tailors, and other westerner-centric businesses, ultimately solidifying the area’s reputation as an expatriate neighbourhood.

Within the next decade, however, a stronger Singaporean presence gradually took shape in Holland Village. This was mainly due to the completion of Buona Vista’s first HDB estate in 1972, as well as Holland Road Shopping Centre, which helped local communities and businesses to stay rooted.

By the 2000s, this liveability was cemented with the opening of Holland Village MRT station. As part of the Circle Line, it continues to connect Holland Village residents to key destinations and business districts today, from HarbourFront to Marina Bay.

What’s happening at Holland Village recently? Also, what’s next?

As of late, Holland Village has welcomed a new wave of retail and dining options at One Holland Village, its latest mixed-use development. The project was jointly developed by Far East Organisation, Sekisui Group, and Sino Group, and it has breathed new life into the neighbourhood with family- and pet-friendly concepts since opening in December 2023.

Notable tenants include Surrey Hills Grocer’s first pet-friendly flagship outlet, a Mini Pitstop (formerly Mini Cooper) showroom, and contemporary Japanese bistro Ginkyo. Familiar names like Cold Storage and Guardian have also opened outlets at One Holland Village, enhancing everyday convenience for residents.

One Holland Village (Source: Far East Organisation, Sekisui House, Sino Group)

Simply put, there are now new reasons to visit, or even settle down in, Holland Village. But perhaps, the most essential factor of all is the availability of new housing options in the neighbourhood. As recently as 2019, private homebuyers were presented with One Holland Village Residences, which features 296 units across one- to four-bedroom configurations.

While One Holland Village Residences has since sold out as of March 2025, more options are on the horizon for homebuyers targeting HDB flats and condo offerings in the area.

Holland Drive GLS site location (Source: URA, ERA Research and Market Intelligence)

Under the 1H 2024 Government Land Sales (GLS) programme, yet another private residential site was launched for sale at Holland Drive in February. It was subsequently awarded to a consortium comprising Capitaland Development, UOL Group, Singapore Land Group and Kheng Leong Co. As it stands, future plans for the plot point towards it being launched as Skye at Holland in 4Q 2025.

Source: HDB, ERA Research and Market Intelligence

Table 1: Subscription rates for Holland Vista, as of 26 June 2025

| Flat Type | No. of Units | No. of Applicants | Seniors | First-Timer Families | First-Timer Singles | Second-Timer Families |

| 2-room | 114 | 415 | 4.0 | 0.4 | N.A. | N.A. |

| 4-room | 228 | 2,233 | N.A. | 6.6 | N.A. | 72.8 |

Source: HDB, ERA Research and Market Intelligence

On the public housing front, some 300 Build-to-Order (BTO) flats were launched under the Holland Vista project during June 2024’s balloting exercise. Featuring 2-room Flexi and 4-room units, Holland Vista is a Prime location project built on the site of a former car park. Furthermore, demand for these BTO flats was clearly strong, as seen by the robust first and second-timer subscription rates across all unit types.

But most importantly, this outcome underscores present-day interest for homes in Holland Village – and for this reason alone, it’s worth taking a look at the neighbourhood’s price trajectory.

Unpacking the growth of Holland Village and its homes

Located in District 10, Holland Village shares its locale with Tanglin and Bukit Timah, which are two of Singapore’s most affluent neighbourhoods. This sense of prestige has in turn, led to an increase in property values in Holland Village.

Chart 1: Median unit prices for non-landed private properties (excluding ECs) in District 10

Source: URA, ERA Research and Market Intelligence

From 2015 up till August 2025, median unit prices for resale non-landed private properties in District 10 have increased overall by 43.7%, rising from $1,562 psf to $2,244 psf. This results in a modest yet steady annual growth rate of about 3.3% across this period.

Chart 2: Median unit prices for non-landed private properties (excluding ECs) in Queenstown

Source: URA, ERA Research and Market Intelligence

Such growth is also reflected in the Queenstown planning area, which Holland Village is a part of. Between 2015 up to August 2025, median unit prices there rose sharply by 78.2%, from $1,258 psf to $2,030 psf; this translates into an annualised growth rate of approximately 4.4%.

Chart 3: Rental performance of non-landed private properties (excluding ECs) in District 10

Source: URA, ERA Research and Market Intelligence

Similarly, within the rental segment, non-landed private homes in District 10 have seen steady growth. Since 2021, median rents have climbed 47.4%, from $3.52 psf to $5.19 psf. At the same time, rental volumes have held relatively stable, with between 1,700 and 2,500 contracts signed each quarter.

Source: URA, ERA Research and Market Intelligence

Beyond price growth and rental prospects, Holland Village’s future potential is also underpinned by its proximity to one-north – itself a fast-growing hub for several high-value industries, including biomedical, Science, Technology, Engineering, and Mathematics (STEM) and Information and Communications Technology (ICT).

In the Draft Master Plan 2025, URA has also announced plans to revitalise neighbourhoods within one-north. Among them is Dover-Medway in the Greater one-north area, which is set to be developed into a new estate. Moreover, it could see up to 6,000 public and private homes being built in total, alongside supporting amenities.

What other new developments will be coming to Holland Village?

Skye at Holland (Source: Capitaland Development, UOL Group, Singapore Land Group and Kheng Leong Co.)

Come 4Q 2025, Holland Village will welcome its newest private home offerings at Skye at Holland. Jointly developed by Capitaland Development, UOL Group, Singapore Land Group and Kheng Leong Co., this project will feature approximately 666 units across two- to five- bedroom configurations.

Furthermore, being just a five-minute walk from Holland Village MRT station and near One Holland Village, Skye at Holland is poised to carry its namesake neighbourhood past its crossroads, bringing new homes and residential convenience to the area. So, will you experience the next chapter in Holland Village’s story?

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.

We’ve all seen them while flicking through the pages of home décor magazines, or when scrolling interior design websites: beautifully-designed homes showcasing the skill and workmanship of the renovation professionals who brought them to life.

But behind every dream abode achieved, there lies the potential for a renovation nightmare – one that’s plagued by miscommunication, frustration, and many a sleepless night. Thankfully, these issues – and much more – can be avoided. All it takes is keeping these renovation tips (and cautionary tales) shared by Qanvast at the top of your mind before your home makeover:

1. Check out the reviews for your shortlisted renovation firms

As with most personal projects, doing your own homework is essential before embarking on a renovation. And one must-do is to take a look at reviews online. Sure, a firm’s portfolio might be front and centre of their advertising, but independent reviews from clients are the real deal. They tell the story of what homeowners have actually gone through – almost like receiving a free audit without actually dipping in your own toes.

What’s more, you won’t have to dig deep to find reviews of your shortlisted renovation firms. Head over to Facebook, Google Reviews, or renovation portals to see what past customers have to say about their experiences, and you’ll have kickstarted your own renovation journey on the right foot.

A true, anonymised tale of a home renovation gone wrong:

One homeowner shared that they had engaged a renovation firm after being drawn to their portfolio, and they were assigned to Ryan (not his real name), who was a designer. At first, the process seemed smooth. However, once work began, Ryan requested that a portion of the renovation cost be transferred via PayNow directly into his personal account.

Finding this suspicious, the homeowner reached out to the firm’s management for clarification. Despite this, Ryan continued to pressure them, insisting that he would pay the company on their behalf if they transferred the funds to him. When the homeowner voiced their discomfort, Ryan produced a receipt, which later turned out to be fake. Unfortunately, the homeowner fell for the scheme and made the payment.

According to the homeowner, the company’s management was not particularly helpful either. They discouraged filing a police report, saying the matter would be settled internally. Although the issue was eventually resolved, the process was drawn out and highly stressful. In hindsight, the homeowner also admitted that they should have paid attention to the firms’ many negative reviews online.

2. Opt for a reliable interior designer (if you prefer a more hands-off renovation)

For many first-time homeowners, one common question that frequently pops up is whether to work with a contractor or an interior designer. While each comes with its own pros and cons, the final decision often boils down to this: would you prefer to play a more active, hands-on role in project management, or leave all of your renovation matters in the hands of an expert?

Hiring a contractor for your renovation is much like engaging a freelancer – you could get quality work for your money, but you’ll also need to take charge of the entire process from start to finish. That means getting hands-on with sourcing furniture and accessories, or even working out the right measurements for customised fixtures.

On the other hand, hiring a trustworthy interior designer may cost more, but they’ll take care of all the heavy lifting and nitty-gritty details necessary to bring your dream home to life. Or put differently, you won’t find yourself grappling with renovation technicalities or project timelines, while juggling work and family matters at the same time.

A true, anonymised tale of a home renovation gone wrong:

Choosing familiarity over formality, a couple decided to hire a contractor who was also a family friend instead of engaging an interior designer. But this choice proved to be a mistake.

The contractor frequently proposed cookie-cutter designs, to the point where the couple had to come up with ideas on their own. They also found themselves having to provide very detailed instructions. For instance, the contractor installed bathroom doors without locks, which the couple felt should have been common sense. Moreover, they had to source for the locks themselves.

Finally, because the contractor was a family friend, the couple found it difficult to be completely honest about their dissatisfaction, as they did not want to strain the friendship.

3. Be wary of promises that are too good to be true

As the age-old adage goes: “If it’s too good to be true, it usually is”. More often than not, the (sometimes false) promise of a good discount or a shorter timeline might sound great on paper, but in reality, home renovations aren’t entirely straightforward – and that’s even with the most thorough preparations made beforehand.

Unforeseen delays, material shortages, or on-site complications can sometimes occur, and they’ll throw a wrench into even the most well-laid plans. Hence, even with careful planning, it’s always wise to buffer in some additional time and money. And even more importantly, make sure to manage your expectations and not fall for sugar-coated claims.

A true, anonymised tale of a home renovation gone wrong:

Faced with a choice between two interior designers, a couple opted for the one that promised a quicker turnaround. He had assured them that the renovation could be completed in December 2024, just one month after their key collection date. Though the couple initially found the timeline questionable, they still decided to proceed.

Eventually, problems arose with the designer, who cited sudden weddings or sick family members as reasons for missed appointments. On one occasion, the couple was scheduled to view fittings in Johor, but was cancelled on at the last minute.

Workmanship was also subpar, and the renovation ultimately stretched over a period of three months. Thankfully, living temporarily at a relative’s place allowed the couple to accommodate the delays without major disruption to their plans.

Still, they regret their decision and would not recommend their designer in the slightest.

4. The right designer for one homeowner might not be the right one for you

Beyond careful planning and budgeting, what lies at the heart of any successful renovation project is chemistry. Finding the right interior designer isn’t just about their awards or portfolios, it’s also about whether their aesthetic sense aligns with yours. Equally important is whether their working and communication style supports a healthy client-designer relationship.

For instance, a designer who excels in masculine industrial-style interiors may struggle to capture the essence of your desired Hello Kitty-themed home. Likewise, a designer who is extremely meticulous and provides constant updates might feel overwhelming to a homeowner who prefers a more hands-off approach to their renovation.

So rather than going by word of mouth or simply trusting referrals from friends and family, why not take the time to get to know your shortlisted interior designers? That way, you can ensure the people overseeing your renovation are partners in building your dream home – rather than the cause of an unwanted nightmare.

A true, anonymised tale of a home renovation gone wrong:

After researching and consulting a few interior designers, a couple decided to work with the same designer whom their family had worked with previously.

However, they encountered numerous issues, with the most annoying being the lack of site management. The designer rarely provided timely updates unless prompted, did not accompany them to purchase fixtures, and failed to offer recommendations suited to the theme they wanted.

The couple found this baffling, given the great experience reported by their family member. They noted that while many homeowners online describe having good chemistry with their designers, they did not experience the same with theirs.

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.

Change is coming. Earlier this year, the Urban Redevelopment Authority (URA) announced its Draft Master Plan for 2025, which outlines Singapore’s land use and development over the medium term. As it takes shape, we’ll witness the rollout of new housing neighbourhoods, commercial centres, as well as meaningful efforts to preserve our environment, nature, and heritage.

But beyond shaping the built and natural environments of Singapore, how else will the Draft Master Plan 2025 set the stage for future development?

What is the Master Plan? And what’s new in the 2025 Draft Master Plan?

Over the decades, Singapore’s land use has been shaped by six finalised Master Plans released every five years from 1958 to 2019. The latest Draft Master Plan 2025 – along with its eventual finalised version – will continue this tradition with forward-looking strategies pursuing further urban development.

Among these strategies is Singapore’s long-term push for decentralisation, which was first set in motion through the 1991 Concept Plan. Since then, this approach of developing regional nodes has shaped our nation’s development, paving the way for areas like Tampines, Changi, Jurong, Woodlands and Punggol to emerge as business hubs.

Source: ERA Research and Market Intelligence

More importantly, however, is the role of decentralisation in shaping the interplay between the three building blocks of Singapore’s economic growth: housing, infrastructure, and jobs.

As more new housing estates are built outside the city core, outlying neighbourhoods gain the capacity to support larger populations. This growth necessitates the creation of new infrastructure, such as transport networks, commercial spaces – or even specialised office centres or industrial parks. In turn, these amenities lay the groundwork for businesses to take root, thereby expanding Singapore’s industries and promoting job creation.

Over three decades later, this effective focus on decentralisation remains central to the expansion of Singapore’s business ecosystem and its residential areas. Similarly, the Draft Master Plan 2025 remains grounded in the urban planning strategies and collaborative approach that informed Singapore’s early development, even amidst a shifting global political-economic landscape.

This continuity is evident in the four key themes underpinning the Draft Master Plan 2025:

- Creating more well-connected homes and residential precincts across the island

- Enabling sustainable growth that supports the evolving needs of our nation, businesses, and workers in an open economy

- Safeguarding a liveable future by guarding against climate change and optimising land use

- Celebrating our built heritage and enhancing familiar places

Curious about what these themes mean in practice? We’ve put together a quick guide summarising all the key highlights below.

More homes and new neighbourhoods being built

With more than 80% of Singapore’s residents living in HDB flats, it’s no exaggeration to say that housing is at the heart of our nation’s urban planning. As outlined in the Draft Master Plan 2025, the next phase of growth will see new neighbourhoods being introduced as part of a greater push towards a more liveable, decentralised Singapore.

These fresh communities will comprise of both public and private residential estates designed with convenience and connectivity in mind. Following earlier announcements for new neighbourhoods at Bukit Timah Turf City, Pearl’s Hill, Marina South, Mount Pleasant, and the former Keppel Golf Course, we’ll see the next wave of housing at:

- Dover-Medway (Greater one-north)

- Former Singapore Racecourse (Kranji)

- Newton, Paterson (Orchard Road)

- Paya Lebar Air Base

- Sembawang Shipyard

Dover-Medway (Greater one-north)

Source: URA, ERA Research and Market Intelligence

As part the Greater one-north knowledge hub, the future Dover-Medway neighbourhood could see as many as 6,000 new homes being built in the area. This incoming supply of public and private housing will be sited east of one-north and Kent Ridge MRT stations, with preparatory steps toward future development expected to commence later this year.

Former Singapore Racecourse (Kranji)

Source: URA, ERA Research and Market Intelligence

Further up in the northern region, the former Singapore Racecourse could receive a new lease of life with its potential transformation into a residential estate. If it comes to fruition, this redevelopment could bring around 14,000 new public and private homes to the area, significantly boosting future housing supply.

In addition to the rare opportunity of living at nature’s doorstep, future residents may also see new amenities being introduced nearby. These include a possible new neighbourhood centre beside Kranji MRT station, as well as fresh leisure and sports offerings.

Newton, Paterson (Orchard Road)

Source: URA, ERA Research and Market Intelligence

Within Singapore’s central core, more residential options could be on the horizon for Newton and Orchard. These expanded offerings – potentially comprising up to 5,000 new private homes in Newton and 1,000 in Orchard – will give Singapore residents more opportunities to live closer to the city centre.

In Newton, three clusters at Newton Circus, Scotts Road and Monk’s Hill are being developed as part of a new neighbourhood.

Meanwhile, plans are underway to reshape the Paterson neighbourhood into a vibrant mixed-use hub via the construction of a new integrated development. Sited right above Orchard MRT station, this future landmark will comprise of retail, office, and residential components, and it will also complement ongoing initiatives like the Strategic Development Incentive (SDI) scheme in breathing new life into the area.

Paya Lebar Air Base

Source: URA, ERA Research and Market Intelligence

Over the next decade, Paya Lebar Air Base (PLAB) will be relocated from its current location in eastern Singapore, with a new township taking its place. This opens up 800ha of land for residential development where a future-ready housing estate will take root alongside brand-new offices and car-free commuter routes.

Presently, development linked to Paya Lebar Air Base (PLAB) has begun, with the first phase commencing at the adjoining Defu industrial estate in Hougang. Originally built in the 1970s to support small and medium-sized enterprises, Defu will be transformed into a ‘10-minute neighbourhood’, putting residents within walking or cycling distance of essential amenities.

Sembawang Shipyard

Source: URA, ERA Research and Market Intelligence

As part of broader efforts to reshape northern Singapore, the North Coast Innovation Corridor was announced in 2013 with the aim of establishing a new commercial belt stretching from Woodlands to Punggol. And with the release of the Draft Master Plan 2025, the redevelopment of Sembawang Shipyard into a housing estate marks the latest step of this ongoing transformation.

By 2028, shipping operations at Sembawang will cease, this will create space for a mixed-use waterfront district with maritime-themed housing estates as a nod to the town’s past.

Enabling sustainable growth with new business nodes

Since the early 1990s, Singapore has pursued a decentralisation strategy that aims to bring jobs further from the city centre and closer to homes.

Alongside the Draft Master Plan 2025, existing economic corridors in the North (North Coast Innovation Corridor), East (Changi Airport and Changi Business Park), and West (Jurong Lake District, Jurong Innovation District, and Tuas Port) will continue to grow as key employment and innovation hubs.

These established nodes will soon be complemented by Bishan in its new identity as a sub-regional centre, as well as the transformation of Jurong Bird Park and Jurong Hill into workplaces of the future.

Bishan sub-regional centre

Since its establishment as a town centre in the early 1980s, Bishan has matured into one of Singapore’s most sought-after residential estates. This is mainly due to a combination of desirable characteristics: its central location, robust transport links, and access to quality amenities over the years.

Under the Draft Master Plan 2025, Bishan’s appeal is set to grow further with its redevelopment into a sub-regional centre where business opportunities and lifestyle offerings meet. New additions that have been revealed thus far include brand-new office towers, a polyclinic, as well as a pedestrian mall connecting future developments and facilities in Bishan. Likewise, a hawker centre and an air-conditioned bus interchange could be in Bishan’s future, with plans for these amenities currently under study.

Jurong Bird Park and Jurong Hill

When the Jurong Lake District was first announced in 2017, it marked the start of Jurong’s journey to becoming Singapore’s Western Gateway. Now, this transformation continues with the Draft Master Plan 2025 unveiling plans for a new 39.2-hectare industrial estate on the former sites of Jurong Bird Park and Jurong Hill Park.

Laying the groundwork for this next chapter are the relocation of Jurong Bird Park in 2023 and the anticipated opening of the Jurong Region Line by 2029. Together, these developments will enhance capacity and connectivity, supporting new business activities at the upcoming industrial estate.

Safeguarding our environment, nature and heritage

Though the Draft Master Plan 2025 primarily focuses on developing Singapore’s built environment, it also takes significant steps to strengthen protections for our environment, nature, and heritage. This balanced approach introduces several key initiatives to ensure sustainable growth, while also preserving the unique identity and biodiversity that define our nation:

- ‘Long Island’ Plan: Approximately 800 ha of land will be reclaimed off the East Coast; this will strengthen our flood resilience, while also creating a new reservoir and additional land for future development needs.

- Kranji Nature Corridor: Intended to strengthen ecological networks in the North, the Kranji Nature Corridor connects the Mandai Mangrove and Mudflat Nature Park with the Central Catchment Nature Reserve. This linkage will facilitate the safe passage of wildlife across these green spaces, hence contributing to the preservation efforts.

- Conservation of Heritage Buildings: Key historical structures are preserved as tangible reminders of Singapore’s foundational pillars in economy, housing, social development, and defence. Notable examples highlighted in the Draft Master Plan 2025 include the NatSteel Steel Pavilion, Pasir Panjang English School, and the Bukit Timah Turf City buildings.

- Establishment of New Identity Nodes: Under the Draft Master Plan 2025, three new identity nodes will be created at Siglap, Moonstone Lane Estate, and Newton. Together, they will serve as cultural focal points celebrating our local heritage and shared Singaporean identity.

- Further Possibilities with Underground Spaces: R&D efforts are underway to expand the use of Singapore’s underground real estate beyond current functions like storing construction materials at Gali Batu; this could free up more surface land for urban development in years to come.

Is Singapore ready for the future with URA’s Master Plan 2025?

As Singapore turns 60 this year, our nation stands at a pivotal point where nurturing future growth must be balanced with preserving our roots. The Draft Master Plan 2025 reflects this reality as it lays the groundwork for future urban transformation across our island home, while also ensuring that Singapore remains a liveable city abundant in greenery and character.

So, to answer the question – Singapore is indeed ready for the future, but this readiness hinges on joint collaboration between our government, businesses, and fellow Singaporeans. This collectiveness will be vital for not just the finalised Master Plan 2025, but for every initiative that will drive Singapore forward over the next 60 years and beyond.

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.

In a city where vertical living is the norm rather than the exception, Springleaf has long stood out as a low-rise enclave characterised by landed homes and abundant greenery. However, change is on the horizon. With the Government’s release of two land plots – Upper Thomson Road (Parcel A) and Upper Thomson Road (Parcel B) – Springleaf is set to welcome its first-ever high-rise developments.

Upper Thomson Road (Parcel A) situated near Springleaf MRT station (Source: URA, ERA Research and Market Intelligence)

Of the two, Parcel A will feature a mixed-use development with both commercial and residential components, while Parcel B is zoned exclusively for residential use. Parcel B has been successfully tendered by veteran developers Guocoland Singapore and Hong Leong Holdings as of April last year, while the tender for Parcel A is set to close later this October.

The launch of both sites marks the beginning of a new chapter in Springleaf’s development. But before any new projects unfold, it’s worth asking: how will this former ‘landed-only’ neighbourhood evolve?

A brief history of Springleaf Precinct

Source: URA, ERA Research and Market Intelligence

In 2022, the Urban Redevelopment Authority (URA) announced plans to develop a 33-hectare area of Springleaf as part of Singapore’s long-term land use strategy. Bounded by Seletar Expressway, Mandai Road, and Upper Thomson Road, this designated site includes the Upper Thomson Road parcels mentioned above, as well as several heritage buildings, while the remainder consists of forested ecological zones designated for “Park” use.

This abundant greenery also makes Springleaf a rare refuge from Singapore’s intense city life, which also allows its landed communities to live closer to nature without giving up on everyday conveniences.

Source: ERA Research and Market Intelligence

Looking further back into history, Springleaf’s current identity as a landed residential enclave reflects its origins as a small settlement within Nee Soon Village, which once functioned as a commercial hub for Singapore’s gambier and pepper trade.

However, with the launch of the Yishun New Town project in 1976, residents of Nee Soon Village were gradually moved to other nearby housing areas as the entire precinct underwent urbanisation.

The original Nee Soon Post Office building (Source: ERA Research and Market Intelligence)

Former Seletar Institute compound located within Upper Thomson Road Parcel B (Source: ERA Research and Market Intelligence)

This reimagining of Nee Soon Village in the 70s introduced two key community amenities to the area: Nee Soon Post Office and Seletar Institute (originally Upper Thomson Secondary School).

Nee Soon Post Office operated from a distinctive two-storey colonial building that still stands today at the junction of Mandai Road, Sembawang Road, and Upper Thomson Road. Similarly, Seletar Institute remains preserved within the boundaries of Upper Thomson Road (Parcel B), even as new construction begins around it.

Furthermore, both buildings have been recognised by URA as built heritage landmarks. Consequently, developers will be tasked with a unique conservation responsibility of ensuring that these historic structures are thoughtfully incorporated into future projects.

Preserving Springleaf’s natural biodiversity

Waterways at Springleaf Nature Park (Source: ERA Research and Market Intelligence)

Beyond its built heritage, Springleaf’s unique character also arises from its closeness to several notable green spaces.

Just past the Seletar Expressway, to the west of both Upper Thomson Road parcels, lies the Central Catchment Nature Reserve (CCNR). As Singapore’s largest nature reserve and an essential green lung, the CCNR covers approximately 2,800 hectares and features notable wildlife attractions such as the Singapore Zoo, Night Safari, and River Safari – all of which highlight its extensive footprint.

The treeline of Springleaf Forest bordering Upper Thomson Road (Parcel A) and Springleaf MRT Station (Source: ERA Research and Market Intelligence)

Closer to the Upper Thomson Road sites is Springleaf Forest, where Sungei Seletar flows through. Although smaller in size, this patch of greenery plays a crucial role in providing a natural buffer and connectivity for the CCNR. For future residents, the preservation of Springleaf Forest helps create a more pleasant living environment and offers the potential for unblocked views of the surrounding greenery.

Previous environmental studies commissioned by the URA have also revealed that Springleaf Forest hosts a diverse range of native flora and fauna. This includes wildlife of conservation importance, such as various species of pangolins and otters.

Source: ERA Research and Market Intelligence

Recognising this ecological significance, the National Parks Board proposed in 2022 to establish Nee Soon Nature Park within Springleaf Forest; this supplements existing green pathways and natural leisure spaces, including the nearby Springleaf Nature Park.

These conservation efforts will also align with the adoption of nature-sensitive design and development practices in upcoming residential projects along Upper Thomson Road.

Some examples of these eco-friendly approaches include adding greener facades to prevent bird collisions and minimising ecological impact by limiting new developments to ‘disturbed ground’ or areas that have previously been developed. Similarly, construction will be carried out in phases to lessen disturbance to the environment and enable progressive monitoring of potential impacts.

Infrastructure and amenities at Springleaf

Source: ERA Research and Market Intelligence

Although Springleaf is best known for its tranquil setting, it is by no means short on amenities for convenient everyday living. For instance, just like the nearby Lentor precinct, Springleaf is served by a dedicated MRT station on the Thomson-East Coast Line (TEL).

Since opening as part of TEL Phase 2 in 2021, Springleaf Station has proven to be a connectivity game-changer for residents living in nearby landed estates, providing links to key destinations such as Caldecott Interchange (which also sits on the Circle Line), as well as central city stops like Orchard and Great World.

Such accessibility will further improve with the upcoming completion of the fifth stage of the TEL; this final phase will see MRT services extended beyond Bayshore to Bedok South and Sungei Bedok, where an interchange with the Downtown Line will further enhance travelling convenience.

Source: ERA Research and Market Intelligence

Source: ERA Research and Market Intelligence

Beyond improving transport accessibility, Springleaf MRT station also serves as a neighbourhood corridor that provides commuters with sheltered access to both sides of Upper Thomson Road. This is especially beneficial for visitors and Springleaf residents who frequent the line of shophouse businesses located just across the previously mentioned development plots.

Mainly composed of eateries, these long-established establishments provide a variety of culinary options – from Yong Tau Foo speciality stalls to Korean Barbeque, and of course, the ever-popular Springleaf Prata. Also included are several small grocery shops and convenience stores like 7-Eleven, which supply daily essentials to the neighbourhood.

For larger shopping trips or a broader selection of groceries, residents can travel beyond Springleaf to malls such as Thomson Plaza and Causeway Point – both of which are a short drive or MRT ride away at Upper Thomson and Woodlands, respectively.

Unpacking the potential of Springleaf’s residential properties

Despite its tranquil, low-density character, Springleaf maintains strong property potential as it is part of District 26 (Upper Thomson/Mandai), which has experienced noticeable appreciation in resale prices for non-landed private homes over the past decade.

Chart 1: Median unit prices for non-landed private properties (excluding ECs) in District 26

Source: URA, ERA Research and Market Intelligence

Between 2015 and the first seven months of 2025, median unit prices for resale non-landed private properties in District 26 increased by 52.5%, rising from $929 psf to $1,417 psf. This consistent growth highlights the long-term potential of District 26, a benefit that Springleaf’s future developments might capitalise on.

Looking beyond price appreciation, there are other factors that may also influence the success of the projects at Upper Thomson Road Parcel A and B. Most notably, future buyers of homes at both sites will benefit from a first-mover advantage, as they will be the pioneering non-landed residential plots in the Springleaf precinct and are also the closest to Springleaf MRT station.

Residential plots on both sides of Seletar Expressway (Source: URA, ERA Research and Market Intelligence)

Moreover, this benefit could extend beyond the immediate vicinity of Springleaf’s existing residential estates. According to zoning designations under the latest URA Master Plan, there are two additional sizeable plots for residential use on both sides of the Seletar Expressway; this increases the likelihood of the first-mover advantage applying to an even larger area as future development progresses.

So, what’s next for the Springleaf precinct?

Springleaf Residence (Source: Guocoland Singapore and Hong Leong Holdings)

Following the successful tender of Upper Thomson Road (Parcel B), Springleaf is poised to welcome its first-ever condominium homes. Developed by Guocoland Singapore and Hong Leong Holdings, the project is scheduled to launch in August 2025, offering 941 units in an appealing location that combines natural beauty with contemporary living.

Offering 1- to 5-bedroom layouts, homes at Springleaf Residence will be part of a thoughtfully designed development amidst preserved heritage features and lush greenery. Consequently, these residences provide a rare chance to live within an iconic enclave that maintains its peaceful character, even as new developments emerge.

Lastly, Springleaf’s enduring charm reminds us that a neighbourhood’s liveability does not always rely on having a shopping mall or a busy town centre. Sometimes, all that is needed is plenty of greenery, good public transport links, thoughtful urban planning – and perhaps, a great prata spot nearby.

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.

As of late May this year, fresh news has emerged that the Singapore Government might consider reviewing or even removing the 15-month wait-out period imposed on private property right-sizers who want to purchase a resale HDB flat.

During a recent visit to the Toa Payoh Ridge Build-to-Order (BTO) project, newly-appointed Minister for National Development Chee Hong Tat told reporters that the authorities would be open to the idea of a rule change “when the situation improves and resale flat prices begin to moderate.”

The 15-month wait-out period was first introduced as a temporary cooling measure in September 2022, aiming to curb demand from private property right-sizers amid rising resale HDB prices. Since then, the HDB Resale Price Index (RPI) has recorded a slower 1.6% quarterly growth in the first quarter of 2025, which Minister Chee pointed out as a possible sign of moderation.

Looking further ahead, the possibility of removing the 15-month wait-out period raises several questions: What could happen to the HDB resale market next? Is the rule still relevant in today’s market? Below, we share some thoughts on these matters.

But first, how did the resale HDB market adjust after the 15-month wait-out period was implemented?

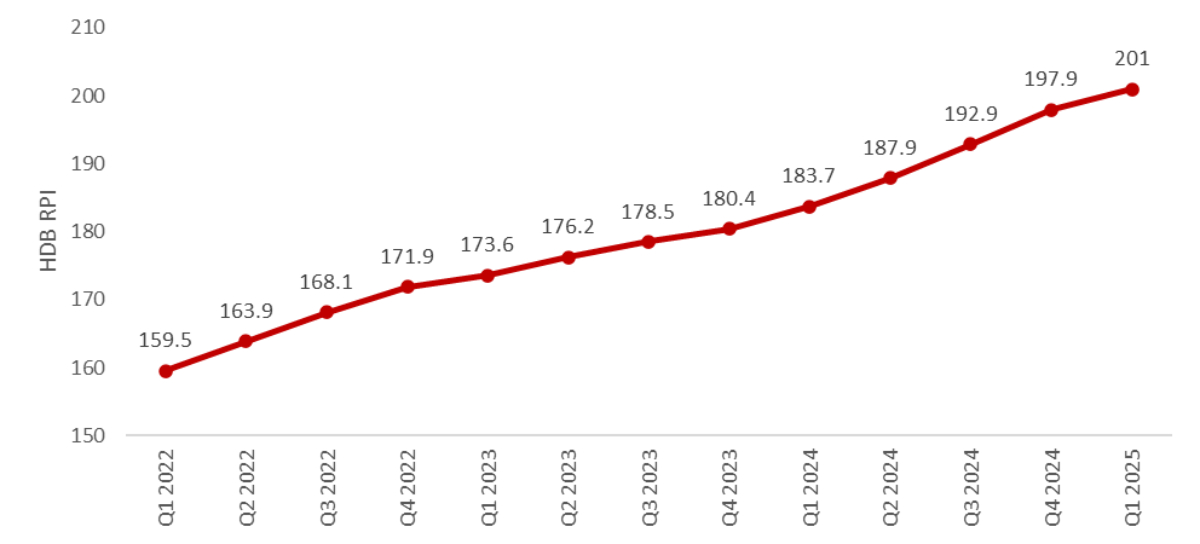

Chart 1: HDB Resale Price Index from 1Q 2023 to 1Q 2025

Source: HDB, ERA Research and Market Intelligence

When examining movements in the HDB RPI after the 15-month wait-out period was implemented in 3Q 2022, it is clear that the rule had a noticeable effect on the secondary market. Although the HDB RPI continued to rise from 168.1 in 3Q 2022 to 173.6 in 1Q 2023, its rate of growth slowed markedly, with quarterly gains shrinking sharply from 2.6% to just 1.0% over the course of six months.

The accompanying decline in resale HDB transaction volumes – from 7,546 to 6,979 units – further supports the notion that the wait-out period had a moderating effect on flat demand from private property right-sizers during this period.

Table 1: HDB Resale Price Index and transaction volume by quarter

Source: HDB, ERA Research and Market Intelligence

However, after the initial 15-month period following the introduction of the wait-out period in September 2022, eligible private property right-sizers were once again permitted to re-enter the secondary HDB market.

This influx of buyers resulted in a noticeable resurgence in both transaction volume and price growth of resale HDB flats. In 1Q 2024, resale transactions increased to 7,068 units, while the HDB RPI recorded a 1.8% q-o-q increase – the steepest quarterly price growth noted since 1Q 2023.

Subsequently, in 2Q 2024, the HDB RPI experienced a further quarterly increase of 2.3%. This is close to the 2.6% q-o-q jump recorded in 3Q 2022, just before the implementation of the wait-out rule.

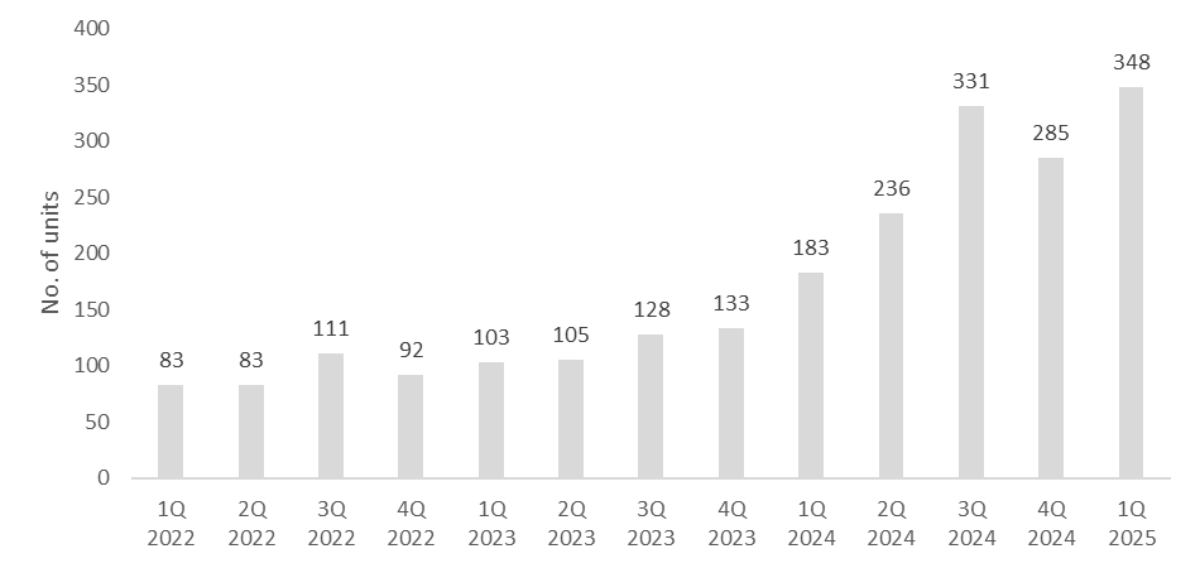

Chart 2: Volume of million-dollar HDB flats by quarter

Source: data.gov.sg, ERA Research and Market Intelligence

This rebound pattern was also mirrored in the number of million-dollar HDB flat transactions – another useful yardstick for assessing the wait-out period’s effectiveness in tempering the resale market.

Following the rule’s introduction, million-dollar flat transactions fell from 111 units in 3Q 2022 to 92 units in 4Q 2022 before staying stable for most of the subsequent quarters.

However, this trend reversed direction over a year later. 1Q 2024 saw the biggest surge in the number of million-dollar flats sold in a quarter, with 183 such transactions—or double the 92 units recorded in 4Q 2022.

This surge in million-dollar HDB resale transactions shows little signs of slowing. As of May 2025, the year-to-date number of million-dollar resale transactions stands at 254 units for 4-room flats and 368 for 5-room flats. This is a notable increase compared to a year ago, with 4-room and 5-room units accounting for 93 and 229 transactions, respectively, from January to May 2024.

Overall, these ongoing increases in both million-dollar HDB flats and general resale prices present a sobering picture: the wait-out period likely experienced peak effectiveness only during its initial 15-month window.

What could happen to the HDB resale market if the 15-month wait-out period is removed?

With the resale HDB market already witnessing a growing number of million-dollar flats, there is little justification for removing the 15-month wait-out period. Doing so would spark a renewed surge in resale HDB prices, thus undermining the rule’s original purpose of keeping the secondary market in check.

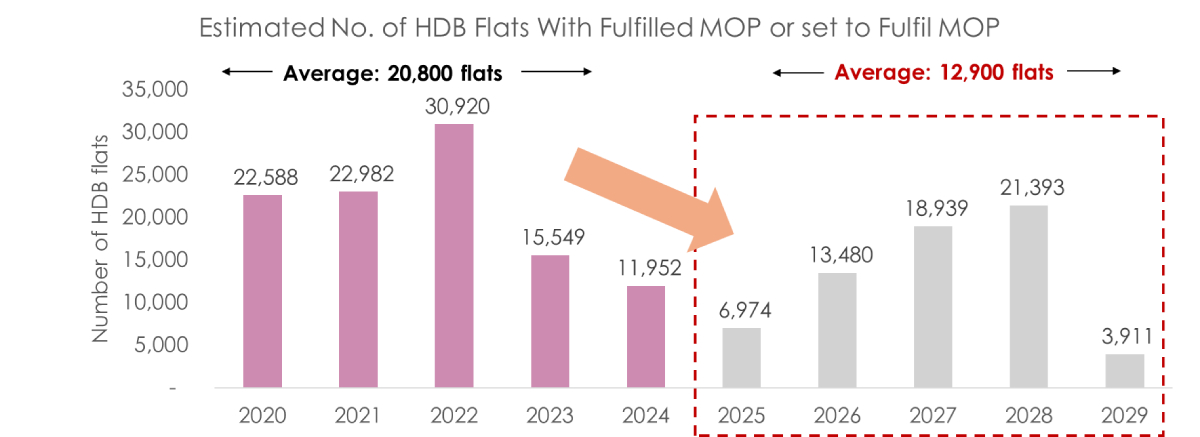

Chart 3: Estimated volume of HDB flats that have met or will meet their MOP

Source: HDB, ERA Research and Market Intelligence

Market demand has also outpaced the available supply of HDB flats fresh out of their 5-year Minimum Occupation Period (MOP), leading to more intense competition in the secondary HDB market. This trend coincides with a shrinking number of HDB flats exiting their MOP, which has been steadily declining since 2022.

In 2022, 30,920 flats were estimated to have reached the end of their MOP, but this is expected to fall to a significant low of 6,974 units in 2025. Such a steep step-down in fresh resale inventory will likely exacerbate scarcity and existing price pressures, especially as demand from upgraders and right-sizers remains firm within the secondary HDB market.

At the same time, a growing bifurcation is emerging in the resale market where recently MOP-ed flats in desirable locations are seeing faster price appreciation than their older counterparts. For instance, in popular towns near the city fringe (e.g. Toa Payoh, Central Area), it is possible to see newer 4-room resale flats commanding double the price of older flats of equal size.

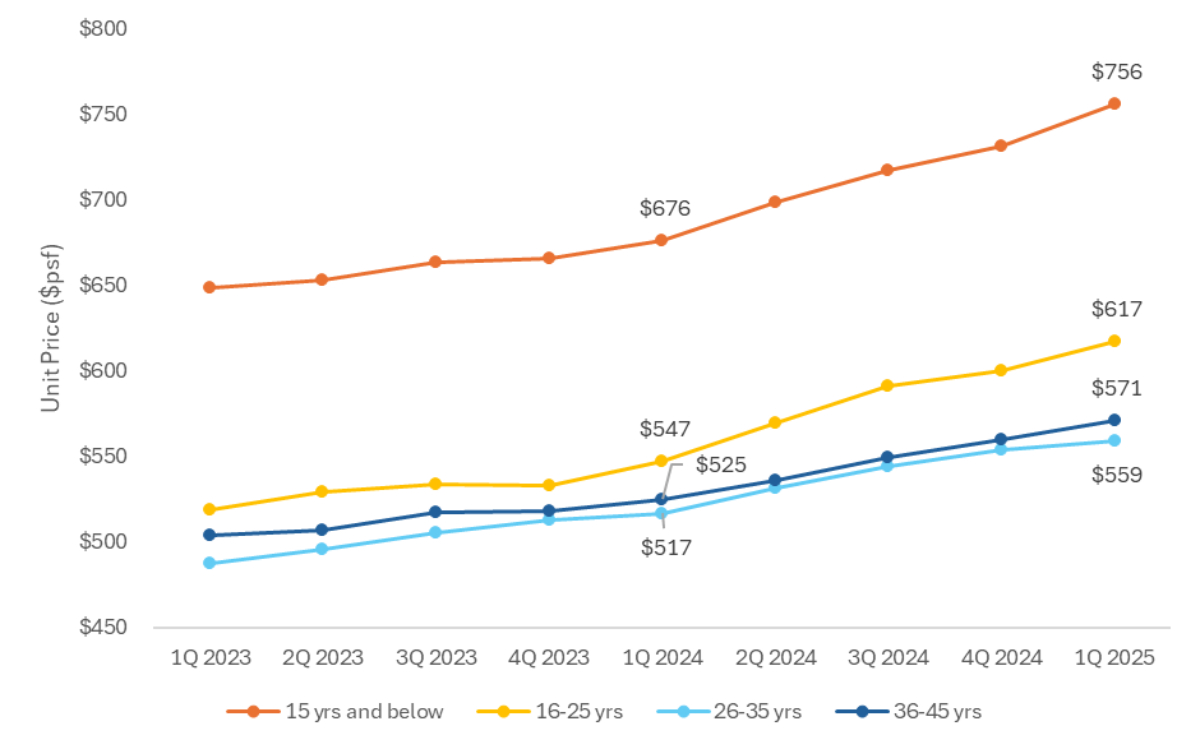

Table 2: Unit price appreciation of ‘younger’ and ‘older’ HDB flats up to 1Q 2025

Source: HDB, ERA Research and Market Intelligence

This gap is further accentuated when looking at the annual price growth of HDB resale flats across different age brackets. Based on a year-on-year comparison of average unit prices as of 1Q 2025, younger resale flats aged “15 years and below” and “16 to 25 years” recorded sharper gains, with growth rates of 11.8% ($676 psf to $756 psf) and 12.8% ($547 psf to $617 psf) respectively.

In contrast, older flats in the “26 to 35 years” and “36 to 45 years” categories saw gentler growth, with unit prices rising by 8.2% ($525 psf to $571 psf) and 8.8% ($517 psf to $559 psf) on the year.

In turn, these divergences in pricing and appreciation rates between newer and older HDB flats is likely due to growing homebuyer awareness about lease decay concerns, leading them to opt for newer units even at a premium. This preference is also anticipated to sustain steady price appreciation in the secondary market, even with the slower gains of older flats moderating the appreciation of newly MOP-ed ones.

So, does the 15-month wait-out period still make sense in today’s context?

While its effectiveness has likely waned, the 15-month wait-out period remains relevant for moderating buying activity and keeping resale HDB prices in check. This perspective is warranted as private homeowners will represent a continuous pool for right-sizing and subsequent demand, even with the wait-out period in effect.

In light of current economic uncertainty, there might be a case for increased flexibility. For instance, the Government could consider implementing buying stipulations for private property right-sizers based on lease tenure. In turn, this would involve restricting HDB purchases by said right-sizers to units with shorter remaining leases.

Such a measure could be a potential solution as it would give private homeowners below the age of 55 the opportunity to secure a replacement home without having to complete the wait-out period. But at the same time, this would prevent HDB resale flat prices from rising too sharply as right-sizer demand would be channelled towards older homes with more moderated price growth, rather than recently MOP-ed flats that typically experience faster appreciation.

Addressing resale market pressures will also require meaningful supply-side intervention. For instance, efforts to deliver Build-To-Order (BTO) flats with shorter waiting periods could effectively divert first-timer demand towards the BTO market and away from the resale segment.

When combined with a refined wait-out policy, such housing supply measures should hopefully provide the necessary breathing room for the resale HDB market to maintain stable and sustainable growth in the long term.

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.

From choosing an HDB or bank loan to deciding between a new launch or a resale unit, today’s homebuyers have no shortage of important decisions to make. Likewise, choosing between a freehold and leasehold property is another key consideration, given the potential bearing on investment yields.

This is due to the unique advantages that freehold and leasehold properties present as investments. Freehold residential properties can be held indefinitely without any expiry date on their lease, allowing owners to retain them as long-term wealth-building assets. Conversely, while leasehold properties offer ownership for a limited period, they often come with lower entry prices that upgraders may find more appealing.

Beyond these distinctions, there is also a common perception that freehold condominiums represent the best option for homebuyers due to their lifetime tenure. However, this belief may not hold true for everyone – particularly homebuyers targeting a medium-term investment window of 4 to 6 years.

In relation to this, a comparative study by ERA Singapore observed that leasehold condominiums are steadily closing the historical profitability gap with freehold homes, driven by the increasing returns of 99-year properties during the aforementioned medium-term holding period.

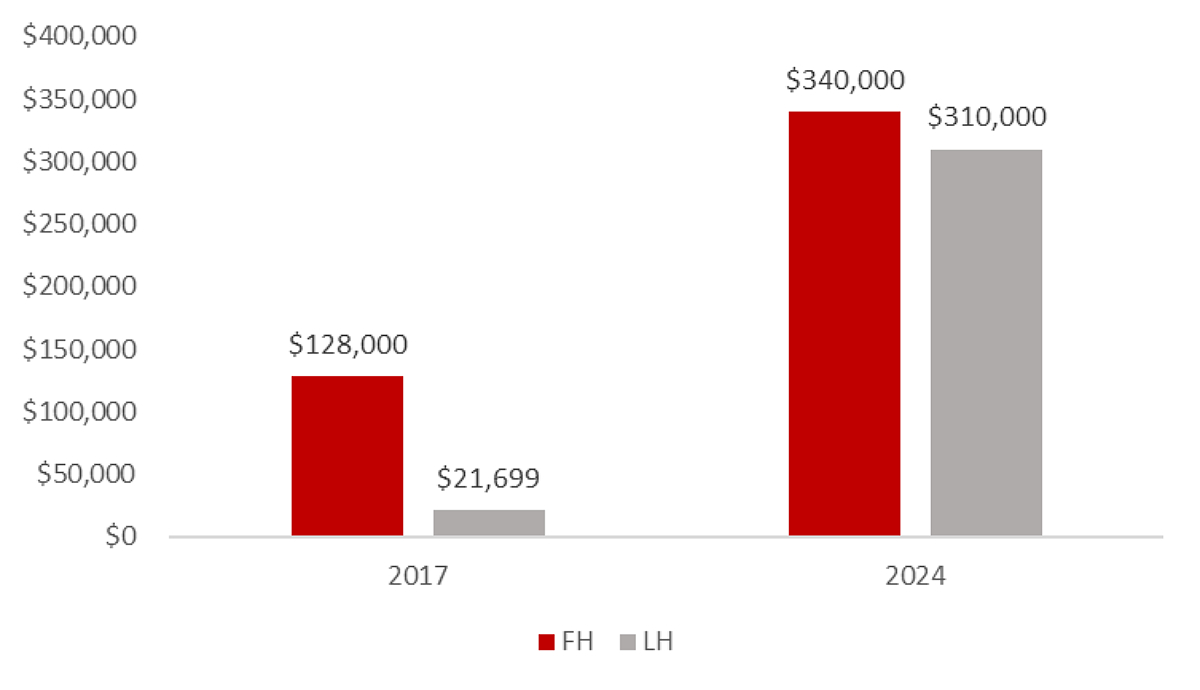

Chart 1: Median profits of freehold and leasehold residential properties within 2km of selected MRT stations (2017 and 2024)

Source: URA, ERA Research and Market Intelligence

In 2017, sampled freehold developments located within 2km of selected MRT stations posted a median profit that was 5.9 times higher than their leasehold counterparts. By 2024, this same figure had fallen to 1.1 times, thus reflecting a shrinking gap in profitability.

But what exactly is driving this growing trend? And how might it influence your next homebuying decisions? For more answers and insights, keep scrolling!

Just how close is the median profitability gap between leasehold and freehold condominiums?

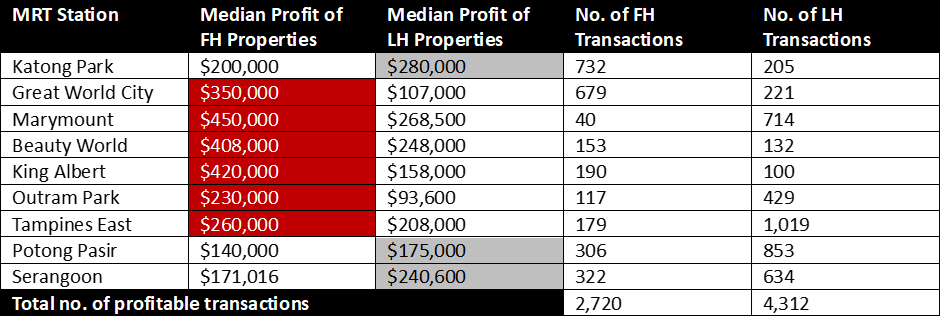

To delve deeper into the profitability gap between leasehold and freehold condominiums, we analysed caveat data from non-landed private residential developments within a 2km radius of nine selected MRT stations, focusing on units bought and sold over a ten-year period from 2015 to 2024.

A 2km radius was also chosen to determine which of the selected MRT stations influenced the profitability of developments across a wider neighbourhood rather than only those in the immediate vicinity. This contrasts a 1km radius, which is a better measure for examining how proximity to an MRT station affects profitability.

The selected MRT stations include: 1) Katong Park, 2) Great World, 3) Marymount, 4) Beauty World, 5) King Albert Park, 6) Outram Park, 7) Tampines East, 8) Potong Pasir, and 9) Serangoon.

The study covered 765 condominium developments, excluding Executive Condominiums. 617 have freehold tenure (including projects with leases exceeding 900 years), while the remaining 148 are leasehold developments.

Furthermore, to ensure a meaningful comparison, only developments with at least 30 transactions during the 10-year period from 2015 to 2024 were included in the analysis.

This methodology yielded 7,032 profitable secondary market transactions for further analysis. The leasehold and freehold properties involved in these transactions had median holding periods of approximately 4 to 6 years, aligning with the medium-term investment window.

Additionally, projects located between two MRT stations were assigned to the closest station for analysis. And finally, profitability was calculated based on the net difference between buying and selling prices – this excludes common administrative costs, such as stamp duties and legal fees.

By applying these criteria and analysing relevant transaction data, we uncovered the following insights:

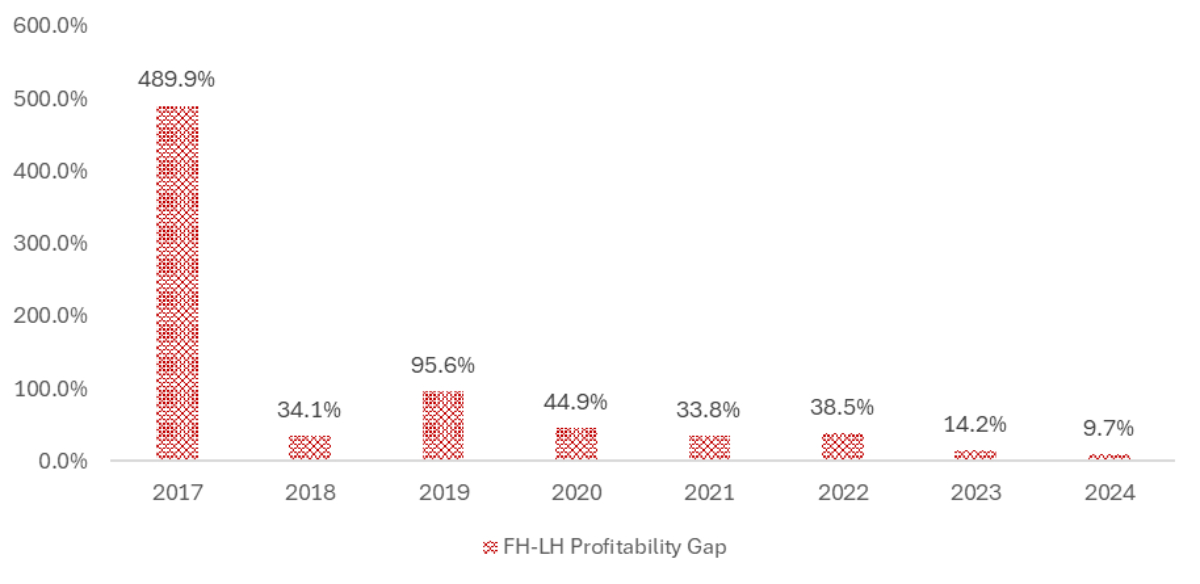

1. The profitability gap between leasehold and freehold properties has been narrowing at a growing pace

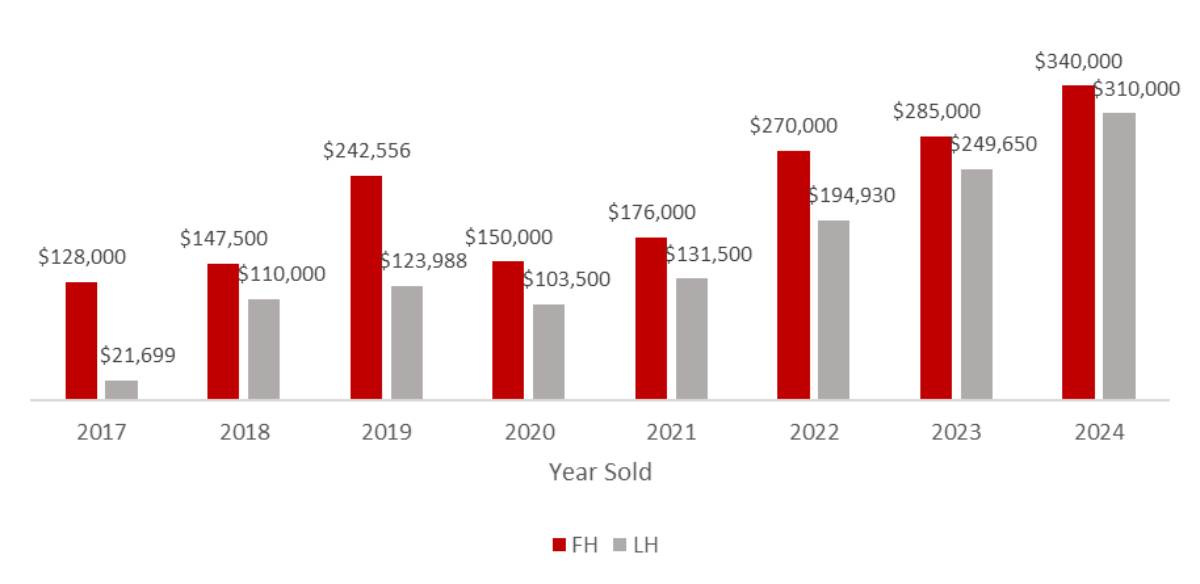

Chart 2: Median profits of freehold and leasehold residential properties within 2km of selected MRT stations by year

Source: URA, ERA Research and Market Intelligence

Based on the data pool of transactions for selected condominium developments, it is apparent that the gap between leasehold and freehold property returns has narrowed significantly.

In 2019, the median profit achieved for freehold condominiums was $242,556, which is $118,568 or 95.6% higher than the $123,988 median for leasehold units. One year later, this margin narrowed sharply to 44.9% in 2020 and has steadily declined since. As of 2024, this gap was just 9.7% – much smaller than the sizeable near-100% difference observed five years earlier.

Chart 3: Percentage gap in median profits of freehold and leasehold residential properties within 2km of selected MRT stations by year

Source: URA, ERA Research and Market Intelligence

This trend is predominantly driven by the increased volume of secondary market transactions occurring at larger and newer leasehold developments, which subsequently leads to more significant price appreciation.

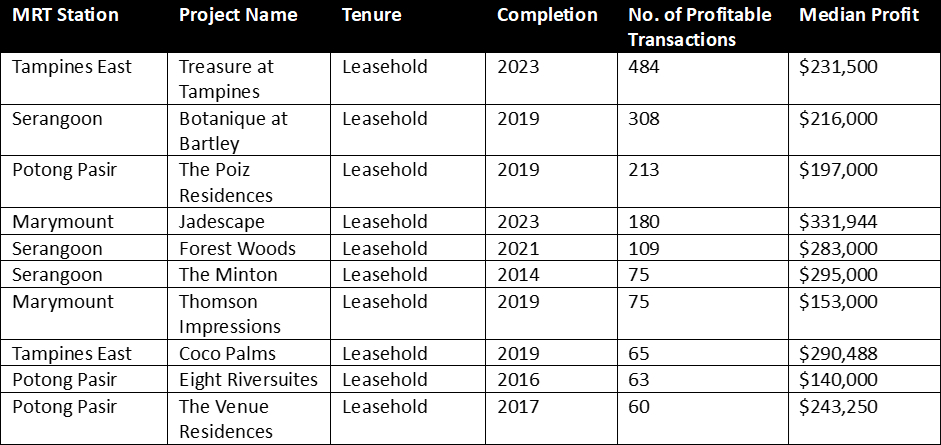

For instance, Jadescape, a 1,206-unit leasehold mega development that obtained its Temporary Occupation Permit (TOP) in 2023, accounted for the largest share of profitable transactions among condominium developments near Marymount MRT station; this strong performance represents 180 of the 745 successful deals identified among projects in the vicinity.

A similar outcome was observed for Treasure at Tampines, another large-scale leasehold condominium project comprising 2,203 units that also achieved its TOP in 2023. On its own, it accounted for 484 of the 1,157 profitable transactions at condominium developments near Tampines East MRT station.

Both of these examples lead us to our next key observation…

2. Leasehold condominiums near MRT stations in the RCR and OCR saw the greatest overall volume of profitable sales

Given their dominant lead in profitable sales at their respective MRT locations, Treasure at Tampines and Jadescape naturally secured places among the Top 10 projects with the highest number of lucrative secondary market transactions.

At the same time, this underscores another key finding: all of the Top 10 best-performing developments are clustered around MRT stations located in the Rest of Central Region (RCR) or Outside Central Region (OCR).

Beyond Tampines East and Marymount, other stations outside of the city centre – like Serangoon and Potong Pasir – also feature prominently in terms of profitable secondary market transactions; this is evidenced by corresponding developments, such as Botanique at Bartley (TOP 2019) and The Poiz Residences (TOP 2019), emerging as standout performers.

Table 1: Top-performing condominiums within 2km of selected MRT stations by volume of profitable transactions

Source: URA, ERA Research and Market Intelligence

This exceptional performance by newer leasehold developments is noteworthy, as it was achieved despite the significantly smaller number of leasehold projects compared to freehold developments in the study (148 vs. 617).

In addition to their newer completion status and convenient access to their respective MRT stations, the success of these top-performing leasehold developments is also linked to their location within popular residential areas. Due to the availability of desirable neighbourhood amenities nearby, such as shopping centres and popular primary schools, RCR and OCR leasehold projects tend to draw substantial HDB upgrader demand. This, in turn, fuels both transaction activity and price appreciation.

Likewise, buyer priorities may have played a role in shaping leasehold demand and price growth too. For instance, families opting for leasehold properties near popular primary schools may view their decision as a strategic medium-term investment, with tenure taking a backseat to the chance of being placed in a desired educational institution.

3. Freehold condominiums saw higher overall median profitability at more MRT locations than leasehold projects

Table 2: Median profits and transaction volume of freehold and leasehold residential properties within 2km of selected MRT stations

Source: URA, ERA Research and Market Intelligence

Although leasehold developments accounted for a larger share of profitable transactions, freehold properties were observed to deliver higher median profits across more MRT locations.

Out of the nine stations studied, six saw freehold properties nearby delivering fatter median profits compared to their leasehold counterparts. This trend was particularly notable for stations in city-centre locations that also saw fewer new launches. For example, near Outram Park and Great World City MRT stations, freehold properties achieved median profits of $230,000 and $350,000 respectively; this far exceeds the $93,600 and $107,000 recorded for leasehold equivalents nearby.

Conversely, leasehold properties experienced higher median profits at ‘mass-market’ locations such as Potong Pasir and Serangoon, where a larger volume of newer leasehold projects may have resulted in more transaction activity, and hence, stronger price growth.

So, what do these findings mean for the private residential market and homebuyers?

While the freehold-leasehold profitability gap may narrow further in the future, the real certainty lies in how supply dynamics will continue to influence price movements for properties of both tenure types.

On one hand, the release of more Government Land Sales (GLS) sites is expected to drive continued price growth in leasehold properties. New projects in popular areas like the future Bayshore estate and Chuan Grove are likely to spur higher transaction volumes, which would further support the price appreciation of leasehold developments in these neighbourhoods.

On the other hand, freehold properties may experience sharper price growth in the near future due to supply-side constraints. With fewer en-bloc opportunities coming to market, the scarcity of freehold redevelopment sites is expected to limit future supply. Such an outcome would result in fewer buying opportunities, and quite possibly, bigger gains for freehold property owners.

Given these equal likelihoods, the wisest course of action for today’s buyers is to base their purchasing decisions on their investment goals, rather than attempting to time or predict the market.

Ultimately, those seeking a legacy asset for future generations should find freehold properties more appealing, given their immunity to lease decay. This characteristic alone makes freehold properties ideal for long-term holds over a decade, making them relevant to buyers prioritising asset preservation and intergenerational wealth transfer.

Conversely, investors targeting medium-term horizons of 4 to 6 years may find leasehold properties more appealing – especially those in suburban locations earmarked for development under URA’s Master Plan. As amenities, connectivity, and commercial offerings improve in line with planned developments, leasehold properties in these areas or estates may see increased transaction volumes and greater resale potential in the foreseeable future.

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.

This article was first published on EdgeProp, featuring expert insights and opinions from Mr. Marcus Chu, CEO of ERA Singapore, ERA Asia Pacific & APAC Realty.

With 29 years of experience in real estate, including four years as the CEO of ERA Singapore, I have had the unique opportunity to witness firsthand the numerous transformations that have influenced Singapore’s real estate scene.

Over numerous building projects, Singapore’s master planning has reshaped our skyline and established a solid foundation for our nation’s and its people’s ongoing development. At the same time, our government has shown a strong commitment to maintaining housing stability by directly addressing market challenges.

Singapore has shown remarkable resilience despite many obstacles, from addressing early land shortages to managing recent pandemic-fuelled supply disruptions.

Similarly, major financial crises have provided transformative insights that led to the implementation of structural protections such as the total debt servicing ratio (TDSR) and the mortgage servicing ratio (MSR).

A resilient market, now tested

As Singapore celebrates its 60th anniversary this year, many reasons exist to take pride in our policy and nation-building accomplishments.

Nevertheless, ongoing success also requires honest reflection and adaptability. Just like past events and demographic shifts have greatly transformed our property market, new trends will continue to emerge — and they will require proactive engagement to ensure local housing stays inclusive and accessible.

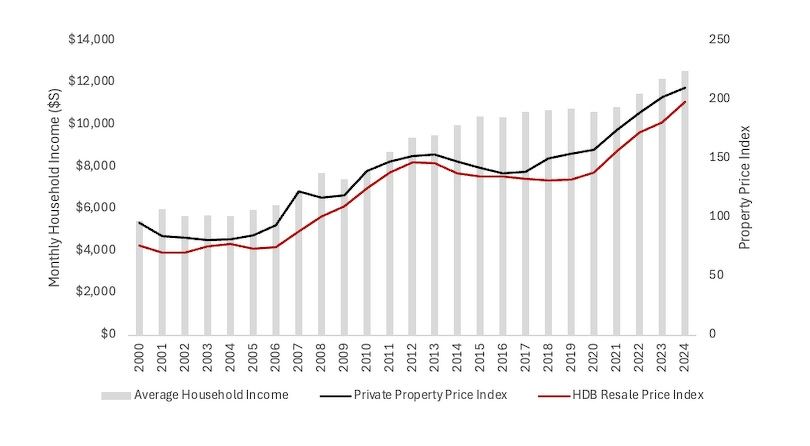

In the last 20 years, average household incomes in Singapore have increased by 111%. Yet, this uptick in earnings has been outpaced by a booming property market, with the Private Property Price Index climbing 148% and the HDB Resale Price Index soaring by an astonishing 169% during the same period.

Median household income versus property price growth (2000 – 2024)

Source: SingStat, URA, HDB, ERA Research & Market Intelligence

The widening gap between income and prices has presented significant challenges to affordability for those seeking to purchase private homes. Although the increase in HDB resale prices has been advantageous for some, many struggle to upgrade due to the parallel rise in private property values.

Executive condominiums (ECs) have become a practical middle-ground choice in this climate. They offer premium condo-style living at a subsidised price in return for stricter eligibility requirements, including an income ceiling of $16,000 and limits on the MSR.

However, despite the continued strong allure of ECs, younger first-time homebuyers now face a steeper path to entry due to rising EC prices and higher upfront cash. In contrast, second-timers often have accumulated housing equity to leverage, and with the deferred payment scheme, it becomes easier for them to purchase an EC.

As concerning as these affordability pressures may be, they are not the only challenges for today’s homebuyers, especially given the broader socio-economic patterns reshaping Singapore’s housing market.

Forces reshaping housing in the next decade

With one in four Singaporeans projected to be 65 or older by 2030, policymakers must address the impending silver tsunami and its extensive socio-economic implications. For instance, alongside this demographic shift, we have observed the growing influence of wealth transfers in driving housing demand.

We have seen a growing number of private homeowners right-sizing in hopes of tapping into their housing equity for retirement while still owning a property that holds value. Simultaneously, some younger homebuyers are now benefiting from parental wealth transfers. It underscores the generational wealth disparity and the widening gap between income growth and housing price appreciation.

On the supply side, rising land costs are also contributing to the growth of private housing prices. Locally, developers acquire land through the Government Land Sales (GLS) programme via a competitive bidding process, where the highest bidder is typically awarded the tender, provided the bid is above the reserve price. This dynamic often drives land prices upward, and more so in desirable locations.

Separately, as part of Singapore’s efforts to meet net-zero emissions by 2050, the government’s carbon pricing strategy will see the carbon tax rise to $25 per tonne of carbon dioxide equivalent (tCO2e) in 2024 and 2025 and $45 tCO2e in 2026 and 2027, with a view to reaching $50–80 tCO2e by 2030. These hikes are set to drive construction costs up, potentially impacting future housing prices.

Better to invest in a home today, instead of waiting for tomorrow

With the abovementioned trends so deeply entrenched in our real estate market, home prices are anticipated to remain stable. Hence, instead of finding the “perfect time” to enter the property market, the wiser approach is to maximise your time. After all, real estate has consistently shown its long-term investment potential with its track record of steady appreciation over time.

For young homebuyers, the most logical first step is to secure a Build-to-Order (BTO) flat as their starter home. BTOs come with a range of subsidies and grants that significantly reduce the cost of homeownership. That will set the stage for future asset progression opportunities.

Buyers should also remain open-minded to take advantage of the first-mover advantage. After all, Singapore’s efficient urban planning ensures that no area is left underdeveloped for long. Identifying these emerging neighbourhoods in advance allows buyers to capitalise on attractive entry prices and potentially benefit from future growth as the area matures and infrastructure improves.

Therefore, planning, patience, and foresight are the keys to unlocking a home and acquiring growth opportunities in real estate. At the same time, buyers should also bear in mind that your journey in real estate isn’t a plan for tomorrow — it’s a future that starts now.

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.

下文由ERA公关经理岳开新翻译

拥有一套公寓是许多本地人的追求,购房者被其良好设施、现代化便利以及黄金地段所吸引。尽管购房成本不菲,但其潜在的回报通常能证明其物有所值。

2024年,私宅价格指数持续稳步上升,全年同比增长3.9%。一方面,这意味着购房者的入场成本更高,但同时也表明市场依然活跃,未来的投资回报前景乐观。

为了验证这一趋势,并考虑到 卖方印花税(SSD) 的影响,我们筛选出了 2024 年盈利交易量最高的公寓项目,这些项目的持有期均不超过 四年。

以下是去年各个地区利润最高的公寓数据。

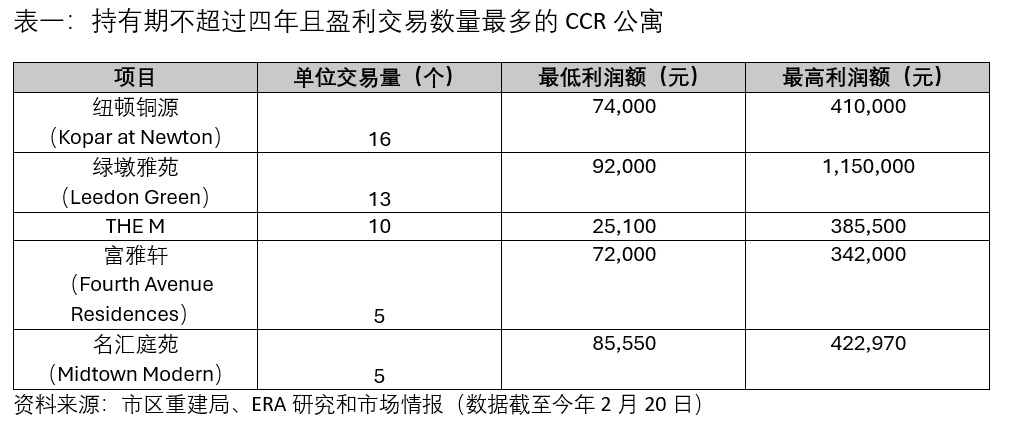

核心中央区(CCR)利润最高的项目

#1:纽顿铜源

CCR中排名第一的是纽顿铜源,这座豪华公寓位于第9邮区,去年共有 16 笔盈利交易。由于该项目 2023 年刚获得临时入伙准证(TOP),在转售市场上更具吸引力,特别受到 偏好全新即刻入住 的买家青睐。

这一趋势也在数据中得到验证:16 笔盈利交易中,有 10 笔为楼花交易(sub-sale),表明买家愿意支付额外溢价,以换取即刻入住的便利。

#2:绿墩雅苑

紧随其后的是绿墩雅苑,共 13 笔盈利交易。这些交易全部为楼花交易(sub-sale),因为项目已于 2023年第四季获得TOP。

项目的亮点不仅仅是交易量,其中 一个四卧房单位(带私人电梯,1496 平方英尺)更是 创下了 CCR 最高盈利纪录,利润达 115 万元。

此外,绿墩雅苑的 最低盈利单位利润(9万2000 元) 也高于其他项目。这可能因项目的位置位于绿墩岭(Leedon Heights)高端住宅区,并且属于永久地契。

#3: The M

排名第三的是The M,这个99年地契的高端综合开发项目位于密陀路(Middle Road),去年共录得 10 笔盈利交易。

The M 的价格增长主要因其优越的地理位置和便利性,项目坐落在第7邮区,靠近武吉士(东西线、滨海市区线)、政府大厦(南北线、东西线)和滨海中心(环线)三大核心地铁站。

此外,The M 还受益于政府推动武吉士地区转型的政策,使其成为中央商务区延伸区的一部分,这进一步提升了项目的吸引力。

值得一提的是,第7邮区近年来迎来了多个新项目,为地区注入了活力。例如,双景岭(Duo Residences)和 City Gate 等优质项目,这也有助于The M 自 2020年推出以来 的价格增长。

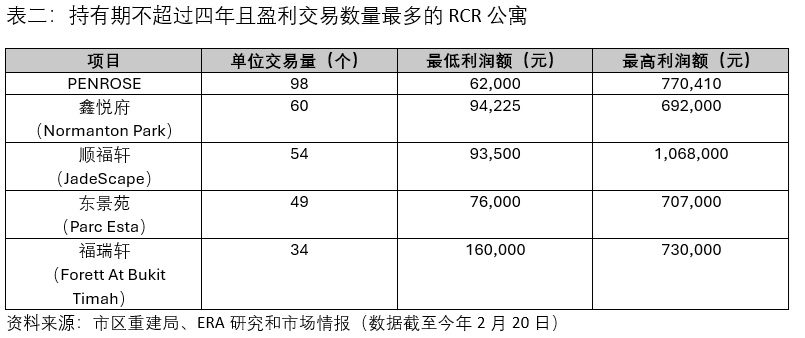

其他中央区(RCR)利润最高的项目

#1: Penrose

PENROSE 位于 第 14 邮区,去年共录得 98 笔盈利交易,成为 RCR 表现最亮眼的公寓项目。该项目位于 沈氏通道(Sims Drive),靠近 巴耶利峇A(Paya Lebar)商圈。

Penrose 的强劲盈利能力得益于近五年前具有竞争力的开盘价格。2020年,第14邮区新项目的中位数单位价格约为 每平方英尺1666元,而 Penrose 的开盘价格仅为每平方英尺1547元,这一价格优势为早期买家提供了更大的升值空间。随着整体房价上涨,他们也享受了更高盈利。

此外,Penrose 靠近阿裕尼(Aljunied)地铁站,再加上“活力加冷总蓝图”(Kallang Alive Master Plan) 规划带来的潜在升值空间,让这个项目未来的增长前景更加看好。

#2:鑫悦府

鑫悦府是去年 RCR 表现第二佳的公寓项目,共有 60 笔盈利交易。这主要因其强劲的租赁投资潜力以及综合型大型开发项目的定位。

除了 1862 套私宅单位,鑫悦府还有 八个商业单位,这为居民提供了便捷的生活设施,提升了整体居住体验。

租赁吸引力方面,项目靠近多个重要商业区,其中包括科学园(Science Park)、丰树商业城(Mapletree Business City)、纬壹(one-north),这里是集生活、工作、娱乐和学习于一体的未来产业园区。

这些因素共同增加了鑫悦府的租赁需求及长期投资价值,使其成为 RCR 区内最具吸引力的项目之一。

#03 顺福轩

顺福轩在2024年以54笔盈利交易名列三甲。这个99年地契的项目位于顺福路(Shunfu Road),于 2023年获得TOP。

除交易量突出外,项目在今年 1月也因一笔创纪录的顶层单位(Penthouse)交易登上本地新闻头条,该单位为卖家带来了 440 万元 的惊人利润。此外,一个 2098 平方英尺的五卧房豪华单位也在转售交易中获得106 万元的可观收益。

顺福轩一系列的高盈利交易,再加上优越的地理位置,如靠近玛丽蒙( Marymount) 和 汤申上段(Upper Thomson) 地铁站,以及碧山—汤申(Bishan-Thomson)区域),使项目成为RCR 最具投资价值公寓之一。

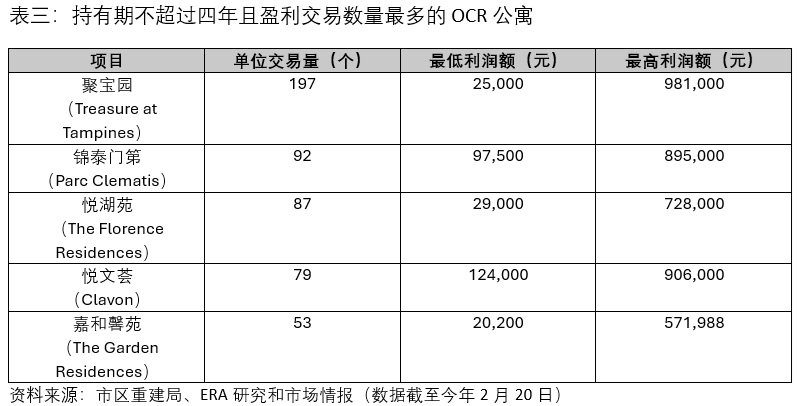

中央区以外(OCR)利润最高的项目

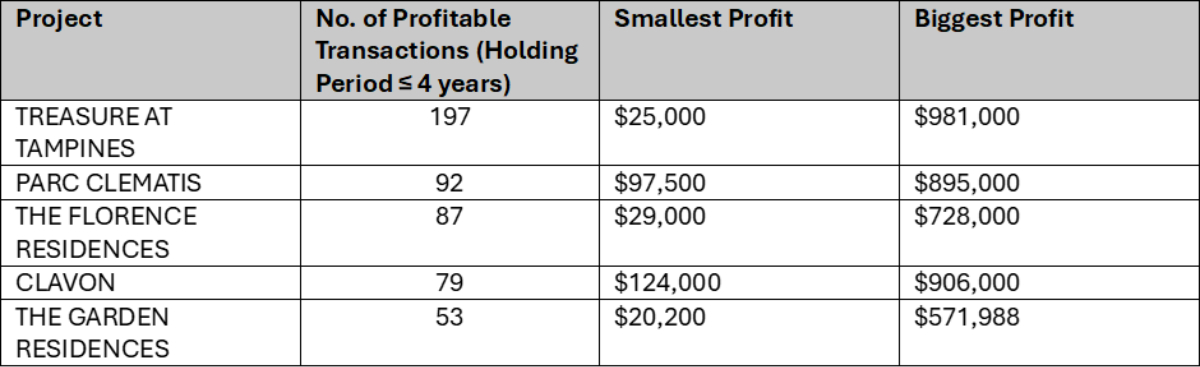

#1: 聚宝园(Treasure at Tampines)

因聚宝园是新加坡霸级规模私宅之一,共2203 个单位,所以去年获得 OCR 最高的转售交易量并不令人意外。其中,有197 笔交易实现盈利,利润介于 2万5000元 至 98万1000元。

这座 99年地契的私宅位于 淡滨尼巷(Tampines Lane),地理位置优越,毗邻多个重要设施和交通要道,其中包括淡滨尼圆巴刹与熟食中心(Tampines Round Market & Food Centre)、泛岛高速公路(PIE)和淡滨尼南高架桥(Tampines South Flyover)。

此外,聚宝园的便利性进一步提升了房价的增值潜力。居民可以方便前往淡滨尼广场(Tampines Mall)、世纪广场(Century Square)和东福坊(Eastpoint Mall),这些商场距离公寓仅约 1 公里,为他们提供了丰富的购物、餐饮和娱乐选择。

#2: 锦泰门第(Parc Clematis)

尽管锦泰门第位于西部的第5邮区,地理位置上与东部第18邮区的聚宝园几乎成犄角之势*,但它们的多个相似处,推动其房价增长。

首先,锦泰门第作为霸级项目,同样受益于规模优势。公寓拥有1450 个单位,这类大型项目通常有更高的交易量,从而可推动房价稳定上涨。

此外,锦泰门第优越的地理位置 也是吸引买家的重要因素之一。项目邻近多个设施,其中包括金文泰地铁站、金文泰广场(Clementi Mall)、NEWest、君超广场(Grantral Mall)。

同时,项目也靠近亚逸拉惹高速公路(AYE),出行便捷,可快速抵达莱佛士坊(Raffles Place)、珊顿道(Shenton Way)及滨海湾金融区(Marina Bay Financial District)等重要商业中心。

#3: 悦湖苑

榜单中前两名均为霸级项目,位居季军的悦湖苑 也不例外,共1410 个单位,原址曾是中等入息公寓(HUDC)Florence Regency,它于2014年私有化,并于2017年集体出售。

悦湖苑 距离后港地铁站仅约 600 米,步行 约5 分钟,预计这可让项目在即将到来的 跨岛线(Cross Island Line,简称CRL)中受益。

当 跨岛线第一阶段于2030年通车后,后港地铁站将成为换乘枢纽,连接 跨岛线与东北线(North-East Line,简称NEL),这将极大提升悦湖苑居民出行的便利性,同时,提高其长期增值潜力。

我们可从上述盈利交易中了解到什么?

对这些按盈利交易项目进行深入分析,可以得出以下几个重点:

首先,即使持有期较短(四年或以下),房产仍能带来可观回报。

这一趋势在刚获得TOP的私宅中表现的尤为明显。这些房产可立即入住且全新,吸引了大量买家,从而推动了更高的盈利交易量。

这种现象在其他地区也均有所体现,去年盈利的转售项目中,楼花交易比例高于普通转售交易,进一步印证了新TOP项目的投资吸引力。

其次,同一地区中,大型综合开发项目(Mega Developments)在价格增长方面往往优于中小型项目。

这主要是两个关键因素:大型综合开发项目可提供的多样化户型选择以及庞大的单位供应量,这通常会产生更多的交易,从而带动销售,并实现更高的资产增值。

那么,如果您正在考虑在大型综合开发项目中购置新房,或者计划在 2025 年购买任何新推出的项目,欢迎查看我们整理的2025 年新楼盘详情。

此外,您也可以随时联系 ERA Trusted Advisor,获取量身定制的房产推荐,满足您的住房需求和偏好!

本文件中的信息仅供参考,不构成对信息的准确性、完整性或可靠性的保证。使用者应自行核实相关信息,并根据具体情况向独立的专业人士(如估价师、财务顾问、银行从业人员及律师)寻求专业意见。ERA及其销售人员对于因使用本信息而导致的任何直接或间接损失概不负责。此外,本文件受著作权法保护,ERA拥有其著作权。未经事先书面许可,任何个人或机构不得以任何形式或手段对本文件进行复制、传播或用于商业用途。

Owning a condo in Singapore is often aspirational, with many homebuyers drawn to the unbeatable mix of ample facilities, modern amenities and prime locations that such dwellings offer. These perks come at a cost, but the potential rewards do justify the investment.

In 2024, the private residential price index continued its steady climb, maintaining the momentum of past years with a 3.9% year-on-year increase. Although this uptick translates into pricier purchases for potential buyers, it also reflects a thriving market with promising opportunities for future returns.

To support this view, we have identified condo developments with the highest volume of profitable deals in 2024, based on a collective pool of 1,445 money-making properties with holding periods of four years or less (i.e., an optimal window for benefiting from Seller Stamp Duty exemption while achieving quick gains). Below are key details about these moneymakers in each region, along with bite-sized insights into their successes.

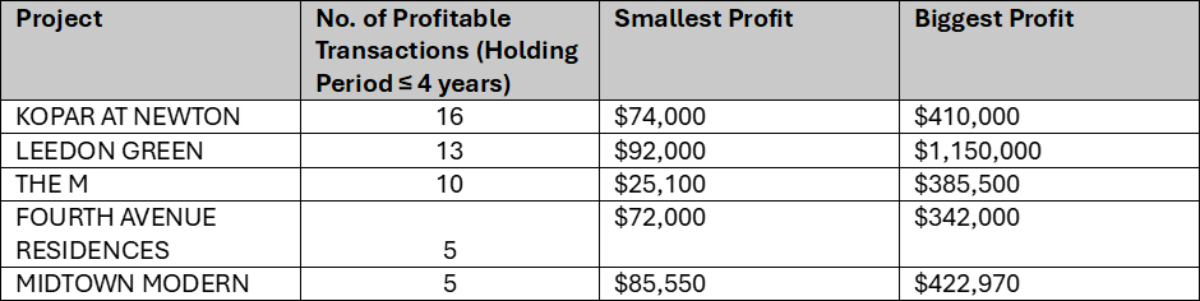

Best-performing Core Central Region (CCR) projects with the most number of profitable deals

Table 1: CCR condominium projects with the greatest number of profitable transactions that have holding periods of no more than 4 years

Source: ERA Research and Market Intelligence, URA (as of 20 Feb 2025)

#1: Kopar at Newton (16 profitable transactions in 2024)

Taking the top spot within the CCR with 16 profitable transactions is Kopar at Newton, a luxury condominium located in District 9. Fresh from obtaining its Temporary Occupation Permit (TOP) last year, Kopar at Newton enjoyed an advantage in the sub-sale market, being particularly appealing to buyers who value newer, move-in-ready homes over resale properties in the same vicinity.

This preference becomes apparent when looking at the numbers: Among Kopar at Newton’s 16 profitable transactions, ten were sub-sale deals, which demonstrates the willingness of buyers to pay for the convenience of immediate occupancy.

#2: Leedon Green (13 profitable transactions in 2024)

Moving down the list, Leedon Green took second place in the CCR with 13 profitable deals, all of which were sub-sales due to its TOP attainment in 4Q 2023. The development also stood out for achieving the highest absolute gains among all regions, with a luxury 4-bedroom unit + private lift (1,496 sq. ft) raking in an impressive $1.15M profit.

In the same vein, Leedon Green’s smallest recorded profit of $92,000 also exceeds the baseline for absolute gains made at other top-performing CCR developments on this list; this may well be due to the development’s location within the prestigious Leedon Heights area and its freehold status in the CCR.

#3: The M (10 profitable transactions in 2024)

Coming in third, with a total of ten profitable transactions, is The M – a premium 99-year leasehold, mixed-use development located on Middle Road. Given its address in District 7, much of The M’s price appreciation can be attributed to its premium location and convenience.

To begin with, the development is located near not one but three key MRT stations: Bugis (East-West, Downtown Lines), City Hall (North-South, East-West Lines), and Esplanade (Circle Line). Likewise, The M also benefits from the Government’s ongoing efforts to transform the surrounding Bugis area into an extension of the Central Business District, which contributes to the desirability of its homes.

Additionally, in recent years, District 7 has also seen various new developments breathing new life into the area. As such, successful projects within the area, like DUO Residences and City Gate, may have also contributed to The M’s price growth since its initial launch in 2020.

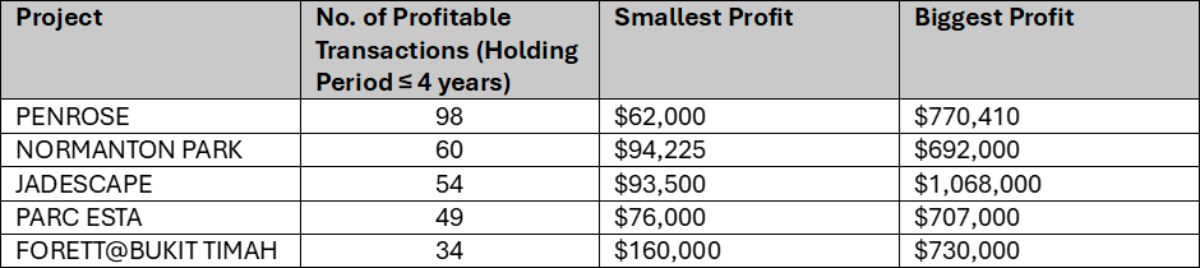

Best-performing Rest of Central Region (RCR) projects with the most number of profitable deals

Table 2: RCR condominium projects with the greatest number of profitable transactions that have holding periods of no more than 4 years

Source: ERA Research and Market Intelligence, URA (as of 20 Feb 2025)

#1: Penrose (98 profitable transactions in 2024)

Within the RCR, Penrose secured the top spot for the best-performing residential development, achieving 98 profitable transactions last year. This 99-year leasehold project is situated at Sims Drive, offering a convenient location near the Paya Lebar Precinct and within the broader, desirable District 14 area.

Penrose’s strong profitability may also be traced back to its competitive launch pricing nearly five years ago. In 2020, while the median unit price of new launches in D14 stood at $1,666 psf, the equivalent for Penrose was $1,547 psf; this made the project a compelling value proposition in D14, while also providing first movers a higher margin for appreciation as home prices grew in the area.