How to Co-Own a Residential Property in Singapore, Even When Breaking the Norm

- ERA Singapore

- 9 min read

- Blog

- 19 Jun 2025

It’s the classic narrative of Singapore’s housing landscape: dating, getting married, and then moving into a newly completed Build-to-Order (BTO) flat as newlyweds. However, this familiar route isn’t always accessible to everyone, whether by personal choice or due to circumstances beyond their control.

Thankfully, for those who are unable to enjoy shared ownership of a property with a spouse, there are still avenues to enter Singapore’s property market with a trusted someone – be they a live-in partner, close friend, or family member. This guide will explore the various housing options, eligibility criteria, and key considerations for co-owning a Singapore property even when legal marriage isn't on the cards.

Why is property co-ownership outside of marriage a consideration for some Singaporeans?

There are numerous reasons why some Singaporeans might opt to co-own a residential property outside of marriage.

While some aspiring homeowners may choose to do so due to practical concerns, such as financial constraints or caregiving responsibilities towards a disabled and/or elderly family member, others may be motivated by personal circumstances. Moreover, not all aspiring homeowners fall within the conventional definitions of family or marital status; yet they too are also seeking pathways to co-ownership.

For instance, a widower who has found love again may choose not to remarry to avoid the hurdles of legal marriage. Accordingly, they might choose to co-own a property with their new partner, which would enable them to build a shared home, sans the bureaucracy and formalities.

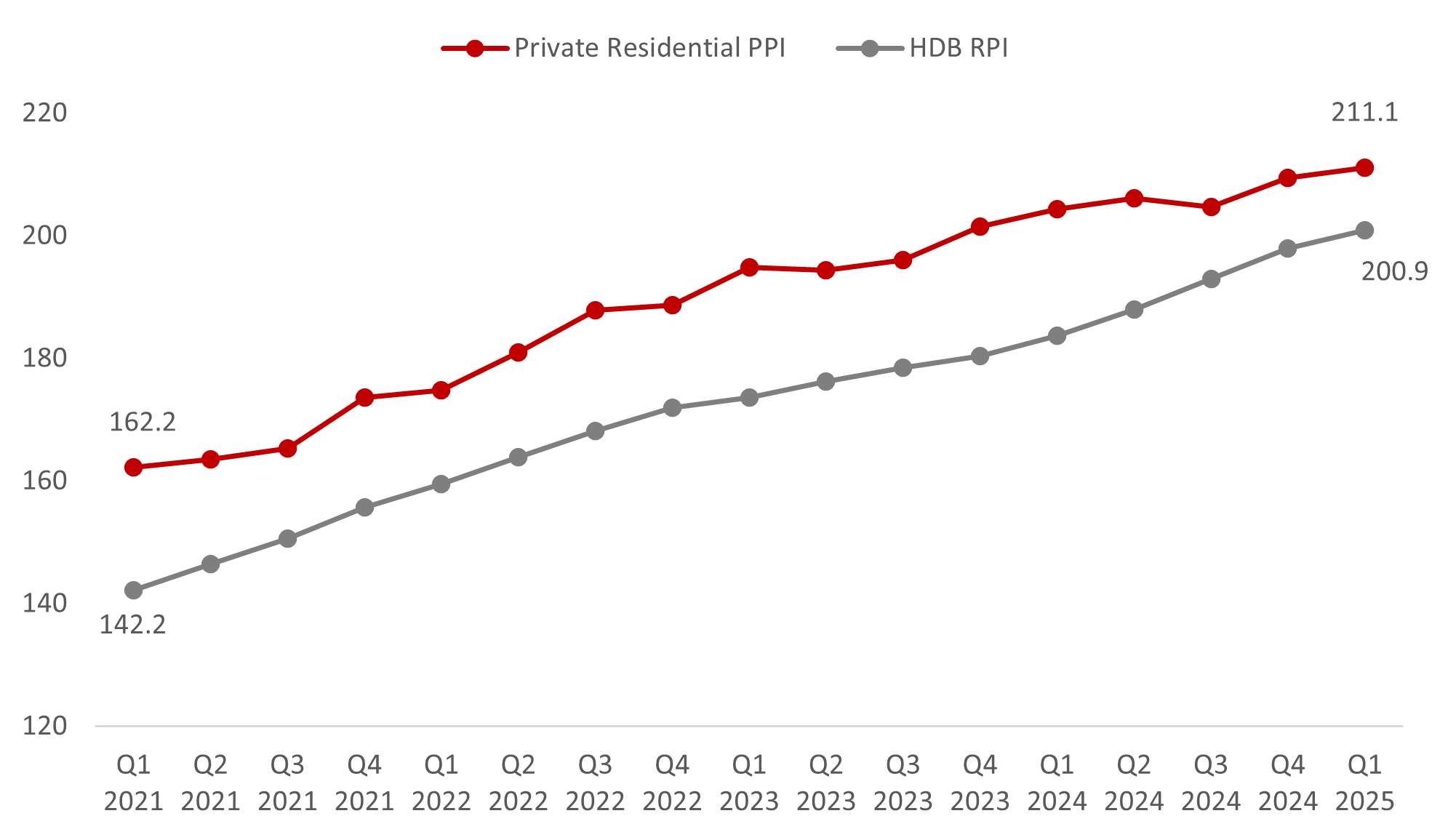

From a purely financial perspective, there is also a compelling case for co-ownership outside of marriage, given the robustness of Singapore’s property market. Property has long been regarded as a reliable investment asset locally, owing to its history of consistent appreciation. Between 2021 and 2025 alone, HDB flats and private homes have experienced significant upward momentum, as evidenced by the sharp 41.3% (142.2 to 200.9) and 30.1% (162.2 to 211.1) increases in their respective price indices.

Chart 1: HDB resale price index (RPI) and private residential property price index (PPI) from 1Q 2021 to 1Q 2025

Source: URA, HDB, ERA Research and Market Intelligence

In this light, property co-ownership transcends merely fulfilling housing needs; it also represents a strategic decision for long-term financial security. This is especially relevant for those who may not have children of their own and/or lack familial support in later stages of life.

However, given the increasing proportion of singles in Singapore’s resident population, personal choice and/or a desire for freedom are likely the main factors influencing interest in alternative paths to homeownership, including co-ownership arrangements.

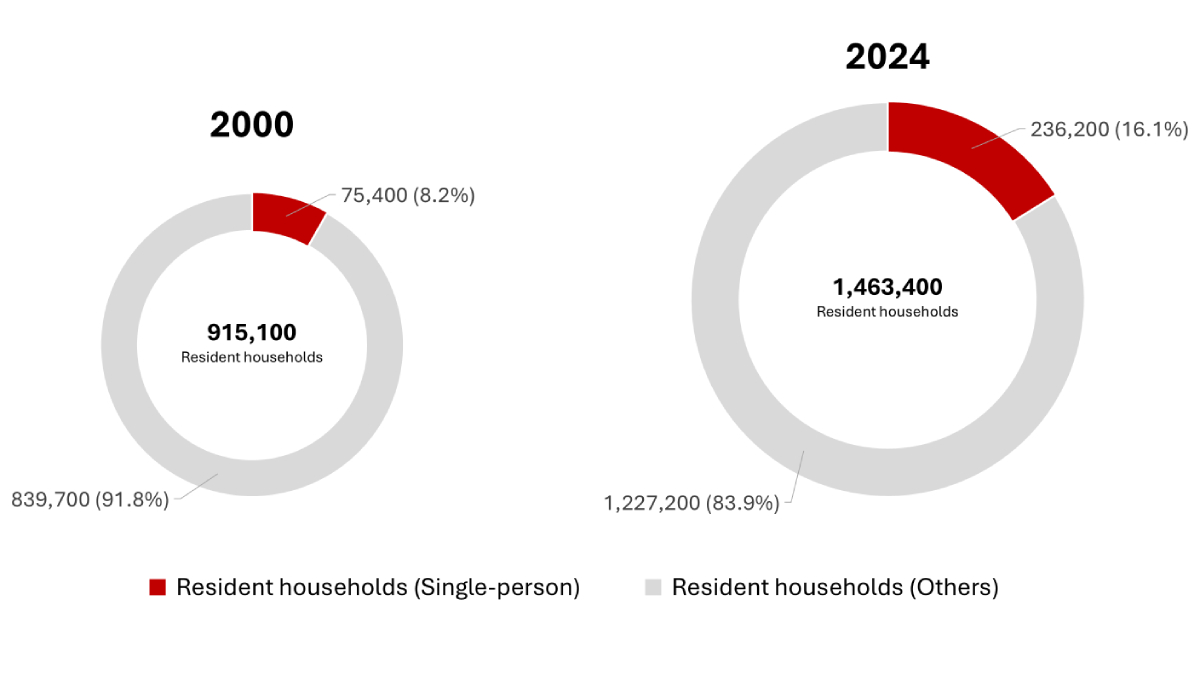

Chart 2: Growth in single-person households as a proportion of total resident households (2000 – 2024)

Source: SingStat, ERA Research and Market Intelligence

These beliefs tie in with a greater preference for single living as well, especially among Singaporeans seeking flexibility and privacy. Based on official SingStat figures, the number of single-person resident households has risen by over 200% from 75,400 in 2020 to 236,200 in 2024. Likewise, the share of single-person resident households has also seen a notable increase, doubling from 8.2% in 2000 (75,400 of 915,100 households) to 16.1% in 2024 (236,200 of 1,463,400 households).

Therefore, given the increasing prevalence of singlehood among Singaporeans, it is reasonable to suggest that there may indeed be a growing need to reimagine local homeownership beyond the traditional couple-centric model.

The Singapore Government has taken steps in this direction, with the most recent change being the expansion of public housing options for singles. A key policy revision in the second half of 2024 now allows singles – or, for co-ownership purposes, groups of up to four singles – to purchase 2-room Flexi HDB flats in any housing estate, including prime locations.

However, different homeownership requirements and considerations will apply depending on whether one is considering co-owning an HDB flat, an executive condominium (EC), or private housing.

What are the laws, rules and considerations for co-owning different residential properties for joint-singles?

Buying an HDB flat will require all parties to be at least 35 years old.

While HDB offers numerous eligibility schemes to support various demographic groups in their housing journey, single buyers interested in co-owning a flat need only focus on one: the Joint Singles Scheme.

Introduced in 1990, the Joint Singles Scheme allows eligible Singaporean men and women at least 35 years old to jointly purchase an HDB flat or Executive Condominium (EC). However, those who are widowed or orphaned may qualify from the age of 21, but only for resale Prime flats, unclassified resale flats, and new Standard and Plus flats.

For the purposes of this piece, we consider joint single households to be living arrangements involving two to four unmarried individuals of any gender. Additionally, if you intend to apply under the Joint Singles Scheme, it is important to take note of the following requirements:

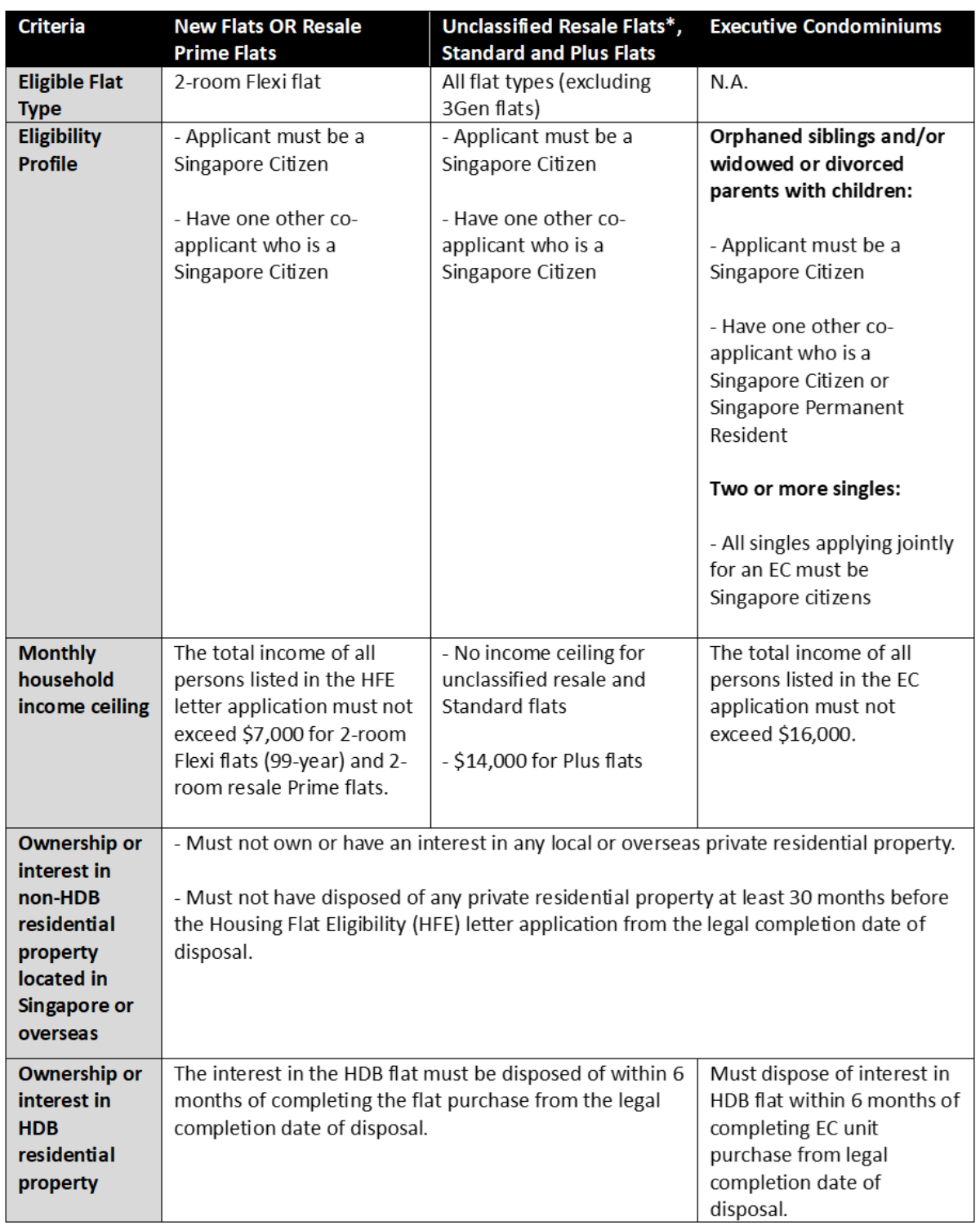

Table 1: Joint singles eligibility criteria for HDB and EC flat purchases

Source: HDB, ERA Research and Market Intelligence

*Unclassified resale flats refer to HDB homes sold before the October 2024 sales exercise that do not fall under either Standard, Plus, or Prime classification categories.

Private home ownership is less cumbersome.

Unlike HDB flats or Executive Condominiums, purchasing private property as co-owners is not subject to specific eligibility criteria. However, co-buyers must consider the manner of holding or, more simply, how ownership is legally shared. This is particularly important for inheritance, as the selected holding method determines how the property is passed on after a co-owner's death.

What are the different manners of holding or ownership types, and how do they matter in inheritance planning?

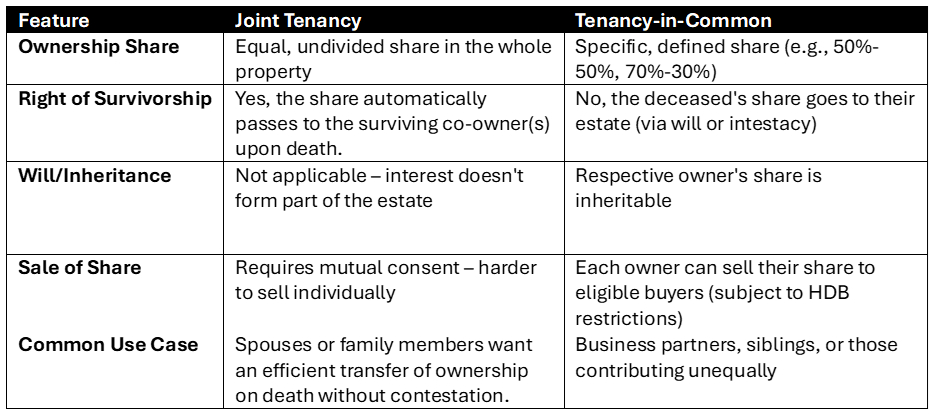

So, there are two property ownership types in Singapore, namely holding the property in Joint Tenancy and Tenancy-in-common. For HDBs, applicants under the Joint Singles Scheme must be registered as co-owners (i.e. the owner-occupier structure is not allowed).

While joint tenancy is the default holding method for HDB flats, buyers can opt for tenancy-in-common. However, this may come with higher legal fees due to the higher complexity of arrangements and the potential for disagreements.

- Joint Tenancy

Under a joint tenancy structure, there is an undivided interest in the property. All owners are regarded as owning the entire property collectively, with no separate or distinct shares. When one owner passes away, the rights of survivorship come into effect. This means that the surviving owner automatically inherits the rights to the full share of the property, irrespective of any existing will.

This is with the exception of when both parties pass away at the same time. In such cases, the order of death becomes legally significant. However, when it is impossible to determine (e.g., simultaneous death in an accident), Singapore law presumes that the younger person passes away later. Hence, the younger party will inherit the entire property before passing it on to their next of kin or will beneficiaries.

For example, Jamie and Ashley are both unmarried 35-year-old singles with no family, who decide to buy an HDB flat together under a joint tenancy arrangement. If Jamie passes away, Ashley will inherit full ownership of the flat.

Below, we have summarised the characteristics of both manners of holding:

Table 2: Summary of manner of holding of property

Source: ERA Research and Market Intelligence

- Tenancy-in-Common

Under the tenancy-in-common structure, owners can agree on their respective ownership percentages, provided they total 100%. For instance, if one party pays for 70% of the property and the other covers 30%, they hold a 70-30% share. These shares are detailed in the title deed. Upon death, each owner’s share will pass to their respective estate rather than to the surviving owner.

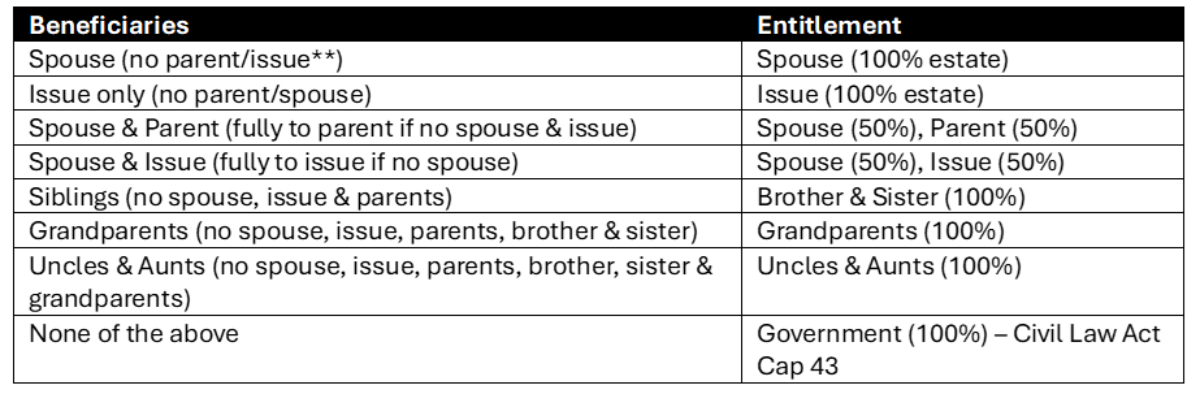

If all owners pass away simultaneously, each owner's share will be allocated to their respective beneficiaries under their wills or according to the Intestate Succession Act if no will exists. The assets will be divided in accordance with the act.

Table 3: Common beneficiaries under the Intestate Succession Act*

Source: Singapore Statutes online (sso.agc.gov.sg)

* The Intestate Succession Act does not apply to Muslims. The estate of a Muslim is governed by Muslim law. ** ‘Issue’ is a legal term referring to one’s direct descendants.

The Tenancy-in-Common ownership structure would be ideal for two parties who have their own estates to pass on the property to, such as divorcees or widows with children, coming together to jointly purchase a property.

For instance, Lewis and Jesse own 70% and 30% of a condominium unit, respectively. If Jesse were to pass away, his share (70%) would go to his estate according to his will, while Lewis would continue owning 30% of the property.

Beyond legalities, what else should you consider before co-owning a residential property?

For many, the legal, emotional, and financial advantages of co-owning a property outside of marriage are very real. Still, it is equally important to recognise the responsibilities and risks that come with it.

Firstly, just as in marriages, breakdowns in relationships between co-owners can make living together challenging. However, unlike most relationships, where it is possible to walk away from the other party, you will be tied to the shared property unless both parties reach a consensus on future ownership.

The same goes for scenarios where financial difficulty is a concern. If one party is unable to cover their share of costs (e.g., mortgage, maintenance fees), the financial pressure may unfairly fall on the rest.

Lastly, inheritance disputes could arise even if a manner of holding or inheritance has been specified. For instance, in an emotionally charged situation, family members of a deceased co-owner may still choose to contest a will despite its legal standing.

For these reasons and more, all parties involved should establish a shared understanding and make definitive arrangements on how ownership should be handled in good times and in bad, before proceeding with a purchase.

Beyond formalising the manner of holding, prudent buyers may also consider drafting a will to facilitate smooth and unambiguous future transfers, particularly when a joint tenancy is involved. Likewise, a consultation with legal and real estate professionals is recommended for more precise understanding and informed guidance. Because just as with the people you love, those you share a roof with deserve nothing less than care and clarity.

I confirm that I have read theprivacy policy and allow my information to be shared with this agent who may contact me later.