A brief history of Singapore’s North Region

In the years around and after Singapore’s independence, the North region of Singapore – comprised of Sembawang, Woodlands, and Yishun remained largely undeveloped. These areas served as kampungs, rubber plantations, and in the case of Sembawang, home to a naval base – both under British and Singaporean power.

Development in the north started with Yishun New Town in the 1980’s, followed by Woodlands later in the decade. Woodlands then rapidly took shape, growing into the regional centre. It featured the town’s transformation into the North’s largest residential town, featuring residential, industrial, and commercial developments.

The 90’s saw a decade of further change for the North, with the opening of Woodlands MRT as part of the North South Line expansion, and the subsequent opening of Woodlands checkpoint in 1999. This marked Woodlands as an important commercial and transport hub for Singaporeans and Malaysians alike, who would often transit through the regional centre to move between the two countries.

Sembawang Naval Base in the time of colonial rule

Interestingly, throughout these two decades, Sembawang remained relatively untouched as a naval base, until the turn of the millennium where we began to see a shift towards a residential town and estate through the construction of HDB flats.

Sembawang Today

Today, Sembawang has grown into a fully-fledged residential town. Its naval heritage remains, with road names in the town paying homage to the British naval vessels that once used to grace the docks of the northern town. A prominent example of this would be the planning subzone Canberra, named after the old HMS Canberra.

A visit to Sembawang today would present you with the picture of an idyllic suburban estate. The town is quiet and peaceful, particularly due to its lower density. Of all the residential towns in the North region, Sembawang is by far the smallest, housing just over 30,000 dwelling units.

Sembawang today is a quaint residential town, with around 30,000 homes

In comparison, Woodlands, the regional centre of the North is home to almost 72,000 dwelling units, while Yishun, the other large residential town in the north is also home to over 69,000 of such homes.

With less than half as many homes, it is evident that Sembawang has received less love than its neighbours. But with a projected ultimate capacity of 65,000 – over double of the current inventory in the area, it is clear that Sembawang will be the next town to experience rapid development.

Bukit Canberra

Spearheading Sembawang’s development and transformation into a new-age residential town is Bukit Canberra, an integrated community and sports hub.

Partially opened since 2021, Bukit Canberra is modelled after Our Tampines Hub, aiming to integrate community focused amenities such as healthcare and dining with sports facilities to promote a greener and more active lifestyle among Singaporeans.

The facility comprises extensive sports facilities, such as indoor and outdoor lap pools, 3km of running trails, a polyclinic, a senior care centre, and a hawker centre with 800 seats and over 40 stalls.

Despite being an entirely modern and new development, Bukit Canberra also does its best to preserve Sembawang’s roots. It is built on the site of the old Chong Pang Village market and hawker centre and will house the refurbished Admiralty House into a library full of historic stories of Sembawang’s naval past during colonial times.

Other Amenities

Shopping and Retail

Despite its small size, Sembawang is home to two shopping centres, Sun Plaza (located next to Sembawang MRT) and Canberra Plaza, an integrated development next to Canberra MRT.

Across the two malls spanning both the neighbourhood’s MRT stations, residents have easy access to amenities and services such as grocery stores, dining options, clinics, enrichment centres, and retail shops. These options easily provide day-to-day necessities for its residents, while alternatives can be easily accessed within 5 minutes at either Yishun or Woodlands, which boast large shopping malls of their own.

Sun Plaza, one of the malls that serve the residents of Sembawang

Nature and Recreation

In terms of recreation, Sembawang is home to its very own Sembawang Park, which is a seaside park with beaches, barbecue pits, and views of the Johor Strait.

Sembawang is also unique as it is home to Sembawang Hot Spring Park, the only natural hot spring park in Singapore. Visitors can enjoy foot-soaking pools and heritage exhibits in a well-maintained and landscaped setting.

Sembawang Hot Spring park is home to the only natural hot spring in Singapore

Transport and Accessibility

Sembawang is connected to Singapore’s transport network through two stations on the North-South Line, Sembawang and Canberra. The line connects Sembawang directly to the city centre in around 30-minutes.

The most recent Thomson-East Coast Line runs through Woodlands MRT station, a mere two stop from Sembawang. The additional line provides access to additional locations, such as various parts of Woodlands, and even all the way through to the east coast of Singapore.

In addition to this, various feeder buses serve the town, providing easier access to nearby MRT stations for residents that might stay slightly out of walking distance from the MRT.

North-South Corridor

Sembawang will also directly benefit from the future North-South Corridor (NSC). The 21.5km multi-vehicle expressway will directly connect Woodlands to Marina Bay and promises a much faster commute to the city for residents in the North region.

The NSC will cut travel times by 10-15 minutes during peak hours, and reduce the reliance on the often-congested Central Expressway. There will also be express bus services to serve those that do not own a vehicle, allowing them a much faster commute on public transport to the city centre.

A New Neighbourhood in Sembawang North

You might ask: what’s the purpose of constructing so many amenities for a town with such a low number of residents? With many plans for development in Sembawang, the picture starts to become clear.

Announced by the Ministry of Development and Housing Development Board in October 2024, we can expect around 8,000 BTO flats and 2,000 new private housing units to be constructed in Sembawang North, a planned 53-hectare residential neighbourhood.

This starts with the BTO exercise in July 2025, where a 775-unit development, Sembawang Beacon will be the first of many housing projects that will occupy the up-and-coming neighbourhood. Additionally, the project completion timeline is slated to be under three years, as it is classified as a Shorter Waiting Time (SWT) project.

SWT projects are normally selected in up-and-coming locations with ample development potential, shoring up confidence that Sembawang North’s development is a priority.

What about the Private Market?

Sembawang is also receiving further development interests in the private and executive condominium markets as well. Currently, there are a few non-landed private homes in the town. As the town still has much room to grow, we can expect many more new condominiums and even ECs built here in the future.

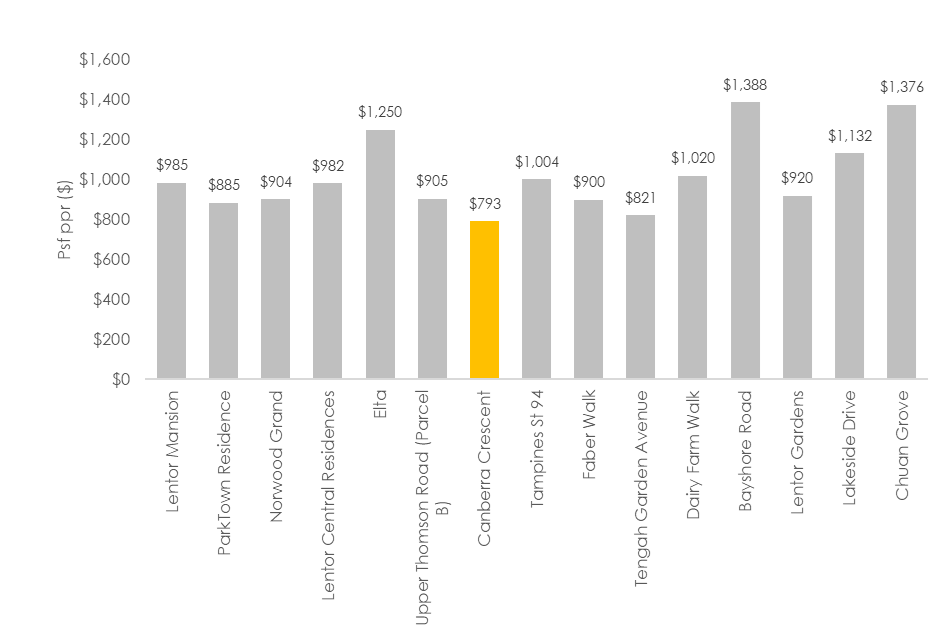

In July 2024, a private residential land parcel was sold via the Government Land Sales at Canberra Crescent.

Chart 1: Land Cost for OCR Private Non-Landed Developments

Source: URA, ERA Research and Market Intelligence as at 21 July 2025

Furthermore, the GLS plot at Canberra Crescent was also tendered at a more attractive land rate compared to other Outside Central Region (OCR) sites. With a land rate of $793 psf ppr, Canberra Crescent Residences, slated to launch in Aug 2025 should feature attractive pricing, allowing buyers to buy into the estate at an accessible price point.

The last new condominiums in the area were The Watergardens at Canberra and The Commondore, both which were launched in 2021. Since then, we have witnessed resale transactions averaging $1,755 psf at The Watergardens at Canberra. This resale price, a significant increase from the median price of $1,469 psf witnessed during its launch month highlights the area’s growth and potential.

Chart 2: Canberra Crescent GLS and EC price comparison

Source: HDB, URA, ERA Research and Market Intelligence

With a land rate that is comparable with that of the last 3 EC sites tendered, Canberra Crescent Residences should offer a compelling alternative for a private property upgrade to HDB owners in the surrounding estate that might have originally been considering an EC instead.

Executive Condominiums (EC)

Recently, in May 2025 we also saw the opening of a GLS tender for an EC site at Sembawang Road. This is the first EC introduced in Sembawang since 2021. The introduction of ECs is a great way to support the development of the town and provides a sustainable upgrading and housing option.

There is currently no stock for ECs, with North Gaia, the last EC launched in the North region having sold out the remainder of its units earlier this year. While there is certainly a supply gap in the market for North region ECs, the demand for this Sembawang site might be moderated by another EC parcel that is currently on sale at Woodlands.

Conclusion

From the full completion of Bukit Canberra, to the upcoming BTO, EC, and private home launches, there is much to be excited about for the quaint town of Sembawang.

The prospect of staying in the North is getting better as time goes by, with developmental plans for not only Sembawang, but in Yishun (the new precinct Chencharu), and Woodlands (Woodlands North Coast and Woodlands regional centre).

With much to look out for – now might very well be the right time to consider investing or staying in Sembawang. If you are curious on how you can do so, do not hesitate to speak to an ERA Trusted Adviser today.

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.

Looking back, the COVID-19 pandemic had more than just an impact on Singapore’s public health. One of the most significant disruptions arising from the crisis were construction delays, which stalled HDB flat completion and created a shortage of homes. With supply unable to keep up with demand, more buyers turned to the resale market, and this applied further upward pressure on prices.

Since then, the resale HDB market has not looked back, exhibiting an unbroken upward trend that has seen prices rise consistently for 22 straight quarters as of 1Q 2025.

While this status quo is expected to continue in the near term, price growth could moderate this year. In 2Q 2024, the HDB resale price index was 187.9. This index rose to 202.8 in 2Q 2025. It was projected that this index would increase at a gentler pace of 3 – 6% year-on-year (y-o-y) in 2025. Additionally, the number of million-dollar flats rose from 419 transactions in 1H 2024 to 763 transactions in 1H 2025.

On the supply side, HDB has launched over 5,000 new Build-to-Order (BTO) flats, as well as another 5,590 Sale of Balance Flats (SBF) in February 2025’s BTO exercise. HDB plans to release a further 19,600 units this year. Not only will this incoming supply provide flat buyers with a more affordable option, but it may also put downward pressure on existing resale prices.

In 2H 2024, the average price of 4- and 5-room flats experienced a consistent overall increase, along with a notable rise in the number of transactions valued at a million dollars or more. Although this might seem intimidating, another way to understand it is that for every million-dollar flat sold, approximately 43 other flats were sold at lower prices. 2H 2024 also saw the general price growth of 4- and 5-room flats remain stable.

Table 1: 1H 2024 vs 1H 2025 HDB Resale Comparison

Source: Data.gov.sg as of 1 July 2025, ERA Research and Market Intelligence

The number of flats transacted at $1 million and above in 1H 2025 accounts for only 4.3% of all transacted flats, meaning that the other 95.7% of flats were transacted below the million-dollar mark.

However, amid these market shifts, one question remains: Are there still affordable flats available now, especially 4-room and 5-room units? The answer is “yes” – and here’s where they can be found.

Affordable 4 Room Flats

The lowest-priced 4-room flat in 1H 2025 was in Tampines, costing $300,000. Of the 4-room flats transacted in 1H-2025 (5,628 transactions), 3,555 were below the average price of $670,000, making up 63.2% of all 4-room flat transactions.

The table below shows the towns with the lowest average price transacted for a 4-room flat.

Table 2: Towns with the lowest transacted average price for a 4 Room Flat in 1H 2025

Source: Data.gov.sg as of 1 July 2025, ERA Research and Market Intelligence *Rounded to the nearest thousand

Reflecting on our findings in 1H 2024, most of the affordable 4-room flats still appear in satellite towns within non-mature estates. This is because there are more HDB estates in these areas, and homes here are usually sold at lower prices than those nearer the Central Region, due to the high demand for housing closer to the centre.

If the size of your home is a major factor in your purchase, most older flats in these areas tend to be larger, especially those built in the 80s and 90s. Woodlands and Yishun feature jumbo flats, which are essentially unsold 3- and 4-room flats combined to create larger units. These units range from 147 to 199 square metres and provide a more spacious living area. This offers buyers greater value for money. However, you might miss out on a potentially longer lease as HDB has stopped building these flats since the 90s.

In 1H 2024, we observed that most 4-room flats sold for under $650k had a remaining lease of 15 years or less. A breakdown of 4-room flats sold in 1H 2025 below the average price of $670,000 showed that the shortest lease among sold flats was 44 years, and most of these flats had between 36 and 45 years remaining.

Chart 1: Breakdown of 4-room resale HDB flats sold for under $669,000 in 2H 2024 by flat age

Source: Data.gov.sg as of 17 June 2025, ERA Research and Market Intelligence

Affordable 5 Room Flats

Moving on to affordable 5-room flats, data collected showed that Jurong East had the lowest transacted price for a 5-room flat in 1H 2025, with a price tag of $445,000 ($398 psf). Although this may seem appealing at first glance, the remaining lease on this unit was just over 50 years, suggesting that its age may have influenced the price.

The total number of transactions below the average price of a 5-room flat ($775,000) was 1,836 transactions. This accounts for 61.1% of all 5-room transactions (3,005 transactions) in the first half of 2025, which essentially means that the majority of 5-room flats transacted in this period are considered “affordable”. Below are the towns offering the lowest prices for 5-room homes:

Table 3: Towns with the lowest transacted average price for a 5 Room Flat in 1H 2025

Source: Data.gov.sg as of 1 July 2025, ERA Research and Market Intelligence *Rounded to the nearest thousand

Again, we observe that the top 5 towns with the lowest average transacted price of 5-room units are in non-mature estates. This may be because, generally, estates like Woodlands and Sembawang are newer and have more land available. The high land supply keeps the prices of these units lower.

Newer estates often lack amenities, requiring residents to travel further for essential necessities. This can be inconvenient, especially for older residents. Consequently, it discourages buyers from opting for more accessible areas with better amenities, which are usually found in mature estates.

Unlike non-mature estates, mature estates like Queenstown and Ang Mo Kio provide accessibility and a wide range of amenities that are usually within 10 minutes of a resident’s home, which is why the demand for these homes is so high.

Although these affordable flats are generally located further from the Central Region, their lease prices are usually higher compared to those in mature estates or closer to the Central Region. Flats in non-mature estates are newer, allowing buyers to see the long-term value of their purchase as more amenities and transport facilities are added over time. Additionally, towns such as Jurong West and Sembawang typically offer larger flats compared to other newer estates, making them appealing to families seeking spacious yet affordable options.

Chart 2: Breakdown of 5-room resale HDB flats sold for under $775,000 in 2H 2024 by flat age

Source: Data.gov.sg as of 17 June 2025, ERA Research and Market Intelligence

Ultimately, this means that flats are largely still affordable for Singaporeans.

If you are currently searching for an affordable resale flat, starting with non-mature estates is a good first step. With fewer amenities and developments, there is a decent supply of flats with lower demand, which could be priced within your budget.

However, if location is fairly important for your home, there are several flats nearer the central area within older estates that have fewer years remaining on their leases.

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.

Co-written By Egan Mah & Stanley Lim

It’s the classic narrative of Singapore’s housing landscape: dating, getting married, and then moving into a newly completed Build-to-Order (BTO) flat as newlyweds. However, this familiar route isn’t always accessible to everyone, whether by personal choice or due to circumstances beyond their control.

Thankfully, for those who are unable to enjoy shared ownership of a property with a spouse, there are still avenues to enter Singapore’s property market with a trusted someone – be they a live-in partner, close friend, or family member. This guide will explore the various housing options, eligibility criteria, and key considerations for co-owning a Singapore property even when legal marriage isn’t on the cards.

Why is property co-ownership outside of marriage a consideration for some Singaporeans?

There are numerous reasons why some Singaporeans might opt to co-own a residential property outside of marriage.

While some aspiring homeowners may choose to do so due to practical concerns, such as financial constraints or caregiving responsibilities towards a disabled and/or elderly family member, others may be motivated by personal circumstances. Moreover, not all aspiring homeowners fall within the conventional definitions of family or marital status; yet they too are also seeking pathways to co-ownership.

For instance, a widower who has found love again may choose not to remarry to avoid the hurdles of legal marriage. Accordingly, they might choose to co-own a property with their new partner, which would enable them to build a shared home, sans the bureaucracy and formalities.

From a purely financial perspective, there is also a compelling case for co-ownership outside of marriage, given the robustness of Singapore’s property market. Property has long been regarded as a reliable investment asset locally, owing to its history of consistent appreciation. Between 2021 and 2025 alone, HDB flats and private homes have experienced significant upward momentum, as evidenced by the sharp 41.3% (142.2 to 200.9) and 30.1% (162.2 to 211.1) increases in their respective price indices.

Chart 1: HDB resale price index (RPI) and private residential property price index (PPI) from 1Q 2021 to 1Q 2025

Source: URA, HDB, ERA Research and Market Intelligence

In this light, property co-ownership transcends merely fulfilling housing needs; it also represents a strategic decision for long-term financial security. This is especially relevant for those who may not have children of their own and/or lack familial support in later stages of life.

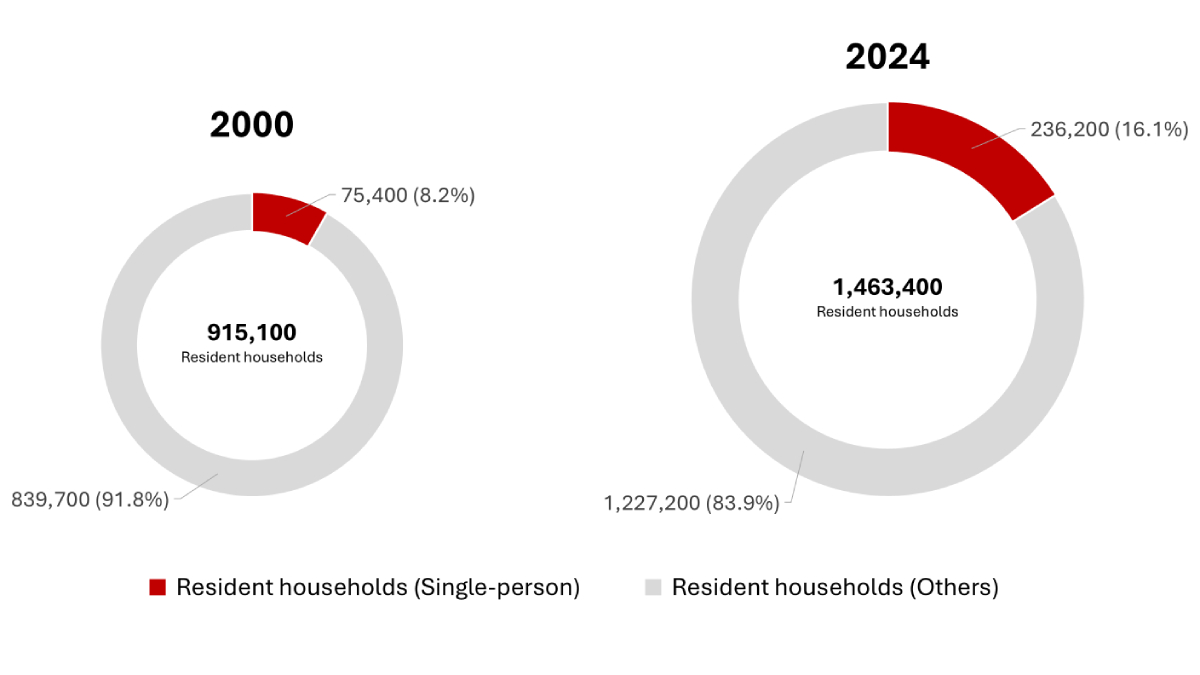

However, given the increasing proportion of singles in Singapore’s resident population, personal choice and/or a desire for freedom are likely the main factors influencing interest in alternative paths to homeownership, including co-ownership arrangements.

Chart 2: Growth in single-person households as a proportion of total resident households (2000 – 2024)

Source: SingStat, ERA Research and Market Intelligence

These beliefs tie in with a greater preference for single living as well, especially among Singaporeans seeking flexibility and privacy. Based on official SingStat figures, the number of single-person resident households has risen by over 200% from 75,400 in 2020 to 236,200 in 2024. Likewise, the share of single-person resident households has also seen a notable increase, doubling from 8.2% in 2000 (75,400 of 915,100 households) to 16.1% in 2024 (236,200 of 1,463,400 households).

Therefore, given the increasing prevalence of singlehood among Singaporeans, it is reasonable to suggest that there may indeed be a growing need to reimagine local homeownership beyond the traditional couple-centric model.

The Singapore Government has taken steps in this direction, with the most recent change being the expansion of public housing options for singles. A key policy revision in the second half of 2024 now allows singles – or, for co-ownership purposes, groups of up to four singles – to purchase 2-room Flexi HDB flats in any housing estate, including prime locations.

However, different homeownership requirements and considerations will apply depending on whether one is considering co-owning an HDB flat, an executive condominium (EC), or private housing.

What are the laws, rules and considerations for co-owning different residential properties for joint-singles?

Buying an HDB flat will require all parties to be at least 35 years old.

While HDB offers numerous eligibility schemes to support various demographic groups in their housing journey, single buyers interested in co-owning a flat need only focus on one: the Joint Singles Scheme.

Introduced in 1990, the Joint Singles Scheme allows eligible Singaporean men and women at least 35 years old to jointly purchase an HDB flat or Executive Condominium (EC). However, those who are widowed or orphaned may qualify from the age of 21, but only for resale Prime flats, unclassified resale flats, and new Standard and Plus flats.

For the purposes of this piece, we consider joint single households to be living arrangements involving two to four unmarried individuals of any gender. Additionally, if you intend to apply under the Joint Singles Scheme, it is important to take note of the following requirements:

Table 1: Joint singles eligibility criteria for HDB and EC flat purchases

Source: HDB, ERA Research and Market Intelligence

*Unclassified resale flats refer to HDB homes sold before the October 2024 sales exercise that do not fall under either Standard, Plus, or Prime classification categories.

Private home ownership is less cumbersome.

Unlike HDB flats or Executive Condominiums, purchasing private property as co-owners is not subject to specific eligibility criteria. However, co-buyers must consider the manner of holding or, more simply, how ownership is legally shared. This is particularly important for inheritance, as the selected holding method determines how the property is passed on after a co-owner’s death.

What are the different manners of holding or ownership types, and how do they matter in inheritance planning?

So, there are two property ownership types in Singapore, namely holding the property in Joint Tenancy and Tenancy-in-common. For HDBs, applicants under the Joint Singles Scheme must be registered as co-owners (i.e. the owner-occupier structure is not allowed).

While joint tenancy is the default holding method for HDB flats, buyers can opt for tenancy-in-common. However, this may come with higher legal fees due to the higher complexity of arrangements and the potential for disagreements.

- Joint Tenancy

Under a joint tenancy structure, there is an undivided interest in the property. All owners are regarded as owning the entire property collectively, with no separate or distinct shares. When one owner passes away, the rights of survivorship come into effect. This means that the surviving owner automatically inherits the rights to the full share of the property, irrespective of any existing will.

This is with the exception of when both parties pass away at the same time. In such cases, the order of death becomes legally significant. However, when it is impossible to determine (e.g., simultaneous death in an accident), Singapore law presumes that the younger person passes away later. Hence, the younger party will inherit the entire property before passing it on to their next of kin or will beneficiaries.

For example, Jamie and Ashley are both unmarried 35-year-old singles with no family, who decide to buy an HDB flat together under a joint tenancy arrangement. If Jamie passes away, Ashley will inherit full ownership of the flat.

Below, we have summarised the characteristics of both manners of holding:

Table 2: Summary of manner of holding of property

Source: ERA Research and Market Intelligence

- Tenancy-in-Common

Under the tenancy-in-common structure, owners can agree on their respective ownership percentages, provided they total 100%. For instance, if one party pays for 70% of the property and the other covers 30%, they hold a 70-30% share. These shares are detailed in the title deed. Upon death, each owner’s share will pass to their respective estate rather than to the surviving owner.

If all owners pass away simultaneously, each owner’s share will be allocated to their respective beneficiaries under their wills or according to the Intestate Succession Act if no will exists. The assets will be divided in accordance with the act.

Table 3: Common beneficiaries under the Intestate Succession Act*

Source: Singapore Statutes online (sso.agc.gov.sg)

* The Intestate Succession Act does not apply to Muslims. The estate of a Muslim is governed by Muslim law. ** ‘Issue’ is a legal term referring to one’s direct descendants.

The Tenancy-in-Common ownership structure would be ideal for two parties who have their own estates to pass on the property to, such as divorcees or widows with children, coming together to jointly purchase a property.

For instance, Lewis and Jesse own 70% and 30% of a condominium unit, respectively. If Jesse were to pass away, his share (70%) would go to his estate according to his will, while Lewis would continue owning 30% of the property.

Beyond legalities, what else should you consider before co-owning a residential property?

For many, the legal, emotional, and financial advantages of co-owning a property outside of marriage are very real. Still, it is equally important to recognise the responsibilities and risks that come with it.

Firstly, just as in marriages, breakdowns in relationships between co-owners can make living together challenging. However, unlike most relationships, where it is possible to walk away from the other party, you will be tied to the shared property unless both parties reach a consensus on future ownership.

The same goes for scenarios where financial difficulty is a concern. If one party is unable to cover their share of costs (e.g., mortgage, maintenance fees), the financial pressure may unfairly fall on the rest.

Lastly, inheritance disputes could arise even if a manner of holding or inheritance has been specified. For instance, in an emotionally charged situation, family members of a deceased co-owner may still choose to contest a will despite its legal standing.

For these reasons and more, all parties involved should establish a shared understanding and make definitive arrangements on how ownership should be handled in good times and in bad, before proceeding with a purchase.

Beyond formalising the manner of holding, prudent buyers may also consider drafting a will to facilitate smooth and unambiguous future transfers, particularly when a joint tenancy is involved. Likewise, a consultation with legal and real estate professionals is recommended for more precise understanding and informed guidance. Because just as with the people you love, those you share a roof with deserve nothing less than care and clarity.

Disclaimer

This information is provided solely on a goodwill basis. It does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For the avoidance of doubt, ERA Realty Network and its salesperson accept no responsibility for the accuracy, reliability and/or completeness of the information provided. ERA owns the copyright in this publication, and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.

This article was first published on EdgeProp, featuring expert insights and opinions from Mr. Marcus Chu, CEO of ERA Singapore, ERA Asia Pacific & APAC Realty.

With 29 years of experience in real estate, including four years as the CEO of ERA Singapore, I have had the unique opportunity to witness firsthand the numerous transformations that have influenced Singapore’s real estate scene.

Over numerous building projects, Singapore’s master planning has reshaped our skyline and established a solid foundation for our nation’s and its people’s ongoing development. At the same time, our government has shown a strong commitment to maintaining housing stability by directly addressing market challenges.

Singapore has shown remarkable resilience despite many obstacles, from addressing early land shortages to managing recent pandemic-fuelled supply disruptions.

Similarly, major financial crises have provided transformative insights that led to the implementation of structural protections such as the total debt servicing ratio (TDSR) and the mortgage servicing ratio (MSR).

A resilient market, now tested

As Singapore celebrates its 60th anniversary this year, many reasons exist to take pride in our policy and nation-building accomplishments.

Nevertheless, ongoing success also requires honest reflection and adaptability. Just like past events and demographic shifts have greatly transformed our property market, new trends will continue to emerge — and they will require proactive engagement to ensure local housing stays inclusive and accessible.

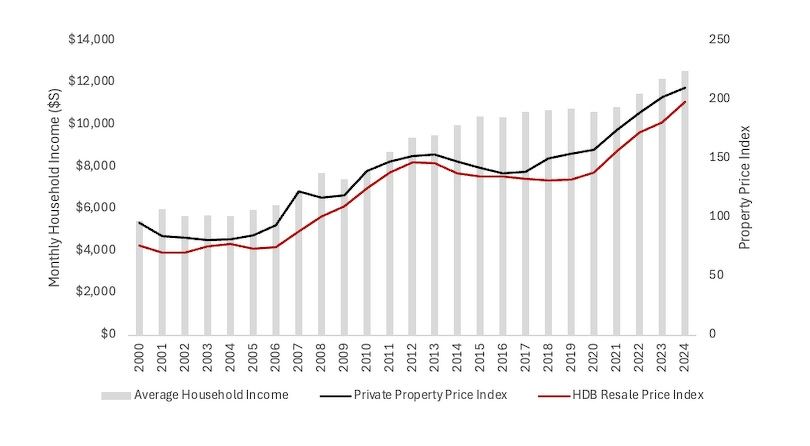

In the last 20 years, average household incomes in Singapore have increased by 111%. Yet, this uptick in earnings has been outpaced by a booming property market, with the Private Property Price Index climbing 148% and the HDB Resale Price Index soaring by an astonishing 169% during the same period.

Median household income versus property price growth (2000 – 2024)

Source: SingStat, URA, HDB, ERA Research & Market Intelligence

The widening gap between income and prices has presented significant challenges to affordability for those seeking to purchase private homes. Although the increase in HDB resale prices has been advantageous for some, many struggle to upgrade due to the parallel rise in private property values.

Executive condominiums (ECs) have become a practical middle-ground choice in this climate. They offer premium condo-style living at a subsidised price in return for stricter eligibility requirements, including an income ceiling of $16,000 and limits on the MSR.

However, despite the continued strong allure of ECs, younger first-time homebuyers now face a steeper path to entry due to rising EC prices and higher upfront cash. In contrast, second-timers often have accumulated housing equity to leverage, and with the deferred payment scheme, it becomes easier for them to purchase an EC.

As concerning as these affordability pressures may be, they are not the only challenges for today’s homebuyers, especially given the broader socio-economic patterns reshaping Singapore’s housing market.

Forces reshaping housing in the next decade

With one in four Singaporeans projected to be 65 or older by 2030, policymakers must address the impending silver tsunami and its extensive socio-economic implications. For instance, alongside this demographic shift, we have observed the growing influence of wealth transfers in driving housing demand.

We have seen a growing number of private homeowners right-sizing in hopes of tapping into their housing equity for retirement while still owning a property that holds value. Simultaneously, some younger homebuyers are now benefiting from parental wealth transfers. It underscores the generational wealth disparity and the widening gap between income growth and housing price appreciation.

On the supply side, rising land costs are also contributing to the growth of private housing prices. Locally, developers acquire land through the Government Land Sales (GLS) programme via a competitive bidding process, where the highest bidder is typically awarded the tender, provided the bid is above the reserve price. This dynamic often drives land prices upward, and more so in desirable locations.

Separately, as part of Singapore’s efforts to meet net-zero emissions by 2050, the government’s carbon pricing strategy will see the carbon tax rise to $25 per tonne of carbon dioxide equivalent (tCO2e) in 2024 and 2025 and $45 tCO2e in 2026 and 2027, with a view to reaching $50–80 tCO2e by 2030. These hikes are set to drive construction costs up, potentially impacting future housing prices.

Better to invest in a home today, instead of waiting for tomorrow

With the abovementioned trends so deeply entrenched in our real estate market, home prices are anticipated to remain stable. Hence, instead of finding the “perfect time” to enter the property market, the wiser approach is to maximise your time. After all, real estate has consistently shown its long-term investment potential with its track record of steady appreciation over time.

For young homebuyers, the most logical first step is to secure a Build-to-Order (BTO) flat as their starter home. BTOs come with a range of subsidies and grants that significantly reduce the cost of homeownership. That will set the stage for future asset progression opportunities.

Buyers should also remain open-minded to take advantage of the first-mover advantage. After all, Singapore’s efficient urban planning ensures that no area is left underdeveloped for long. Identifying these emerging neighbourhoods in advance allows buyers to capitalise on attractive entry prices and potentially benefit from future growth as the area matures and infrastructure improves.

Therefore, planning, patience, and foresight are the keys to unlocking a home and acquiring growth opportunities in real estate. At the same time, buyers should also bear in mind that your journey in real estate isn’t a plan for tomorrow — it’s a future that starts now.

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.

下文由ERA公关经理岳开新翻译

此前我们曾探讨过,延长中央商务区奖励计划(CBD Incentive Scheme,简称CBDI)与战略发展奖励计划(Strategic Development Incentive Scheme,简称SDI)对振兴中央商务区所起的重要作用。这些计划为市中心老旧建筑的重建注入了活力,成为城市更新的重要催化剂。如今,作为中央商务区的延伸区域,滨海南将肩负起重塑新加坡城市景观的关键使命,揭开发展新篇章。

中央商务区的演变

19世纪

新加坡最早的商业区可追溯至19世纪初,当时商业活动沿新加坡河两岸逐步展开。凭借海上丝绸之路的战略地位,新加坡迅速崛起为重要自由港,成为中国、印度与东南亚之间贸易的枢纽。

当时,驳船码头(Boat Quay)、克拉码头(Clarke Quay)及莱佛士坊(Raffles Place)一带陆续建起大量店屋,支撑快速发展的贸易活动与日益壮大的商圈。银行及其他相关企业也随之进驻,逐步形成新加坡首个真正意义上的商业核心区。

来源:郭尚慰收藏,PictureSG,新加坡国家图书馆

进入20世纪初,随着新加坡港口地位不断上升,商业区开始面临严重拥堵问题。由于缺乏系统的城市规划,商铺、住宅与工厂混杂分布,造成道路阻塞、污染加剧,引发公众对健康与环境的担忧。

为应对这些挑战,新加坡政府在1960至1970年代启动大规模城市提升计划,旨在以更有序的方式重塑城市面貌。

1966年出台的《土地征用法令》(Land Acquisition Act)和1967年政府售地计划(Government Land Sales, 简称GLS)的推出,有效解决了土地所有权零散的问题,并为私人开发设立了更透明、规范的土地获取机制。这些政策为现代中央商务区的发展奠定了坚实基础。

迈向现代化的摩天商务区

在城市规划框架下,下一阶段的发展聚焦于建设高层办公大楼,推动中央商务区的现代化。Hong Leong Building(1976年)、华侨银行中心(OCBC Centre,1976年)、大华银行广场(UOB Plaza,1972年)和新加坡置地大厦(Singapore Land Tower,1980年)是首批拔地而起的摩天大楼,至今仍屹立在新加坡的天际线中。

这些高楼不仅重塑了城市轮廓,也满足了不断增长的办公空间需求,为新加坡金融中心的发展提供了基础设施支撑。

进入2000年代,新加坡作为区域金融枢纽的地位愈发稳固,带动了对高品质办公空间的持续需求。与此同时,商业价值稳步上扬,空置率维持在低位,吸引大量机构与私人投资者将目光投向这一市场,以期实现长期资本增值与稳定回报。

此外,中央商务区拥有覆盖全岛的交通网络,连通性强,大幅提升商务便利性。作为新加坡商业生态的核心枢纽,中央商业区不仅承载着贸易与商务活动,也促进了企业间的交流与合作。

在2024年全球金融中心指数(Global Financial Centres Index)中,新加坡在全球133个金融中心中排名第四,进一步巩固了其作为全球领先金融枢纽的地位。这一成就或将进一步推升对优质办公空间的需求。随着现有中央商业区发展逐渐饱和,且社会对绿色可持续发展的呼声日益高涨,滨海南的开发无疑为新加坡商务区的扩展提供了恰逢其时的契机。

滨海南:新加坡全新可持续综合社区的诞生

资料来源:市区重建局

资料来源:市区重建局

滨海南将被打造为一个集住宅、零售、酒店、办公与生活配套设施于一体的综合用途社区,各类设施皆可在10分钟步行范围内轻松抵达。根据总体规划,该区域正通过政府售地计划,由市区重建局主导转型升级。

2023年,由鑫丰集团(Kingsford Group)牵头的财团以每平方英尺每容积率(psf ppr)1402元的最高报价成功竞得滨海花园巷(Marina Gardens Lane)地块,计划建设937个住宅单位,将在2025年正式推出,成为滨海南首批亮相的地标性项目。

资料来源:鑫丰集团

紧接着在2024年1月,滨海花园弯(Marina Gardens Crescent)的一块白地地段仅收到国浩房地产(GuocoLand)牵头财团的一项报价,报价为每平方英尺每容积率984元。然而,市区重建局认为该报价未能体现土地应有价值,决定不予接受,并选择暂时保留地块。

这一决定充分彰显了市区重建局在维护国家土地资产价值方面的坚定立场与长远眼光。

结语

随着新加坡持续吸引全球企业与高端人才,滨海南将在未来城市发展的蓝图中扮演至关重要的角色。它不仅是一个现代化、绿色可持续、以人为本的社区,支撑着国家的经济增长,更是一个全新、充满活力的宜居住宅区——一个让新加坡人率先安家的地方。

如您有兴趣了解滨海南将为未来业主与租户带来哪些生活与投资机遇,欢迎随时联系 ERA 值得信赖的房产顾问,获取更多资讯!

本文中的信息仅供参考,不构成对信息的准确性、完整性或可靠性的保证。使用者应自行核实相关信息,并根据具体情况向独立的专业人士(如估价师、财务顾问、银行从业人员及律师)寻求专业意见。ERA及其销售人员对于因使用本信息而导致的任何直接或间接损失概不负责。此外,本文件受著作权法保护,ERA拥有其著作权。未经事先书面许可,任何个人或机构不得以任何形式或手段对本文件进行复制、传播或用于商业用途。

下文由ERA公关经理岳开新翻译

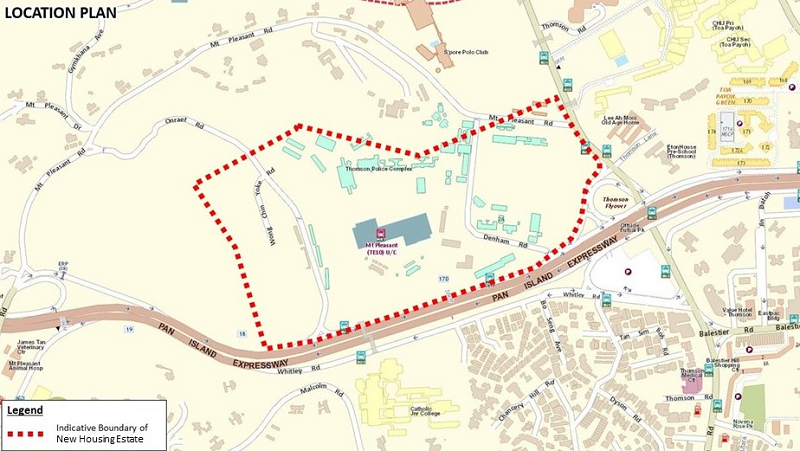

在2025年财政预算案中,黄循财总理宣布了一系列与住房市场相关的政策。其中一项是:政府将在今年10月首次于快乐山(Mount Pleasant)地区推出预购组屋(BTO)项目。

快乐山位于新加坡中部,其名称源自区内的一座小山丘。该地区因保留了大量殖民时期的“黑白洋房”而闻名,这些洋房曾是已拆除的旧警察学院高级官员的住所。如今,包括警察学院旧址在内的33公顷土地将被重新规划,用于建设新的BTO住宅区。

图一,即将建设快乐山预购组屋项目范围

那么,这个新组屋区能带来哪些期待?

快乐山组屋区可被视为大巴窑的延伸,因此也将享有与城市边缘地区相似的便利与交通连通性。尽管目前项目周边缺乏生活配套,但其邻近大巴窑、马里士他和汤申等成熟社区,居民可以轻松享用这些区域的完善设施。

由于地理位置接近市中心,并且将直接连接地铁站,该项目预计将被归类为“优选地段”(Plus)或“黄金地段”(Prime)项目,类似近期推出的碧湾(Bayshore)和丹戎禺(Tanjong Rhu)项目。

这意味着项目将受到更严格的转售和出租限制,例如:10年的最低居住年限、转售时的津贴回收机制,以及转售买家的收入上限。

值得一提的是,快乐山距离的大巴窑西部长期以来都是百万组屋交易最活跃的区域之一。而距离该项目最近的现有组屋,就位于靠近加利谷地铁站(Caldecott MRT)的大巴窑西部。

地理优势:学校、设施与交通连通性

学校

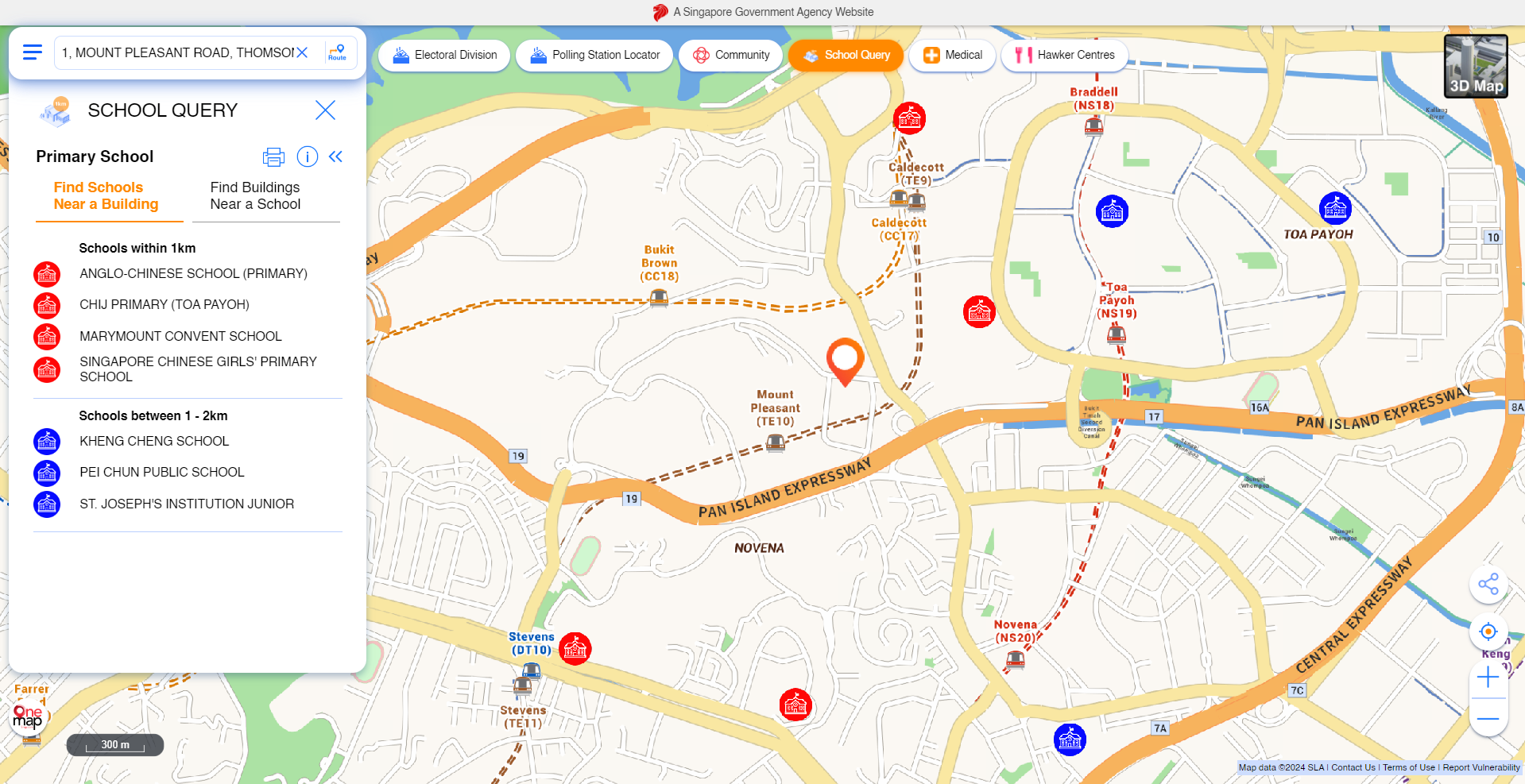

对于已有或计划要孩子的家庭来说,快乐山组屋区很可能位于一些热门小学1公里内,当然具体情况仍有待政府最终确认。

目前,英华小学(ACS Primary)就在1公里范围内,但预计将在2030年迁至登加(Tengah)新校址。现有校址未来是否会被保留为教育用途,或改作其他发展用途,还尚未明确。

图二:快乐山组屋项目周边的学校

资料来源:OneMap、市区重建局、ERA研究与市场情报(截至2025年5月8日)

未来转售潜力如何?

目前该地区尚无组屋项目,但可作参考的最近项目是位于大巴窑西部、大巴窑1巷(Lorong 1 Toa Payoh)一带,且靠近加利谷地铁站。

这里新组屋供应有限。截至今年5月,大巴窑组屋区屋龄少于15年的三房式及以上单位仅有2,727个,供应有限。这种稀缺性已成为推动当地组屋价格持续上涨的主要原因之一。

数据显示,在过去一年内,屋龄不超过15年的四房式组屋平均转售价高达107万元,而五房式组屋更是达到惊人的138万元。

表一:屋龄少于15年的四房及以上组屋的平均转售价

资料来源:市区重建局、ERA研究与市场情报(截至2025年5月7日)

是否意味着成功申请到快乐山预购组屋就如同中大奖呢?恐怕事情并没有那么简单。

从靠近市中心的优越位置,到便利的地铁连接,再到被中央集水区绿意环绕的环境,加上邻近大巴窑西部组屋的强劲价格表现,种种因素的确为该项目的未来转售潜力提供支撑。

但与此同时,若该项目最终归类为“优选”或“黄金地段”,其更严格的转售政策可能在一定程度上抑制投机性需求。

值得注意的是,在即将到来的7月预购组屋中,位于大巴窑的一个项目也可能被归类为“优选地段”,其定价和政策或可为快乐山项目提供参考。

结语

如果你是首次购屋者,快乐山组屋项目是一个值得考虑的选项吗?

与其他预购组屋不同,它将建于城市边缘一块保留用地上,是全新打造的住宅区。而大多数新项目如登加、碧湾等,位置相对偏远。

此外,项目不仅靠近第10和第11邮区这些高端地段,还直接连接地铁站,交通便利,使其成为吸引力十足的居住地区。对于希望靠近家人(如住在大巴窑、史蒂芬或诺维娜)的购房者而言,这也可能是一个理想的选择。

本文中的信息仅供参考,不构成对信息的准确性、完整性或可靠性的保证。使用者应自行核实相关信息,并根据具体情况向独立的专业人士(如估价师、财务顾问、银行从业人员及律师)寻求专业意见。ERA及其销售人员对于因使用本信息而导致的任何直接或间接损失概不负责。此外,本文件受著作权法保护,ERA拥有其著作权。未经事先书面许可,任何个人或机构不得以任何形式或手段对本文件进行复制、传播或用于商业用途。

During Budget 2025, Prime Minister Lawrence Wong made a series of announcements with regards to the housing market. Among them was the official confirmation that we will see the inaugural launch of public housing Build-To-Order (BTO) flats in Mount Pleasant during the October 2025 BTO launch.

Mount Pleasant, located in the central region of Singapore, named after a hill located within its boundaries. The area is well known for its many black and white bungalows, which used to be home to senior officers of the (former) Police Academy, which has since been torn down. 33 hectares of land, inclusive of the former location of the police academy and its surrounding areas will now house these BTO projects.

The boundaries of the upcoming Mount Pleasant public housing estate

What can we expect from this new housing estate?

This Mount Pleasant HDB estate can be seen as an extension of Toa Payoh – its nearest and adjacent HDB town. It will experience the same city-fringe convenience and connectivity. While there are currently no amenities located in the immediate vicinity, residents can take advantage of the estate’s proximity to Toa Payoh, Balestier and Thomson, where there are plenty of amenities to be found.

Considering its location being near the central region of Singapore, and having immediate access to an MRT station (such as Bayshore and Tanjong Rhu that have launched recently), we can expect this project to be a Plus or Prime project. In short, they would come with tighter resale and rental restrictions, such as a longer 10-year Minimum Occupation Period (MOP), subsidy clawback upon resale, and a resale income ceiling.

Moreover, its neighbouring and closest HDB town, Toa Payoh, is regularly among the top five HDB towns in the number of million-dollar flats transacted annually. The closest HDB flats to the Mount Pleasant housing estate are those located in Toa Payoh West, within the vicinity of Caldecott MRT station.

Location attributes: schools, amenities, transport and connectivity

Schools

Those with or looking to have children (particularly daughters) will be pleased to know that the Mount Pleasant HDB estate will very likely be within the 1km priority enrolment distance of prominent primary schools, such as But this is subject to eventual confirmation by the government.

ACS Primary currently sits within 1km of the site, but is expected to shift to its new location in Tengah in 2030. It is unsure if the grounds that hold the current school will be repurposed to host another school in the future, or be used for other forms or urban redevelopment.

Image 2: Schools within the vicinity of Mount Pleasant Road, where the projects will be built around

Source: OneMap, ERA Research and Market Intelligence as at 8 May 2025

What About Future Resale-ability?

While there are no existing housing projects in the direct locale, the nearest comparable projects would be those located in Toa Payoh West, along Lorong 1 Toa Payoh and close by to Caldecott MRT station.

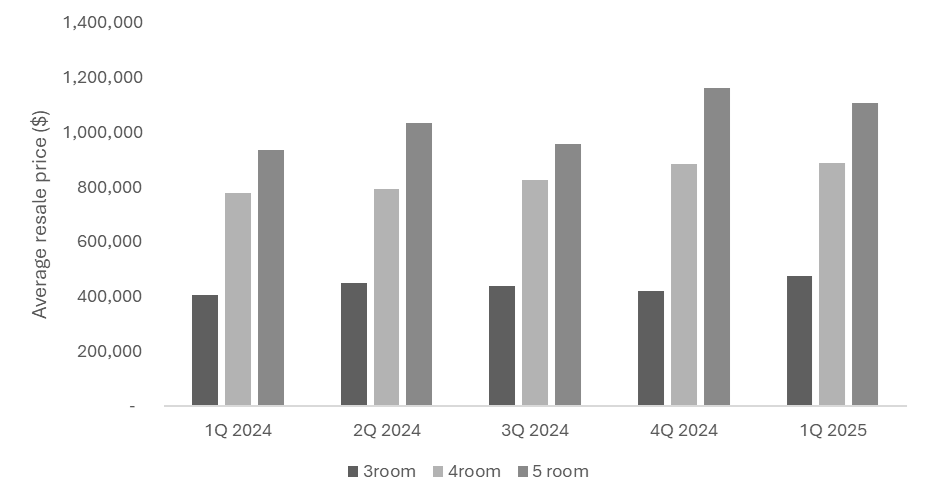

There is a lack of newer flats in the locale around Toa Payoh West/Caldecott MRT. As of May 2025, there are only 2,727 3-room and larger flats under 15 years of age in Toa Payoh town itself. Their scarcity has caused property prices to grow at an extremely fast pace in the area.

In fact, the average resale price of 4-room flats aged under 15 years in this sample area was $1.07 million, with the average for 5-room flats at a whopping $1.38 million across the past year.

Chart 1: Average resale prices of 4-room and larger HDB flats under 15 years old

Source: HDB, ERA Research and Market Intelligence as at 7 May 2025

Does this necessarily mean that scoring a unit in the Mount Pleasant BTO launch is the next golden ticket? The answer might not as straightforward as it seems.

A combination of factors make these projects attractive for future resale buyers: from its city fringe location, doorstep MRT convenience, and charming location surrounded by the lush greenery of Singapore’s central water catchment areas. All of this is on top of the fantastic price performance of nearby Toa Payoh West resale flats, which share some of the same attributes.

This demand will be therefore balanced by the fact that these projects will be classified most likely under “Prime”, or at the very least “Plus”. In the upcoming July BTO launch, we will see a Toa Payoh project, that is likely to fall under the Prime category as well. The categorisation and pricing of that project will likely be indicative of what to expect from the upcoming Mount Pleasant HDB project.

Conclusion

If you are a first-time homebuyer, could the Mount Pleasant HDB project be something worth considering?

The project differs itself from other BTO flats as it is an entirely new housing estate built on a conserved piece of land in the city fringe. Most other projects in new, or up-and-coming estates are located in farther-out satellite towns, such as Tengah, or the future Bayshore precinct.

Its unique locational and features stand out with its close proximity to prime districts 10 and 11, and access to an already-built MRT station. This is an extremely convenient location to stay in – connectivity wise, and is sure to attract homebuyers purely for that reason. This project could also be a great option for those who want to stay close by to family residing in Toa Payoh, Stevens, or Novena.

BTO flats with strong locational attributes are now balanced by having tighter resale restrictions – buyers now have to exercise more discretion when applying for a new flat.

However, if your primary objective is asset progression, you are probably better off going for one of the standard projects in the year. A standard flat with a 5-year MOP would be the most flexible when it comes to resale restrictions, allowing for swift progression in your property journey.

Overall, everyone’s property journey is unique – being presented with the facts, you can now decide if Mount Pleasant’s BTO project is the right move for you. If you have any further inquiries, do not hesitate to reach out to an ERA trusted adviser today!

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.

下文由ERA公关经理岳开新翻译

尽管全球局势动荡,但新加坡经济稳定确保本地住宅市场有足够韧性来应对挑战。

2025年4月2日,美国总统特朗普在美国解放日(Liberation Day)发布了一项超出预期的关税政策,震惊全球市场。根据这一政策,除了对所有进口商品征收10%的统一基准关税外,部分国家将面临更高的关税。

美国此举的动机明确:通过调整价格竞争力,推动国内外商品之间的公平竞争,从而吸引制造业回流美国,并提振国内消费。自2001年以来,美国制造业在全球产出的占比已从28.4%下降至2023年的17.4%,而2024年,美国商品贸易逆差已达到1.2万亿美元。

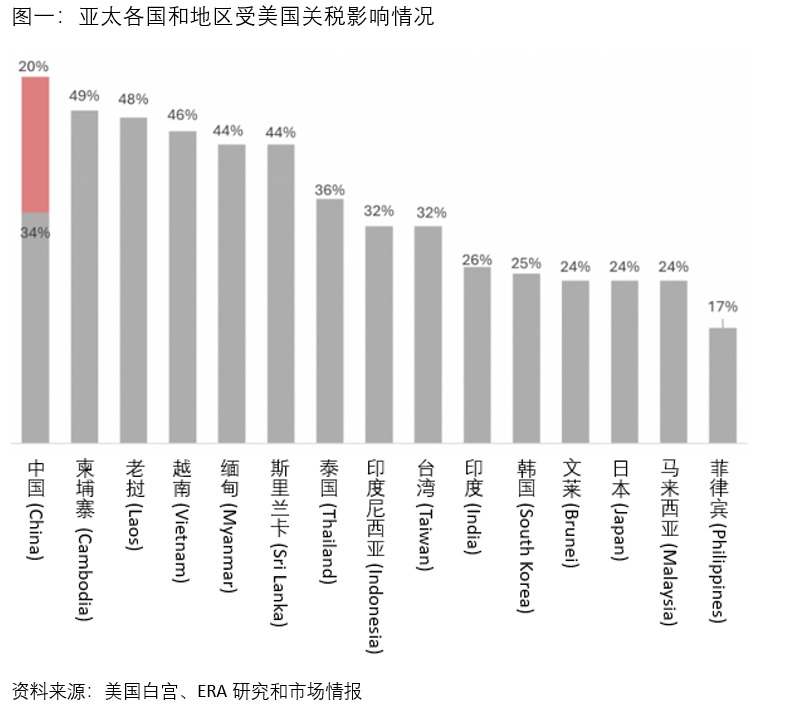

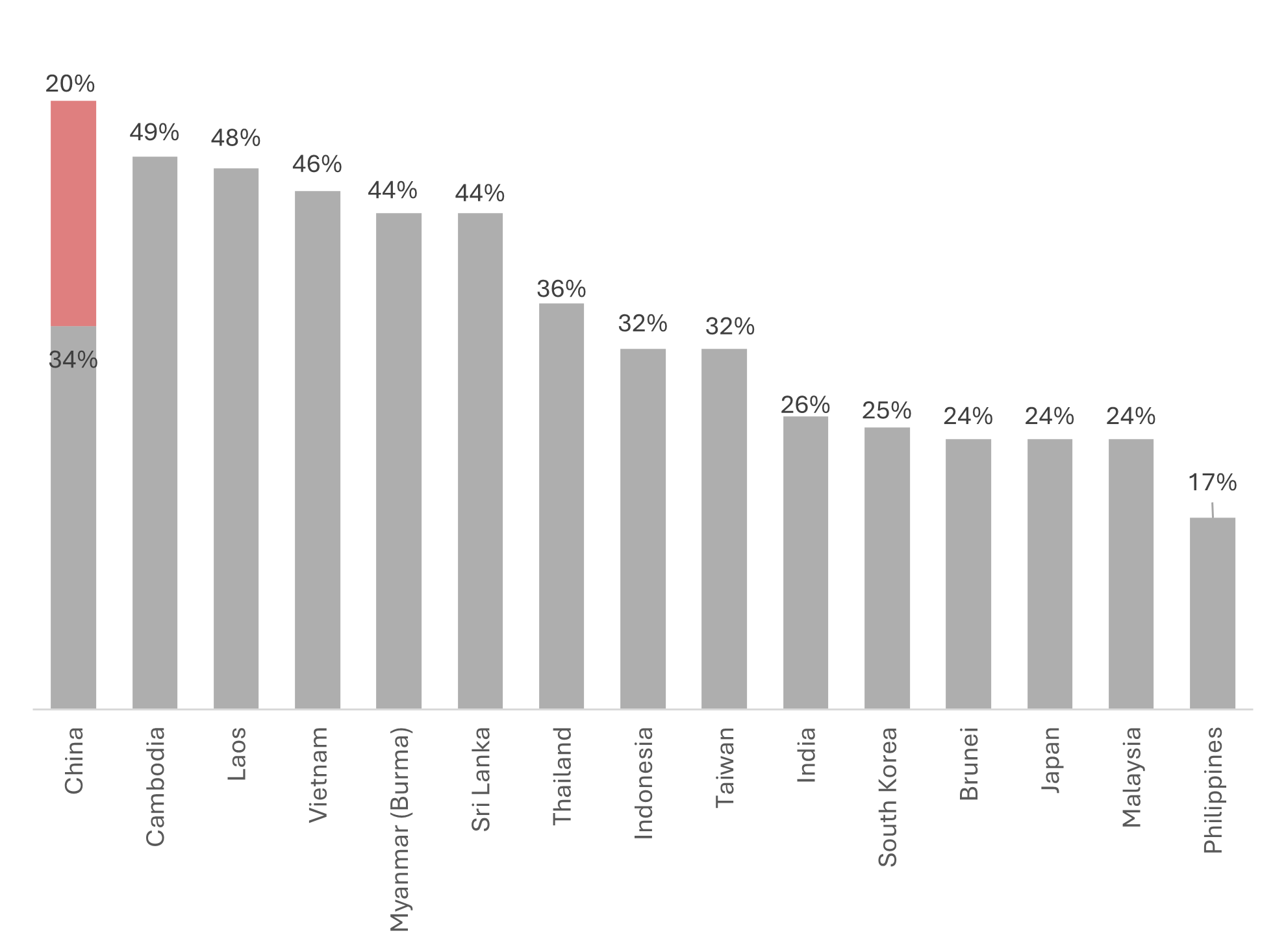

在受影响的国家中,中国是这场贸易战加剧的主要目标,除了此前已施加的20%关税外,还需再承受34%的额外关税。同时,一些东南亚国家也受到重创。例如,柬埔寨(49%)、老挝(48%)和越南(46%)是受新关税影响最为严重的市场之一。尽管新加坡不在高关税国家名单中,但我们的对美出口同样会受到10%基准关税的影响。

全球股市暴跌,美国经济可能因通货膨胀和他国报复性关税而受创

新关税政策实施后的第一个交易日,投资者的恐慌情绪引发了全球股市的暴跌,并激发了市场对经济衰退的担忧。

美国这一强硬举措迅速引发了贸易伙伴的报复性关税对策。例如,中国几乎在第一时间对所有美国进口商品加征了34%的关税。

与此同时,美国国内进口成本的上升可能加剧通货膨胀,进一步加重消费者和企业的负担。全球范围内,这可能导致贸易需求放缓,从而拖累整体经济增长。

市场的担忧会影响新加坡住宅市场吗?

在这一轮新关税中,美国对新加坡进口商品设定了10%的关税,低于其他亚太国家。此外,新加坡决定不采取报复性关税,以避免贸易战升级。尽管新关税政策带来的不确定性会对全球经济增长产生压力,而新加坡作为一个高度依赖贸易的国家,难免会受到一定影响。

但从另一个角度看,本地的房产投机可能会减少,购房者将更多地倾向于刚需和长期计划。

短期内,尽管全球经济不确定依旧存在,且贸易战升级的风险可能会抑制住宅市场的需求,但从中长期的展望来看,ERA仍保持谨慎乐观的态度。ERA认为,新加坡住宅市场本身并不具投机性,坚实的经济基本面将为中长期投资者提供稳定的增长机会。

高通胀和经济增长放缓,或使美联储最多实施四次降息

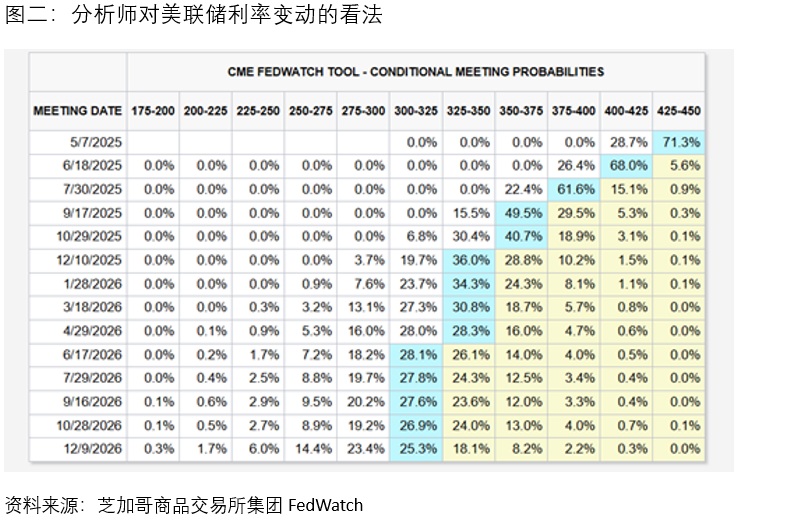

根据芝加哥商品交易所集团(CME)的调查,分析师认为美联储可能在今年实施最多四次降息,主要由于贸易关税引发的更高通货膨胀和经济增长放缓。如果这一预期成真,联邦基金利率可能会降至3.25%至3.50%之间。这将有助于进一步缓解房贷利率,减轻购房者的房贷负担。

需求放缓及进口成本下降有望使建筑成本上涨趋于缓和

如果中国决定将其过剩产能转向其他国家,并以更低的价格进行出口,可能会导致亚太地区面临通缩压力。具体到建筑行业,由于中国房地产市场的放缓,国内需求减弱,钢筋价格已有所下滑。此外,美国对钢材进口加征25%关税,进一步打击了钢材需求,尤其是削弱了中国钢铁的出口。

在这样的背景下,亚太地区可能面临廉价钢材大量涌入的风险,这将有助于降低建筑材料成本。然而,建筑材料成本的下降是否能够有效缓解房价压力仍需观察。即使未来建筑成本下降,对房价的影响可能有限,因为新加坡的房价受多种因素影响,包括土地成本、劳动力成本等。

新加坡作为避风港,预计将持续吸引外国投资,这有助于保障就业并支撑住房需求。

新贸易关税的实施预计将有效遏制企业的“中国加一”(China Plus One)策略,该策略旨在降低对中国制造的依赖,并减轻贸易战带来的影响。受新政策影响,区域内许多低成本制造业可能因更高的贸易关税面临挑战。

然而,新加坡与美国始终保持着平衡互利的合作关系。2024年,美国对新加坡的货物贸易顺差达到了28亿美元,这进一步巩固了新加坡作为美国可信赖贸易伙伴的地位,可能使新加坡免于面临更苛刻的关税政策。

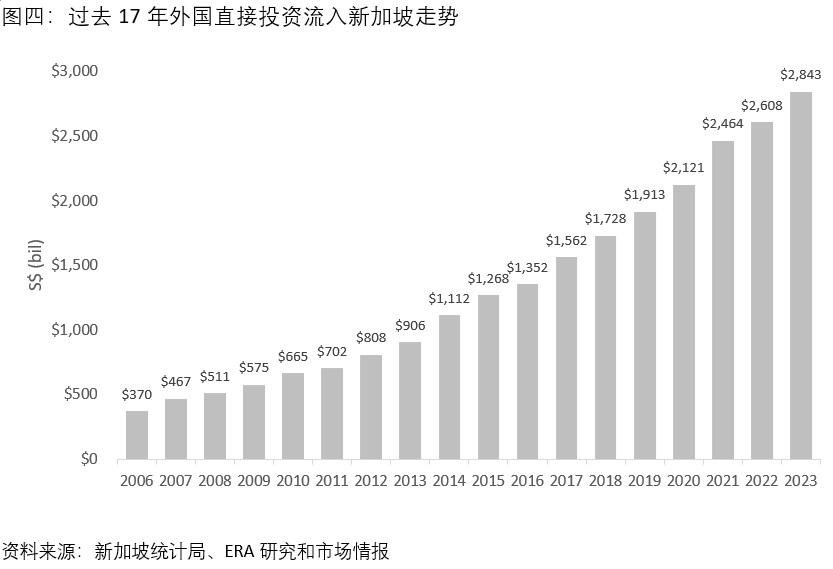

在当前形势下,寻求避风港与增长机会的区域投资者预计将继续被新加坡稳定的社会环境以及透明、开放的经济政策所吸引。这将推动外国直接投资(FDI)的持续流入,促进整体经济发展,并创造更多就业机会,进一步支撑住宅与商业地产的需求。同时,新加坡作为国际金融中心的地位以及健全的法律体系,在全球经济不确定性加剧的背景下,更加巩固了其作为投资首选地的吸引力。

新加坡多元化的经济结构和广泛的多边贸易伙伴关系有助于缓解经济冲击

新加坡多元化的经济结构和广泛的贸易伙伴网络将有效减轻个别国家贸易关税的影响。截至目前,新加坡已签署27项自由贸易协定,并将继续推动并维护与志同道合国家之间的开放、公平和自由贸易关系。

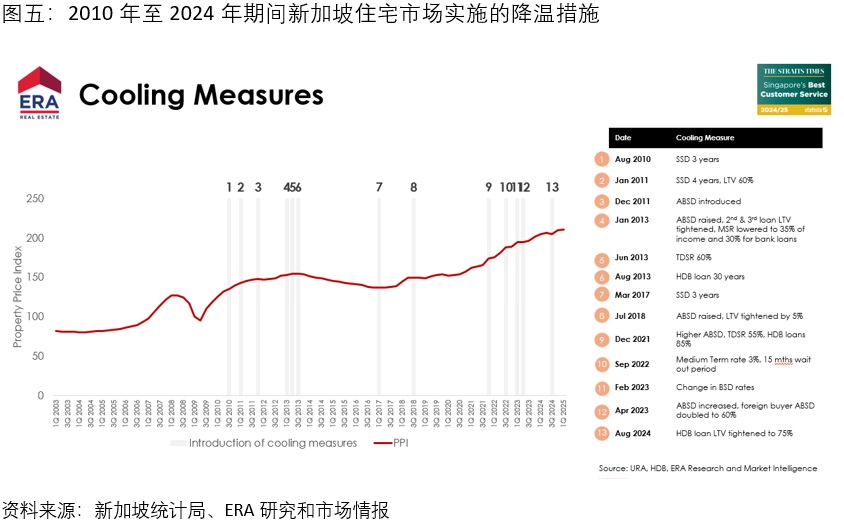

住宅市场的降温措施为应对外部冲击提供了灵活应对空间

自2010年至2024年,新加坡政府共推出了13轮降温措施,以稳定住宅市场并确保价格的可持续增长。

这些措施包括在2023年4月实施的60%的额外买家印花税(ABSD),旨在打击外国买家的投机性投资。此外,政府对购买二套房的买家征收较高的ABSD,以抑制房产的过度积累,帮助平抑房价增长,维护市场稳定。

总结

综上所述,尽管面临全球经济挑战,ERA依然对新加坡住宅市场在中长期保持积极展望。

新加坡政府已经为此奠定了坚实的基础,包括签署广泛的自由贸易协定、发展先进的基础设施以及培养高素质劳动力。这些努力为新加坡吸引持续的外国投资创造了有利条件,而外国投资是推动新加坡长期经济增长的关键驱动力,并为本地创造了大量就业机会。

住房方面,政府采取务实的措施,既能有效跟上需求增长,又能避免过度投机性资产积累。政府始终将保障住房可负担性作为核心目标,并通过可持续的价格增长实现这一目标。此外,政府实施的多轮降温措施为应对外部经济冲击提供了充足的空间,能够迅速作出反应。

总之,新加坡房地产市场建立在韧性、远见和审慎治理的基础上。ERA相信,在持续的政策支持和强劲的需求推动下,新加坡的住宅市场将继续展现增长潜力和长期价值,为购房者提供机会,也为投资者创造回报。

本文件中的信息仅供参考,不构成对信息的准确性、完整性或可靠性的保证。使用者应自行核实相关信息,并根据具体情况向独立的专业人士(如估价师、财务顾问、银行从业人员及律师)寻求专业意见。ERA及其销售人员对于因使用本信息而导致的任何直接或间接损失概不负责。此外,本文件受著作权法保护,ERA拥有其著作权。未经事先书面许可,任何个人或机构不得以任何形式或手段对本文件进行复制、传播或用于商业用途。

The world may be “shook”, but the firm economic fundamentals ensure that the Singapore’s residential market is well-positioned to weather the storm.

On Liberation Day, 2 April 2025, President Donald Trump shook the world by unveiling a higher-than-expected Reciprocal Tariff Policy. In addition to a sweeping 10% baseline trade tariff on all imports, selected countries will face steeper trade tariffs under the policy.

The implementation of this tariff policy holds clear motivations. US manufacturing has declined from 28.4% of global output in 2001 to 17.4% in 2023, while United States goods trade deficit has reached US$1.2 trillion in 2024. Through this move, President Donald Trump aims to level the playing field on pricing, which in turn, could bring manufacturing jobs back to United States and boost domestic consumption.

While China, the primary target in the deepening trade war faces a 34% tariff on top of the earlier imposed 20%, several smaller Southeast Asia Markets are also deeply impacted. Cambodia (49%), Laos (48%) and Vietnam (46%) are among the markets that are worst hit by the new tariffs. Despite not on the list of countries affected by higher tariffs, Singapore will still be subjected to the 10% baseline tariffs on our exports to the United States.

Chart 1: Asia Pacific Markets impacted by higher trade Tariffs imposed by United States

\

\

Source: The White House, ERA Research and Market Intelligence

Global stock markets plunge, while the United States could potentially face whiplash from rising inflation and retaliatory tariffs

As the trade war intensifies, uncertainty and fear among investors sent global stock markets plunging on the Monday following the implementation of the Reciprocal Tariff Policy on 5 April 2025. More importantly, these developments have sparked fears of a broader economic downturn.

This aggressive move by the United States could provoke retaliatory tariffs from trade partners, such as China, which almost instantaneously retaliated with a 34% levy on all US imports.

Meanwhile, domestically, rising import costs may fuel inflation and put further pressure on consumers and businesses in United States. Globally, this could spell slower trade demand, which could translate to slower growth.

For now, the market may be gripped by heightened volatility, but what can we expect for the Singapore residential market?

Singapore will face a moderate impact due to the lower baseline 10% trade tariff and has decided against retaliatory tariffs. However, other countries may choose to retaliate and further intensify the ongoing trade war. This heightened volatility will weigh on global economic growth, and on Singapore’s growth, given our heavy reliance on trade.

On a more positive note, residential homebuyers tend to be less speculative, often taking a medium- to long-term view of the market and are more likely to be driven by genuine housing needs.

Although uncertainty persists and the risk of an escalating trade war may dampen near-term demand in the residential market, ERA maintains a cautiously optimistic medium- to long-term outlook. ERA believes that Singapore’s residential sector is non-speculative and will continue to offer growth opportunities for investors with a medium- to long-term perspective, supported by several key fundamentals.

-

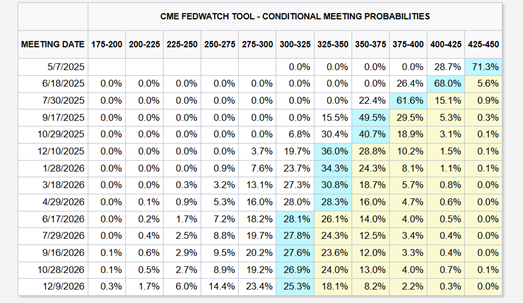

Fed could implement up to four rate cuts due to potentially “higher inflation and slower growth”

Analysts surveyed by CME Group suggest the Federal Reserve could implement up to four rate cuts in 2025, potentially driven by higher inflation and slower growth resulting from trade tariffs. Should this materialise, the federal funds rate could fall to between 3.25% and 3.50%. This could lead to a further moderation in mortgage interest rates which will help ease housing costs.

Chart 2: Analysts view on probabilities of changes to the Fed rates

Source: CME FedWatch

-

Construction cost may ease with cheaper imports ahead as demand slows

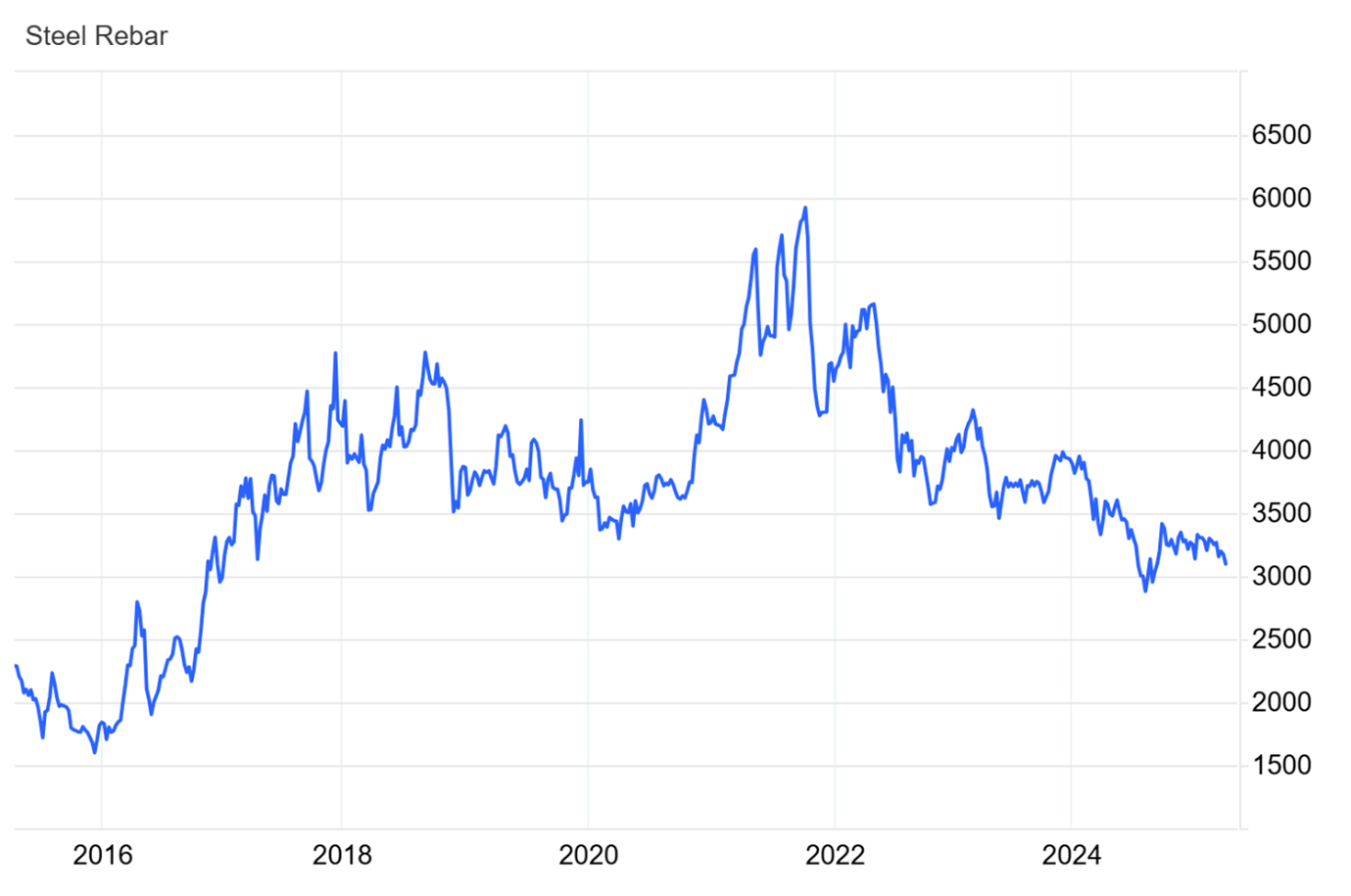

The region may face significant deflationary pressures if China decides to divert its export surpluses and flood the market with cheaper exports. Specific to the construction sector, the slowdown in China’s real estate market has led to weaker domestic demand and softer prices for steel rebar. The 25% US import tariffs are a double whammy on steel demand and could further dampen export demand for Chinese producers.

There could be a risk of a flood of cheaper steel exports in the region, driving down construction material costs. Could this mark the beginning of moderating construction material costs, thereby helping to ease housing prices? Although this might seem plausible, moderating construction costs ahead could have muted impact on housing prices, since Singapore home prices are influenced by a variety of factors including land and labour cost.

Chart 3: Steel Rebar Prices on a steady decline since late 2021 on the back of sluggish demand

Source: tradingeconomics.com

-

Singapore’s safe haven status could continue to attract foreign investments seeking growth in the region, ensuring job opportunities which can support driving housing demand

The imposition of trade tariffs is set to effectively curb the ‘China Plus One’ strategy, which is widely adopted by companies to reduce reliance on China and mitigate the impact of the trade war. Consequentially, many of the regional low-cost manufacturing hubs could face challenges due to higher trade tariffs.

Singapore, however, maintained a balanced and mutually beneficial partnership with the United States, as reinforced by the U.S. goods trade surplus with Singapore, which stood at US$2.8 billion in 2024. This underscores our position as a trusted trade ally and has likely shielded us from harsher tariff measures.

Investors in the region seeking safe havens and growth could look to Singapore, drawn by it’s relative stability, transparent and open economy. This could drive a steady influx of Foreign Direct Investment (FDI) which is instrumental in supporting job opportunities and contribute to the overall economic development of Singapore. This in turn could support demand for residential and commercial properties in Singapore. Singapore’s status as a financial hub and its robust legal framework further enhances its attractiveness in times of economic uncertainty.

Chart 4: Steady increase in Foreign Direct Investment

Source: Singstat, ERA Research and Market Intelligence

-

Singapore’s diversified economy and extensive multilateral trade partners can help mitigate economic shocks

Singapore’s diversified economy and broad network of trade partners will mitigate the impact of individual countries’ trade tariffs. Till date, Singapore has 27 free trade agreements and will continue to pursue and uphold open, fair, and free trade among like-minded countries.

-

Proactive cooling measures in the residential market provide flexibility to navigate against external shocks

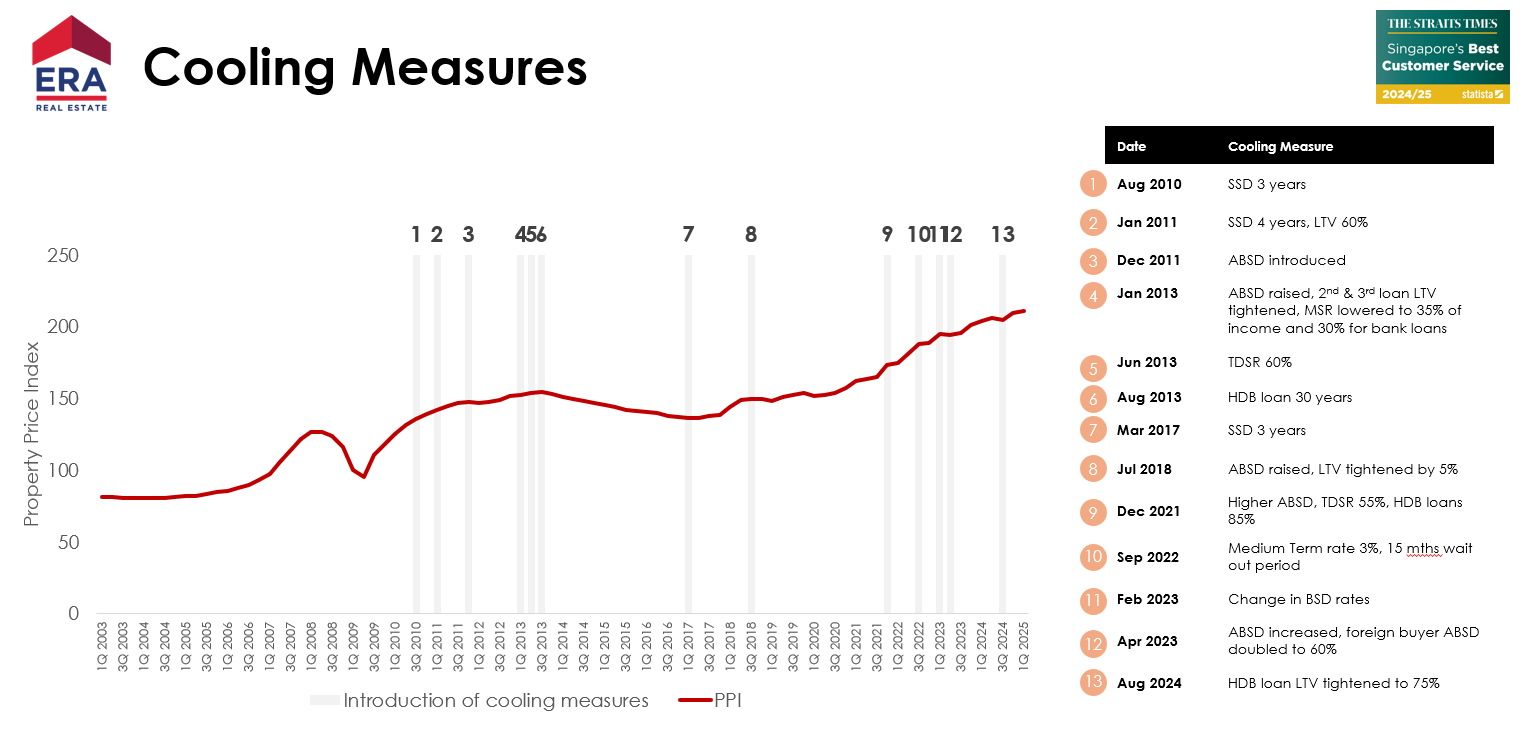

Between 2010 and 2024, the Singapore government introduced 13 rounds of cooling measures aimed at maintaining a stable residential market and ensuring sustainable price growth.

These measures included the significant 60% Additional Buyer’s Stamp Duty (ABSD) implemented in April 2023, targeting speculative investment from foreign buyers. Additionally, the higher Additional Buyer’s Stamp Duty (ABSD) on second homes is intended to discourage accumulation of multiple properties, helping to moderate home price growth and maintain market stability. All of this contributes to sustaining the intrinsic value of residential properties in Singapore.

Chart 5: Cooling Measures for Singapore Residential Market

Source: URA, HDB, MND, ERA Research and Market Intelligence

In conclusion

There you have it – and this is why ERA maintains a positive medium- to long-term outlook for Singapore’s residential market, even in the face of global headwinds.

Much of the groundwork has been laid by our government prior. This includes establishing extensive free trade agreements, developing sophisticated infrastructure, and nurturing a highly educated workforce. These efforts form a firm foundation that continues to attract sustained foreign investment, a key driver of Singapore’s long-term economic growth, as well as creating job opportunities.

When it comes to housing, the government takes a pragmatic approach to keep pace with demand, while being careful to discourage excessive accumulation of property assets for speculative purposes. Instead, the focus remains deeply rooted in ensuring that homes stay accessible for Singaporeans through sustainable price growth. Furthermore, the multiple rounds of cooling measures offer plenty of room for the government to respond swiftly should the property market face external shock.

In summary, Singapore’s property market is built on a foundation of resilience, foresight, and prudent governance. ERA believes that with sustained policy support and strong demand drivers, Singapore’s residential market will continue to present resilient growth potential and long-term value for both homeowners and investors.

Disclaimer

This information is provided solely on a goodwill basis and does not relieve parties of their responsibility to verify the information from the relevant sources and/or seek appropriate advice from relevant professionals such as valuers, financial advisers, bankers and lawyers. For avoidance of doubt, ERA Realty Network and its salesperson accepts no responsibility for the accuracy, reliability and/or completeness of the information provided. Copyright in this publication is owned by ERA and this publication may not be reproduced or transmitted in any form or by any means, in whole or in part, without prior written approval.

下文由ERA公关经理岳开新翻译

拥有一套公寓是许多本地人的追求,购房者被其良好设施、现代化便利以及黄金地段所吸引。尽管购房成本不菲,但其潜在的回报通常能证明其物有所值。

2024年,私宅价格指数持续稳步上升,全年同比增长3.9%。一方面,这意味着购房者的入场成本更高,但同时也表明市场依然活跃,未来的投资回报前景乐观。

为了验证这一趋势,并考虑到 卖方印花税(SSD) 的影响,我们筛选出了 2024 年盈利交易量最高的公寓项目,这些项目的持有期均不超过 四年。

以下是去年各个地区利润最高的公寓数据。

核心中央区(CCR)利润最高的项目

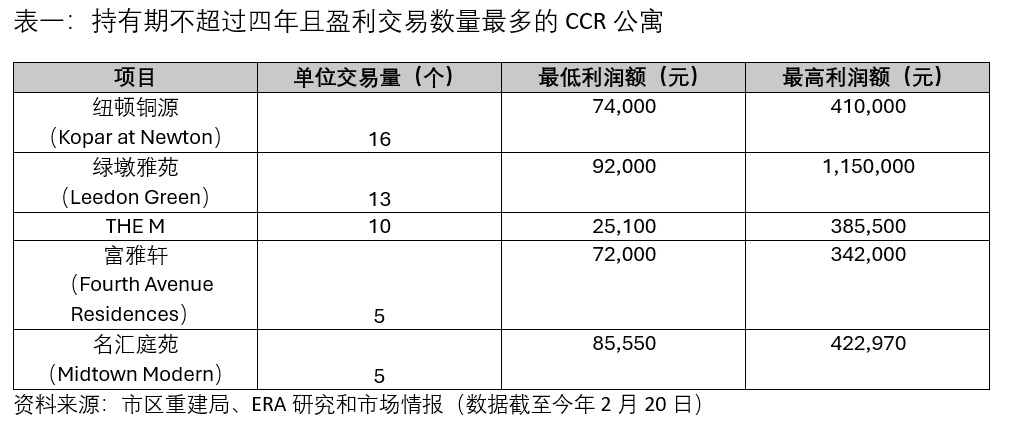

#1:纽顿铜源

CCR中排名第一的是纽顿铜源,这座豪华公寓位于第9邮区,去年共有 16 笔盈利交易。由于该项目 2023 年刚获得临时入伙准证(TOP),在转售市场上更具吸引力,特别受到 偏好全新即刻入住 的买家青睐。

这一趋势也在数据中得到验证:16 笔盈利交易中,有 10 笔为楼花交易(sub-sale),表明买家愿意支付额外溢价,以换取即刻入住的便利。

#2:绿墩雅苑

紧随其后的是绿墩雅苑,共 13 笔盈利交易。这些交易全部为楼花交易(sub-sale),因为项目已于 2023年第四季获得TOP。

项目的亮点不仅仅是交易量,其中 一个四卧房单位(带私人电梯,1496 平方英尺)更是 创下了 CCR 最高盈利纪录,利润达 115 万元。

此外,绿墩雅苑的 最低盈利单位利润(9万2000 元) 也高于其他项目。这可能因项目的位置位于绿墩岭(Leedon Heights)高端住宅区,并且属于永久地契。

#3: The M

排名第三的是The M,这个99年地契的高端综合开发项目位于密陀路(Middle Road),去年共录得 10 笔盈利交易。

The M 的价格增长主要因其优越的地理位置和便利性,项目坐落在第7邮区,靠近武吉士(东西线、滨海市区线)、政府大厦(南北线、东西线)和滨海中心(环线)三大核心地铁站。

此外,The M 还受益于政府推动武吉士地区转型的政策,使其成为中央商务区延伸区的一部分,这进一步提升了项目的吸引力。

值得一提的是,第7邮区近年来迎来了多个新项目,为地区注入了活力。例如,双景岭(Duo Residences)和 City Gate 等优质项目,这也有助于The M 自 2020年推出以来 的价格增长。

其他中央区(RCR)利润最高的项目

#1: Penrose

PENROSE 位于 第 14 邮区,去年共录得 98 笔盈利交易,成为 RCR 表现最亮眼的公寓项目。该项目位于 沈氏通道(Sims Drive),靠近 巴耶利峇A(Paya Lebar)商圈。

Penrose 的强劲盈利能力得益于近五年前具有竞争力的开盘价格。2020年,第14邮区新项目的中位数单位价格约为 每平方英尺1666元,而 Penrose 的开盘价格仅为每平方英尺1547元,这一价格优势为早期买家提供了更大的升值空间。随着整体房价上涨,他们也享受了更高盈利。

此外,Penrose 靠近阿裕尼(Aljunied)地铁站,再加上“活力加冷总蓝图”(Kallang Alive Master Plan) 规划带来的潜在升值空间,让这个项目未来的增长前景更加看好。

#2:鑫悦府

鑫悦府是去年 RCR 表现第二佳的公寓项目,共有 60 笔盈利交易。这主要因其强劲的租赁投资潜力以及综合型大型开发项目的定位。

除了 1862 套私宅单位,鑫悦府还有 八个商业单位,这为居民提供了便捷的生活设施,提升了整体居住体验。

租赁吸引力方面,项目靠近多个重要商业区,其中包括科学园(Science Park)、丰树商业城(Mapletree Business City)、纬壹(one-north),这里是集生活、工作、娱乐和学习于一体的未来产业园区。

这些因素共同增加了鑫悦府的租赁需求及长期投资价值,使其成为 RCR 区内最具吸引力的项目之一。

#03 顺福轩

顺福轩在2024年以54笔盈利交易名列三甲。这个99年地契的项目位于顺福路(Shunfu Road),于 2023年获得TOP。

除交易量突出外,项目在今年 1月也因一笔创纪录的顶层单位(Penthouse)交易登上本地新闻头条,该单位为卖家带来了 440 万元 的惊人利润。此外,一个 2098 平方英尺的五卧房豪华单位也在转售交易中获得106 万元的可观收益。

顺福轩一系列的高盈利交易,再加上优越的地理位置,如靠近玛丽蒙( Marymount) 和 汤申上段(Upper Thomson) 地铁站,以及碧山—汤申(Bishan-Thomson)区域),使项目成为RCR 最具投资价值公寓之一。

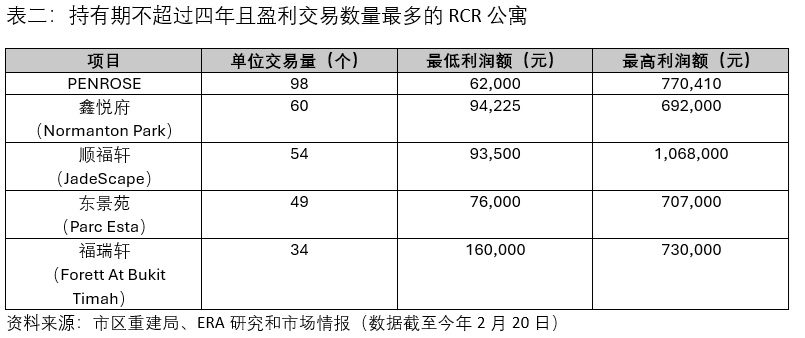

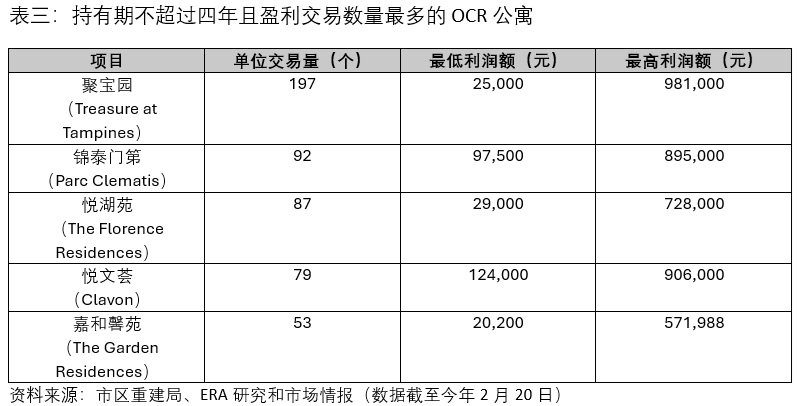

中央区以外(OCR)利润最高的项目

#1: 聚宝园(Treasure at Tampines)

因聚宝园是新加坡霸级规模私宅之一,共2203 个单位,所以去年获得 OCR 最高的转售交易量并不令人意外。其中,有197 笔交易实现盈利,利润介于 2万5000元 至 98万1000元。

这座 99年地契的私宅位于 淡滨尼巷(Tampines Lane),地理位置优越,毗邻多个重要设施和交通要道,其中包括淡滨尼圆巴刹与熟食中心(Tampines Round Market & Food Centre)、泛岛高速公路(PIE)和淡滨尼南高架桥(Tampines South Flyover)。

此外,聚宝园的便利性进一步提升了房价的增值潜力。居民可以方便前往淡滨尼广场(Tampines Mall)、世纪广场(Century Square)和东福坊(Eastpoint Mall),这些商场距离公寓仅约 1 公里,为他们提供了丰富的购物、餐饮和娱乐选择。

#2: 锦泰门第(Parc Clematis)

尽管锦泰门第位于西部的第5邮区,地理位置上与东部第18邮区的聚宝园几乎成犄角之势*,但它们的多个相似处,推动其房价增长。

首先,锦泰门第作为霸级项目,同样受益于规模优势。公寓拥有1450 个单位,这类大型项目通常有更高的交易量,从而可推动房价稳定上涨。

此外,锦泰门第优越的地理位置 也是吸引买家的重要因素之一。项目邻近多个设施,其中包括金文泰地铁站、金文泰广场(Clementi Mall)、NEWest、君超广场(Grantral Mall)。

同时,项目也靠近亚逸拉惹高速公路(AYE),出行便捷,可快速抵达莱佛士坊(Raffles Place)、珊顿道(Shenton Way)及滨海湾金融区(Marina Bay Financial District)等重要商业中心。

#3: 悦湖苑

榜单中前两名均为霸级项目,位居季军的悦湖苑 也不例外,共1410 个单位,原址曾是中等入息公寓(HUDC)Florence Regency,它于2014年私有化,并于2017年集体出售。

悦湖苑 距离后港地铁站仅约 600 米,步行 约5 分钟,预计这可让项目在即将到来的 跨岛线(Cross Island Line,简称CRL)中受益。

当 跨岛线第一阶段于2030年通车后,后港地铁站将成为换乘枢纽,连接 跨岛线与东北线(North-East Line,简称NEL),这将极大提升悦湖苑居民出行的便利性,同时,提高其长期增值潜力。

我们可从上述盈利交易中了解到什么?

对这些按盈利交易项目进行深入分析,可以得出以下几个重点:

首先,即使持有期较短(四年或以下),房产仍能带来可观回报。

这一趋势在刚获得TOP的私宅中表现的尤为明显。这些房产可立即入住且全新,吸引了大量买家,从而推动了更高的盈利交易量。

这种现象在其他地区也均有所体现,去年盈利的转售项目中,楼花交易比例高于普通转售交易,进一步印证了新TOP项目的投资吸引力。

其次,同一地区中,大型综合开发项目(Mega Developments)在价格增长方面往往优于中小型项目。

这主要是两个关键因素:大型综合开发项目可提供的多样化户型选择以及庞大的单位供应量,这通常会产生更多的交易,从而带动销售,并实现更高的资产增值。

那么,如果您正在考虑在大型综合开发项目中购置新房,或者计划在 2025 年购买任何新推出的项目,欢迎查看我们整理的2025 年新楼盘详情。

此外,您也可以随时联系 ERA Trusted Advisor,获取量身定制的房产推荐,满足您的住房需求和偏好!

本文件中的信息仅供参考,不构成对信息的准确性、完整性或可靠性的保证。使用者应自行核实相关信息,并根据具体情况向独立的专业人士(如估价师、财务顾问、银行从业人员及律师)寻求专业意见。ERA及其销售人员对于因使用本信息而导致的任何直接或间接损失概不负责。此外,本文件受著作权法保护,ERA拥有其著作权。未经事先书面许可,任何个人或机构不得以任何形式或手段对本文件进行复制、传播或用于商业用途。