4Q 2025 HDB Quarterly Report: Moderate Sales Close Out the Year on a Stable Note

- Ethan Hariyono and Stanley Lim

- 4 min read

- Research

- 2 Jan 2026

Figures are based off the official flash estimates for HDB quarterly statistics, released on 2 January 2026. Other supplementary data based on data.gov.sg as of 30 December 2025.

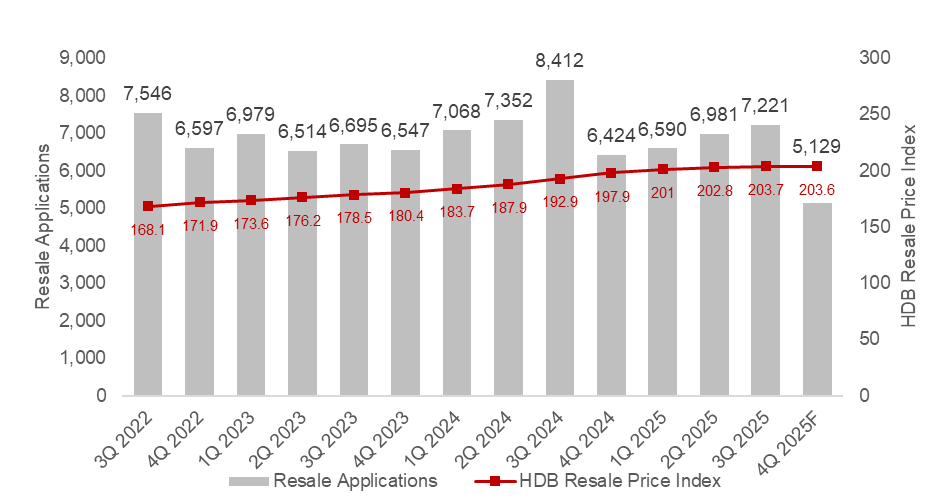

In 4Q 2025, the HDB Resale Price Index (RPI) stayed flat quarter-on-quarter (q-o-q), remaining largely unchanged at 203.6 from 3Q 2025’s figure of 203.7. Simultaneously, a total of 5,129 resale transactions were registered over the quarter, representing a 28.3% q-o-q decline over the 7,157 cases recorded in 3Q 2025.

Resale Price Index (RPI) Stays Flat Amid Holiday Season

With the HDB RPI holding steady at 203.6 in 4Q 2025, this marks the first time since 2020 that resale prices have remained unchanged across quarters. This also puts full-year growth at 2.9% for the HDB RPI, which is noticeably slower than the 9.7% year-on-year (y-o-y) uptick observed in 2024.

Despite marking the slowest price growth since 2019, this outcome still aligns with ERA’s full-year forecast of 3-6% for 2025.

Chart 1: HDB RPI vs Number of Transactions

HDB Resale Transactions Moderate in Tandem with SBF Launches

For 4Q 2025, a total of 5,129 HDB flats were sold on the resale market, bringing the full-year figure to 26,042 transactions. This marks a 29.0% q-o-q decline from the 7,221 registered cases in 3Q 2025, as well as a 10.2% y-o-y downtick in resale volume from the 28,986 transactions in 2024.

This decline was largely due to competing supply from additional Sales of Balance Flats (SBF) exercises and a smaller pool of flats reaching their Minimum Occupation Period (MOP) in 2025.

This year, two SBF exercises were launched – one in February and the other in July following its initial announcement during Budget 2025. February’s SBF exercise was also notably the largest to date, offering 5,590 flats.

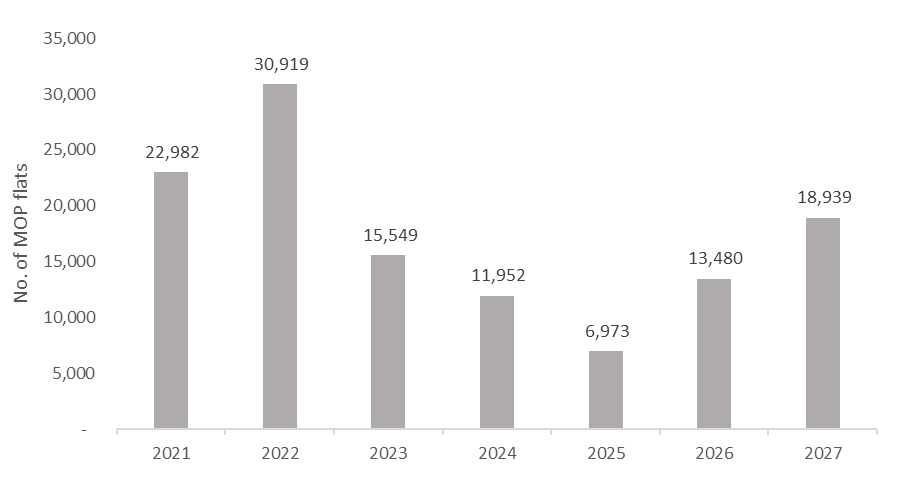

At the same time, MOP flat volume fell to 6,973 units this year. This supply of MOP flats is also the lowest in 11 years, since 2014, when only 5,301 units became available on the resale market.

Smaller MOP Flat Supply Keeps Resale Market Moderated

With only 6,974 HDB flats fulfilling their MOP in 2025, this puts pipeline supply for the resale market at its lowest level since 2014 when 5,301 units completed their MOP.

This has helped to sustain resale price growth throughout the year, particularly within centrally-located, mature estates. However, with a projected doubling of MOP supply to 13,480 units in 2026, buyers may reasonably expect some relief.

Chart 2: Number of MOP Flats by year

Table 1: Distribution of MOP Flats by Town in 2025

| Town | MOP flats | % |

| Punggol | 1,794 | 25.7% |

| Toa Payoh | 1,258 | 18.0% |

| Bukit Batok | 1,113 | 16.0% |

| Queenstown | 809 | 11.6% |

| Ang Mo Kio | 590 | 8.5% |

| Tampines | 527 | 7.6% |

| Clementi | 385 | 5.5% |

| Bedok | 215 | 3.1% |

| Yishun | 156 | 2.2% |

| Choa Chu Kang | 126 | 1.8% |

| Total | 6,973 | 100.0% |

Source: data.gov.sg, ERA Research and Market Intelligence

Among the flats reaching MOP in 2025, 30% of them are in popular, centrally located housing estates such as Toa Payoh and Queenstown, which tend to command higher resale prices. They are popular among buyers, since they are not subject to the more stringent resale restrictions under the new “Plus” and “Prime” classification.

Uptick in Million-Dollar Flat Transactions Persists

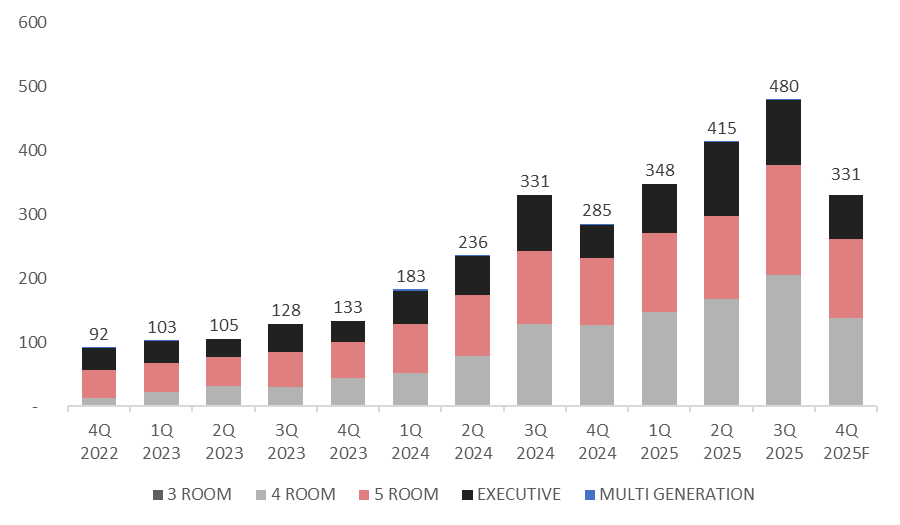

In 4Q 2025, a further 331 million-dollar flat transactions were recorded up to 30 December 2025. While this represents the lowest quarterly tally in 2025, this still sets a new record high of 1,574 million-dollar HDB transactions for the full year. This figure is also approximately 52.1% higher than the previous peak of 1,035 units seen in 2024.

Nonetheless, the HDB resale market remains affordable, with the majority of transactions (73%) taking place below the $750,000 mark in 2025. Additionally, million-dollar flat sales made up only 6.9% of all transactions observed in 4Q 2025.

Chart 3: HDB Flat Transactions over $1m

These higher-value transactions remained concentrated in mature estates, which accounted for around 91% of all million-dollar deals over 4Q 2025.

In addition, over half (52.4%) of million-dollar deals in the year (up to 30 December 2025) involved newer flats aged 15 years or below. This reflects ongoing demand for newer HDB homes in centrally-located, mature estates.

Overall HDB Prices Remain Affordable

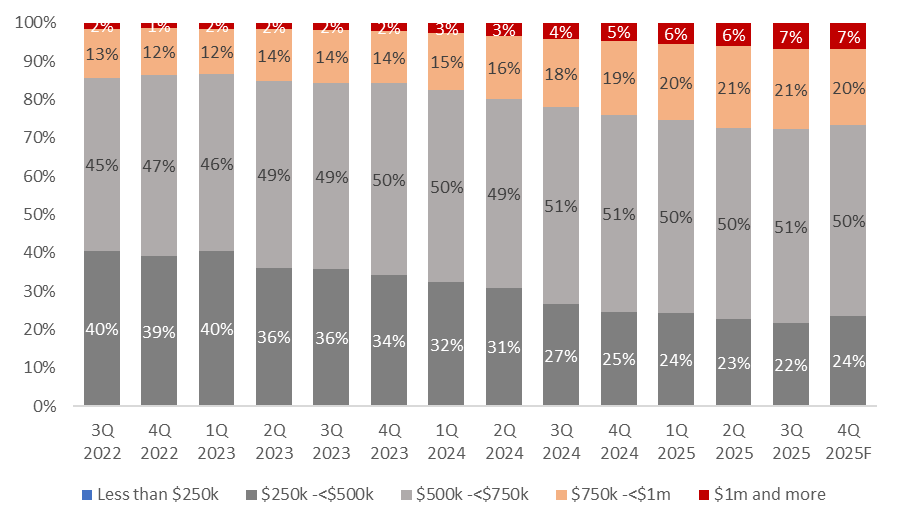

Chart 4: HDB Transactions by Price Ranges

In 4Q 2025, half of all HDB transactions fell within the $500,000 to $750,000 range, which is considered to be affordable for many local buyers. Meanwhile, an additional 24% of resale HDB flats transacted during the quarter were priced between $250,000 to $500,000.

Collectively, this indicates that nearly three-quarters of HDB resale transactions remain affordable for the average homebuyer.

ERA’s Outlook and Forecast for 2026

Table 2: ERA forecast of HDB Resale Market

2024 | 2025 (Flash) | 2026F | |

| Resale Price Index at 4Q | 197.9 | 203.6 | + 2% - 5% y-o-y |

| Resale Volume | 27,023 | 5,129 | 26,000 to 27,000 |

Source: URA, ERA Research and Market Intelligence

In 2026, we expect the wider resale HDB market to see around 26,000 to 27,000 transactions, with price growth ranging from 2% to 5%. This aligns with the Singapore government’s aim for a stable and sustainable public housing market.

I confirm that I have read theprivacy policy and allow my information to be shared with this agent who may contact me later.