4Q 2025 URA Private Residential Report: Year-End Dip After Strong 3Q, Firm Outlook for 2026

- Egan Mah and Kwong Seong Ping

- 10 min read

- Research

- 2 Jan 2026

Figures are based off the official flash estimates for URA quarterly statistics, released on 2 January 2026.

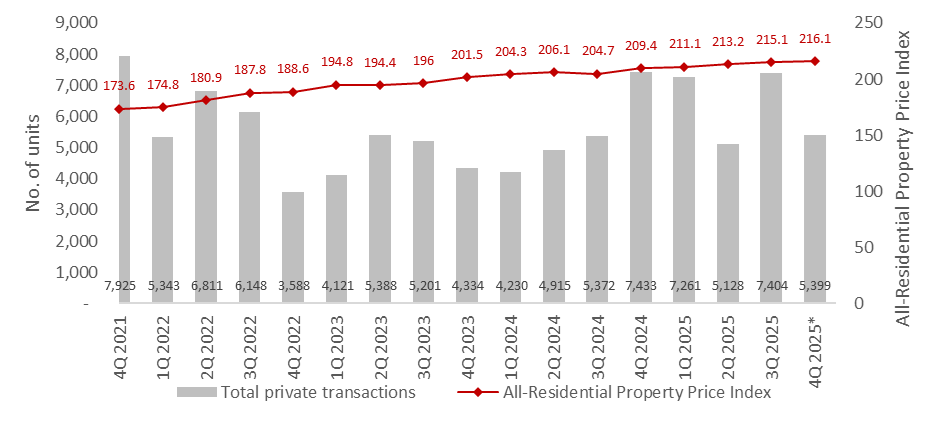

According to flash estimates released by the Urban Redevelopment Authority (URA) for 4Q 2025, the All-Residential Property Price Index rose modestly by 0.7% quarter-on-quarter (q-o-q). Based on caveat data as of 29 December 2025, total transaction volume of private homes decreased by 27.1% q-o-q to 5,399 transactions from 7,404 transactions registered in 3Q 2025.

Chart 1: All-Residential Property Price Index and Total Private Transaction Volume

Source: URA, ERA Research and Market Intelligence

*Based on flash estimates and URA caveat data as of 29 December 2025

The overall non-landed private property price index fell by a marginal by 0.1% q-o-q to 208.3 in 4Q 2025. This was largely due to the higher base effect in 3Q 2025, which saw a bumper slate of new launches.

- The Core Central Region (CCR) non-landed price index registered the sharpest decline, reflecting a 3.2% q-o-q fall. This is largely due to a higher base, as 3Q 2025 saw a sharp 1.7% increase.

- The Outside Central Region (OCR), which grew by a further 1.0% q-o-q, extending the 0.8% from 3Q 2025. Meanwhile, the Rest of Central Region (RCR) saw a 0.7% q-o-q increase in corresponding prices.

The Landed property price index rose 3.5% q-o-q, extending the uptick from the previous quarter, supported by stronger demand from condo upgraders.

However, as buyers gravitated towards new launches, resale and sub-sale activity in the secondary market softened during the quarter.

With an additional 4,575 private residential units in the 1H 2026 GLS Confirmed List, the fresh supply will continue to reinforce the Government’s aim to stabilise land prices and maintain a steady flow of new homes over the coming years.

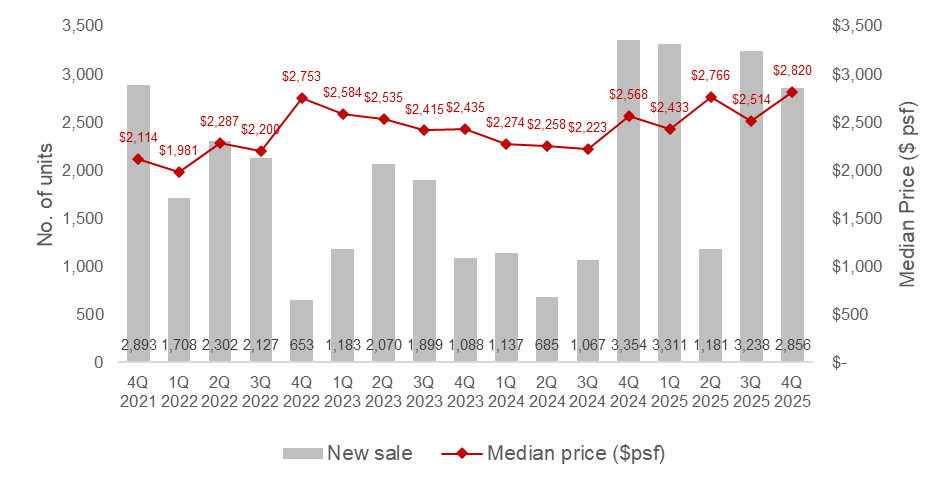

New Sale (Non-Landed Homes, Excluding ECs)

According to caveats as of 29 December 2025, new sale transactions saw a decline of 12.6% q-o-q to 2,856 units in 4Q 2025. This steep decline came on the back of fewer launches, with five developments launched compared to nine in 3Q 2025. Despite the decline, 4Q 2025 sales performance was still exceptional, carrying the strong sales momentum from the previous quarter.

This takes the total new home transactions to 10,611 units in 2025, surpassing 2024’s full-year tally of 6,469 units. Strong new home demand was underpinned by locations that had either experienced a pause in new supply or welcomed their inaugural project.

Non-landed CCR prices recorded a steeper decline of 3.2% q-o-q, mainly reflecting the higher pace of growth in 3Q 2025. The previous quarter’s 1.7% increase was supported by four CCR launches, compared with just one in 4Q 2025. Nonetheless, the strong sales momentum carried into this quarter, with Skye at Holland - the sole CCR launch in 4Q 2025 - performing exceptionally well.

Chart 2: New Sale Transactions and Median Price for Non-Landed Homes (excluding ECs)

Source: URA as of 29 Dec 2025, ERA Research and Market Intelligence

In total, five new launches debuted in 4Q 2025. The four launches in October 2025 achieved take-up rates of over 80% on their respective launch days. Tighter supply arising from fewer new home completions in 2025 led to spillover demand into the primary market. In addition, easing interest rates and rising HDB prices have strengthened buyers’ financial capacity to enter the private residential market. As a result, strong sales momentum is likely to carry into 2026.

Table 1: List of new launches in 4Q 2025

Source: URA and ERApro as of 29 Dec 2025, ERA Research and Market Intelligence

The Central Region continues to take Centre Stage

Four of the five new launches in 4Q 2025 were in the Central Region (CCR and RCR). This followed the trend of the previous quarter when four CCR and three RCR developments were launched.

The strong market conditions in 3Q 2025 gave buyers the confidence to commit to higher-valued homes, including those in the Central Region, despite higher prices. At the same time, rising new home prices and strong take-up rates in other regions made city-fringe and central locations increasingly compelling. This helped drive the strong performance of projects such as Skye at Holland, Penrith and Zyon Grand.

Skye at Holland combines a prime CCR location near an MRT station with convenient access to amenities, all at a palatable price point, with median transaction prices of $2,948 psf recorded in 4Q 2025. Its balanced proposition of attractive pricing, family friendly layouts and a strong location that supports a steady exit strategy drove robust demand. As a result, Skye at Holland sold the highest number of units during the quarter and emerged as the best-selling project of 2025, with 99.4% of units sold.

It has been more than five years since the last condominium launch in the vicinity of Queenstown MRT Station, making the highly anticipated launch of Penrith particularly appealing to buyers. Queenstown is also home to a sizeable stock of high-value HDB flats that fetch strong resale prices, which likely contributed to the pool of buyers. This, in turn, underscores a strong exit strategy for future investment buyers.

Zyon Grand, the latest launch among the cluster of GLS sites around River Valley/Zion Road, achieved a commendable take-up rate of over 86.0% since its launch in October 2025. As an integrated development near the city centre, it offers highly efficient unit layouts, while higher floor units offer panoramic views of Singapore’s city skyline. Despite the median price psf crossing the $3,000, buyers are undeterred as these factors strongly appeal to them.

The Sen, located in Upper Bukit Timah, has seen 24.2% of its units sold since launch. The project is primarily geared towards owner-occupiers, who typically take more time to assess layouts, orientation, and long-term suitability, before making a new purchase, which explains the measured yet healthy sales pace.

Faber Residence, the only OCR launch of 4Q 2025, saw robust sales performance

Faber Residence, the sole OCR launch in 4Q 2025, is located in the well-established Clementi town. As a low-rise, low-density development within a landed-housing enclave, it is well-suited for families seeking a private and tranquil living environment. Furthermore, its strong focus on liveability, with functional spaces and efficient floor plates, is a strong draw for buyers accustomed to larger living spaces.

The project sold at a median price of $2,149 psf, which was at a much more palatable price range compared to the other projects that launched in the month. Furthermore, it was the only OCR condo launched in the West region since Elta earlier in the year, and the last OCR launch that we will see until 2026, which could have drawn in a crowd of more price-sensitive buyers. It achieved a sales rate of 86% during its launch and have sold 91% of its 399 units till date.

Executive Condominium (EC)

With no new EC launches, new EC sales fell to 426 units in 4Q 2025, representing a 58.3% q-o-q decline. This is in contrast to 3Q 2025, which saw the launch of Otto Place in Bukit Batok. Till date, the 98.9% of the development has been sold, with just seven units available. Island-wide, the available EC stock has continued to tighten, with just these seven units at Otto Place remaining.

Despite rising prices and a larger down payment required due to the tighter 30% Mortgage Servicing Ratio (MSR) and $16,000 income ceiling, ECs still present value buys in the market when compared to private properties. Unlike private homes, EC remains attractive to HDB upgraders who can benefit from the deferred payment scheme if required and are not subject to the ABSD.

This tightening supply is expected to shift buyer attention to the upcoming EC launches in 1Q 2026. Coastal Cabana at Jalan Loyang Besar and Rivelle Tampines, will collectively introduce 1,320 units to the market. While both developments are in the east, buyers looking for ECs in other regions will likely have to wait till end-2026 for other upcoming launches in Sembawang, Woodlands and Senja Close.

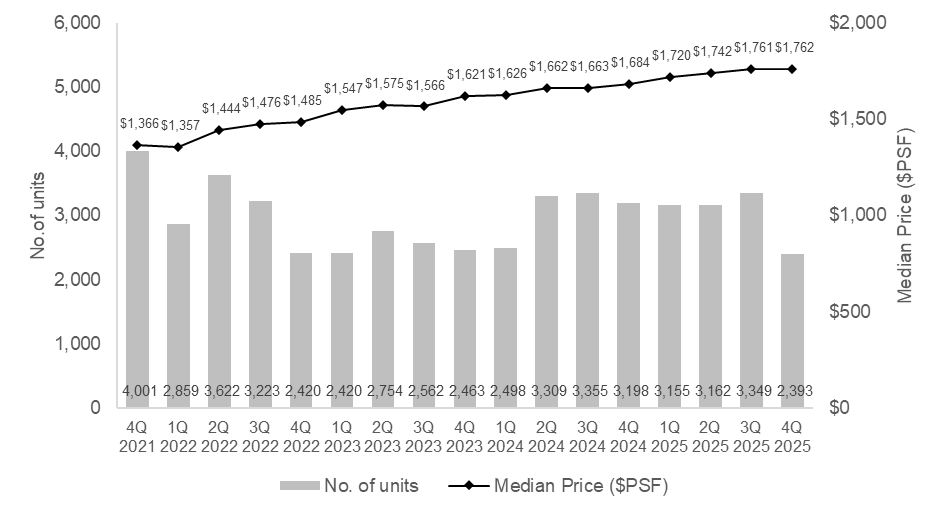

Resale and Sub-Sale (Non-Landed Homes, Excluding EC)

In 4Q 2025, resale transactions for non-landed private homes (excluding ECs) fell 28.5% q-o-q to 2,393 units. This is the lowest number since 2Q 2022 and marks a deviation from the relatively consistent trend of resale transaction volumes of around 3,000 units per quarter observed over the past six quarters.

Buyer attention shifted away from the resale market, largely due to the bumper pipeline of new home launches in desirable locations, which offered buyers a wider range of choices.

Chart 3: Resale Transactions and Median Price for Non-Landed Homes (excluding ECs)

Source: URA as of 29 Dec 2025, ERA Research and Market Intelligence

In contrast to the downtick in transaction volume, median unit prices for resale non-landed private properties (excluding ECs) rose slightly to $1,762 psf in 4Q 2025 from $1,761 psf in 3Q. This measured rise reflects stable growth in the segment. It also continues the upward momentum observed [WS1] since 4Q 2023.

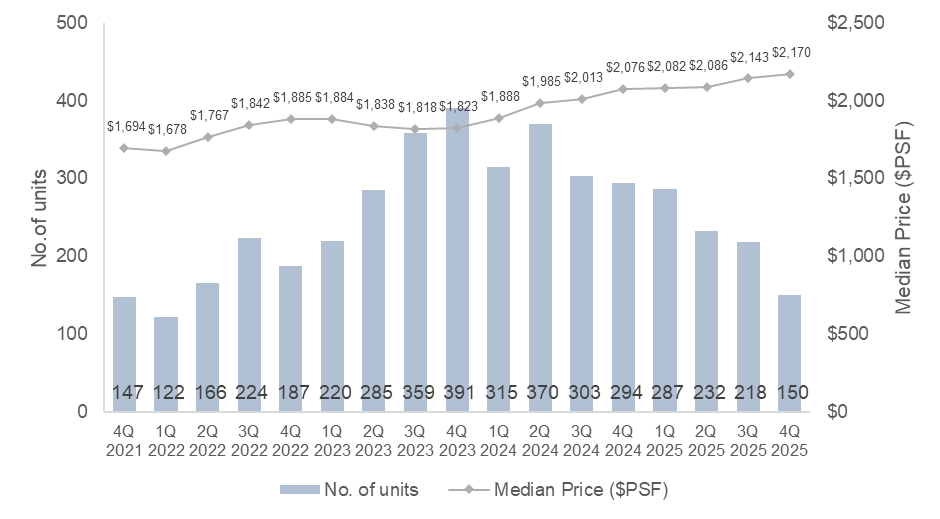

Chart 4: Sub-Sale Transactions and Median Price for Non-Landed Homes (excluding ECs)

Source: URA as of 29 Dec 2025, ERA Research and Market Intelligence

Within the sub-sale segment, transaction volumes fell by a further 31.2% q-o-q to 150 deals based on caveat data. This translates to sub-sales accounting for 2.8% of all non-landed private property (excluding ECs) deals made in 4Q 2025.

Full-year private home completions (excluding ECs) are projected to reach 5,249 units by end-2025, down from 8,460 units in 2024. This decline is the primary factor behind falling sub-sale transactions, which have been on a steady downward trend since 2Q 2024.

On the other hand, the median unit price for sub-sales rose 1.3% q-o-q to $2,170 psf. This uptick likely resulted from a higher proportion of sub-sale transactions in the OCR (67 units) and RCR (70 units). Together, transactions in the OCR and RCR made up 91.3% of all sub-sale activity for 4Q 2025, while the CCR accounted for a smaller share of 8.7% (13 units). Buyers of CCR properties may have turned towards new launches due to their attractive price and longer remaining tenures.

The most popular recently completed developments in 4Q 2025 were Normanton Park (RCR, 25 units), The Watergardens At Canberra (OCR, 15 units) and Penrose (RCR, 10 units).

Market Outlook

The dip in transactions in 4Q 2025 was largely due to the stellar performance seen in 3Q 2025 and the seasonal year-end lull. Developers typically postpone launches in December, when buyers travel during the holiday season. This moderation does not signal a softening market but rather reflects a seasonal pause.

Within the secondary market, it is expected that resale and sub-sale transactions will continue to moderate as a shrinking number of fresh completions continues to weigh on available supply. Additionally, the robust pipeline of upcoming projects has correspondingly diverted buyer demand from the resale and sub-sale markets.

2025 was a strong year for Singapore’s private residential market, underpinned by resilient demand, steady economic conditions and renewed confidence as global risks eased. Attention now turns to the extent to which this momentum can be sustained into 2026.

In 2026, the private residential market is expected to remain resilient, with moderate price growth supported by strong owner-occupier demand and ongoing right-sizing trends. Buyers can look forward to a pipeline of 19 private residential projects, and 5 EC launches slated for the year. While this is fewer than 2025, which saw 24 private developments and 2 EC launches, overall homebuying demand is expected to remain healthy.

Barring any unforeseen circumstances, ERA Singapore projects new home sales to be between 9,000 to 10,000 units, while the secondary market is expected to record 13,000 to 14,000 transactions, pointing to stable underlying demand in the year ahead.

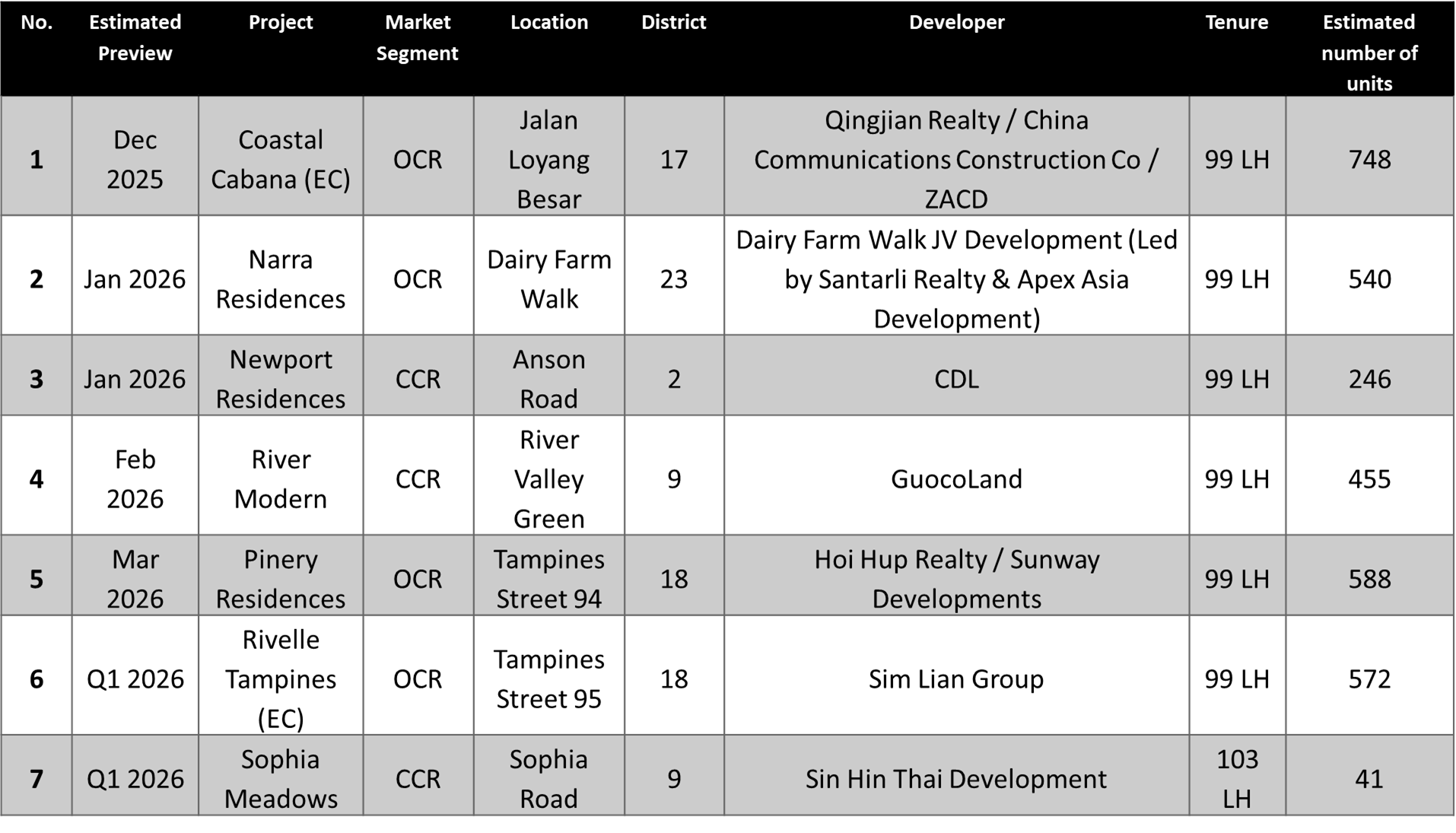

Table 2: Upcoming launches in 2025/1Q 2026

Source: ERA Project Marketing

I confirm that I have read theprivacy policy and allow my information to be shared with this agent who may contact me later.